Das könnte Ihnen auch gefallen

- The Driving Force Behind The Boom and Bust in Construction in EuropeDokument36 SeitenThe Driving Force Behind The Boom and Bust in Construction in EuropecaitlynharveyNoch keine Bewertungen

- EUROPEAN COMMISSION COUNTRY REPORT ON BELGIUM 2015Dokument89 SeitenEUROPEAN COMMISSION COUNTRY REPORT ON BELGIUM 2015Ilias MansouriNoch keine Bewertungen

- The Economic Benefits of Cloud Computing To Business and The Wider EMEA EconomyDokument89 SeitenThe Economic Benefits of Cloud Computing To Business and The Wider EMEA EconomyEmilio Notareschi100% (1)

- Investment Report 2022/2023 - Key Findings: Resilience and renewal in EuropeVon EverandInvestment Report 2022/2023 - Key Findings: Resilience and renewal in EuropeNoch keine Bewertungen

- Deuda Pública en UEDokument4 SeitenDeuda Pública en UEelenaNoch keine Bewertungen

- Globale Electronic IndustryDokument15 SeitenGlobale Electronic IndustryMehfooz AnsariNoch keine Bewertungen

- 20-12-21 Background Paper - Infrastructure Sharing and Co-Deployment in Europe - Final - v2 - (Clean)Dokument30 Seiten20-12-21 Background Paper - Infrastructure Sharing and Co-Deployment in Europe - Final - v2 - (Clean)Catalina GrigoreNoch keine Bewertungen

- EN EN: European CommissionDokument19 SeitenEN EN: European CommissionaNoch keine Bewertungen

- Hourly Labour Costs Ranged From 5.4 To 43.5 Across The EU Member States in 2018Dokument4 SeitenHourly Labour Costs Ranged From 5.4 To 43.5 Across The EU Member States in 2018vengadeshNoch keine Bewertungen

- Germany's Low Debt Level and Investment in 5G NetworksDokument7 SeitenGermany's Low Debt Level and Investment in 5G NetworksericNoch keine Bewertungen

- Banco Sabadell CEO Discusses Economic Outlook and Bank FundamentalsDokument35 SeitenBanco Sabadell CEO Discusses Economic Outlook and Bank FundamentalsseyviarNoch keine Bewertungen

- Ict For Growth: A Targeted Approach: PolicyDokument11 SeitenIct For Growth: A Targeted Approach: PolicyBruegelNoch keine Bewertungen

- Industry 4.0: The Digital German Ideology: Christian FuchsDokument10 SeitenIndustry 4.0: The Digital German Ideology: Christian FuchsAnna RodinaNoch keine Bewertungen

- A Computable General Equilibrium Modeling Platform For The Azorean Economy: A Simple Approach With International TradeDokument24 SeitenA Computable General Equilibrium Modeling Platform For The Azorean Economy: A Simple Approach With International TradeFrancisco SilvaNoch keine Bewertungen

- The 2012 EU Industrial R&D ScoreboardDokument126 SeitenThe 2012 EU Industrial R&D ScoreboardM3pHNoch keine Bewertungen

- Comp Mech Eng 2012 Sum - enDokument26 SeitenComp Mech Eng 2012 Sum - enLjubomir FilipovskiNoch keine Bewertungen

- GermanyDokument52 SeitenGermanyMinh Trần Bảo NgọcNoch keine Bewertungen

- Digitalisation in Europe 2022-2023: Evidence from the EIB Investment SurveyVon EverandDigitalisation in Europe 2022-2023: Evidence from the EIB Investment SurveyNoch keine Bewertungen

- Construction Industry in Germany: Structural Data On Production and EmploymentDokument10 SeitenConstruction Industry in Germany: Structural Data On Production and EmploymentShilpa AgrawalNoch keine Bewertungen

- Technology Focus On Cloud ComputingDokument41 SeitenTechnology Focus On Cloud Computingkamal waniNoch keine Bewertungen

- PIGS Countries' New Challenges Under Europe 2020 Strategy: Danubius University of Galati, Faculty of EconomicsDokument10 SeitenPIGS Countries' New Challenges Under Europe 2020 Strategy: Danubius University of Galati, Faculty of EconomicsЕлизавета МиняйленкоNoch keine Bewertungen

- 2010 Annual Economic Report at a GlanceDokument3 Seiten2010 Annual Economic Report at a Glanceurz_spiderman2630Noch keine Bewertungen

- Indicators For Measuring ICT AccessDokument19 SeitenIndicators For Measuring ICT AccessmingesNoch keine Bewertungen

- Research Innovation Performance: ItalyDokument14 SeitenResearch Innovation Performance: ItalyionpetaNoch keine Bewertungen

- Session 3 - ICT - ProductiivtyDokument15 SeitenSession 3 - ICT - ProductiivtyMuhammad AbdullahNoch keine Bewertungen

- MACRO ECONOMIC THEORY AND POLICY CIA 1 ConvDokument20 SeitenMACRO ECONOMIC THEORY AND POLICY CIA 1 ConvAastha SinghNoch keine Bewertungen

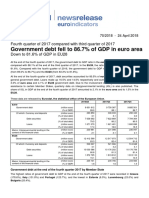

- Government Debt Fell To 86.7% of GDP in Euro Area: Fourth Quarter of 2017 Compared With Third Quarter of 2017Dokument4 SeitenGovernment Debt Fell To 86.7% of GDP in Euro Area: Fourth Quarter of 2017 Compared With Third Quarter of 2017Alyss AlysikNoch keine Bewertungen

- Ede 1112Dokument60 SeitenEde 1112javierodNoch keine Bewertungen

- Energy Efficiency NetherlandsDokument20 SeitenEnergy Efficiency NetherlandsJean Briham Pardo BaqueroNoch keine Bewertungen

- Term Paper: Topic: The Internal Economic Problems in ItalyDokument28 SeitenTerm Paper: Topic: The Internal Economic Problems in ItalyДаня РезикNoch keine Bewertungen

- Researchers' Report 2013: Country Profile: ItalyDokument10 SeitenResearchers' Report 2013: Country Profile: ItalyDristorXelaNoch keine Bewertungen

- 9708 - s12 - QP - 41 - Case Study ResponseDokument7 Seiten9708 - s12 - QP - 41 - Case Study ResponseZainab SiddiqueNoch keine Bewertungen

- EIB Group activity in EU cohesion regions 2022Von EverandEIB Group activity in EU cohesion regions 2022Noch keine Bewertungen

- A Review of International Mobile Roaming To December 2011: Ewan SutherlandDokument17 SeitenA Review of International Mobile Roaming To December 2011: Ewan SutherlandAnna XpNoch keine Bewertungen

- Reinforcing CompetitivenessDokument7 SeitenReinforcing CompetitivenessEKAI CenterNoch keine Bewertungen

- Energy 2012Q1 - ChinaDokument13 SeitenEnergy 2012Q1 - ChinaTerry LiNoch keine Bewertungen

- Implicaciones A Largo Plazo de La Revolución de Las TIC Aplicación de Las Lecciones de La Teoría Del Crecimiento y La Contabilidad Del CrecimientoDokument15 SeitenImplicaciones A Largo Plazo de La Revolución de Las TIC Aplicación de Las Lecciones de La Teoría Del Crecimiento y La Contabilidad Del CrecimientoAkira Shiroma YaipenNoch keine Bewertungen

- GermanyDokument58 SeitenGermanyMinh Trần Bảo NgọcNoch keine Bewertungen

- Executive SummaryDokument15 SeitenExecutive SummaryGeorgeZlatkoffNoch keine Bewertungen

- Itallian Regulatory AuthorityDokument50 SeitenItallian Regulatory AuthorityJames OmaraNoch keine Bewertungen

- Paradigms of the e-Economy: Opportunities for RomaniaDokument8 SeitenParadigms of the e-Economy: Opportunities for RomaniaRaluca LauraNoch keine Bewertungen

- Technology Focus On Artificial IntelligenceDokument38 SeitenTechnology Focus On Artificial Intelligencekamal waniNoch keine Bewertungen

- Soitec Announces Full Year Results For 2011-2012Dokument11 SeitenSoitec Announces Full Year Results For 2011-2012Lachlan MarkayNoch keine Bewertungen

- The Challenge of Digital Transformation in The Automotive Industry-2020Dokument180 SeitenThe Challenge of Digital Transformation in The Automotive Industry-2020DoveNoch keine Bewertungen

- Industria 4.0 InglesDokument10 SeitenIndustria 4.0 InglesFernando Gandolfo PérezNoch keine Bewertungen

- Managing Business Finance AssignmentDokument21 SeitenManaging Business Finance Assignmentjerrygmathew100% (1)

- Broadband 2011Dokument119 SeitenBroadband 2011amedinagomez3857Noch keine Bewertungen

- European Competitiveness Report 2012Dokument236 SeitenEuropean Competitiveness Report 2012Luis OliveiraNoch keine Bewertungen

- Fiscal Challenges To Euro ZoneDokument18 SeitenFiscal Challenges To Euro Zonepayal sachdevNoch keine Bewertungen

- The Eurozone CrisisDokument39 SeitenThe Eurozone CrisisPetros NikolaouNoch keine Bewertungen

- BMW - StrategyDokument12 SeitenBMW - StrategyArup SarkarNoch keine Bewertungen

- EOCIC Priority Sector Report - Mobility TechnologiesDokument31 SeitenEOCIC Priority Sector Report - Mobility TechnologiesVip ShoesNoch keine Bewertungen

- Macro Economic Impacts of EU SF To New MSsDokument34 SeitenMacro Economic Impacts of EU SF To New MSsAleksandra AnticNoch keine Bewertungen

- Germany Country Risk AnalysisDokument22 SeitenGermany Country Risk Analysisamitsharma_acdsNoch keine Bewertungen

- Financing the digitalisation of small and medium-sized enterprises: The enabling role of digital innovation hubsVon EverandFinancing the digitalisation of small and medium-sized enterprises: The enabling role of digital innovation hubsNoch keine Bewertungen

- ROK Silicon Europe - January 2012Dokument7 SeitenROK Silicon Europe - January 2012SiliconEuropeNoch keine Bewertungen

- ADL StrategicChoiceDokument56 SeitenADL StrategicChoiceABCDNoch keine Bewertungen

- Orange Reports Solid Q1 2012 Results Despite Market ChallengesDokument14 SeitenOrange Reports Solid Q1 2012 Results Despite Market ChallengesFinni ShajiNoch keine Bewertungen

- Situation, Prospects and Challenges of Spanish and EU Construction Sector - Julián NúñezDokument47 SeitenSituation, Prospects and Challenges of Spanish and EU Construction Sector - Julián NúñezinigonunezNoch keine Bewertungen

- Euro Debt Crisis: From Shared Prosperity To Probable CollapseDokument33 SeitenEuro Debt Crisis: From Shared Prosperity To Probable CollapseNor IzzatinaNoch keine Bewertungen

- MRC Medical Research Council-Strategic Plan 2014-2019Dokument52 SeitenMRC Medical Research Council-Strategic Plan 2014-2019Acuacria DosNoch keine Bewertungen

- Cost Model - Country Analysis Report (CAR) For GermanyDokument31 SeitenCost Model - Country Analysis Report (CAR) For GermanyAcuacria DosNoch keine Bewertungen

- The Laws of Project Management PDFDokument4 SeitenThe Laws of Project Management PDFva3ttnNoch keine Bewertungen

- European Partnerships under Horizon EuropeDokument126 SeitenEuropean Partnerships under Horizon EuropeAcuacria DosNoch keine Bewertungen

- Critical Reading As ReasoningDokument18 SeitenCritical Reading As ReasoningKyle Velasquez100% (3)

- B2BDokument31 SeitenB2BAjay MaheskaNoch keine Bewertungen

- Transistor InfoDokument3 SeitenTransistor InfoErantha SampathNoch keine Bewertungen

- IALA Design of Fairways Doc - 307 - EngDokument42 SeitenIALA Design of Fairways Doc - 307 - EngDeanna Barrett100% (2)

- Easi-Pay Guide via e-ConnectDokument29 SeitenEasi-Pay Guide via e-ConnectKok WaiNoch keine Bewertungen

- Kurzweil MicropianoDokument24 SeitenKurzweil Micropianoestereo8Noch keine Bewertungen

- Ticketreissue PDFDokument61 SeitenTicketreissue PDFnicoNicoletaNoch keine Bewertungen

- 2007 Output Stops RemovedDokument45 Seiten2007 Output Stops RemovedAisyah DzulqaidahNoch keine Bewertungen

- Datasheet - SP 275K INH String InvDokument1 SeiteDatasheet - SP 275K INH String Invsharib26Noch keine Bewertungen

- Computer LanguagesDokument3 SeitenComputer LanguagesGurvinder Singh100% (1)

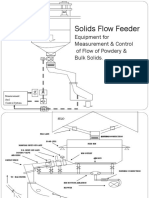

- Solids Flow Feeder Equipment for Precise Measurement & ControlDokument7 SeitenSolids Flow Feeder Equipment for Precise Measurement & ControlAbhishek DuttaNoch keine Bewertungen

- (Airplane Design) Jan Roskam - Airplane Design Part V - Component Weight Estimation. 5-DARcorporation (2018)Dokument227 Seiten(Airplane Design) Jan Roskam - Airplane Design Part V - Component Weight Estimation. 5-DARcorporation (2018)Daniel Lobato Bernardes100% (1)

- Bringing Industrial Automation Environment Into Classroom: A Didactic Three-Tank and Heat Exchanger ModuleDokument5 SeitenBringing Industrial Automation Environment Into Classroom: A Didactic Three-Tank and Heat Exchanger Modulenicacio_89507470Noch keine Bewertungen

- Gordon M. Pugh Davidg - RasmussenDokument2 SeitenGordon M. Pugh Davidg - RasmussenKuroKy KrausserNoch keine Bewertungen

- BS Basics Boundary Scan PDFDokument2 SeitenBS Basics Boundary Scan PDFShankar ArunmozhiNoch keine Bewertungen

- B2B ApiDokument350 SeitenB2B ApiratnavelpNoch keine Bewertungen

- BUK9Y53-100B DatasheetDokument12 SeitenBUK9Y53-100B Datasheetisomeso21Noch keine Bewertungen

- Schools Division of Pasay City outlines 5S workplace organizationDokument9 SeitenSchools Division of Pasay City outlines 5S workplace organizationJhaexelle allenah AlfonsoNoch keine Bewertungen

- wndw3 Print PDFDokument520 Seitenwndw3 Print PDFbryanth9Noch keine Bewertungen

- Tapered Roller Bearings, RBC Tapered Thrust Bearings: Producing High-Quality Products Since 1929Dokument16 SeitenTapered Roller Bearings, RBC Tapered Thrust Bearings: Producing High-Quality Products Since 1929eblees100Noch keine Bewertungen

- Aztech+700WR-3G User ManualDokument57 SeitenAztech+700WR-3G User Manualkero_the_hero67% (3)

- ASV Posi-Track PT-80 Track Loader Parts Catalogue Manual PDFDokument14 SeitenASV Posi-Track PT-80 Track Loader Parts Catalogue Manual PDFfisekkkdNoch keine Bewertungen

- OTC13998Dokument15 SeitenOTC13998Raifel MoralesNoch keine Bewertungen

- Learjet 45 Pilot Traning Manual Volumen 2Dokument539 SeitenLearjet 45 Pilot Traning Manual Volumen 2Agustin Bernales88% (8)

- Operations and Service 69UG15: Diesel Generator SetDokument64 SeitenOperations and Service 69UG15: Diesel Generator SetAnonymous NYymdHgyNoch keine Bewertungen

- Simovert Masterdrives VCDokument16 SeitenSimovert Masterdrives VCangeljavier9Noch keine Bewertungen

- II B.Tech II Semester Regular Examinations, Apr/May 2007 Chemical Engineering Thermodynamics-IDokument7 SeitenII B.Tech II Semester Regular Examinations, Apr/May 2007 Chemical Engineering Thermodynamics-IrajaraghuramvarmaNoch keine Bewertungen

- Why I Play Bass March 14 2013Dokument293 SeitenWhy I Play Bass March 14 2013Paul van Niekerk80% (5)

- The Contemporary WorldDokument9 SeitenThe Contemporary WorldDennis RaymundoNoch keine Bewertungen

- Complete Checklist for Manual Upgrades to Oracle Database 12c R1Dokument27 SeitenComplete Checklist for Manual Upgrades to Oracle Database 12c R1Augustine OderoNoch keine Bewertungen