Das könnte Ihnen auch gefallen

- 1Dokument11 Seiten1nayak_gajananaNoch keine Bewertungen

- Vranda Statement PDFDokument7 SeitenVranda Statement PDFvarun raghuveerNoch keine Bewertungen

- Gmail - PSG PDFDokument1 SeiteGmail - PSG PDFJehangir Allam100% (2)

- SUDHIR 1DZIRE VxiDokument2 SeitenSUDHIR 1DZIRE VxiEIL RFCLNoch keine Bewertungen

- D JavaApps EMAIL-SERVERv1 (1) .1 Temp 111116095854219Dokument2 SeitenD JavaApps EMAIL-SERVERv1 (1) .1 Temp 111116095854219amardeepjassal85Noch keine Bewertungen

- PDFDokument22 SeitenPDFAnonymous ccPU4fNoch keine Bewertungen

- Sample Bank StatementDokument9 SeitenSample Bank Statementemma adeoyeNoch keine Bewertungen

- Archana V Offfer LetterDokument10 SeitenArchana V Offfer LetterKetsyNoch keine Bewertungen

- 1571988702732Dokument33 Seiten1571988702732LS GUPTANoch keine Bewertungen

- Offer Letter GBDokument1 SeiteOffer Letter GBHarshitBhargavaNoch keine Bewertungen

- ., I.K.Gujral Punjab Technical UniversityDokument2 Seiten., I.K.Gujral Punjab Technical UniversityParth SharmaNoch keine Bewertungen

- PDF 816776770290723Dokument1 SeitePDF 816776770290723Sunita SinghNoch keine Bewertungen

- T12604121120044450 SoadDokument4 SeitenT12604121120044450 Soadnitu kumariNoch keine Bewertungen

- Manish Kumar - Appointment LetterDokument4 SeitenManish Kumar - Appointment Letterak4784449Noch keine Bewertungen

- Anuj ASAPM2826N ITR-VDokument1 SeiteAnuj ASAPM2826N ITR-Vapi-27088128Noch keine Bewertungen

- 914010004015551 (5)Dokument3 Seiten914010004015551 (5)Eureka KashyapNoch keine Bewertungen

- Indusind BankDokument65 SeitenIndusind BankNadeem KhanNoch keine Bewertungen

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDokument5 SeitenStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceAmit GodaraNoch keine Bewertungen

- COMPANY REGISTRATION - CompressedDokument2 SeitenCOMPANY REGISTRATION - CompressedPunjab SinghNoch keine Bewertungen

- Offer Letter SampleDokument2 SeitenOffer Letter Sampleyevadimata vinakuNoch keine Bewertungen

- LIC Premium 2016 PDFDokument1 SeiteLIC Premium 2016 PDFRakesh KumarNoch keine Bewertungen

- Rochak Agrawal-Offer PDFDokument4 SeitenRochak Agrawal-Offer PDFrochak agrawalNoch keine Bewertungen

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDokument2 SeitenStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing Balanceravi_seth_9Noch keine Bewertungen

- Deposit Confirmation/Renewal AdviceDokument1 SeiteDeposit Confirmation/Renewal Advicekunal singhNoch keine Bewertungen

- Anamita Basu Human Resources: For Any Query Pls - ContactDokument1 SeiteAnamita Basu Human Resources: For Any Query Pls - Contactkushlesh jamuarNoch keine Bewertungen

- Indian Income Tax Return Acknowledgement: Do Not Send This Acknowledgement To CPC, BengaluruDokument1 SeiteIndian Income Tax Return Acknowledgement: Do Not Send This Acknowledgement To CPC, BengaluruRoshanjit ThakurNoch keine Bewertungen

- GST Certificate - Pandurang SambhudasDokument3 SeitenGST Certificate - Pandurang SambhudasPandurang sambhudasNoch keine Bewertungen

- Central Board of Secondary Education: Result: PassDokument1 SeiteCentral Board of Secondary Education: Result: PassYashNoch keine Bewertungen

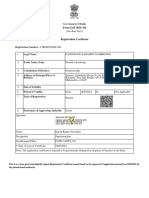

- Registration CertificateDokument1 SeiteRegistration CertificateLuckyGuptaNoch keine Bewertungen

- House No 1073 Sector 43 B Chandigarh Sector 22 Chandigarh CHANDIGARH - CHA - 160022 Chandigarh, IndiaDokument1 SeiteHouse No 1073 Sector 43 B Chandigarh Sector 22 Chandigarh CHANDIGARH - CHA - 160022 Chandigarh, IndiamanishaNoch keine Bewertungen

- Appt of Biswajit Bhuiya PDFDokument313 SeitenAppt of Biswajit Bhuiya PDFsurajit maiti100% (1)

- Statement of Assets and Liabilities As On - (This Form Should Be Obtained From Borrower / Co-Borrower/guarantors)Dokument4 SeitenStatement of Assets and Liabilities As On - (This Form Should Be Obtained From Borrower / Co-Borrower/guarantors)Raghu Veer100% (1)

- Appointment LetterDokument3 SeitenAppointment Letterpoonam shuklaNoch keine Bewertungen

- Releving Letter OMHDokument2 SeitenReleving Letter OMHmass100% (1)

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDokument7 SeitenStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceGagan Sales Agencies SunamNoch keine Bewertungen

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDokument1 SeiteStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing Balancesandip nagareNoch keine Bewertungen

- 2Dokument2 Seiten2Arun KumarNoch keine Bewertungen

- Provisional Tax Saving Fixed Deposit Confirmation AdviceDokument3 SeitenProvisional Tax Saving Fixed Deposit Confirmation AdviceKunda MalleshNoch keine Bewertungen

- Account Statement From 1 Jan 2012 To 30 Jun 2012: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDokument3 SeitenAccount Statement From 1 Jan 2012 To 30 Jun 2012: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceRavi AgarwalNoch keine Bewertungen

- Bank StatementDokument1 SeiteBank StatementDasari RavikiranNoch keine Bewertungen

- Account Statement For Account:2962002100013400: Branch DetailsDokument3 SeitenAccount Statement For Account:2962002100013400: Branch DetailsBest Auto TechNoch keine Bewertungen

- No Objection Cerificate ApplicationDokument4 SeitenNo Objection Cerificate ApplicationSelvaArockiamNoch keine Bewertungen

- Acctstmt FDokument3 SeitenAcctstmt FAbhay SinghNoch keine Bewertungen

- Bank DetailsDokument11 SeitenBank DetailsANANDA MAITYNoch keine Bewertungen

- VK TradersDokument16 SeitenVK TradersMOHAN ChandNoch keine Bewertungen

- Step Transaction Acknowledgment: SuccessDokument1 SeiteStep Transaction Acknowledgment: Success@nshu_theachieverNoch keine Bewertungen

- Ankit MishraDokument7 SeitenAnkit MishraRähûl Prätäp SïnghNoch keine Bewertungen

- Income From Salaries: Rs. Rs. Rs. SCH - NoDokument2 SeitenIncome From Salaries: Rs. Rs. Rs. SCH - Nosrinivas maguluriNoch keine Bewertungen

- Offer Letter - Akash Gupta PDFDokument4 SeitenOffer Letter - Akash Gupta PDFkaushal vermaNoch keine Bewertungen

- Indian Income Tax Return Acknowledgement: Name of Premises/Building/VillageDokument1 SeiteIndian Income Tax Return Acknowledgement: Name of Premises/Building/VillagesamaadhuNoch keine Bewertungen

- Provisional Certificate0230Dokument1 SeiteProvisional Certificate0230Neduri KalyanNoch keine Bewertungen

- Salary Slip (31692031 April, 2019) PDFDokument1 SeiteSalary Slip (31692031 April, 2019) PDFMuhammad AdnanNoch keine Bewertungen

- 910010041067322 (1)Dokument2 Seiten910010041067322 (1)MiteshSuneriyaNoch keine Bewertungen

- HDFC YsDokument2 SeitenHDFC YsAkshat ShahNoch keine Bewertungen

- NOC Letter For Name Change (From Previous Owner)Dokument1 SeiteNOC Letter For Name Change (From Previous Owner)Gurdeep SinghNoch keine Bewertungen

- Excel Salary Slip Format DownloadDokument2 SeitenExcel Salary Slip Format DownloadNandgulabDeshmukhNoch keine Bewertungen

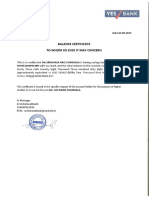

- Yes Bank Interest CertificateDokument1 SeiteYes Bank Interest CertificateSourabh PunshiNoch keine Bewertungen

- Offer Latter DraftDokument3 SeitenOffer Latter DraftHimanshu1712Noch keine Bewertungen

- SUPERCARD Most Important Terms and Conditions (MITC)Dokument17 SeitenSUPERCARD Most Important Terms and Conditions (MITC)jinesh vgNoch keine Bewertungen

- Supercard Most Important Terms and ConditionsDokument26 SeitenSupercard Most Important Terms and Conditionstauseef21scribdNoch keine Bewertungen

- Airtel Channel ListDokument3 SeitenAirtel Channel ListorekishNoch keine Bewertungen

- Oasis of Stillness PDF - Google SearchDokument3 SeitenOasis of Stillness PDF - Google SearchorekishNoch keine Bewertungen

- Arm I LlariaDokument2 SeitenArm I LlariaorekishNoch keine Bewertungen

- T. Shanmugham - WikipediaDokument1 SeiteT. Shanmugham - WikipediaorekishNoch keine Bewertungen

- Mrugaraju - WikipediaDokument5 SeitenMrugaraju - WikipediaorekishNoch keine Bewertungen

- Enlightenment Without God Swami Rama PDFDokument75 SeitenEnlightenment Without God Swami Rama PDForekishNoch keine Bewertungen

- Shiva Svarodaya Text With English Translation Ram Kumar Rai PDFDokument112 SeitenShiva Svarodaya Text With English Translation Ram Kumar Rai PDForekish100% (2)

- Vedic Astrology Diary 2006-03-07 - The Double Transit in Timing MarriageDokument2 SeitenVedic Astrology Diary 2006-03-07 - The Double Transit in Timing Marriageorekish100% (2)

- MySQL Database of Indian Cities and States, Latitude and Longitude.. GitHubDokument16 SeitenMySQL Database of Indian Cities and States, Latitude and Longitude.. GitHuborekishNoch keine Bewertungen

- Shaktanand: Shiv Swarodaya: Some Interesting AspectsDokument12 SeitenShaktanand: Shiv Swarodaya: Some Interesting AspectsorekishNoch keine Bewertungen

- Aghora at The Left Hand of GodDokument167 SeitenAghora at The Left Hand of Godorekish95% (21)

- Why The Strengths Are Interesting?: FormulationDokument5 SeitenWhy The Strengths Are Interesting?: FormulationTang Zhen HaoNoch keine Bewertungen

- Industry Analysis: Liquidity RatioDokument10 SeitenIndustry Analysis: Liquidity RatioTayyaub khalidNoch keine Bewertungen

- The Possibility of Making An Umbrella and Raincoat in A Plastic WrapperDokument15 SeitenThe Possibility of Making An Umbrella and Raincoat in A Plastic WrapperMadelline B. TamayoNoch keine Bewertungen

- Global Supply Chain Planning at IKEA: ArticleDokument15 SeitenGlobal Supply Chain Planning at IKEA: ArticleyashNoch keine Bewertungen

- Brita. SWOTDokument21 SeitenBrita. SWOTNarayan TiwariNoch keine Bewertungen

- Modern Money and Banking BookDokument870 SeitenModern Money and Banking BookRao Abdur Rehman100% (6)

- Exim BankDokument79 SeitenExim Banklaxmi sambre0% (1)

- Correlations in Forex Pairs SHEET by - YouthFXRisingDokument2 SeitenCorrelations in Forex Pairs SHEET by - YouthFXRisingprathamgamer147Noch keine Bewertungen

- Presentation NGODokument6 SeitenPresentation NGODulani PinkyNoch keine Bewertungen

- Intellectual Property RightsDokument2 SeitenIntellectual Property RightsPuralika MohantyNoch keine Bewertungen

- Nissan Leaf - The Bulletin, March 2011Dokument2 SeitenNissan Leaf - The Bulletin, March 2011belgianwafflingNoch keine Bewertungen

- 2017 Metrobank - Mtap Deped Math Challenge Elimination Round Grade 2 Time Allotment: 60 MinDokument2 Seiten2017 Metrobank - Mtap Deped Math Challenge Elimination Round Grade 2 Time Allotment: 60 MinElla David100% (1)

- Ape TermaleDokument64 SeitenApe TermaleTeodora NedelcuNoch keine Bewertungen

- De Mgginimis Benefit in The PhilippinesDokument3 SeitenDe Mgginimis Benefit in The PhilippinesSlardarRadralsNoch keine Bewertungen

- Ifland Engineers, Inc.-Civil Engineers - RedactedDokument18 SeitenIfland Engineers, Inc.-Civil Engineers - RedactedL. A. PatersonNoch keine Bewertungen

- Alcor's Impending Npo FailureDokument11 SeitenAlcor's Impending Npo FailureadvancedatheistNoch keine Bewertungen

- RMC 46-99Dokument7 SeitenRMC 46-99mnyng100% (1)

- Fatigue Crack Growth Behavior of JIS SCM440 Steel N 2017 International JournDokument13 SeitenFatigue Crack Growth Behavior of JIS SCM440 Steel N 2017 International JournSunny SinghNoch keine Bewertungen

- TIPS As An Asset Class: Final ApprovalDokument9 SeitenTIPS As An Asset Class: Final ApprovalMJTerrienNoch keine Bewertungen

- Session 2Dokument73 SeitenSession 2Sankit Mohanty100% (1)

- 2023 DPWH Standard List of Pay Items Volume II DO 6 s2023Dokument103 Seiten2023 DPWH Standard List of Pay Items Volume II DO 6 s2023Alaiza Mae Gumba100% (1)

- Project On SurveyorsDokument40 SeitenProject On SurveyorsamitNoch keine Bewertungen

- GST Rate-: Type of Vehicle GST Rate Compensation Cess Total Tax PayableDokument3 SeitenGST Rate-: Type of Vehicle GST Rate Compensation Cess Total Tax PayableAryanNoch keine Bewertungen

- Ekspedisi Central - Google SearchDokument1 SeiteEkspedisi Central - Google SearchSketch DevNoch keine Bewertungen

- Scheme For CBCS Curriculum For B. A Pass CourseDokument18 SeitenScheme For CBCS Curriculum For B. A Pass CourseSumanNoch keine Bewertungen

- Year 2016Dokument15 SeitenYear 2016fahadullahNoch keine Bewertungen

- Econ 140 Chapter1Dokument5 SeitenEcon 140 Chapter1Aysha AbdulNoch keine Bewertungen

- Microsoft Word - CHAPTER - 05 - DEPOSITS - IN - BANKSDokument8 SeitenMicrosoft Word - CHAPTER - 05 - DEPOSITS - IN - BANKSDuy Trần TấnNoch keine Bewertungen

- Quasha, Asperilla, Ancheta, Peña, Valmonte & Marcos For Respondent British AirwaysDokument12 SeitenQuasha, Asperilla, Ancheta, Peña, Valmonte & Marcos For Respondent British Airwaysbabyclaire17Noch keine Bewertungen

- NaftaDokument18 SeitenNaftaShabla MohamedNoch keine Bewertungen