Das könnte Ihnen auch gefallen

- Balance Sheet Income StatementDokument50 SeitenBalance Sheet Income Statementgurbaxeesh0% (1)

- SSSForm Retirement ClaimDokument3 SeitenSSSForm Retirement ClaimMark JosephNoch keine Bewertungen

- Financial Accounting and Reporting Study Guide NotesVon EverandFinancial Accounting and Reporting Study Guide NotesBewertung: 1 von 5 Sternen1/5 (1)

- Multi-Step Income Statement - CRDokument16 SeitenMulti-Step Income Statement - CRVivian BastoNoch keine Bewertungen

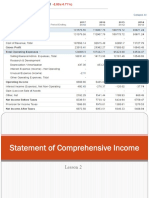

- Lesson 2 Statement of Comprehensive IncomeDokument23 SeitenLesson 2 Statement of Comprehensive IncomePaulette Sarno80% (5)

- Financial ManagementDokument32 SeitenFinancial ManagementMarkus Bernabe Davira100% (2)

- FABM1 Q4 Module 9 Source Documents Used in Merchandising BusinessDokument16 SeitenFABM1 Q4 Module 9 Source Documents Used in Merchandising Businessrio100% (1)

- Fundamentals of Accountancy, Business, and Management 2: ExpectationDokument131 SeitenFundamentals of Accountancy, Business, and Management 2: ExpectationAngela Garcia100% (1)

- SBI Reverse Mortgage LoanDokument5 SeitenSBI Reverse Mortgage LoanVishwa Prasanna Kumar100% (1)

- Module in Fabm 1: Department of Education Schools Division of Pasay CityDokument6 SeitenModule in Fabm 1: Department of Education Schools Division of Pasay CityAngelica Mae SuñasNoch keine Bewertungen

- Statement of Financial Position: Fundamentals of Accountancy, Business and Management 2Dokument55 SeitenStatement of Financial Position: Fundamentals of Accountancy, Business and Management 2Arminda Villamin75% (4)

- Senior High School S.Y. 2019-2020Dokument4 SeitenSenior High School S.Y. 2019-2020Cy Dollete-Suarez100% (1)

- Change in Equity SCEDokument3 SeitenChange in Equity SCEAizia Sarceda Guzman100% (2)

- Production BudgetDokument11 SeitenProduction BudgetSamson, Ma. Louise Ren A.Noch keine Bewertungen

- Week11-Completing The Accounting CycleDokument44 SeitenWeek11-Completing The Accounting CycleAmir Indrabudiman100% (2)

- Horizontal and Vertical AnalysisDokument28 SeitenHorizontal and Vertical AnalysisRachelle78% (9)

- Statement of Comprehensive IncomeDokument30 SeitenStatement of Comprehensive IncomeSheilaMarieAnnMagcalas100% (4)

- Account StatementDokument2 SeitenAccount StatementSiva KumaranNoch keine Bewertungen

- Cash Flow StatementDokument10 SeitenCash Flow StatementSheilaMarieAnnMagcalasNoch keine Bewertungen

- Cash Flow StatementDokument59 SeitenCash Flow StatementApple Crissa Mae Rejas100% (1)

- FABM 2 - Lesson1 5Dokument78 SeitenFABM 2 - Lesson1 5Sis HopNoch keine Bewertungen

- Accountancy, Business, and Management 2Dokument200 SeitenAccountancy, Business, and Management 2Sab Ibarreta100% (2)

- SEPA DocumentDokument7 SeitenSEPA DocumentRajendran Suresh100% (1)

- Business Finance: Quarter I (Week 5)Dokument12 SeitenBusiness Finance: Quarter I (Week 5)clarisse ginez83% (6)

- Cash Flow StatementsDokument15 SeitenCash Flow StatementsMaryjoy CuyosNoch keine Bewertungen

- Accounting Books - Journal, Ledger and Trial BalanceDokument35 SeitenAccounting Books - Journal, Ledger and Trial BalanceGhie Ragat100% (3)

- Journalizing Transactions (Review) - 9.5.17Dokument13 SeitenJournalizing Transactions (Review) - 9.5.17Jessa Beloy100% (1)

- Accounting 2 Week 1 4 LPDokument33 SeitenAccounting 2 Week 1 4 LPMewifell100% (1)

- Statement of Changes in Equity - Practice ExercisesDokument2 SeitenStatement of Changes in Equity - Practice ExercisesEvangeline Gicale25% (8)

- Fundamentals of Accountancy, Business and Management 2: Quarter 1-Module 5Dokument28 SeitenFundamentals of Accountancy, Business and Management 2: Quarter 1-Module 5Leigh Guittap100% (2)

- Chapter 11 - Standard Cost & Balance ScorecardDokument65 SeitenChapter 11 - Standard Cost & Balance ScorecardPadlah Riyadi. SE., Ak., CA., MM.100% (2)

- Abm 2Dokument11 SeitenAbm 2Kyla Balistoy100% (1)

- A Study of Cash Management at Axis BankDokument34 SeitenA Study of Cash Management at Axis BankHimanshuNoch keine Bewertungen

- Change in Equity SCEDokument3 SeitenChange in Equity SCEAizia Sarceda GuzmanNoch keine Bewertungen

- CashflowDokument6 SeitenCashflowAizia Sarceda Guzman71% (7)

- FinDokument4 SeitenFinTintin Brusola Salen67% (3)

- Identify Which of The Following Transactions FallDokument1 SeiteIdentify Which of The Following Transactions FallAdoree Ramos75% (4)

- Self-Learning Kit: Region I Schools Division of Ilocos Sur Bantay, Ilocos SurDokument13 SeitenSelf-Learning Kit: Region I Schools Division of Ilocos Sur Bantay, Ilocos SurLiam Aleccis Obrero CabanitNoch keine Bewertungen

- FABM2 Module 06 (Q1-W7)Dokument8 SeitenFABM2 Module 06 (Q1-W7)Christian Zebua75% (4)

- CHAPTER 2 Horizontal-AnalysisDokument1 SeiteCHAPTER 2 Horizontal-AnalysisAiron Bendaña0% (1)

- FABM2 Module 03 (Q1-W4)Dokument6 SeitenFABM2 Module 03 (Q1-W4)Christian ZebuaNoch keine Bewertungen

- Special ExamDokument3 SeitenSpecial ExamAdoree Ramos50% (2)

- Assignment November11 KylaAccountingDokument2 SeitenAssignment November11 KylaAccountingADRIANO, Glecy C.Noch keine Bewertungen

- TG - FundaofABM-Lesson 6Dokument8 SeitenTG - FundaofABM-Lesson 6HLeigh Nietes-Gabutan100% (5)

- Financial Statement AnalysisDokument25 SeitenFinancial Statement AnalysisAldrin CustodioNoch keine Bewertungen

- Module 6 - Fabm2-MergedDokument37 SeitenModule 6 - Fabm2-MergedJaazaniah S. PavilionNoch keine Bewertungen

- Dela Pena, C. Marygold Bank Recon AnswerDokument6 SeitenDela Pena, C. Marygold Bank Recon AnswerDe Nev OelNoch keine Bewertungen

- Fabm-2 2Dokument33 SeitenFabm-2 2KIRSTEN HENRYK CHINGNoch keine Bewertungen

- Abm General and Special JournalDokument63 SeitenAbm General and Special JournalEstelle Gammad33% (3)

- YVONNE MerchandisingDokument1 SeiteYVONNE Merchandisingart50% (2)

- Answers in Fundamentals of Accountancy, Business and Management 1Dokument14 SeitenAnswers in Fundamentals of Accountancy, Business and Management 1Sherilyn Diaz0% (2)

- Activity 4.1 JKL Company Horizontal AnalysisDokument4 SeitenActivity 4.1 JKL Company Horizontal AnalysisChancellor RimuruNoch keine Bewertungen

- 13 Accounting Cycle of A Service Business 2Dokument28 Seiten13 Accounting Cycle of A Service Business 2Ashley Judd Mallonga Beran60% (5)

- Financial Statement Analysis PT 2Dokument43 SeitenFinancial Statement Analysis PT 2Kim Patrick VictoriaNoch keine Bewertungen

- Report in Business Finance: Group 2 - Review of Financial Statement Preparation, Analysis, and InterpretationDokument14 SeitenReport in Business Finance: Group 2 - Review of Financial Statement Preparation, Analysis, and InterpretationKOUJI N. MARQUEZNoch keine Bewertungen

- Fabm Notes Grade 12Dokument9 SeitenFabm Notes Grade 12hello hahahNoch keine Bewertungen

- Time Value of Money: Abm5 - Business FinanceDokument34 SeitenTime Value of Money: Abm5 - Business FinanceBarbie BleuNoch keine Bewertungen

- Sweet Beginnings Co - XLSX CASE STUDY ANSWERDokument11 SeitenSweet Beginnings Co - XLSX CASE STUDY ANSWERYna AlfonsoNoch keine Bewertungen

- A.) Income StatementDokument2 SeitenA.) Income StatementShawn Mendez100% (2)

- Fabm2 Q2 M4 - 4 CsefDokument20 SeitenFabm2 Q2 M4 - 4 CsefZeus MalicdemNoch keine Bewertungen

- Sdo Batangas: Department of EducationDokument15 SeitenSdo Batangas: Department of EducationPrincess GabaynoNoch keine Bewertungen

- Business Finance: Financial Planning Tools and ConceptsDokument14 SeitenBusiness Finance: Financial Planning Tools and ConceptsElyzel Joy Tingson100% (1)

- ABM 12 (Cash Flow Statement) CFSDokument6 SeitenABM 12 (Cash Flow Statement) CFSBianca DalipeNoch keine Bewertungen

- ABM 12 (Cash Flow Statement) CFSDokument6 SeitenABM 12 (Cash Flow Statement) CFSWella LozadaNoch keine Bewertungen

- FABM 2 Lesson 6 CFSDokument28 SeitenFABM 2 Lesson 6 CFSKia MorenoNoch keine Bewertungen

- Topic IV - Cash Flow Statement - Jianne's FABM NotesDokument5 SeitenTopic IV - Cash Flow Statement - Jianne's FABM NotesJianne Ricci GalitNoch keine Bewertungen

- 4cash Flow StatementDokument8 Seiten4cash Flow StatementMarilyn Nelmida TamayoNoch keine Bewertungen

- Worksheet 1 Answer KeyDokument1 SeiteWorksheet 1 Answer KeyAizia Sarceda Guzman100% (1)

- 09 Instructor's Guide PDFDokument4 Seiten09 Instructor's Guide PDFAizia Sarceda GuzmanNoch keine Bewertungen

- Statement of ComprehensiveDokument3 SeitenStatement of ComprehensiveAizia Sarceda GuzmanNoch keine Bewertungen

- 01 Activity 1 PDFDokument1 Seite01 Activity 1 PDFAizia Sarceda GuzmanNoch keine Bewertungen

- Life After High School - A Post Secondary Students Guide To Success by Shawna NarayanDokument92 SeitenLife After High School - A Post Secondary Students Guide To Success by Shawna Narayanapi-344973256Noch keine Bewertungen

- Cork Chamber - Chamberlink (Nov 2013)Dokument24 SeitenCork Chamber - Chamberlink (Nov 2013)Imelda V. MulcahyNoch keine Bewertungen

- Salient Features of Islamic BankingDokument2 SeitenSalient Features of Islamic BankingNoor Hafizah0% (2)

- Cipla Names Umang Vohra As MD & Global CEO - Business Standard NewsDokument5 SeitenCipla Names Umang Vohra As MD & Global CEO - Business Standard NewsZekria Noori AfghanNoch keine Bewertungen

- Legcoun Problems and AnswersDokument18 SeitenLegcoun Problems and AnswersceeeyNoch keine Bewertungen

- Written ReportDokument19 SeitenWritten ReportAaron PaladaNoch keine Bewertungen

- Summary (Banking) VitalijaSDokument2 SeitenSummary (Banking) VitalijaSv sNoch keine Bewertungen

- VA Department of Veterans Affairs: Trier, John C 03/23/10Dokument2 SeitenVA Department of Veterans Affairs: Trier, John C 03/23/10John TrierNoch keine Bewertungen

- 02 FABM1 Module1 - Lesson2 Independent AssessmentDokument2 Seiten02 FABM1 Module1 - Lesson2 Independent AssessmentAtasha Nicole G. BahandeNoch keine Bewertungen

- 20 Basic Accounting Terms List For Preparation of PPSC, FPSC & NTS Tests - Government Jobs & Private Jobs in Pakistan 2018Dokument3 Seiten20 Basic Accounting Terms List For Preparation of PPSC, FPSC & NTS Tests - Government Jobs & Private Jobs in Pakistan 2018Dustar Ali HaideriNoch keine Bewertungen

- Debt and The Millennium Development Goals: A New Deal For Low-Income CountriesDokument11 SeitenDebt and The Millennium Development Goals: A New Deal For Low-Income CountriesOxfamNoch keine Bewertungen

- Vimal Chandra Grover Vs Bank of India On 26 April, 2000Dokument8 SeitenVimal Chandra Grover Vs Bank of India On 26 April, 2000Taannyya TiwariNoch keine Bewertungen

- Lighthouse Point News July IssueDokument76 SeitenLighthouse Point News July IssueJon FrangipaneNoch keine Bewertungen

- Principles of Lending and RecoveryDokument1.332 SeitenPrinciples of Lending and RecoverySridhara babu. N - ಶ್ರೀಧರ ಬಾಬು. ಎನ್Noch keine Bewertungen

- Boddicker Dan - 663 - ScannedDokument14 SeitenBoddicker Dan - 663 - ScannedZach EdwardsNoch keine Bewertungen

- Project Icpna Intermedio 12, IN PAIRS - FULLDokument2 SeitenProject Icpna Intermedio 12, IN PAIRS - FULLSamuel SaavedraNoch keine Bewertungen

- Advanced Accounting 1 - Millan: Problem 1-4: Exercises: ComputationalDokument10 SeitenAdvanced Accounting 1 - Millan: Problem 1-4: Exercises: ComputationalFritzNoch keine Bewertungen

- As 17 Segment ReportingDokument5 SeitenAs 17 Segment ReportingcalvinroarNoch keine Bewertungen

- Debt F-GDokument261 SeitenDebt F-GkenindiNoch keine Bewertungen

- Principles OF AccountsDokument9 SeitenPrinciples OF AccountsdonNoch keine Bewertungen

- Exercise 2.1Dokument9 SeitenExercise 2.1Stephanie XieNoch keine Bewertungen

- BCOMHDokument8 SeitenBCOMHamul65Noch keine Bewertungen

- List of CommittiesDokument2 SeitenList of CommittiesPrabhu Charan TejaNoch keine Bewertungen

- Promissory Note SampleDokument2 SeitenPromissory Note SampleRidzsr DharhaidherNoch keine Bewertungen