Das könnte Ihnen auch gefallen

- Industrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisVon EverandIndustrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisNoch keine Bewertungen

- Eiis Unit 4Dokument35 SeitenEiis Unit 4Nivesh GuptaNoch keine Bewertungen

- Chap 14 EOU EPZ STP SEZDokument10 SeitenChap 14 EOU EPZ STP SEZAshish MalikNoch keine Bewertungen

- Epcg and Sez BenefitsDokument2 SeitenEpcg and Sez BenefitsRajiv GuptaNoch keine Bewertungen

- Eou SchemeDokument6 SeitenEou Schemedll_dollieNoch keine Bewertungen

- Presentation On EOUDokument24 SeitenPresentation On EOUManish Kumar100% (1)

- Export Oriented Units (Eous), Electronics Hardware Technology Parks (Ehtps), Software Technology Parks (STPS) and Bio-Technology Parks (BTPS)Dokument21 SeitenExport Oriented Units (Eous), Electronics Hardware Technology Parks (Ehtps), Software Technology Parks (STPS) and Bio-Technology Parks (BTPS)Bharat JainNoch keine Bewertungen

- Write Short Notes OnDokument16 SeitenWrite Short Notes OnSheikh SadiqueNoch keine Bewertungen

- EOUDokument31 SeitenEOUdasharathdhageNoch keine Bewertungen

- SlideshoweouDokument18 SeitenSlideshoweoukittudevisreeNoch keine Bewertungen

- ELP Manufacture and Other Operations in Bonded Warehouse MinDokument3 SeitenELP Manufacture and Other Operations in Bonded Warehouse MinELP LawNoch keine Bewertungen

- ANF5ADokument9 SeitenANF5ACharles JacobNoch keine Bewertungen

- Presented by Arunima Debnath Ankita (GROUP NO.-15)Dokument18 SeitenPresented by Arunima Debnath Ankita (GROUP NO.-15)Arunima DebnathNoch keine Bewertungen

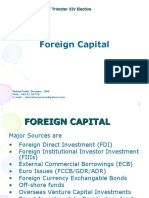

- Foreign Capital: Mba (Tech) 5 Year / Trimster XIV ElectiveDokument16 SeitenForeign Capital: Mba (Tech) 5 Year / Trimster XIV ElectiveshivimanyuNoch keine Bewertungen

- Foreign Trade Policy May19Dokument22 SeitenForeign Trade Policy May19H JNoch keine Bewertungen

- Export Oriented Units (Eous), Electronics Hardware Technology Parks (Ehtps), Software Technology Parks (STPS) and Bio-Technology Parks (BTPS)Dokument23 SeitenExport Oriented Units (Eous), Electronics Hardware Technology Parks (Ehtps), Software Technology Parks (STPS) and Bio-Technology Parks (BTPS)Kavya MamathaNoch keine Bewertungen

- Chapter 6 FTP 2023Dokument12 SeitenChapter 6 FTP 2023dimple.dhamechaaNoch keine Bewertungen

- Eou Ehtp STP Biotech Parks, An Explained Version of Foreign Trade PolicyDokument34 SeitenEou Ehtp STP Biotech Parks, An Explained Version of Foreign Trade PolicyAshfaque NagpurwalaNoch keine Bewertungen

- Export Promotion Capital Goods Scheme EPCG SchemeDokument4 SeitenExport Promotion Capital Goods Scheme EPCG SchemeanuragNoch keine Bewertungen

- Foreign CapitalDokument15 SeitenForeign Capitaldranita@yahoo.comNoch keine Bewertungen

- Customs STPIDokument33 SeitenCustoms STPISuresh BishnoiNoch keine Bewertungen

- Schemes in FTP 2015-16: Brief ComparisonDokument4 SeitenSchemes in FTP 2015-16: Brief Comparisonmaulesh bhattNoch keine Bewertungen

- Special Economic ZoneDokument24 SeitenSpecial Economic ZoneSiva SankariNoch keine Bewertungen

- MOOWRDokument2 SeitenMOOWRvinaycrNoch keine Bewertungen

- Eou & Sez Schemes Are One Among Them, Which Provides An Internationally Competitive Duty Oriented Units (Eous) What Does Eou Mean?Dokument9 SeitenEou & Sez Schemes Are One Among Them, Which Provides An Internationally Competitive Duty Oriented Units (Eous) What Does Eou Mean?Surjan SinghNoch keine Bewertungen

- ExportDokument2 SeitenExportruby402sharonNoch keine Bewertungen

- FTP 2Dokument13 SeitenFTP 2Sachi Bani PerharNoch keine Bewertungen

- Circular No. 11 /2009-CusDokument6 SeitenCircular No. 11 /2009-CusrpadmakrishnanNoch keine Bewertungen

- Eou ManualDokument3 SeitenEou ManualastuteNoch keine Bewertungen

- Btax302 Lesson10 PezaandboiregisteredentitiesDokument18 SeitenBtax302 Lesson10 PezaandboiregisteredentitiesJr Reyes PedidaNoch keine Bewertungen

- 11 - Sez, Eou, STP and Ehtp SchemesDokument23 Seiten11 - Sez, Eou, STP and Ehtp SchemesSamaresh RoyNoch keine Bewertungen

- WOFEDokument6 SeitenWOFEhuokeqiangNoch keine Bewertungen

- DTREDokument10 SeitenDTRESeeraj KhanNoch keine Bewertungen

- Faqs On Export and FTP Related Issues of GSTDokument6 SeitenFaqs On Export and FTP Related Issues of GSTJigar PunamiyaNoch keine Bewertungen

- 1 EBCL Extra ClassroomnotesDokument23 Seiten1 EBCL Extra ClassroomnotesMahak AgarwalNoch keine Bewertungen

- Anf 5A Application Form For Epcg Authorisation IssueDokument6 SeitenAnf 5A Application Form For Epcg Authorisation IssuesrinivasNoch keine Bewertungen

- Presentation ON The Customs Act, 1962, and The Customs Tariff Act, 1975Dokument32 SeitenPresentation ON The Customs Act, 1962, and The Customs Tariff Act, 1975ClanlordNoch keine Bewertungen

- (EOU) Export Oriented UnitsDokument25 Seiten(EOU) Export Oriented UnitsswathiNoch keine Bewertungen

- For Boi IncentivesDokument7 SeitenFor Boi Incentiveskimberly fanoNoch keine Bewertungen

- Presentation by S.ClementDokument54 SeitenPresentation by S.ClementVivek DoshiNoch keine Bewertungen

- Cin 2Dokument77 SeitenCin 2fharooksNoch keine Bewertungen

- FDI July '20Dokument17 SeitenFDI July '20Yogesh SalujaNoch keine Bewertungen

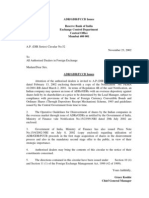

- ADR/GDR/FCCB Issues Reserve Bank of India Exchange Control Department Central Office Mumbai 400 001Dokument4 SeitenADR/GDR/FCCB Issues Reserve Bank of India Exchange Control Department Central Office Mumbai 400 001karthikag25Noch keine Bewertungen

- Policy For EOU / FTZ / SEZ Units: Objectives, Criteria and Benefits Procedures and DocumentationDokument18 SeitenPolicy For EOU / FTZ / SEZ Units: Objectives, Criteria and Benefits Procedures and Documentationnaveenrana99Noch keine Bewertungen

- Statement of Significant Accounting PoliciesDokument6 SeitenStatement of Significant Accounting PoliciesthomasNoch keine Bewertungen

- EOU, EHTP, STP, BTP SchemesDokument2 SeitenEOU, EHTP, STP, BTP SchemesaleeshatenetNoch keine Bewertungen

- Vodafone International Holdings B.V. vs. Union of India 1. About Hutchision Essar LimitedDokument6 SeitenVodafone International Holdings B.V. vs. Union of India 1. About Hutchision Essar LimitedasdfqwerasdNoch keine Bewertungen

- Vat HandoutsDokument7 SeitenVat HandoutsjulsNoch keine Bewertungen

- Foreign Trade Policy 1Dokument31 SeitenForeign Trade Policy 1vmchawlaNoch keine Bewertungen

- DTRERules Updatedversion Upto12.09.2019Dokument17 SeitenDTRERules Updatedversion Upto12.09.2019abid205Noch keine Bewertungen

- India New Foreign Trade Policy 2015Dokument15 SeitenIndia New Foreign Trade Policy 2015Hameem KhanNoch keine Bewertungen

- Incentives EPZDokument1 SeiteIncentives EPZMOHAMMED ALI CHOWDHURYNoch keine Bewertungen

- VatDokument7 SeitenVatCharla SuanNoch keine Bewertungen

- Presentation On Special Economic Zone - Il&Fs IdcDokument49 SeitenPresentation On Special Economic Zone - Il&Fs IdcPranita PatiNoch keine Bewertungen

- Export Promotion SchemesDokument45 SeitenExport Promotion Schemesasifanis100% (1)

- Equity Valuation: Models from Leading Investment BanksVon EverandEquity Valuation: Models from Leading Investment BanksJan ViebigNoch keine Bewertungen

- Whistle Blower Policy: Bridgestone India Private LimitedDokument8 SeitenWhistle Blower Policy: Bridgestone India Private LimitedRajiv GuptaNoch keine Bewertungen

- Manufacturing Setup ProceduresDokument1 SeiteManufacturing Setup ProceduresRajiv GuptaNoch keine Bewertungen

- DVD R4xDisc PDFDokument1 SeiteDVD R4xDisc PDFRajiv GuptaNoch keine Bewertungen

- Girls Hostel Allotment List 2018-19 PDFDokument2 SeitenGirls Hostel Allotment List 2018-19 PDFRajiv GuptaNoch keine Bewertungen

- JEE Main 2018 Answer Key by IITian Pace Code CDokument1 SeiteJEE Main 2018 Answer Key by IITian Pace Code CRajiv GuptaNoch keine Bewertungen

- Journal On Threpetical Study On MutraDokument6 SeitenJournal On Threpetical Study On MutraVijay DawarNoch keine Bewertungen

- Governor General and Viceroy of India 1 5 14Dokument22 SeitenGovernor General and Viceroy of India 1 5 14RaviNoch keine Bewertungen

- India Truth SeekerDokument8 SeitenIndia Truth SeekerSharon SeebergerNoch keine Bewertungen

- 503020001Dokument3 Seiten503020001shadabrkhanNoch keine Bewertungen

- Medical Doctor ListDokument2 SeitenMedical Doctor ListRajeesh M R0% (1)

- New York Tsurphu Goshir Dharma Center ClassesDokument4 SeitenNew York Tsurphu Goshir Dharma Center ClassesJustin von BujdossNoch keine Bewertungen

- OrchhaDokument6 SeitenOrchhaJaseer AliNoch keine Bewertungen

- Medicine Buddha TEXTDokument20 SeitenMedicine Buddha TEXTGloria Rinchen ChödrenNoch keine Bewertungen

- KP - Eliminating Significators - Jupiters WebDokument3 SeitenKP - Eliminating Significators - Jupiters WebvinoohmNoch keine Bewertungen

- Angkor Wat EssayDokument3 SeitenAngkor Wat Essayapi-443413528100% (1)

- Tantra YogaDokument5 SeitenTantra YogaAghora37Noch keine Bewertungen

- Chitpavan Brahmin Origin and HistoryDokument10 SeitenChitpavan Brahmin Origin and HistoryAshok RBNoch keine Bewertungen

- Bhavishya Purana - Gita Press Gorakhpur - 3 (Gita Press Gorakhpur) (Z-Library)Dokument214 SeitenBhavishya Purana - Gita Press Gorakhpur - 3 (Gita Press Gorakhpur) (Z-Library)rubiksflixNoch keine Bewertungen

- Ec9 10 710Dokument56 SeitenEc9 10 710madhuNoch keine Bewertungen

- Aspects of Kundalini Yoga in ThelemaDokument30 SeitenAspects of Kundalini Yoga in ThelemaGustavo MarquesNoch keine Bewertungen

- PTS 2024 Preparatory Test 13 Solutions EngDokument21 SeitenPTS 2024 Preparatory Test 13 Solutions EngKrishna PrintsNoch keine Bewertungen

- D. G. White, Tantric AlchemyDokument25 SeitenD. G. White, Tantric Alchemynandana11Noch keine Bewertungen

- Concept of PatitapavanDokument3 SeitenConcept of PatitapavanRadhikaNoch keine Bewertungen

- Romantic Love StoryDokument1 SeiteRomantic Love StoryAshok Siri100% (3)

- B. Com-TYDokument21 SeitenB. Com-TYNehaNoch keine Bewertungen

- Sree Lakshmi Ashtottara Satanaama StotramDokument7 SeitenSree Lakshmi Ashtottara Satanaama StotramAnand SriramNoch keine Bewertungen

- Synopsis - Thesis On Article 21 of Constitution of IndiaDokument10 SeitenSynopsis - Thesis On Article 21 of Constitution of IndiaVipul Bhatotia100% (2)

- Law Prep MockDokument40 SeitenLaw Prep MockAmulya KaushikNoch keine Bewertungen

- APSC Mains 2020 History Paper I Question PaperDokument2 SeitenAPSC Mains 2020 History Paper I Question PaperEquatorNoch keine Bewertungen

- God Parshuram Story in HindiDokument3 SeitenGod Parshuram Story in HindiCynthiaNoch keine Bewertungen

- UFO - Ufology - UFOs and VimanasDokument29 SeitenUFO - Ufology - UFOs and VimanasNikšaNoch keine Bewertungen

- Durga Like The Nude Goddess of The Indus ValleyDokument22 SeitenDurga Like The Nude Goddess of The Indus ValleypervincarumNoch keine Bewertungen

- Indian Baby Boy NamesDokument62 SeitenIndian Baby Boy Namesjarbandhan54% (13)

- Besnagar and Bhom: Two Paradigms of Ancient Canal StructuresDokument8 SeitenBesnagar and Bhom: Two Paradigms of Ancient Canal StructuresOpen Access JournalNoch keine Bewertungen