Das könnte Ihnen auch gefallen

- Summary: 12: Review and Analysis of Wagner and Harter's BookVon EverandSummary: 12: Review and Analysis of Wagner and Harter's BookNoch keine Bewertungen

- Unleashing Innovation: How Whirlpool Transformed an IndustryVon EverandUnleashing Innovation: How Whirlpool Transformed an IndustryBewertung: 3 von 5 Sternen3/5 (2)

- Outsource or Else!: How a Vp of Software Saved His CompanyVon EverandOutsource or Else!: How a Vp of Software Saved His CompanyNoch keine Bewertungen

- Companies, Snakes & Ladders: Success in the Arab Corporate JungleVon EverandCompanies, Snakes & Ladders: Success in the Arab Corporate JungleNoch keine Bewertungen

- Analysisof Financial StatementsDokument208 SeitenAnalysisof Financial StatementsSebastianNoch keine Bewertungen

- Platform Business Models A Complete Guide - 2019 EditionVon EverandPlatform Business Models A Complete Guide - 2019 EditionNoch keine Bewertungen

- Indispensable: How To Become The Company That Your Customers Can't Live WithoutVon EverandIndispensable: How To Become The Company That Your Customers Can't Live WithoutBewertung: 4 von 5 Sternen4/5 (4)

- ERP-Based Implementation Tools A Complete Guide - 2019 EditionVon EverandERP-Based Implementation Tools A Complete Guide - 2019 EditionNoch keine Bewertungen

- Summary: Profitable Growth Is Everyone's Business: Review and Analysis of Charan's BookVon EverandSummary: Profitable Growth Is Everyone's Business: Review and Analysis of Charan's BookNoch keine Bewertungen

- Growth Strategy Process Flow A Complete Guide - 2020 EditionVon EverandGrowth Strategy Process Flow A Complete Guide - 2020 EditionNoch keine Bewertungen

- The Innovation Toolkit 2: The Innovation Toolkit, #2Von EverandThe Innovation Toolkit 2: The Innovation Toolkit, #2Noch keine Bewertungen

- Shockproof: How to Hardwire Your Business for Lasting SuccessVon EverandShockproof: How to Hardwire Your Business for Lasting SuccessNoch keine Bewertungen

- Value as a Service: Embracing the Coming DisruptionVon EverandValue as a Service: Embracing the Coming DisruptionBewertung: 3 von 5 Sternen3/5 (2)

- Strategic Networking 2.0: Harness the Power of Connection and Inclusion for Business ClassVon EverandStrategic Networking 2.0: Harness the Power of Connection and Inclusion for Business ClassNoch keine Bewertungen

- Leading in Times of Crisis: Navigating Through Complexity, Diversity and Uncertainty to Save Your BusinessVon EverandLeading in Times of Crisis: Navigating Through Complexity, Diversity and Uncertainty to Save Your BusinessNoch keine Bewertungen

- Collapse of Distinction (Review and Analysis of McKain's Book)Von EverandCollapse of Distinction (Review and Analysis of McKain's Book)Noch keine Bewertungen

- Bye Bye Banks?: How Retail Banks are Being Displaced, Diminished and Disintermediated by Tech Startups and What They Can Do to SurviveVon EverandBye Bye Banks?: How Retail Banks are Being Displaced, Diminished and Disintermediated by Tech Startups and What They Can Do to SurviveNoch keine Bewertungen

- Digital Business Ecosystem A Complete Guide - 2019 EditionVon EverandDigital Business Ecosystem A Complete Guide - 2019 EditionNoch keine Bewertungen

- The Growth Code: The Key to Unlocking Sustainable Growth in any Modern BusinessVon EverandThe Growth Code: The Key to Unlocking Sustainable Growth in any Modern BusinessNoch keine Bewertungen

- Buy-In (Review and Analysis of Kotter and Whitehead's Book)Von EverandBuy-In (Review and Analysis of Kotter and Whitehead's Book)Noch keine Bewertungen

- Double-Digit Growth (Review and Analysis of Treacy's Book)Von EverandDouble-Digit Growth (Review and Analysis of Treacy's Book)Noch keine Bewertungen

- Individual Development Plan A Complete Guide - 2021 EditionVon EverandIndividual Development Plan A Complete Guide - 2021 EditionNoch keine Bewertungen

- Succession or Promotion?: A new outlook into succession planningVon EverandSuccession or Promotion?: A new outlook into succession planningNoch keine Bewertungen

- Sweat, Scale, Sell: Build Your Business Into An Asset of ValueVon EverandSweat, Scale, Sell: Build Your Business Into An Asset of ValueNoch keine Bewertungen

- You're Not Fired as a Result of Mergers, Acquisitions & ReorganizationsVon EverandYou're Not Fired as a Result of Mergers, Acquisitions & ReorganizationsNoch keine Bewertungen

- CUSTOMER DRIVEN LEADERSHIP: How To Win with Entrepreneurial Servant Leadership, Responsiveness to Client Data, & Constant CreativityVon EverandCUSTOMER DRIVEN LEADERSHIP: How To Win with Entrepreneurial Servant Leadership, Responsiveness to Client Data, & Constant CreativityNoch keine Bewertungen

- Going All In: How to implement Excellence in your businessVon EverandGoing All In: How to implement Excellence in your businessNoch keine Bewertungen

- Application Program Interface A Complete Guide - 2020 EditionVon EverandApplication Program Interface A Complete Guide - 2020 EditionNoch keine Bewertungen

- The 2R Manager: When to Relate, When to Require, and How to Do Both EffectivelyVon EverandThe 2R Manager: When to Relate, When to Require, and How to Do Both EffectivelyBewertung: 4 von 5 Sternen4/5 (2)

- Ambidextrous Organization A Complete Guide - 2020 EditionVon EverandAmbidextrous Organization A Complete Guide - 2020 EditionNoch keine Bewertungen

- The Science of Being Great (Barnes & Noble Digital Library)Von EverandThe Science of Being Great (Barnes & Noble Digital Library)Bewertung: 3 von 5 Sternen3/5 (8)

- Customer CEO: How to Profit from the Power of Your CustomersVon EverandCustomer CEO: How to Profit from the Power of Your CustomersNoch keine Bewertungen

- Do You Have Who It Takes?: Managing Talent Risk in a High-Stakes Technical WorkforceVon EverandDo You Have Who It Takes?: Managing Talent Risk in a High-Stakes Technical WorkforceBewertung: 3 von 5 Sternen3/5 (1)

- The Retention Revolution: 7 Surprising (and Very Human!) Ways to Keep Employees Connected to Your CompanyVon EverandThe Retention Revolution: 7 Surprising (and Very Human!) Ways to Keep Employees Connected to Your CompanyBewertung: 3 von 5 Sternen3/5 (1)

- Business Planning and Control System The Ultimate Step-By-Step GuideVon EverandBusiness Planning and Control System The Ultimate Step-By-Step GuideNoch keine Bewertungen

- Summary of Brian E. Becker, David Ulrich & Mark A. Huselid's The HR ScorecardVon EverandSummary of Brian E. Becker, David Ulrich & Mark A. Huselid's The HR ScorecardNoch keine Bewertungen

- IT Demand Management A Complete Guide - 2021 EditionVon EverandIT Demand Management A Complete Guide - 2021 EditionNoch keine Bewertungen

- Network Advantage: How to Unlock Value From Your Alliances and PartnershipsVon EverandNetwork Advantage: How to Unlock Value From Your Alliances and PartnershipsNoch keine Bewertungen

- The Startup Habit: The Right Habits to Fuel the Entrepreneur in YouVon EverandThe Startup Habit: The Right Habits to Fuel the Entrepreneur in YouNoch keine Bewertungen

- How To Be The Best (In Business): Insights from my 40-year career (as well as before and after).Von EverandHow To Be The Best (In Business): Insights from my 40-year career (as well as before and after).Noch keine Bewertungen

- How a Hashtag Changed The World: Stories, Lessons and Reflections from the #LinkedInLocal MovementVon EverandHow a Hashtag Changed The World: Stories, Lessons and Reflections from the #LinkedInLocal MovementNoch keine Bewertungen

- Acctg For Related Party TransactionsDokument163 SeitenAcctg For Related Party TransactionsRisaiah OsborneNoch keine Bewertungen

- Blood Pressure Log 18Dokument1 SeiteBlood Pressure Log 18Yousab KaldasNoch keine Bewertungen

- Blood Pressure Log 03Dokument1 SeiteBlood Pressure Log 03Yousab KaldasNoch keine Bewertungen

- Blood Pressure Log 30Dokument2 SeitenBlood Pressure Log 30Yousab KaldasNoch keine Bewertungen

- Watercolor Brush Precision Practice Sheet by Nourane OwaisDokument1 SeiteWatercolor Brush Precision Practice Sheet by Nourane OwaisYousab KaldasNoch keine Bewertungen

- Blood Pressure Log 04Dokument2 SeitenBlood Pressure Log 04Yousab KaldasNoch keine Bewertungen

- Strategic Audit WorksheetDokument1 SeiteStrategic Audit WorksheetYousab KaldasNoch keine Bewertungen

- Blood Pressure Log 31Dokument1 SeiteBlood Pressure Log 31Yousab KaldasNoch keine Bewertungen

- Suggestions For Case AnalysisDokument27 SeitenSuggestions For Case AnalysisYousab KaldasNoch keine Bewertungen

- Blood Pressure Log 02Dokument1 SeiteBlood Pressure Log 02Yousab KaldasNoch keine Bewertungen

- Yasmina Answer Model-Final EditionDokument21 SeitenYasmina Answer Model-Final EditionYousab KaldasNoch keine Bewertungen

- First: Generic Strategies Generic Competitive Strategies:: Product DifferentiationDokument8 SeitenFirst: Generic Strategies Generic Competitive Strategies:: Product DifferentiationYousab KaldasNoch keine Bewertungen

- Strategic Audit For Transportation and Engineering Company For Tires (Trenco)Dokument16 SeitenStrategic Audit For Transportation and Engineering Company For Tires (Trenco)Yousab KaldasNoch keine Bewertungen

- Strat I GiesDokument11 SeitenStrat I GiesYousab KaldasNoch keine Bewertungen

- Marketing Plan (Dina)Dokument9 SeitenMarketing Plan (Dina)Yousab KaldasNoch keine Bewertungen

- The Functional Structure 2. Divisional Structure 3. The Strategic Business Unit (SBU) Structure 4. The Matrix StructureDokument17 SeitenThe Functional Structure 2. Divisional Structure 3. The Strategic Business Unit (SBU) Structure 4. The Matrix StructureYousab KaldasNoch keine Bewertungen

- HRM BriefDokument16 SeitenHRM BriefYousab KaldasNoch keine Bewertungen

- Some Types of CultureDokument10 SeitenSome Types of CultureYousab KaldasNoch keine Bewertungen

- Arab Academy For Science and Technology: Case Analysis: XYZ CompanyDokument16 SeitenArab Academy For Science and Technology: Case Analysis: XYZ CompanyYousab KaldasNoch keine Bewertungen

- 9.main Guideline For MarketingDokument18 Seiten9.main Guideline For MarketingYousab KaldasNoch keine Bewertungen

- Grand StrategyDokument3 SeitenGrand StrategyYousab KaldasNoch keine Bewertungen

- Comprehensive Exam Answer - 13.12.2013Dokument8 SeitenComprehensive Exam Answer - 13.12.2013Yousab KaldasNoch keine Bewertungen

- EXternal Factors PESTLEDokument3 SeitenEXternal Factors PESTLEYousab KaldasNoch keine Bewertungen

- Efe, Ife, CPM, QSPM MatrixDokument6 SeitenEfe, Ife, CPM, QSPM MatrixYousab Kaldas100% (1)

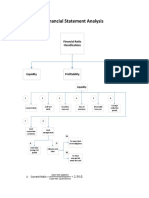

- Financial Statement AnalysisDokument5 SeitenFinancial Statement AnalysisYousab KaldasNoch keine Bewertungen

- External Environment - Task Environment: (1) MarketsDokument14 SeitenExternal Environment - Task Environment: (1) MarketsYousab KaldasNoch keine Bewertungen

- What Is Marketing?Dokument3 SeitenWhat Is Marketing?Yousab KaldasNoch keine Bewertungen

- SwotDokument9 SeitenSwotYousab KaldasNoch keine Bewertungen

- 1.1. The Boston Consulting Group (BCG) MatrixDokument4 Seiten1.1. The Boston Consulting Group (BCG) MatrixYousab KaldasNoch keine Bewertungen

- Template For Answering The Comprehensive Exam: 1 - Introduction & Company ProfileDokument21 SeitenTemplate For Answering The Comprehensive Exam: 1 - Introduction & Company ProfileYousab KaldasNoch keine Bewertungen

- Strategies and Tactics For ChangeDokument3 SeitenStrategies and Tactics For ChangeYousab KaldasNoch keine Bewertungen

- AEC 103 - Intermediate Accounting: Assignment 3 Accounts Receivable and Estimation of Doubtful AccountDokument4 SeitenAEC 103 - Intermediate Accounting: Assignment 3 Accounts Receivable and Estimation of Doubtful Accountjames bryan angklaNoch keine Bewertungen

- The Practice of Value Investing - , by Li Lu - LONGRIVERDokument10 SeitenThe Practice of Value Investing - , by Li Lu - LONGRIVERNick SposaNoch keine Bewertungen

- Delhi Pubic School, Nacharam Accountancy - Xi Question BankDokument9 SeitenDelhi Pubic School, Nacharam Accountancy - Xi Question BanklasyaNoch keine Bewertungen

- Managing Personal FinanceDokument39 SeitenManaging Personal FinanceBeverly EroyNoch keine Bewertungen

- Bourdieu Forms of CapitalDokument15 SeitenBourdieu Forms of Capitalapi-50446167100% (2)

- Cash Receipts CycleDokument19 SeitenCash Receipts CycleYenNoch keine Bewertungen

- Financial Statement AnalysisDokument3 SeitenFinancial Statement AnalysisAsad Rehman100% (1)

- Credit and Thrift Co-Operatives in NigeriaDokument6 SeitenCredit and Thrift Co-Operatives in NigeriaAbu FadilahNoch keine Bewertungen

- Project On Spending and Saving of College StudentsDokument61 SeitenProject On Spending and Saving of College StudentsKerala Techie Teens100% (1)

- Accounts Question and AnswerDokument47 SeitenAccounts Question and AnswerVinod Kumar PrajapatiNoch keine Bewertungen

- Deepak Eduworld PVT LTD: Receipt AmountDokument22 SeitenDeepak Eduworld PVT LTD: Receipt AmountSupriya BoseNoch keine Bewertungen

- JM IncDokument3 SeitenJM IncJomar VillenaNoch keine Bewertungen

- Img09/27/2022 - UCC Financing Statement (NYS Treasury)Dokument8 SeitenImg09/27/2022 - UCC Financing Statement (NYS Treasury)al malik ben beyNoch keine Bewertungen

- FAR 1 - Midterm - Practice Questions 2Dokument2 SeitenFAR 1 - Midterm - Practice Questions 2Yanela YishaNoch keine Bewertungen

- Entrepreneurship - Quarter 2 Week 9Dokument8 SeitenEntrepreneurship - Quarter 2 Week 9SHEEN ALUBANoch keine Bewertungen

- Ifrs 9 Cash and ReceivablesDokument50 SeitenIfrs 9 Cash and ReceivablesHagere EthiopiaNoch keine Bewertungen

- BM - Simple and CompoundDokument50 SeitenBM - Simple and CompoundMarites Domingo - Paquibulan100% (1)

- Chapter 7 - Clubbing of Income - NotesDokument17 SeitenChapter 7 - Clubbing of Income - NotesRahul TiwariNoch keine Bewertungen

- Vocabulary Worksheet and Key PDFDokument6 SeitenVocabulary Worksheet and Key PDFChristina PerezNoch keine Bewertungen

- An Overview of Customer Service Department of Kailash Bikas Bank LTDDokument31 SeitenAn Overview of Customer Service Department of Kailash Bikas Bank LTDArzu dhungana0% (1)

- Yc Vy BCM LB VTGJ O6 MDokument5 SeitenYc Vy BCM LB VTGJ O6 MAbhi saxenaNoch keine Bewertungen

- HDFC ProjectDokument31 SeitenHDFC ProjectSakshi SharmaNoch keine Bewertungen

- Winter 2007 Midterm With SolutionsDokument13 SeitenWinter 2007 Midterm With Solutionsupload55Noch keine Bewertungen

- A2 Level Essential Vocabulary: The Global Economy (Economics)Dokument10 SeitenA2 Level Essential Vocabulary: The Global Economy (Economics)A Grade EssaysNoch keine Bewertungen

- Chap 009Dokument20 SeitenChap 009Ela PelariNoch keine Bewertungen

- Chapter 9 Solution Manual MacroDokument5 SeitenChapter 9 Solution Manual MacroMega Pop LockerNoch keine Bewertungen

- Project On Mutual Funds As An Investment AvenueDokument18 SeitenProject On Mutual Funds As An Investment AvenueRishi vardhiniNoch keine Bewertungen

- Understanding Financial StatementsDokument36 SeitenUnderstanding Financial StatementsDurga PrasadNoch keine Bewertungen

- Monetary PolicyDokument10 SeitenMonetary PolicyAshish MisraNoch keine Bewertungen

- FIN 370 Final Exam 30 Questions With AnswersDokument11 SeitenFIN 370 Final Exam 30 Questions With Answersassignmentsehelp0% (1)