Das könnte Ihnen auch gefallen

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Magoosh GMAT EbookDokument116 SeitenMagoosh GMAT Ebooktellmewhour100% (1)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- Normal Procedures Airbus A320 Ver 8Dokument13 SeitenNormal Procedures Airbus A320 Ver 8SS MalikNoch keine Bewertungen

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Trading Plan TemplateDokument29 SeitenTrading Plan TemplateGeraldValNoch keine Bewertungen

- Shakespeare Sonnets ExerciseDokument2 SeitenShakespeare Sonnets ExerciseKaylee KimNoch keine Bewertungen

- Harmonic Elliott Wave RelationshipsDokument120 SeitenHarmonic Elliott Wave Relationshipsnathaniel.chrNoch keine Bewertungen

- UCA Thesis Dissertation Guide Rev. 12-8-2014Dokument43 SeitenUCA Thesis Dissertation Guide Rev. 12-8-2014nathaniel.chrNoch keine Bewertungen

- National Climate Assessment - Forest Sector Technical ReportDokument623 SeitenNational Climate Assessment - Forest Sector Technical ReportmizzakeeNoch keine Bewertungen

- David Stendahl Money Management Strategies For Serious TradersDokument46 SeitenDavid Stendahl Money Management Strategies For Serious TradersIan Moncrieffe100% (1)

- StallDokument16 SeitenStallbhalchandrak1867100% (1)

- Summary of Blended Coal FeedingDokument3 SeitenSummary of Blended Coal FeedingS V NAGESHNoch keine Bewertungen

- Introduction To HVACSystems (General)Dokument94 SeitenIntroduction To HVACSystems (General)Francis Boey100% (1)

- Depvar Indepvars Numlist Numlist: Arima - ARIMA, ARMAX, and Other Dynamic Regression ModelsDokument24 SeitenDepvar Indepvars Numlist Numlist: Arima - ARIMA, ARMAX, and Other Dynamic Regression ModelsJimena MartinNoch keine Bewertungen

- Markov Chain Monte Carlo and Applied Bayesian PDFDokument102 SeitenMarkov Chain Monte Carlo and Applied Bayesian PDFnathaniel.chrNoch keine Bewertungen

- Arimax ArimaDokument57 SeitenArimax ArimaTeresaMadurai100% (1)

- Prediction of Stock Price UsingDokument11 SeitenPrediction of Stock Price Usingshahmed999Noch keine Bewertungen

- What-If Analysis TemplateDokument5 SeitenWhat-If Analysis Templatenathaniel.chrNoch keine Bewertungen

- 4 Prediction of Stock Price UsingDokument35 Seiten4 Prediction of Stock Price Usingnathaniel.chrNoch keine Bewertungen

- What-If Model - Users Guide: Project CostsDokument32 SeitenWhat-If Model - Users Guide: Project CostsvxspidyNoch keine Bewertungen

- 111 Market ST Wyckoff Said It FirstDokument10 Seiten111 Market ST Wyckoff Said It FirstNathan ChrisNoch keine Bewertungen

- Work RedesignDokument40 SeitenWork Redesignnathaniel.chrNoch keine Bewertungen

- Take Home Exam Fin 4910 6440 Spring 2008Dokument4 SeitenTake Home Exam Fin 4910 6440 Spring 2008nathaniel.chrNoch keine Bewertungen

- 8-1-7 Book Review MishraDokument2 Seiten8-1-7 Book Review Mishranathaniel.chrNoch keine Bewertungen

- Chaos Theory and Strategy: Theory, Application, and Managerial ImplicationsDokument12 SeitenChaos Theory and Strategy: Theory, Application, and Managerial Implicationsnathaniel.chrNoch keine Bewertungen

- Deepwater BookletDokument36 SeitenDeepwater Bookletnathaniel.chrNoch keine Bewertungen

- 91 - 1 Engle Forecasting Illiquidity-1Dokument35 Seiten91 - 1 Engle Forecasting Illiquidity-1nathaniel.chrNoch keine Bewertungen

- 00V Alexander Pagonidis The IBS Effect Mean Reversion in Equity ETFs 1Dokument27 Seiten00V Alexander Pagonidis The IBS Effect Mean Reversion in Equity ETFs 1Kyungseok SonNoch keine Bewertungen

- T Burns e GM StalkerDokument6 SeitenT Burns e GM StalkerPaulo PenicheiroNoch keine Bewertungen

- Market Data Symbol GuideDokument5 SeitenMarket Data Symbol Guidenathaniel.chrNoch keine Bewertungen

- Galbraithmatrix1971 PDFDokument12 SeitenGalbraithmatrix1971 PDFTotok SudjarwantoNoch keine Bewertungen

- Introduction To Corporate Finance: Pre-Class MaterialDokument23 SeitenIntroduction To Corporate Finance: Pre-Class Materialnathaniel.chrNoch keine Bewertungen

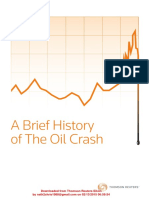

- A Brief History of The Oil CrashDokument19 SeitenA Brief History of The Oil Crashnathaniel.chrNoch keine Bewertungen

- IBM SPSS Statistics 23Dokument1 SeiteIBM SPSS Statistics 23nathaniel.chrNoch keine Bewertungen

- BinomialModel MultiPeriodDokument43 SeitenBinomialModel MultiPeriodnathaniel.chrNoch keine Bewertungen

- Secondary Design 1980Dokument4 SeitenSecondary Design 1980maheshbandhamNoch keine Bewertungen

- Maximum Allowable Diminution NKK Selida 27Dokument35 SeitenMaximum Allowable Diminution NKK Selida 27takis vlastosNoch keine Bewertungen

- UNCCD Convention ENG 0Dokument56 SeitenUNCCD Convention ENG 0Alex Sia Hong RuiNoch keine Bewertungen

- Cruel Summer by James Dawson ExtractDokument12 SeitenCruel Summer by James Dawson ExtractOrion Publishing Group0% (1)

- Present TenseDokument3 SeitenPresent TenseLê LongNoch keine Bewertungen

- Explanation and Practice Will and Going ToDokument8 SeitenExplanation and Practice Will and Going ToCristinaNoch keine Bewertungen

- Formation and Characteristics of Icebergs, GlacierDokument75 SeitenFormation and Characteristics of Icebergs, GlacierDENWIL VINCENT MONERANoch keine Bewertungen

- Laurie Baker: Peelay Ifa Ashfaque Fourth - Yr.B.ArchDokument30 SeitenLaurie Baker: Peelay Ifa Ashfaque Fourth - Yr.B.ArchIfa PeelayNoch keine Bewertungen

- Summative English-7Dokument3 SeitenSummative English-7Agyao Yam FaithNoch keine Bewertungen

- AM 4206M Dotocdogio PDFDokument2 SeitenAM 4206M Dotocdogio PDFtrungvuNoch keine Bewertungen

- U4SV - 1. The EnvironmentDokument21 SeitenU4SV - 1. The EnvironmentMaru C.Noch keine Bewertungen

- 11 Qty Tech Updated PDFDokument7 Seiten11 Qty Tech Updated PDFWilsonNoch keine Bewertungen

- 4S-10 01Dokument27 Seiten4S-10 01Claudio Hernández PobleteNoch keine Bewertungen

- Tài Liệu Livestream: A. Liên Từ Kết HợpDokument3 SeitenTài Liệu Livestream: A. Liên Từ Kết HợpHợp PhạmNoch keine Bewertungen

- More Warming Ev (Both Sides)Dokument250 SeitenMore Warming Ev (Both Sides)Brian LiaoNoch keine Bewertungen

- Butler Belcher GermanDokument27 SeitenButler Belcher GermanKumaranNoch keine Bewertungen

- The Chemistry of The AtmosphereDokument44 SeitenThe Chemistry of The AtmosphereZEID AL-HUSSEIN ISMAEL SARAIL100% (1)

- The Basin Campsite To Heaton GapDokument19 SeitenThe Basin Campsite To Heaton GapAlan ChanNoch keine Bewertungen

- 2018 Martin Luther King, Jr. Youth Poetry Contest WinnersDokument14 Seiten2018 Martin Luther King, Jr. Youth Poetry Contest WinnersSean BakerNoch keine Bewertungen

- 9.1740.xx - XXX TDL14 V3.12 EngDokument30 Seiten9.1740.xx - XXX TDL14 V3.12 EngdotronganhtuanNoch keine Bewertungen

- 9 AbbreviationDokument158 Seiten9 AbbreviationArtem CvetkovNoch keine Bewertungen

- Heat Exchanger TypesDokument7 SeitenHeat Exchanger TypesMarwan ShamsNoch keine Bewertungen

- Quirino ProvinceDokument26 SeitenQuirino ProvinceAlyssa Mae SantiagoNoch keine Bewertungen

- Flood in IndonesiaDokument4 SeitenFlood in IndonesiaarifcahyagumelarNoch keine Bewertungen