Das könnte Ihnen auch gefallen

- AcademyCloudArchitecting Module 01Dokument36 SeitenAcademyCloudArchitecting Module 01Kaichun YauNoch keine Bewertungen

- Regional Rural Banks of India: Evolution, Performance and ManagementVon EverandRegional Rural Banks of India: Evolution, Performance and ManagementNoch keine Bewertungen

- Project Report On PNB Home LoanDokument43 SeitenProject Report On PNB Home Loangunpriya75% (4)

- Gauhati University: G.U. Registration No. 003864 of 2009-2010Dokument67 SeitenGauhati University: G.U. Registration No. 003864 of 2009-2010Ruchi Sachan0% (2)

- Accountancy Model Project - XiDokument19 SeitenAccountancy Model Project - XiHana KabeerNoch keine Bewertungen

- HDFC: Bank's Focus Area, Marketing or OperationsDokument48 SeitenHDFC: Bank's Focus Area, Marketing or OperationsShubham SinghalNoch keine Bewertungen

- Securitization in India: Managing Capital Constraints and Creating Liquidity to Fund Infrastructure AssetsVon EverandSecuritization in India: Managing Capital Constraints and Creating Liquidity to Fund Infrastructure AssetsNoch keine Bewertungen

- A Project Report On HDFC and SbiDokument47 SeitenA Project Report On HDFC and SbiMminu CharaniaNoch keine Bewertungen

- Blackbook FinalDokument70 SeitenBlackbook FinalHunney MasandNoch keine Bewertungen

- Customer Satisfaction Towards HDFC BANKS AND SBI PDFDokument90 SeitenCustomer Satisfaction Towards HDFC BANKS AND SBI PDFKrishma RatheeNoch keine Bewertungen

- Role of Non-Banking Financial Institutions in IndiaDokument72 SeitenRole of Non-Banking Financial Institutions in Indiapriya33% (3)

- A Study On Financial Performance of HDFC BankDokument53 SeitenA Study On Financial Performance of HDFC BankFelix BadigerNoch keine Bewertungen

- BLACK BOOK Project1 On HDFCDokument52 SeitenBLACK BOOK Project1 On HDFCFc UkNoch keine Bewertungen

- IDBI Bank Project: Analysis of Products, Services, Financials and Customer SatisfactionDokument49 SeitenIDBI Bank Project: Analysis of Products, Services, Financials and Customer Satisfactionshweta GuptaNoch keine Bewertungen

- Analysis of Product & Services of HDFC BANK LTD.Dokument93 SeitenAnalysis of Product & Services of HDFC BANK LTD.Sami ZamaNoch keine Bewertungen

- Project Reports On Non Performing Assets NPAs in Banking IndustryDokument72 SeitenProject Reports On Non Performing Assets NPAs in Banking IndustryRajpal Sheoran67% (6)

- Kotak Mahindra Bank - India's leading private sector bankDokument9 SeitenKotak Mahindra Bank - India's leading private sector bankPrajwal KaDwad100% (1)

- Working Management of Axis BankDokument53 SeitenWorking Management of Axis BankAayushi Sharma50% (2)

- Competitive Study of Financial Institutions Offering Home Loans with Reference to ICICI BankDokument92 SeitenCompetitive Study of Financial Institutions Offering Home Loans with Reference to ICICI BankNitin Vats100% (1)

- Project ReportHDFC BANKDokument48 SeitenProject ReportHDFC BANKmonudeepakNoch keine Bewertungen

- A Study On Home Loans - SbiDokument69 SeitenA Study On Home Loans - Sbirajesh bathula100% (1)

- Retail Banking Front Office Management Activity For HDFC Bank by Nisha Wadekar This Project Is Very Useful To StudentDokument51 SeitenRetail Banking Front Office Management Activity For HDFC Bank by Nisha Wadekar This Project Is Very Useful To Studentganeshkhale7052Noch keine Bewertungen

- Analysis of The Loans and Advances: "Jivan Commercial Co-Operative Bank"Dokument59 SeitenAnalysis of The Loans and Advances: "Jivan Commercial Co-Operative Bank"VaibhavJoshi100% (1)

- Final Report On Study of Npa by Pankaj BohraDokument101 SeitenFinal Report On Study of Npa by Pankaj Bohrapankaj bohraNoch keine Bewertungen

- Sip Report On Punjab National BankDokument75 SeitenSip Report On Punjab National BankIshaan YadavNoch keine Bewertungen

- Project Cash Management in Banks ProjectDokument45 SeitenProject Cash Management in Banks Projectkedar dhuriNoch keine Bewertungen

- Synopsis On Education LoansDokument10 SeitenSynopsis On Education Loansshriya guptaNoch keine Bewertungen

- Financial Services Offered by BankDokument52 SeitenFinancial Services Offered by BankIshan Vyas100% (2)

- HDFC ProfileDokument10 SeitenHDFC ProfilePunitha AradhyaNoch keine Bewertungen

- CP of Sbi BankDokument4 SeitenCP of Sbi Bankharman singh0% (1)

- Project of Idbi AnkitaDokument71 SeitenProject of Idbi AnkitaAnamika Singh33% (3)

- Comparative Analysis On NPA of Private & Public Sector BanksDokument86 SeitenComparative Analysis On NPA of Private & Public Sector BanksNagireddy Kalluri100% (1)

- Boi ProjectDokument66 SeitenBoi Projectnitin0010Noch keine Bewertungen

- Project SbiDokument103 SeitenProject SbiShree Cyberia50% (2)

- Comercial BankingDokument84 SeitenComercial BankingSiddhesh KhotNoch keine Bewertungen

- Project Report On Banking SystemDokument16 SeitenProject Report On Banking SystemArun Kumar0% (1)

- "Financial Analysis of HDFC Bank": Symbiosis Centre For Distance Learning, PuneDokument69 Seiten"Financial Analysis of HDFC Bank": Symbiosis Centre For Distance Learning, PuneBheeshm Singh100% (1)

- A STUDY ON LOANS & ADVANCES OF STATE BANK OF INDIADokument98 SeitenA STUDY ON LOANS & ADVANCES OF STATE BANK OF INDIAShanu shriNoch keine Bewertungen

- Growth in Banking SectorDokument30 SeitenGrowth in Banking SectorHarish Rawal Harish RawalNoch keine Bewertungen

- SBI Non Performing AssetsDokument43 SeitenSBI Non Performing AssetsVikram RokadeNoch keine Bewertungen

- Study on NPAs at SBIDokument85 SeitenStudy on NPAs at SBIBasappaSarkarNoch keine Bewertungen

- MBA 4th Sem A STUDY ON BANKING OPERATIONS IN AN ECONOMYDokument42 SeitenMBA 4th Sem A STUDY ON BANKING OPERATIONS IN AN ECONOMYraghav bansalNoch keine Bewertungen

- WORKING CAPITAL OF AXIS BANKDokument84 SeitenWORKING CAPITAL OF AXIS BANKSami Zama100% (2)

- Sanjana Financial Statement ProjectDokument49 SeitenSanjana Financial Statement ProjectPooja SahaniNoch keine Bewertungen

- Project Report On Impact of NPA in The Performance of Financial InstitutionDokument96 SeitenProject Report On Impact of NPA in The Performance of Financial InstitutionManu Yuvi100% (1)

- Npa of SbiDokument40 SeitenNpa of SbiLOCAL ADDA WAALENoch keine Bewertungen

- Service Quality of HDFC BankDokument77 SeitenService Quality of HDFC BankEr Mohsin KhanNoch keine Bewertungen

- Cash Flow Project PDFDokument85 SeitenCash Flow Project PDFjakir shaikNoch keine Bewertungen

- Final NPA ProjectDokument87 SeitenFinal NPA Projectmayur ahireNoch keine Bewertungen

- Comparative Analysis On NBFC & Banks NPADokument33 SeitenComparative Analysis On NBFC & Banks NPABHAVESH KHOMNENoch keine Bewertungen

- Growth of Mutual Fund Industry in IndiaDokument77 SeitenGrowth of Mutual Fund Industry in IndiaSarah PandaNoch keine Bewertungen

- Financial Performance of HDFC BankDokument51 SeitenFinancial Performance of HDFC Bankabhasa50% (6)

- Consumer Finance..yatith Poojari (Yp)Dokument67 SeitenConsumer Finance..yatith Poojari (Yp)Yatith PoojariNoch keine Bewertungen

- The Housing Development Finance Corporation LimitedDokument13 SeitenThe Housing Development Finance Corporation LimitedshibanibhNoch keine Bewertungen

- Comparative Study of The Public Sector Amp Private Sector BankDokument68 SeitenComparative Study of The Public Sector Amp Private Sector Bankankurp68Noch keine Bewertungen

- Project Presentation On "Reverse Mortgage in India": Presenter: Shaikh Azharoddin Shakeel. Roll No.03 Mms-IiDokument17 SeitenProject Presentation On "Reverse Mortgage in India": Presenter: Shaikh Azharoddin Shakeel. Roll No.03 Mms-IiAzharNoch keine Bewertungen

- Ad New 4Dokument30 SeitenAd New 4ADITYA DHONENoch keine Bewertungen

- Corporate Salary Account Report For HDFC BankDokument42 SeitenCorporate Salary Account Report For HDFC BankShubhranshu SumanNoch keine Bewertungen

- HDFC SipDokument61 SeitenHDFC SipIndranil SarkarNoch keine Bewertungen

- Bhushan Ramekar SipDokument90 SeitenBhushan Ramekar SipAkshay ShindeNoch keine Bewertungen

- Samar's HDFC Internship Project ReportDokument61 SeitenSamar's HDFC Internship Project Reportsinghekansh1803Noch keine Bewertungen

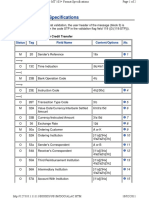

- MT 103+ Format Specifications: MT 103+ Single Customer Credit TransferDokument2 SeitenMT 103+ Format Specifications: MT 103+ Single Customer Credit Transferme Nader100% (1)

- Unit 7 Channels of DistributionDokument14 SeitenUnit 7 Channels of DistributionKritika RajNoch keine Bewertungen

- Resume Janet HeathDokument3 SeitenResume Janet Heathapi-271971026Noch keine Bewertungen

- Dematerialisation Is The Process of Converting The Physical Form of Shares Into Electronic FormDokument15 SeitenDematerialisation Is The Process of Converting The Physical Form of Shares Into Electronic FormNitin KanojiaNoch keine Bewertungen

- Cargo Manifest TrackingDokument3 SeitenCargo Manifest TrackingAchmad PurwantoNoch keine Bewertungen

- Uhf VHF Radio Arc 182Dokument10 SeitenUhf VHF Radio Arc 182wisnu septiantoNoch keine Bewertungen

- 1 Aug 22 - 27 Jan 22Dokument42 Seiten1 Aug 22 - 27 Jan 22Anurag SinghNoch keine Bewertungen

- Nma Moto AddendumDokument3 SeitenNma Moto Addendumapi-257017808Noch keine Bewertungen

- Bank Practice and Procedures (Acfn2113) : Prepared By: Tewodros EDokument37 SeitenBank Practice and Procedures (Acfn2113) : Prepared By: Tewodros Eመስቀል ኃይላችን ነውNoch keine Bewertungen

- MR - Meraki Wireless Access PointsDokument12 SeitenMR - Meraki Wireless Access PointsTerrel YehNoch keine Bewertungen

- Handout On The Pawnshop Regulation ActDokument3 SeitenHandout On The Pawnshop Regulation Actamazing_pinoyNoch keine Bewertungen

- Practical No 1Dokument4 SeitenPractical No 149 Roshni PoojaryNoch keine Bewertungen

- Chapter 7 Warehouse Operations & ManagementDokument69 SeitenChapter 7 Warehouse Operations & ManagementKhánh Đoan Lê Đình100% (1)

- Dog Concierges, LLC: Transaction Analysis and Statement of Cash Flows PreparationDokument9 SeitenDog Concierges, LLC: Transaction Analysis and Statement of Cash Flows PreparationCristina Elizabeth Portilla BravoNoch keine Bewertungen

- FormatDokument2 SeitenFormatShahid IsrarNoch keine Bewertungen

- Hotel Booking Ref-0109230128557Dokument5 SeitenHotel Booking Ref-0109230128557Sourabh BhardwajNoch keine Bewertungen

- Reliance JioDokument12 SeitenReliance JioShamsheer ShahulNoch keine Bewertungen

- DownloadDokument8 SeitenDownloadGellerteNoch keine Bewertungen

- RG-AP810-I Wi-Fi 6 Dual-Radio Access Point Datasheet - For Preview - 09270949Dokument18 SeitenRG-AP810-I Wi-Fi 6 Dual-Radio Access Point Datasheet - For Preview - 09270949takeshiyamato11Noch keine Bewertungen

- Network Devices - TutorialspointDokument6 SeitenNetwork Devices - TutorialspointThusharika ThilakaratneNoch keine Bewertungen

- Bill Statement 01 2024Dokument3 SeitenBill Statement 01 2024Satyabrat DasNoch keine Bewertungen

- JAIIB RBWM Memory Based Shift 1 2 3Dokument2 SeitenJAIIB RBWM Memory Based Shift 1 2 3Venu TarigoppulaNoch keine Bewertungen

- Question Bank (Front Office)Dokument17 SeitenQuestion Bank (Front Office)akshay ranaNoch keine Bewertungen

- ITS323Y09S1E01 Midterm Exam AnswersDokument19 SeitenITS323Y09S1E01 Midterm Exam AnswersRachel PacisNoch keine Bewertungen

- Electronic Commerce SystemsDokument48 SeitenElectronic Commerce SystemsYasir HasnainNoch keine Bewertungen

- Life Insurance ProductsDokument6 SeitenLife Insurance ProductsBharani GogulaNoch keine Bewertungen

- Trial Balance AdjustmentsDokument8 SeitenTrial Balance AdjustmentsAngel DIMACULANGANNoch keine Bewertungen

- Ta Bill FormatDokument6 SeitenTa Bill FormatHimanshu ChoudharyNoch keine Bewertungen