Das könnte Ihnen auch gefallen

- Coal India LTD - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel BrokingDokument2 SeitenCoal India LTD - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel Brokingmoisha sharmaNoch keine Bewertungen

- Vindhya Telelinks LTD - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel BrokingDokument2 SeitenVindhya Telelinks LTD - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel Brokingmoisha sharmaNoch keine Bewertungen

- Update On Government Stimulus Package - Part 1 - Size of Economic Package, Stock Recommendations, Total Stimulus Etc - Angel BrokingDokument4 SeitenUpdate On Government Stimulus Package - Part 1 - Size of Economic Package, Stock Recommendations, Total Stimulus Etc - Angel Brokingmoisha sharmaNoch keine Bewertungen

- Nestle India LTD - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel BrokingDokument4 SeitenNestle India LTD - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel Brokingmoisha sharmaNoch keine Bewertungen

- Auto - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel BrokingDokument6 SeitenAuto - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel Brokingmoisha sharmaNoch keine Bewertungen

- Parag Milk Foods LTD - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel BrokingDokument8 SeitenParag Milk Foods LTD - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel Brokingmoisha sharmaNoch keine Bewertungen

- Inox Wind LTD - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel BrokingDokument7 SeitenInox Wind LTD - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel Brokingmoisha sharmaNoch keine Bewertungen

- Avenue Supermarts LTD - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel BrokingDokument8 SeitenAvenue Supermarts LTD - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel Brokingmoisha sharmaNoch keine Bewertungen

- Reliance Industries Rights Issue Update - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel BrokingDokument2 SeitenReliance Industries Rights Issue Update - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel Brokingmoisha sharmaNoch keine Bewertungen

- V I P Industries LTD - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel BrokingDokument4 SeitenV I P Industries LTD - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel Brokingmoisha sharmaNoch keine Bewertungen

- Sun Pharmaceuticals Industries LTD - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel BrokingDokument6 SeitenSun Pharmaceuticals Industries LTD - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel Brokingmoisha sharmaNoch keine Bewertungen

- AngelTopPicks (April 2020) - List of Company Profiles, Performance Report, Stock Info & Key Financials - Angel BrokingDokument10 SeitenAngelTopPicks (April 2020) - List of Company Profiles, Performance Report, Stock Info & Key Financials - Angel Brokingmoisha sharmaNoch keine Bewertungen

- Aurobindo Pharma LTD - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel BrokingDokument10 SeitenAurobindo Pharma LTD - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel Brokingmoisha sharmaNoch keine Bewertungen

- Bata India LTD - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel BrokingDokument8 SeitenBata India LTD - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel Brokingmoisha sharmaNoch keine Bewertungen

- KEI Industries LTD - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel BrokingDokument8 SeitenKEI Industries LTD - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel Brokingmoisha sharmaNoch keine Bewertungen

- Blue Star LTD - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel BrokingDokument9 SeitenBlue Star LTD - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel Brokingmoisha sharmaNoch keine Bewertungen

- Mahindra & Mahindra LTD - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel BrokingDokument8 SeitenMahindra & Mahindra LTD - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel Brokingmoisha sharmaNoch keine Bewertungen

- Axis Bank LTD - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel BrokingDokument7 SeitenAxis Bank LTD - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel Brokingmoisha sharmaNoch keine Bewertungen

- ICICI Bank LTD - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel BrokingDokument6 SeitenICICI Bank LTD - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel Brokingmoisha sharmaNoch keine Bewertungen

- Ashok Leyland LTD - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel BrokingDokument8 SeitenAshok Leyland LTD - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel Brokingmoisha sharmaNoch keine Bewertungen

- Safari Industries (India) LTD - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel BrokingDokument8 SeitenSafari Industries (India) LTD - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel Brokingmoisha sharmaNoch keine Bewertungen

- Maruti Suzuki India LTD - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel BrokingDokument8 SeitenMaruti Suzuki India LTD - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel Brokingmoisha sharmaNoch keine Bewertungen

- Affle (India) LTD - Company Profile, Issue Details, Balance Sheet & Key Ratios - Angel BrokingDokument8 SeitenAffle (India) LTD - Company Profile, Issue Details, Balance Sheet & Key Ratios - Angel Brokingmoisha sharmaNoch keine Bewertungen

- Amber Enterprises India LTD - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel BrokingDokument7 SeitenAmber Enterprises India LTD - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel Brokingmoisha sharmaNoch keine Bewertungen

- CSB Bank - Company Profile, Issue Details, Balance Sheet & Key Ratios - Angel BrokingDokument7 SeitenCSB Bank - Company Profile, Issue Details, Balance Sheet & Key Ratios - Angel Brokingmoisha sharmaNoch keine Bewertungen

- IRCTC - Company Profile, Issue Details, Balance Sheet & Key Ratios - Angel BrokingDokument8 SeitenIRCTC - Company Profile, Issue Details, Balance Sheet & Key Ratios - Angel Brokingmoisha sharmaNoch keine Bewertungen

- Spandana Sphoorty Financial Limited - Company Profile, Issue Details, Balance Sheet & Key Ratios - Angel BrokingDokument7 SeitenSpandana Sphoorty Financial Limited - Company Profile, Issue Details, Balance Sheet & Key Ratios - Angel Brokingmoisha sharmaNoch keine Bewertungen

- Sterling & Wilson Solar LTD - Company Profile, Issue Details, Balance Sheet & Key Ratios - Angel BrokingDokument6 SeitenSterling & Wilson Solar LTD - Company Profile, Issue Details, Balance Sheet & Key Ratios - Angel Brokingmoisha sharmaNoch keine Bewertungen

- Prince Pipes & Fittings Limited - Company Profile, Issue Details, Balance Sheet & Key Ratios - Angel BrokingDokument8 SeitenPrince Pipes & Fittings Limited - Company Profile, Issue Details, Balance Sheet & Key Ratios - Angel Brokingmoisha sharmaNoch keine Bewertungen

- Ujjivan Small Finance Bank - Company Profile, Issue Details, Balance Sheet & Key Ratios - Angel BrokingDokument7 SeitenUjjivan Small Finance Bank - Company Profile, Issue Details, Balance Sheet & Key Ratios - Angel Brokingmoisha sharmaNoch keine Bewertungen

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5782)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (587)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (72)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (265)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (119)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Icici Prudential Asset Management Company LTD.: Revision and Practice Test Kit Version 3Dokument21 SeitenIcici Prudential Asset Management Company LTD.: Revision and Practice Test Kit Version 3Neeraj KumarNoch keine Bewertungen

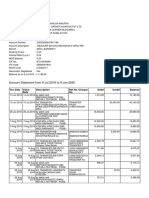

- Account Statement From 9 Jul 2019 To 9 Jan 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDokument4 SeitenAccount Statement From 9 Jul 2019 To 9 Jan 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalancemauryapiaeNoch keine Bewertungen

- Contract of Indemnity and Law of GuaranteeDokument7 SeitenContract of Indemnity and Law of GuaranteeBilawal Mughal100% (1)

- Deutsche Postbank: Broad Deployment of Sap For Banking Smooths IntegrationDokument4 SeitenDeutsche Postbank: Broad Deployment of Sap For Banking Smooths IntegrationErich BasurtoNoch keine Bewertungen

- Business Week Global1000 AlphaDokument2 SeitenBusiness Week Global1000 Alphapolly1221Noch keine Bewertungen

- Case Study - Contract Part 1Dokument5 SeitenCase Study - Contract Part 1Như NgôNoch keine Bewertungen

- ch04 Fundamental of Financial Accounting by Edmonds (4th Edition)Dokument79 Seitench04 Fundamental of Financial Accounting by Edmonds (4th Edition)Awais AzeemiNoch keine Bewertungen

- Accounting Fraud: A Study On Sonali Bank Limited (Hallmark) ScamDokument42 SeitenAccounting Fraud: A Study On Sonali Bank Limited (Hallmark) Scammunatasneem94% (17)

- Audit Evidence PDFDokument47 SeitenAudit Evidence PDFEsa SulyNoch keine Bewertungen

- Supreme Court Nazul OrdersDokument44 SeitenSupreme Court Nazul OrdersSparkNoch keine Bewertungen

- Audit 1Dokument11 SeitenAudit 1zarfarie aron100% (2)

- Specialized Loan Servicing Charges $250 For A Refi, and $125 For A Loan ModDokument4 SeitenSpecialized Loan Servicing Charges $250 For A Refi, and $125 For A Loan ModTim BryantNoch keine Bewertungen

- AFM Study Support Guide: Plan Prepare PassDokument26 SeitenAFM Study Support Guide: Plan Prepare PassSarah SeeNoch keine Bewertungen

- NISM Certifications List All SerisesDokument3 SeitenNISM Certifications List All SerisesSayantan Munna PaulNoch keine Bewertungen

- Work Life BalanceDokument69 SeitenWork Life BalanceSagar Paul'gNoch keine Bewertungen

- Indemnity and GuaranteeDokument22 SeitenIndemnity and Guaranteeakkig150% (2)

- Review Questions: Chart of AccountsDokument4 SeitenReview Questions: Chart of AccountsHasan NajiNoch keine Bewertungen

- SBI History and OperationsDokument54 SeitenSBI History and OperationsaanchaliyaNoch keine Bewertungen

- Residence and Travel Questionnaire: Tataaia/Nb/Dm/126Dokument2 SeitenResidence and Travel Questionnaire: Tataaia/Nb/Dm/126Data CentrumNoch keine Bewertungen

- Organizational Structure ofDokument16 SeitenOrganizational Structure ofakanksha singhNoch keine Bewertungen

- Audit of Accounting Changes and Correction of ErrorsDokument24 SeitenAudit of Accounting Changes and Correction of ErrorsHarvey Dienne Quiambao90% (10)

- Law Project - The Negotiable Instrument Act - RevisedV1Dokument48 SeitenLaw Project - The Negotiable Instrument Act - RevisedV1Teena Varma100% (3)

- Launch Presentation Zim Consumer 2011 FINAL PDFDokument52 SeitenLaunch Presentation Zim Consumer 2011 FINAL PDFKristi DuranNoch keine Bewertungen

- Ivd STF 2Dokument2 SeitenIvd STF 2ChakriNoch keine Bewertungen

- External Sector: Chapter-11Dokument17 SeitenExternal Sector: Chapter-11ShafarudinNoch keine Bewertungen

- Bajaj Allianz General Insurance CompanyDokument12 SeitenBajaj Allianz General Insurance CompanymkbhimaniNoch keine Bewertungen

- International Banks: Preyanth T KDokument8 SeitenInternational Banks: Preyanth T KnofaNoch keine Bewertungen

- Certificate in Insurance: Unit 1 - Insurance, Legal and RegulatoryDokument29 SeitenCertificate in Insurance: Unit 1 - Insurance, Legal and RegulatorytamzNoch keine Bewertungen

- M'sian Resources Corp Berhad: Construction and Property Development Activities Gather Momentum in 1QFY12/10 - 19/5/2010Dokument4 SeitenM'sian Resources Corp Berhad: Construction and Property Development Activities Gather Momentum in 1QFY12/10 - 19/5/2010Rhb InvestNoch keine Bewertungen

- Account Statement: From 2023/02/01 To 2023/02/28Dokument4 SeitenAccount Statement: From 2023/02/01 To 2023/02/28mohamed desoukiNoch keine Bewertungen