Das könnte Ihnen auch gefallen

- 10 Science Notes 06 Life Processes 1Dokument12 Seiten10 Science Notes 06 Life Processes 1All Rounder HindustanNoch keine Bewertungen

- Extra Questions-ElectricityDokument2 SeitenExtra Questions-ElectricityCorey PageNoch keine Bewertungen

- 12.3 QB-q3Dokument5 Seiten12.3 QB-q3Corey PageNoch keine Bewertungen

- Test Human EyeDokument1 SeiteTest Human EyeCorey PageNoch keine Bewertungen

- E.G. Bacterium NitrosomonasDokument1 SeiteE.G. Bacterium NitrosomonasCorey PageNoch keine Bewertungen

- Test ElectricityDokument12 SeitenTest ElectricityCorey PageNoch keine Bewertungen

- Notes-Winds, Storms and CyclonesDokument5 SeitenNotes-Winds, Storms and CyclonesCorey PageNoch keine Bewertungen

- Behavioural Skills-4 PDFDokument24 SeitenBehavioural Skills-4 PDFPragati VatsaNoch keine Bewertungen

- Tense-Mixed ExerciseDokument2 SeitenTense-Mixed ExerciseCorey PageNoch keine Bewertungen

- Test WindsDokument1 SeiteTest WindsCorey PageNoch keine Bewertungen

- Chapter 8 Winds Storms and CyclonesDokument19 SeitenChapter 8 Winds Storms and CyclonesCorey PageNoch keine Bewertungen

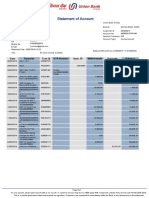

- OpTransactionHistoryUX3 - PDF02 07 2019Dokument1 SeiteOpTransactionHistoryUX3 - PDF02 07 2019Corey PageNoch keine Bewertungen

- 7 Challenges - A Workbook On CommunicationsDokument104 Seiten7 Challenges - A Workbook On CommunicationsRaj100% (2)

- Exercise Questions-Winds, CycloneDokument5 SeitenExercise Questions-Winds, CycloneCorey PageNoch keine Bewertungen

- Subham Bhaiya 5 PDFDokument31 SeitenSubham Bhaiya 5 PDFRazor RockNoch keine Bewertungen

- Stress Analysis On Hotel Employees PDFDokument12 SeitenStress Analysis On Hotel Employees PDFCorey PageNoch keine Bewertungen

- READMEDokument1 SeiteREADMESuyog TangadkarNoch keine Bewertungen

- IBC 301 Question Bank - Hindi 2017-18Dokument5 SeitenIBC 301 Question Bank - Hindi 2017-18Corey PageNoch keine Bewertungen

- Gold Monetization Scheme 150703111313 Lva1 App6891Dokument25 SeitenGold Monetization Scheme 150703111313 Lva1 App6891Corey PageNoch keine Bewertungen

- Synopsis GSTDokument16 SeitenSynopsis GSTCorey PageNoch keine Bewertungen

- New QUESTIONNAIRE OF EMPLOYEE WELFARE MEASURES 1Dokument4 SeitenNew QUESTIONNAIRE OF EMPLOYEE WELFARE MEASURES 1Corey Page100% (1)

- Principles & Practices of BankingDokument33 SeitenPrinciples & Practices of BankingPritam BhadadeNoch keine Bewertungen

- Balance of Payment (BOP)Dokument35 SeitenBalance of Payment (BOP)Ritick KannaNoch keine Bewertungen

- BankingDokument153 SeitenBankingBijit KarmakarNoch keine Bewertungen

- RMDokument7 SeitenRMCorey PageNoch keine Bewertungen

- Ecological Solid Waste Management Act of PDFDokument35 SeitenEcological Solid Waste Management Act of PDFCorey Page100% (1)

- Roles of Government in Business1214Dokument21 SeitenRoles of Government in Business1214Corey PageNoch keine Bewertungen

- Types of PlanningDokument14 SeitenTypes of PlanningCorey Page100% (2)

- Presentation 1Dokument19 SeitenPresentation 1Corey PageNoch keine Bewertungen

- Blue Sky & Red SunsetsDokument15 SeitenBlue Sky & Red SunsetsCorey PageNoch keine Bewertungen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (73)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (120)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Home Quiz Partnership AccountingDokument3 SeitenHome Quiz Partnership AccountingKeith Anthony AmorNoch keine Bewertungen

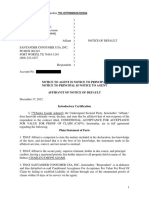

- Affidavit and Notice of Default - Sample-A4vDokument3 SeitenAffidavit and Notice of Default - Sample-A4vsparkled34100% (6)

- Midterm Examination For AC11N: ProblemDokument1 SeiteMidterm Examination For AC11N: ProblemLeica JaymeNoch keine Bewertungen

- BCE: INC Case AnalysisDokument6 SeitenBCE: INC Case AnalysisShuja Ur RahmanNoch keine Bewertungen

- Debit AccountancyDokument33 SeitenDebit AccountancyJuancho Miguel0% (1)

- Exercise - Dilutive Securities - AdillaikhsaniDokument4 SeitenExercise - Dilutive Securities - Adillaikhsaniaidil fikri ikhsan100% (1)

- Mini Project On Insurance NewDokument18 SeitenMini Project On Insurance NewRomil SodhiyaNoch keine Bewertungen

- Financing Current AssetsDokument9 SeitenFinancing Current Assetspbelim100% (1)

- Statuatory ComplianceDokument9 SeitenStatuatory Compliancescribd5378Noch keine Bewertungen

- Earnest Money Receipt AgreementDokument5 SeitenEarnest Money Receipt AgreementLeticia R. Tuadles0% (1)

- AFAR-02 Corporate LiquidationDokument2 SeitenAFAR-02 Corporate LiquidationRamainne RonquilloNoch keine Bewertungen

- Self Help Groups (SHGS) in India: Ethiopian DelegationDokument10 SeitenSelf Help Groups (SHGS) in India: Ethiopian DelegationKamal DeenNoch keine Bewertungen

- Bank of England Summary HaircutsDokument1 SeiteBank of England Summary HaircutsRoss80Noch keine Bewertungen

- Sun Microsystems Case StudyDokument17 SeitenSun Microsystems Case StudyJosh Krisha100% (3)

- Lehman - Index Arbitrage - A PrimerDokument6 SeitenLehman - Index Arbitrage - A Primerleetaibai100% (1)

- Commercial Bank PDFDokument13 SeitenCommercial Bank PDFTanhaNoch keine Bewertungen

- Ualification Nit Number and Title: Earning Outcome and Assessment CriteriaDokument9 SeitenUalification Nit Number and Title: Earning Outcome and Assessment CriteriaZainab ShahidNoch keine Bewertungen

- IA2 02 - Handout - 1 PDFDokument10 SeitenIA2 02 - Handout - 1 PDFMelchie RepospoloNoch keine Bewertungen

- Negotiation of Hotel Management AgreementsDokument14 SeitenNegotiation of Hotel Management AgreementsCalvawell MuzvondiwaNoch keine Bewertungen

- DEPOSITED SCHEMES OF SUCO CO-OPERATIVE BANK PampapathiDokument58 SeitenDEPOSITED SCHEMES OF SUCO CO-OPERATIVE BANK PampapathiHasan shaikhNoch keine Bewertungen

- Lecture-3 On Classification of IncomeDokument14 SeitenLecture-3 On Classification of Incomeimdadul haqueNoch keine Bewertungen

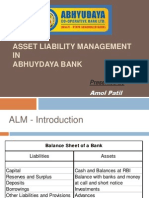

- Asset Liability Management IN Abhuydaya Bank: Amol PatilDokument14 SeitenAsset Liability Management IN Abhuydaya Bank: Amol Patilpari0000Noch keine Bewertungen

- Functions of RbiDokument4 SeitenFunctions of RbiMunish PathaniaNoch keine Bewertungen

- 501 C 3Dokument26 Seiten501 C 3api-370055350% (2)

- Form No. 16: Part ADokument2 SeitenForm No. 16: Part AasifNoch keine Bewertungen

- Federal Income Tax OUTLINEDokument22 SeitenFederal Income Tax OUTLINErufus.kingslee3327100% (7)

- HDFC Bank Credit Cards GSTIN: 33AAACH2702H2Z6 HSN Code - 9971Dokument1 SeiteHDFC Bank Credit Cards GSTIN: 33AAACH2702H2Z6 HSN Code - 9971Kuldeep SheoranNoch keine Bewertungen

- MEMORANDUM OF AGREEMENT DraftsDokument3 SeitenMEMORANDUM OF AGREEMENT DraftsRichard Colunga80% (5)

- Activity Sheet in Business Enterprise SimulationDokument8 SeitenActivity Sheet in Business Enterprise SimulationAimee Lasaca100% (1)

- A Research Project On Impact of FII: On Money MarketDokument9 SeitenA Research Project On Impact of FII: On Money Marketsamruddhi_khaleNoch keine Bewertungen