Das könnte Ihnen auch gefallen

- Report On Micro FinanceDokument55 SeitenReport On Micro Financearvind.vns14395% (73)

- Chapter 4 Rural Banking and Micro Financing 1Dokument16 SeitenChapter 4 Rural Banking and Micro Financing 1saloniNoch keine Bewertungen

- The Functional Microfinance Bank: Strategies for SurvivalVon EverandThe Functional Microfinance Bank: Strategies for SurvivalNoch keine Bewertungen

- Women EntrepreneurshipDokument83 SeitenWomen Entrepreneurshipkaranjangid17Noch keine Bewertungen

- Microfinance Chapter 1Dokument27 SeitenMicrofinance Chapter 1Prakash KumarNoch keine Bewertungen

- Micro Finance (BankingDokument35 SeitenMicro Finance (BankingAsim Waghu100% (1)

- Access to Finance: Microfinance Innovations in the People's Republic of ChinaVon EverandAccess to Finance: Microfinance Innovations in the People's Republic of ChinaNoch keine Bewertungen

- Report On Micro FinanceDokument55 SeitenReport On Micro FinanceSudeepti TanejaNoch keine Bewertungen

- Research BdoDokument64 SeitenResearch Bdo00-scribd-0045% (11)

- Financial Inclusion for Micro, Small, and Medium Enterprises in Kazakhstan: ADB Support for Regional Cooperation and Integration across Asia and the Pacific during Unprecedented Challenge and ChangeVon EverandFinancial Inclusion for Micro, Small, and Medium Enterprises in Kazakhstan: ADB Support for Regional Cooperation and Integration across Asia and the Pacific during Unprecedented Challenge and ChangeNoch keine Bewertungen

- Microfinance 140113043356 Phpapp01Dokument40 SeitenMicrofinance 140113043356 Phpapp01Manjula guptaNoch keine Bewertungen

- Current Trends & Cases in Finance: MicrofinanceDokument101 SeitenCurrent Trends & Cases in Finance: MicrofinanceManavAgarwalNoch keine Bewertungen

- Micro Finance and SHG - Ethiraj College-Ssp-14 Dec 21Dokument29 SeitenMicro Finance and SHG - Ethiraj College-Ssp-14 Dec 21sathyanandaprabhu2786Noch keine Bewertungen

- Inroduction: Microfinance Is A Category of Financial ServicesDokument23 SeitenInroduction: Microfinance Is A Category of Financial ServicesNikilNoch keine Bewertungen

- MFS PPT FinalDokument18 SeitenMFS PPT FinalvijaybharvadNoch keine Bewertungen

- Banking and Microfinance - IIDokument24 SeitenBanking and Microfinance - IIKoyelNoch keine Bewertungen

- MFAssignmentDokument15 SeitenMFAssignmentRiturajNoch keine Bewertungen

- Rural Banking and Micro Finance: Unit: IVDokument17 SeitenRural Banking and Micro Finance: Unit: IVkimberly0jonesNoch keine Bewertungen

- Micro Finance - Keys & Challenges:-A Review Mohit RewariDokument13 SeitenMicro Finance - Keys & Challenges:-A Review Mohit Rewarisonia khuranaNoch keine Bewertungen

- FSM AssignmentDokument50 SeitenFSM AssignmentHardik PatelNoch keine Bewertungen

- Microfinance Institutions in India:Salient Features: Hemant SinghDokument3 SeitenMicrofinance Institutions in India:Salient Features: Hemant Singhbeena antuNoch keine Bewertungen

- Picturing Micro Finance: S. Arun Kumar Dhanamjaya Bhupathi E.Mohanraj - PresentDokument23 SeitenPicturing Micro Finance: S. Arun Kumar Dhanamjaya Bhupathi E.Mohanraj - PresentjeyaselwynNoch keine Bewertungen

- Status of Microfinance and Its Delivery Models in IndiaDokument13 SeitenStatus of Microfinance and Its Delivery Models in IndiaSiva Sankari100% (1)

- Nice OneDokument23 SeitenNice Onemayank4948Noch keine Bewertungen

- The Role of Micro Finance in SHGDokument12 SeitenThe Role of Micro Finance in SHGijgarph100% (1)

- Annapurna ReportDokument31 SeitenAnnapurna ReportPritish KumarNoch keine Bewertungen

- Micro FinanceDokument17 SeitenMicro FinanceAbhineet DhaliwalNoch keine Bewertungen

- Sustainability of MFI's in India After Y.H.Malegam CommitteeDokument18 SeitenSustainability of MFI's in India After Y.H.Malegam CommitteeAnup BmNoch keine Bewertungen

- Unit 5-1Dokument7 SeitenUnit 5-1Yuvashree GNoch keine Bewertungen

- Role of NGO SectorDokument14 SeitenRole of NGO SectorriyasoniyaNoch keine Bewertungen

- MicroFinance Raheel (1MS18MBA40)Dokument18 SeitenMicroFinance Raheel (1MS18MBA40)Anees AnavattiNoch keine Bewertungen

- Amity UniversityDokument7 SeitenAmity Universityrsrpk27Noch keine Bewertungen

- Microfinance Research PaperfinalDokument9 SeitenMicrofinance Research PaperfinalChauhan NeelamNoch keine Bewertungen

- Need For MF Gap DD and SSDokument2 SeitenNeed For MF Gap DD and SSalviarpitaNoch keine Bewertungen

- Report On Micro FinanceDokument54 SeitenReport On Micro Financemohsinmalik07100% (1)

- Term Paper of Banking & Insurance: Topic: Micro Finance Development Overview and ChallengesDokument18 SeitenTerm Paper of Banking & Insurance: Topic: Micro Finance Development Overview and ChallengesSumit SinghNoch keine Bewertungen

- Project Report On "A Critical Analysis of Micro Finance in India"Dokument55 SeitenProject Report On "A Critical Analysis of Micro Finance in India"Om Prakash MishraNoch keine Bewertungen

- "Microfinance & Financial Inclusion": Presented byDokument20 Seiten"Microfinance & Financial Inclusion": Presented byaugust6Noch keine Bewertungen

- CRISIL Ratings India Top 50 MfisDokument68 SeitenCRISIL Ratings India Top 50 MfisDavid Raju GollapudiNoch keine Bewertungen

- The Microfinance Industry in IndiaDokument3 SeitenThe Microfinance Industry in IndiaPrashant Upashi SonuNoch keine Bewertungen

- Microfinance in IndiaDokument27 SeitenMicrofinance in IndiaPraveen Green BeretNoch keine Bewertungen

- "Microfinance in India": Presented byDokument18 Seiten"Microfinance in India": Presented byVinita RaiNoch keine Bewertungen

- Micro Finance in IndiaDokument59 SeitenMicro Finance in IndiaApurva Bangera100% (1)

- A Study of The Performance of Microfinance Institutions in India in Present Era - A Tool For Poverty AlleviationDokument10 SeitenA Study of The Performance of Microfinance Institutions in India in Present Era - A Tool For Poverty AlleviationjyotivermaNoch keine Bewertungen

- Building Sustainable Microfinance Institutions in IndiaDokument18 SeitenBuilding Sustainable Microfinance Institutions in IndiaAlok BhandariNoch keine Bewertungen

- Topic of The Week For Discussion: 12 To 18 March: Topic: Microfinance Sector in IndiaDokument2 SeitenTopic of The Week For Discussion: 12 To 18 March: Topic: Microfinance Sector in Indiarockstar104Noch keine Bewertungen

- Microfinance - Current Status and Growing Concerns in India: Executive SummaryDokument7 SeitenMicrofinance - Current Status and Growing Concerns in India: Executive SummaryNaresh RajNoch keine Bewertungen

- Micro Finance Research Paper....Dokument14 SeitenMicro Finance Research Paper....Anand ChaudharyNoch keine Bewertungen

- AMFPL Credit Appraisal PolicyDokument16 SeitenAMFPL Credit Appraisal PolicyPranav GuptaNoch keine Bewertungen

- Microfinance Paper PresentationDokument8 SeitenMicrofinance Paper Presentationtulasinad123Noch keine Bewertungen

- 2 Pillars of MicrofinanceDokument26 Seiten2 Pillars of MicrofinanceAbhishek GargNoch keine Bewertungen

- Micro Finance Sector in India ModelDokument9 SeitenMicro Finance Sector in India Modelswati singhNoch keine Bewertungen

- Notes Micro FinanceDokument9 SeitenNotes Micro Financesofty1980Noch keine Bewertungen

- Microfinance in IndiaDokument12 SeitenMicrofinance in IndiaRavi KiranNoch keine Bewertungen

- Awareness of MicrofinanceDokument34 SeitenAwareness of MicrofinanceDisha Tiwari100% (1)

- Financial Management of Microfinance Companies in IndiaDokument6 SeitenFinancial Management of Microfinance Companies in IndiaIJRASETPublicationsNoch keine Bewertungen

- SMART PUSHNOTE - An Agent Based Intelligent Push Notification System 2017-18Dokument60 SeitenSMART PUSHNOTE - An Agent Based Intelligent Push Notification System 2017-18sachin mohanNoch keine Bewertungen

- Module V Micro FinanceDokument12 SeitenModule V Micro FinanceRuksana NisamudheenNoch keine Bewertungen

- A Brief On Microfinance: Patni InternalDokument4 SeitenA Brief On Microfinance: Patni InternalshiprathereNoch keine Bewertungen

- Intro To Micro FinanceDokument32 SeitenIntro To Micro FinanceHarsha Kiran BhupalamNoch keine Bewertungen

- Dissertation Report On Issue and Success Factors in Micro FinancingDokument71 SeitenDissertation Report On Issue and Success Factors in Micro FinancingMohd KabeerNoch keine Bewertungen

- Banking India: Accepting Deposits for the Purpose of LendingVon EverandBanking India: Accepting Deposits for the Purpose of LendingNoch keine Bewertungen

- Aa Ki MatraDokument1 SeiteAa Ki Matrakaranjangid17Noch keine Bewertungen

- Badi e Ki MatraDokument1 SeiteBadi e Ki Matrakaranjangid17Noch keine Bewertungen

- Ae Ki Matra ExeciseDokument1 SeiteAe Ki Matra Execisekaranjangid17Noch keine Bewertungen

- Ae Ki MatraDokument1 SeiteAe Ki Matrakaranjangid17Noch keine Bewertungen

- ComputerDokument1 SeiteComputerkaranjangid17Noch keine Bewertungen

- E Ki Matra ExerciseDokument1 SeiteE Ki Matra Exercisekaranjangid17Noch keine Bewertungen

- Module A: Discussion QuestionsDokument10 SeitenModule A: Discussion Questionskaranjangid17Noch keine Bewertungen

- Consumersatisfactiontowardsreliancejio 170419141747Dokument81 SeitenConsumersatisfactiontowardsreliancejio 170419141747Vikas Gupta MirzapurNoch keine Bewertungen

- Parts of ComputerDokument1 SeiteParts of Computerkaranjangid17Noch keine Bewertungen

- FinalDokument123 SeitenFinalkaranjangid17Noch keine Bewertungen

- HRMDokument2 SeitenHRMkaranjangid17Noch keine Bewertungen

- Reliance Jio Presentation PDFDokument27 SeitenReliance Jio Presentation PDFSravyaNoch keine Bewertungen

- Performance Review System Mba HR ProjectDokument55 SeitenPerformance Review System Mba HR Projectr_priyanka425Noch keine Bewertungen

- GenEnglish - Paper II DMRC PDFDokument7 SeitenGenEnglish - Paper II DMRC PDFAnonymous Clyy9NNoch keine Bewertungen

- Impact of Microfinance in India: Tilika Chawda C50Dokument29 SeitenImpact of Microfinance in India: Tilika Chawda C50karanjangid17Noch keine Bewertungen

- Digital Banking and CurrencyDokument51 SeitenDigital Banking and Currencykaranjangid17Noch keine Bewertungen

- Micro Finance SHG PPT 120928142952 Phpapp01Dokument30 SeitenMicro Finance SHG PPT 120928142952 Phpapp01karanjangid17Noch keine Bewertungen

- Policy Framework Paper On MicrofinanceDokument80 SeitenPolicy Framework Paper On MicrofinanceYoucef GrimesNoch keine Bewertungen

- Temba - DissertationDokument69 SeitenTemba - Dissertationdeo847Noch keine Bewertungen

- Rural Marketing ManualDokument21 SeitenRural Marketing ManualRahul Verma RVNoch keine Bewertungen

- Unit 4-2Dokument22 SeitenUnit 4-2Yuvashree GNoch keine Bewertungen

- Bank Mandiri Entry StrategyDokument20 SeitenBank Mandiri Entry StrategyEka DarmadiNoch keine Bewertungen

- Module 2: Oversight Government Official For Micro EnterprisesDokument17 SeitenModule 2: Oversight Government Official For Micro EnterprisesJamiella CristobalNoch keine Bewertungen

- Banto 2020 Microfinance Institutions, Banking, Growth and Transmission ChannelA GMM Panel Data Analysis From Developing CountriesDokument25 SeitenBanto 2020 Microfinance Institutions, Banking, Growth and Transmission ChannelA GMM Panel Data Analysis From Developing CountriesngaNoch keine Bewertungen

- Hand in Hand - Case Study 02Dokument4 SeitenHand in Hand - Case Study 02Dzenan OmanovicNoch keine Bewertungen

- IJRCM Dec 12Dokument13 SeitenIJRCM Dec 12dhanush rNoch keine Bewertungen

- Growth of Micro Finance in India A Descriptive StudyDokument12 SeitenGrowth of Micro Finance in India A Descriptive StudyBobby ShrivastavaNoch keine Bewertungen

- Islamic Microfinance in LuxembergDokument7 SeitenIslamic Microfinance in LuxembergroytanladiasanNoch keine Bewertungen

- Five Developments For Asia Green Development BankDokument5 SeitenFive Developments For Asia Green Development BankkaythweNoch keine Bewertungen

- Chapter 6 Business FinancingDokument16 SeitenChapter 6 Business Financingtegegne abdissaNoch keine Bewertungen

- Rural BankingDokument2 SeitenRural BankingHarshal WankhedeNoch keine Bewertungen

- Thesis On Financial RiskDokument7 SeitenThesis On Financial Riskheatheredwardsmobile100% (2)

- YOMA Bank (Branch Visit Report)Dokument8 SeitenYOMA Bank (Branch Visit Report)kyawthNoch keine Bewertungen

- Moolani FoundationDokument17 SeitenMoolani Foundations_gonzalez750% (1)

- Internship Report On Grameen Bank - CompleteDokument65 SeitenInternship Report On Grameen Bank - CompleteMishu100% (2)

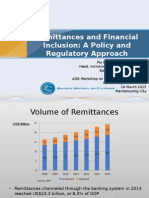

- Remittances and Financial Inclusion: A Policy and Regulatory ApproachDokument19 SeitenRemittances and Financial Inclusion: A Policy and Regulatory ApproachAsian Development Bank ConferencesNoch keine Bewertungen

- Ag. Credit Study FinalDokument21 SeitenAg. Credit Study FinalMd Golzare nabiNoch keine Bewertungen

- Financial Inclusion From BIMSDokument14 SeitenFinancial Inclusion From BIMSDeepu T MathewNoch keine Bewertungen

- Unity Small Finance Bank LimitedDokument10 SeitenUnity Small Finance Bank LimitedMainathan NagarajanNoch keine Bewertungen

- Developmental Banking Institutions Course Code: MBAD16F33B4 MBA III - Section E, ODD Semester Prof. Siju NairDokument48 SeitenDevelopmental Banking Institutions Course Code: MBAD16F33B4 MBA III - Section E, ODD Semester Prof. Siju NairK C Keerthiraj gowdaNoch keine Bewertungen

- Group Assignment For MFI CourseDokument2 SeitenGroup Assignment For MFI CoursesimmyNoch keine Bewertungen

- Rethinking Microfinance and Grameen Bank ModelDokument24 SeitenRethinking Microfinance and Grameen Bank ModelWOD BangladeshNoch keine Bewertungen

- 05 Elms Review 1 - Arg MRLFJRDDokument3 Seiten05 Elms Review 1 - Arg MRLFJRDMurielle Fajardo100% (1)

- How To Manage Variable Loan Installments: FLOSS ManualsDokument25 SeitenHow To Manage Variable Loan Installments: FLOSS ManualsKidanemariam TesfayNoch keine Bewertungen

- RBI Circular On External Commercial Borrowings (ECB)Dokument60 SeitenRBI Circular On External Commercial Borrowings (ECB)vhkprasadNoch keine Bewertungen

- Yemen Breaking The Vicious Cycle of Poverty Through MicrofinanceDokument3 SeitenYemen Breaking The Vicious Cycle of Poverty Through MicrofinancecapteniwolaNoch keine Bewertungen