Das könnte Ihnen auch gefallen

- ACCT1101 Wk4 Tutorial 3 SolutionsDokument8 SeitenACCT1101 Wk4 Tutorial 3 SolutionskyleNoch keine Bewertungen

- AY2021-22 ANISETTY SINDHU-EFPPS3410N-ComputationDokument3 SeitenAY2021-22 ANISETTY SINDHU-EFPPS3410N-Computationforty oneNoch keine Bewertungen

- Afe 3582Dokument6 SeitenAfe 3582sarah josephNoch keine Bewertungen

- Cashflow Analysis - Beta - GammaDokument14 SeitenCashflow Analysis - Beta - Gammashahin selkarNoch keine Bewertungen

- Standlone Cash Flow StatementDokument2 SeitenStandlone Cash Flow StatementVaibhav SìňghNoch keine Bewertungen

- WTB 2016 Tec, Inc. Interim Fs 2016Dokument32 SeitenWTB 2016 Tec, Inc. Interim Fs 2016KarlayaanNoch keine Bewertungen

- Exercise 5-9 (Part Level Submission) : Allessandro Scarlatti Company Balance Sheet (Partial) DECEMBER 31, 2014Dokument3 SeitenExercise 5-9 (Part Level Submission) : Allessandro Scarlatti Company Balance Sheet (Partial) DECEMBER 31, 2014Tntnntnt ntntNoch keine Bewertungen

- Jawaban Soal UTS Akuntansi Keu - MenengahDokument4 SeitenJawaban Soal UTS Akuntansi Keu - MenengahJessinthaNoch keine Bewertungen

- Answer 4 - "Answers Only For Vaughn Company, Bennett Enterprise"Dokument3 SeitenAnswer 4 - "Answers Only For Vaughn Company, Bennett Enterprise"Rheu ReyesNoch keine Bewertungen

- "Finacial Statement": TugasDokument7 Seiten"Finacial Statement": TugasSekar Arum OctavanyNoch keine Bewertungen

- IAS1 Presentation of Financial StatementsDokument8 SeitenIAS1 Presentation of Financial StatementsAdnan AshrafNoch keine Bewertungen

- Riddhi Siddhi Grain StoreDokument9 SeitenRiddhi Siddhi Grain StoreRavi KarnaNoch keine Bewertungen

- Vinod Singh Computation Revised-3Dokument4 SeitenVinod Singh Computation Revised-3vinodNoch keine Bewertungen

- Income Statement For The Year Ended, December, 31, 2016: Pt. ZaliaDokument4 SeitenIncome Statement For The Year Ended, December, 31, 2016: Pt. ZaliaNofi Nurlaila0% (1)

- Working Papers SAIDokument7 SeitenWorking Papers SAISai RillNoch keine Bewertungen

- Srinivas Vutukuri AY 2021-2022: Computation of Income (ITR4)Dokument3 SeitenSrinivas Vutukuri AY 2021-2022: Computation of Income (ITR4)forty oneNoch keine Bewertungen

- Budhanilkantha Healthcare Pvt. LTD: For: R. Puri & AssociatesDokument3 SeitenBudhanilkantha Healthcare Pvt. LTD: For: R. Puri & AssociatesSanjiv GuptaNoch keine Bewertungen

- Manishkumar Kumudchandra Dhruve AY 2021-2022: Computation of Income (ITR2)Dokument3 SeitenManishkumar Kumudchandra Dhruve AY 2021-2022: Computation of Income (ITR2)Sanjay ThakkarNoch keine Bewertungen

- 2019 Unit 4 Budgeting SAC Solution BookDokument3 Seiten2019 Unit 4 Budgeting SAC Solution BookLachlan McFarlandNoch keine Bewertungen

- VREIT VFund Management Inc. Report Q12023 18may23 For FilingDokument9 SeitenVREIT VFund Management Inc. Report Q12023 18may23 For FilingjvNoch keine Bewertungen

- CardStatement 2018-01-08Dokument6 SeitenCardStatement 2018-01-08grihit singhNoch keine Bewertungen

- 2017-18 CoiDokument2 Seiten2017-18 CoiAshok ShahNoch keine Bewertungen

- 04 Assignments Practical Questions NEWDokument21 Seiten04 Assignments Practical Questions NEWBhupendra MendoleNoch keine Bewertungen

- Bsbfia412-Case Study 2019Dokument15 SeitenBsbfia412-Case Study 2019Pattaniya KosayothinNoch keine Bewertungen

- Finance Save MartDokument5 SeitenFinance Save MartTristan ElfanNoch keine Bewertungen

- Computation 21 1Dokument1 SeiteComputation 21 1Laba MeherNoch keine Bewertungen

- Computation FY 18-19 PDFDokument6 SeitenComputation FY 18-19 PDFRuch JainNoch keine Bewertungen

- Balance Sheet PDFDokument12 SeitenBalance Sheet PDFzeeshan shaikhNoch keine Bewertungen

- PL and Balance Sheet Detailed FormatDokument5 SeitenPL and Balance Sheet Detailed FormatPradeep G MenonNoch keine Bewertungen

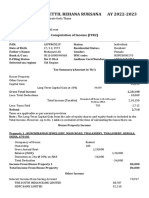

- AY2022-23 KALLA PUTHIYAVEETTIL REHANA RUKSANA-ASFPR0552F-ComputationDokument3 SeitenAY2022-23 KALLA PUTHIYAVEETTIL REHANA RUKSANA-ASFPR0552F-ComputationSourabh PunshiNoch keine Bewertungen

- Ilovepdf MergedDokument7 SeitenIlovepdf MergedRavi ChristoNoch keine Bewertungen

- Kashato Practice Set - 2020-10thedDokument84 SeitenKashato Practice Set - 2020-10thedMary Jhiezael Pascual83% (12)

- Running Head: Financial AccountingDokument9 SeitenRunning Head: Financial AccountingKashémNoch keine Bewertungen

- TM PQsDokument10 SeitenTM PQsAnooshayNoch keine Bewertungen

- Employee Details Payment & Leave Details: Arrears Current AmountDokument1 SeiteEmployee Details Payment & Leave Details: Arrears Current Amountindhar666Noch keine Bewertungen

- Midterm Pretest - Cost Model-Partial Goodwill FinalDokument9 SeitenMidterm Pretest - Cost Model-Partial Goodwill FinalWinnie LaraNoch keine Bewertungen

- 6 - COMPUTATION OF TAXABLE VALUE - Q - As - AFTER SESSION - 9Dokument21 Seiten6 - COMPUTATION OF TAXABLE VALUE - Q - As - AFTER SESSION - 9Mighty SinghNoch keine Bewertungen

- Glainier Industríal CorporationDokument43 SeitenGlainier Industríal CorporationGraceila CalopeNoch keine Bewertungen

- Model Ans - Sas - I April 2018Dokument68 SeitenModel Ans - Sas - I April 2018প্রীতম সেনNoch keine Bewertungen

- QuizDokument41 SeitenQuizbar barNoch keine Bewertungen

- CLWY Q1 2019 FinancialsDokument3 SeitenCLWY Q1 2019 FinancialskdwcapitalNoch keine Bewertungen

- 2021-22 Acknowledgement PDFDokument1 Seite2021-22 Acknowledgement PDFSidvik InfotechNoch keine Bewertungen

- NitishDokument1 SeiteNitishkaushikdutta176Noch keine Bewertungen

- Kashato Pracetice Set Answer KeyDokument66 SeitenKashato Pracetice Set Answer KeySnowy WhiteNoch keine Bewertungen

- Statement of Financial Position Sci: Adjustement To Reconcile Net Income To Net Cash Provided by Operating ActivitiesDokument6 SeitenStatement of Financial Position Sci: Adjustement To Reconcile Net Income To Net Cash Provided by Operating ActivitiesSai RillNoch keine Bewertungen

- Taj Nepal Pvt. LTD 76 TaxDokument31 SeitenTaj Nepal Pvt. LTD 76 TaxSunny DesharNoch keine Bewertungen

- Darlami Hardware & SuppliersDokument3 SeitenDarlami Hardware & SuppliersManoj gurungNoch keine Bewertungen

- Coca-Cola (Ticker Symbol KO On NYSE) : Standardized Balance Sheet and Income Statement (Millions)Dokument6 SeitenCoca-Cola (Ticker Symbol KO On NYSE) : Standardized Balance Sheet and Income Statement (Millions)Sayan BiswasNoch keine Bewertungen

- PROBLEM NO. 1 - Pistons Company: Note: Prepare "T" Accounts Then Post Identified AdjustmentsDokument13 SeitenPROBLEM NO. 1 - Pistons Company: Note: Prepare "T" Accounts Then Post Identified AdjustmentsShiela Mae BautistaNoch keine Bewertungen

- Star ReportsDokument38 SeitenStar ReportsAnnisa DewiNoch keine Bewertungen

- Revenue: Non-Current AssetsDokument5 SeitenRevenue: Non-Current Assetsfahim tusarNoch keine Bewertungen

- Bhaivav Laxmi Ma Galla Bhandar7677Dokument14 SeitenBhaivav Laxmi Ma Galla Bhandar7677Ravi KarnaNoch keine Bewertungen

- Cash Flow QuestionDokument2 SeitenCash Flow QuestionomairNoch keine Bewertungen

- Chapter 5 - Selected SolutionsDokument13 SeitenChapter 5 - Selected SolutionsNouh Al-SayyedNoch keine Bewertungen

- The Catholic Syrian Bank LimitedDokument2 SeitenThe Catholic Syrian Bank Limitedsaravanan aNoch keine Bewertungen

- CH 12 Wiley Plus Kimmel Quiz & HWDokument9 SeitenCH 12 Wiley Plus Kimmel Quiz & HWmkiNoch keine Bewertungen

- Rajesh Bora Itr PLBS 2022Dokument5 SeitenRajesh Bora Itr PLBS 2022ABDUL KHALIKNoch keine Bewertungen

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineVon EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNoch keine Bewertungen

- A Comparative Analysis of Tax Administration in Asia and the Pacific—Sixth EditionVon EverandA Comparative Analysis of Tax Administration in Asia and the Pacific—Sixth EditionNoch keine Bewertungen

- 1 - Tute 1 Intro To ITDokument1 Seite1 - Tute 1 Intro To IT林志成Noch keine Bewertungen

- ACW2491 Lecture 3 Handout SolutionStudentS22016Dokument4 SeitenACW2491 Lecture 3 Handout SolutionStudentS22016林志成Noch keine Bewertungen

- 1 - Tutorial 11 - StudentDokument4 Seiten1 - Tutorial 11 - Student林志成Noch keine Bewertungen

- ACW2491 Lecture 4 Handout SolutionS22016Dokument4 SeitenACW2491 Lecture 4 Handout SolutionS22016林志成Noch keine Bewertungen

- ACW1100 Tutorial Week2Dokument12 SeitenACW1100 Tutorial Week2林志成Noch keine Bewertungen

- Presentation 1Dokument4 SeitenPresentation 1林志成Noch keine Bewertungen

- Presentation 1Dokument1 SeitePresentation 1林志成Noch keine Bewertungen

- Newton Newman, Reggie Ratner Appleton Water Tower: Chapter 21: I Finish FallingDokument4 SeitenNewton Newman, Reggie Ratner Appleton Water Tower: Chapter 21: I Finish Falling林志成Noch keine Bewertungen

- Modeling Peak ProfitabiliytDokument23 SeitenModeling Peak ProfitabiliytBrentjaciow100% (1)

- A222 Tutorial 2 BKAL1013Dokument9 SeitenA222 Tutorial 2 BKAL1013Ali AzizanNoch keine Bewertungen

- Accounting Best PracticesDokument23 SeitenAccounting Best Practicesralph237100% (1)

- Topic: Internship Report On Financial Performance of Aneesha Dye-Chem Company Limited Submitted ToDokument35 SeitenTopic: Internship Report On Financial Performance of Aneesha Dye-Chem Company Limited Submitted ToBadhan Roy BandhanNoch keine Bewertungen

- Submitted By: Submitted ToDokument10 SeitenSubmitted By: Submitted Tosuraj ban100% (1)

- 2015 - Valuation of SharesDokument31 Seiten2015 - Valuation of SharesGhanshyam KhandayathNoch keine Bewertungen

- 12 Account SP 01 PDFDokument24 Seiten12 Account SP 01 PDFJanvi KushwahaNoch keine Bewertungen

- Deccan Industries: Summary of Rated InstrumentsDokument6 SeitenDeccan Industries: Summary of Rated Instrumentsmohamed shufiyanNoch keine Bewertungen

- Eaton V - FIN711 - Week 8 - Individual Leadership Plan Addendum - FinanceDokument14 SeitenEaton V - FIN711 - Week 8 - Individual Leadership Plan Addendum - FinancevjeatonNoch keine Bewertungen

- GP Manual FinalDokument111 SeitenGP Manual Finalskumara0% (1)

- AccountingDokument5 SeitenAccountingRaveena JainNoch keine Bewertungen

- 17 Answers To All ProblemsDokument25 Seiten17 Answers To All ProblemsRaşitÖnerNoch keine Bewertungen

- Gwyn 2Dokument8 SeitenGwyn 2Jhay Sy LynNoch keine Bewertungen

- MCB PPT Slids of Finance For VU StudentsDokument54 SeitenMCB PPT Slids of Finance For VU StudentsMudassar Yameen75% (4)

- Goal Seek ExcelDokument21 SeitenGoal Seek ExcelAsna Sicantik ManikNoch keine Bewertungen

- Contract Accounting Journal EntriesDokument3 SeitenContract Accounting Journal Entrieskawasakidude21100% (2)

- FABM 1 Week 3 4Dokument20 SeitenFABM 1 Week 3 4RD Suarez67% (6)

- Revenue Memorandum Circulars PDFDokument90 SeitenRevenue Memorandum Circulars PDFJewellrie Dela CruzNoch keine Bewertungen

- Chapter - 3 - ANALYZING FINANCIAL STATEMNETSDokument33 SeitenChapter - 3 - ANALYZING FINANCIAL STATEMNETSWijdan Saleem EdwanNoch keine Bewertungen

- Reflection Paper About Revenue CycleDokument1 SeiteReflection Paper About Revenue CycleJoshua TagayunaNoch keine Bewertungen

- Note On Business Model Analysis For The EntrepreneurDokument7 SeitenNote On Business Model Analysis For The Entrepreneurjulieismysushiname0% (1)

- AP Long Test 1 - CHANGES&ERROR, CASH ACCRUAL, SINGLE ENTRYDokument12 SeitenAP Long Test 1 - CHANGES&ERROR, CASH ACCRUAL, SINGLE ENTRYjasfNoch keine Bewertungen

- MODULE 01 Transaction Processes and Business ProcessesDokument6 SeitenMODULE 01 Transaction Processes and Business ProcessesRed ReyesNoch keine Bewertungen

- Power BI - Revenue - Industry Agnostic Revenue - Analysis - Step-by-Step GuideDokument15 SeitenPower BI - Revenue - Industry Agnostic Revenue - Analysis - Step-by-Step GuideGian Carlo Gonzales AnastacioNoch keine Bewertungen

- Chapter-Iv Data Analysis &interpretation Cash Flow StatementDokument24 SeitenChapter-Iv Data Analysis &interpretation Cash Flow StatementananthakumarNoch keine Bewertungen

- Financial Plan: A. Start Up Cost and CapitalizationDokument17 SeitenFinancial Plan: A. Start Up Cost and CapitalizationMaritess MunozNoch keine Bewertungen

- Public Sector Accounting Cat1 March 2022Dokument4 SeitenPublic Sector Accounting Cat1 March 2022hasfa konsoNoch keine Bewertungen

- Test Bank Accounting 25th Editon Warren Chapter 6 Accounting For Merchandising Businesses PDFDokument130 SeitenTest Bank Accounting 25th Editon Warren Chapter 6 Accounting For Merchandising Businesses PDFAverose Bautista100% (1)

- Finance Report of Bharat BiotechDokument5 SeitenFinance Report of Bharat BiotechUnicorn SpiderNoch keine Bewertungen

- Unit 5 - Financial Reporting and Analysis PDFDokument118 SeitenUnit 5 - Financial Reporting and Analysis PDFEstefany MariáteguiNoch keine Bewertungen