Das könnte Ihnen auch gefallen

- Investment Objective Historical Performance: Philam Fund, IncDokument1 SeiteInvestment Objective Historical Performance: Philam Fund, IncWeas ChuckNoch keine Bewertungen

- Ffs Pfi Jun 30 2019Dokument1 SeiteFfs Pfi Jun 30 2019Ramil MontealtoNoch keine Bewertungen

- Investment Objective Historical Performance: Pami Horizon Fund, IncDokument1 SeiteInvestment Objective Historical Performance: Pami Horizon Fund, IncRamil MontealtoNoch keine Bewertungen

- ASTM C129 2011 Non Load Bearing Concrete MasonryDokument1 SeiteASTM C129 2011 Non Load Bearing Concrete MasonryKamille Anne GabaynoNoch keine Bewertungen

- Equity Fund: % Top 10 Holding As On 31st March 2019Dokument1 SeiteEquity Fund: % Top 10 Holding As On 31st March 2019Sajith KumarNoch keine Bewertungen

- Peso Powerhouse Fund - Fund Fact Sheet - December - 2020Dokument2 SeitenPeso Powerhouse Fund - Fund Fact Sheet - December - 2020Jayr LegaspiNoch keine Bewertungen

- Peso Wealth Optimizer Fund 2036 - Fund Fact Sheet - December - 2020Dokument3 SeitenPeso Wealth Optimizer Fund 2036 - Fund Fact Sheet - December - 2020Jayr LegaspiNoch keine Bewertungen

- GSIS Mutual Fund, Inc. (GMFI) : Historical PerformanceDokument1 SeiteGSIS Mutual Fund, Inc. (GMFI) : Historical Performanceapi-25886697Noch keine Bewertungen

- Peso Emperor Fund - Fund Fact Sheet - October - 2020Dokument2 SeitenPeso Emperor Fund - Fund Fact Sheet - October - 2020Jayr LegaspiNoch keine Bewertungen

- ATRAM Phil Equity Smart Index Fund Fact Sheet Jan 2022Dokument2 SeitenATRAM Phil Equity Smart Index Fund Fact Sheet Jan 2022jvNoch keine Bewertungen

- Peso Emperor Fund - Fund Fact Sheet - December - 2020Dokument2 SeitenPeso Emperor Fund - Fund Fact Sheet - December - 2020Jayr LegaspiNoch keine Bewertungen

- Shinhan Supreme Balance FundDokument1 SeiteShinhan Supreme Balance FundhhhahaNoch keine Bewertungen

- MP - 3 - Peso Growth FundDokument2 SeitenMP - 3 - Peso Growth FundFrank TaquioNoch keine Bewertungen

- Archipelago Equity Growth FactsheetDokument1 SeiteArchipelago Equity Growth FactsheetDaniel WijayaNoch keine Bewertungen

- Shinhan Balance Fund - Agustus - 2023 - enDokument1 SeiteShinhan Balance Fund - Agustus - 2023 - enwongjuliusNoch keine Bewertungen

- Debt FundDokument8 SeitenDebt Fundapi-3705377Noch keine Bewertungen

- First Metro Save and Learn Fixed Income FundDokument1 SeiteFirst Metro Save and Learn Fixed Income FundkimencinaNoch keine Bewertungen

- Fund Fact Sheets - Prosperity Bond FundDokument1 SeiteFund Fact Sheets - Prosperity Bond FundJeuz Llorenz Colendra-ApitaNoch keine Bewertungen

- HDFC Diversified Equity FundDokument1 SeiteHDFC Diversified Equity FundMayank RajNoch keine Bewertungen

- Hybrid Fund Completes 5 Years NoteDokument3 SeitenHybrid Fund Completes 5 Years NoteMohamed Rajiv AshaNoch keine Bewertungen

- Diversified JulyDokument1 SeiteDiversified JulyPiyushNoch keine Bewertungen

- Beware of Spurious Fraud Phone CallsDokument2 SeitenBeware of Spurious Fraud Phone Callsrajish2014Noch keine Bewertungen

- Annual Investment Report 2016-17Dokument15 SeitenAnnual Investment Report 2016-17DARSHANNoch keine Bewertungen

- Fund Fact Sheets - Prosperity Index FundDokument1 SeiteFund Fact Sheets - Prosperity Index FundJohh-RevNoch keine Bewertungen

- Fund Fact Sheets - Prosperity Bond FundDokument1 SeiteFund Fact Sheets - Prosperity Bond FundJohh-RevNoch keine Bewertungen

- Capital Growth FundDokument1 SeiteCapital Growth FundHimanshu AgrawalNoch keine Bewertungen

- Fund Fact Sheets - Prosperity Equity FundDokument1 SeiteFund Fact Sheets - Prosperity Equity FundJohh-RevNoch keine Bewertungen

- Rootstock SCI Worldwide Flexible Fund - Minimum Disclosure DocumentDokument4 SeitenRootstock SCI Worldwide Flexible Fund - Minimum Disclosure DocumentMartin NelNoch keine Bewertungen

- Conservative at Least Five (5) Years: Account of The ClientDokument2 SeitenConservative at Least Five (5) Years: Account of The ClientkimencinaNoch keine Bewertungen

- Peso Asia Pacific Property Income Fund - Fund Fact Sheet - October - 2020Dokument2 SeitenPeso Asia Pacific Property Income Fund - Fund Fact Sheet - October - 2020Jayr LegaspiNoch keine Bewertungen

- Shinhan Balance Fund Factsheet PDFDokument1 SeiteShinhan Balance Fund Factsheet PDFjoecool87Noch keine Bewertungen

- Discovery Fund April 23Dokument1 SeiteDiscovery Fund April 23Satyajeet AnandNoch keine Bewertungen

- Product Snapshot: DSP Bond FundDokument2 SeitenProduct Snapshot: DSP Bond FundManoj SharmaNoch keine Bewertungen

- ALFM Peso Bond FundDokument2 SeitenALFM Peso Bond FundkimencinaNoch keine Bewertungen

- PIALEFDokument1 SeitePIALEFEileen LauNoch keine Bewertungen

- DebtDokument9 SeitenDebtapi-3705377Noch keine Bewertungen

- Fund Manager'S Report (Islamic Funds) January 2017: AMC Rating: AM2 by JCR-VISDokument8 SeitenFund Manager'S Report (Islamic Funds) January 2017: AMC Rating: AM2 by JCR-VISmuhammad taufikNoch keine Bewertungen

- India's No.1 Portfolio Management Services PortalDokument1 SeiteIndia's No.1 Portfolio Management Services Portalrahul patelNoch keine Bewertungen

- SAMShariaEquityFund 1402 PDFDokument1 SeiteSAMShariaEquityFund 1402 PDFMuhammad RafifNoch keine Bewertungen

- Welspun Enterprises LTD - Investor Presentation - 2Dokument36 SeitenWelspun Enterprises LTD - Investor Presentation - 2Dwijendra ChanumoluNoch keine Bewertungen

- PMS Guide August 2019Dokument88 SeitenPMS Guide August 2019HetanshNoch keine Bewertungen

- Diversified Equity FundDokument1 SeiteDiversified Equity FundHimanshu AgrawalNoch keine Bewertungen

- Blue Chip JulyDokument1 SeiteBlue Chip JulyPiyushNoch keine Bewertungen

- HDFC Opportunities FundDokument1 SeiteHDFC Opportunities FundManjunath BolashettiNoch keine Bewertungen

- Philequity Peso Bond Fund: Navps As of Dec 27, 2019Dokument1 SeitePhilequity Peso Bond Fund: Navps As of Dec 27, 2019Marlon DNoch keine Bewertungen

- Fund Fact Sheets - Prosperity Balanced FundDokument1 SeiteFund Fact Sheets - Prosperity Balanced FundJohh-RevNoch keine Bewertungen

- HDFC Discovery FundDokument1 SeiteHDFC Discovery FundHarsh SrivastavaNoch keine Bewertungen

- Canara Robeco Emerging Equities: For Private CirculationDokument1 SeiteCanara Robeco Emerging Equities: For Private CirculationAadeesh JainNoch keine Bewertungen

- AD15 June11Dokument2 SeitenAD15 June11Alvin LimNoch keine Bewertungen

- HDFC BlueChip FundDokument1 SeiteHDFC BlueChip FundKaran ShambharkarNoch keine Bewertungen

- Investmentz AugustDokument11 SeitenInvestmentz AugustAnimesh PalNoch keine Bewertungen

- Asset Allocation Fund (5) : Hybrid Hybrid BalancedDokument2 SeitenAsset Allocation Fund (5) : Hybrid Hybrid BalancedHayston DezmenNoch keine Bewertungen

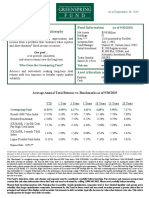

- Greenspring Fund Philosophy Fund Information: (As of 9/30/2019)Dokument2 SeitenGreenspring Fund Philosophy Fund Information: (As of 9/30/2019)Anonymous TtkcZvPNoch keine Bewertungen

- PGPSFDokument2 SeitenPGPSFFabian NgNoch keine Bewertungen

- LiquiLoans - LiteratureDokument28 SeitenLiquiLoans - LiteratureNeetika SahNoch keine Bewertungen

- Portfolios Factsheet: Fund Objective Fund DetailsDokument1 SeitePortfolios Factsheet: Fund Objective Fund DetailsJ. BangjakNoch keine Bewertungen

- December Fund-Factsheets-Individual1Dokument2 SeitenDecember Fund-Factsheets-Individual1Navneet PandeyNoch keine Bewertungen

- ATRAM Phil Equity Smart Index Fund Fact Sheet Nov 2018Dokument2 SeitenATRAM Phil Equity Smart Index Fund Fact Sheet Nov 2018Roan Roan RuanNoch keine Bewertungen

- 6 - Kiid - Uitf - Eq - Bpi Eq - Jun2015Dokument3 Seiten6 - Kiid - Uitf - Eq - Bpi Eq - Jun2015Nonami AbicoNoch keine Bewertungen

- DIVIDEND INVESTING: Maximizing Returns while Minimizing Risk through Selective Stock Selection and Diversification (2023 Guide for Beginners)Von EverandDIVIDEND INVESTING: Maximizing Returns while Minimizing Risk through Selective Stock Selection and Diversification (2023 Guide for Beginners)Noch keine Bewertungen

- Wachovia Case StudyDokument12 SeitenWachovia Case Studyvivekb67100% (1)

- Abel - 3 - A Review of Determinants of Financial Inclusion PDFDokument8 SeitenAbel - 3 - A Review of Determinants of Financial Inclusion PDFAbd Al-Rahman IIINoch keine Bewertungen

- Internship Report NiB BankDokument10 SeitenInternship Report NiB BankAbdul WaheedNoch keine Bewertungen

- Arabi Bin Hamzah No 521 Lot 6746 JLN Sultan Tengah Samariang Aman Phase 4 93050 KUCHING, SARDokument3 SeitenArabi Bin Hamzah No 521 Lot 6746 JLN Sultan Tengah Samariang Aman Phase 4 93050 KUCHING, SARcancalokNoch keine Bewertungen

- Closing Case Caterpillar IncDokument3 SeitenClosing Case Caterpillar InczaheerkhanafridiNoch keine Bewertungen

- First Direct: Group 9 Strategic PlaningDokument11 SeitenFirst Direct: Group 9 Strategic PlaningWasiq ImranNoch keine Bewertungen

- Banking Laws Cases Part 1Dokument181 SeitenBanking Laws Cases Part 1Keisha Yna V. RamirezNoch keine Bewertungen

- Vat Rate (Up To Finance Act 2013-2014)Dokument38 SeitenVat Rate (Up To Finance Act 2013-2014)Sakib Ahmed AnikNoch keine Bewertungen

- Credit Appraisal in Sbi Bank Project6 ReportDokument106 SeitenCredit Appraisal in Sbi Bank Project6 ReportVenu S100% (1)

- Bismillah Group ScandalDokument3 SeitenBismillah Group ScandalAhmad HNoch keine Bewertungen

- PERE - Private Equity Real EstateDokument1 SeitePERE - Private Equity Real EstatePereNoch keine Bewertungen

- Collateral Document Delivery Request Form v2Dokument1 SeiteCollateral Document Delivery Request Form v2Teena BarrettoNoch keine Bewertungen

- Module 4 - Double Entry Bookkeeping System and The Accounting EquationDokument9 SeitenModule 4 - Double Entry Bookkeeping System and The Accounting EquationMark Christian BrlNoch keine Bewertungen

- FM - 1 - Accounts of Professional PersonsDokument15 SeitenFM - 1 - Accounts of Professional Personsyagnesh trivedi100% (1)

- Guthrie-Jensen - Corporate ProfileDokument8 SeitenGuthrie-Jensen - Corporate ProfileRalph GuzmanNoch keine Bewertungen

- I. Convertible Currencies With Bangko Sentral:: Run Date/timeDokument1 SeiteI. Convertible Currencies With Bangko Sentral:: Run Date/timeLucito FalloriaNoch keine Bewertungen

- Inbt Finals ReviewerDokument11 SeitenInbt Finals ReviewerQuenie SagunNoch keine Bewertungen

- Disbursement Voucher Disbursement Voucher: Classificat Ion of Disbursement Classificat Ion of DisbursementDokument8 SeitenDisbursement Voucher Disbursement Voucher: Classificat Ion of Disbursement Classificat Ion of DisbursementErica Dizon100% (1)

- Order FormDokument1 SeiteOrder FormFirasNoch keine Bewertungen

- Office of The PO Cum DWO, PURULIA District: Government of West BengalDokument3 SeitenOffice of The PO Cum DWO, PURULIA District: Government of West BengalJharna RoyNoch keine Bewertungen

- SYNOPSIS HDFC BankDokument4 SeitenSYNOPSIS HDFC BanksargunkaurNoch keine Bewertungen

- Carana BankDokument26 SeitenCarana BankRakesh Kolasani NaiduNoch keine Bewertungen

- Rail Ticket 12 M WouDokument2 SeitenRail Ticket 12 M WouTiyyagura RoofusreddyNoch keine Bewertungen

- Defining General Options AddendumDokument16 SeitenDefining General Options AddendumchinnaNoch keine Bewertungen

- Daily Cash Flow Template ExcelDokument60 SeitenDaily Cash Flow Template ExcelPro ResourcesNoch keine Bewertungen

- Accounting Systems For Thrift Co-Operatives Promoted by Co-OperativeDokument42 SeitenAccounting Systems For Thrift Co-Operatives Promoted by Co-OperativemadhanagopalNoch keine Bewertungen

- BOC Main Branch ContactDokument3 SeitenBOC Main Branch ContactshakecokeNoch keine Bewertungen

- FactSet Bank TrackerDokument9 SeitenFactSet Bank TrackerBrianNoch keine Bewertungen

- Deposit SlipDokument2 SeitenDeposit SlipLalit PardasaniNoch keine Bewertungen

- Pelzer Company Reconciled Its Bank and Book Statement Balances ofDokument2 SeitenPelzer Company Reconciled Its Bank and Book Statement Balances ofAmit PandeyNoch keine Bewertungen