Das könnte Ihnen auch gefallen

- The Increasing Importance of Migrant Remittances from the Russian Federation to Central AsiaVon EverandThe Increasing Importance of Migrant Remittances from the Russian Federation to Central AsiaNoch keine Bewertungen

- IAP ProblemsDokument6 SeitenIAP ProblemsBianca LizardoNoch keine Bewertungen

- CPAR AP - Audit of CashDokument9 SeitenCPAR AP - Audit of CashJohn Carlo CruzNoch keine Bewertungen

- Audit of CashDokument4 SeitenAudit of CashAivan De LeonNoch keine Bewertungen

- Auditing Problems2Dokument31 SeitenAuditing Problems2Kimberly Milante100% (1)

- Bank Recon SeatworkDokument2 SeitenBank Recon SeatworkhfjhdjhfjdehNoch keine Bewertungen

- Bank Recon Seatwork PDFDokument2 SeitenBank Recon Seatwork PDFhfjhdjhfjdeh100% (1)

- MTDrill 2Dokument17 SeitenMTDrill 2Cedric Legaspi TagalaNoch keine Bewertungen

- AP PrinciplesDokument8 SeitenAP PrinciplesLinh NguyễnNoch keine Bewertungen

- Prelim Exam ManuscriptDokument10 SeitenPrelim Exam ManuscriptJulie Mae Caling MalitNoch keine Bewertungen

- Auditing Problems v.1 - 2018Dokument18 SeitenAuditing Problems v.1 - 2018Christine Ballesteros Villamayor33% (3)

- Auditing Problems: Problem No. 1 - Audit of Property, Plant, and Equipment (Ppe)Dokument19 SeitenAuditing Problems: Problem No. 1 - Audit of Property, Plant, and Equipment (Ppe)Marco Louis Duval UyNoch keine Bewertungen

- 123123Dokument3 Seiten123123xjammerNoch keine Bewertungen

- Auditing-23 A 1Dokument5 SeitenAuditing-23 A 1Johnfree VallinasNoch keine Bewertungen

- Financial Accounting - Exercises Proof of Cash: Date Debit Credit BalanceDokument2 SeitenFinancial Accounting - Exercises Proof of Cash: Date Debit Credit BalanceStephany Joy M. MendezNoch keine Bewertungen

- PROBLEM 1: (CPAR Final Preboards October 2015 - Auditing Problems)Dokument5 SeitenPROBLEM 1: (CPAR Final Preboards October 2015 - Auditing Problems)Jessie J.Noch keine Bewertungen

- Problems For Proof of Cash and Bank ReconDokument2 SeitenProblems For Proof of Cash and Bank ReconTine Vasiana DuermeNoch keine Bewertungen

- Prelims Intermedaite AcctgDokument4 SeitenPrelims Intermedaite AcctgJohn Evan Raymund BesidNoch keine Bewertungen

- Nissan FinalDokument4 SeitenNissan FinalPrince Jayanmar BerbaNoch keine Bewertungen

- Cash ProblemsDokument5 SeitenCash ProblemsAnna AldaveNoch keine Bewertungen

- Auditing Practice Problem 6Dokument2 SeitenAuditing Practice Problem 6Jessa Gay Cartagena TorresNoch keine Bewertungen

- Audit of Cash and Cash Equivalents - Set BDokument5 SeitenAudit of Cash and Cash Equivalents - Set BZyrah Mae SaezNoch keine Bewertungen

- Statement of Account: Transaction Date Description DebitDokument2 SeitenStatement of Account: Transaction Date Description DebitIkramNoch keine Bewertungen

- A. Anggaran Pengumpulan PiutangDokument4 SeitenA. Anggaran Pengumpulan PiutangSafri SimabuaNoch keine Bewertungen

- Proof of Cash Simulated ProblemDokument3 SeitenProof of Cash Simulated ProblemephraimNoch keine Bewertungen

- Proof of Cash - DiscussionDokument4 SeitenProof of Cash - DiscussionJoyce Anne GarduqueNoch keine Bewertungen

- Auditing ProblemsDokument17 SeitenAuditing ProblemsKathleenCusipagNoch keine Bewertungen

- Sweet Beginnings CoDokument11 SeitenSweet Beginnings CoJonalyn LodorNoch keine Bewertungen

- Sweet Beginnings Co PDFDokument11 SeitenSweet Beginnings Co PDFannica castroNoch keine Bewertungen

- Sweet Beginnings Co.Dokument11 SeitenSweet Beginnings Co.Andrew Farol67% (3)

- Pak Enings HTDokument15 SeitenPak Enings HTVincent SampianoNoch keine Bewertungen

- This Study Resource WasDokument3 SeitenThis Study Resource WasKyree VladeNoch keine Bewertungen

- DocxDokument25 SeitenDocxPhilip Castro67% (3)

- Debits and Credits - Bad DebtDokument25 SeitenDebits and Credits - Bad DebtRevilyn Grace Bangayan100% (1)

- Auditing Problems v1 2018 CompressDokument36 SeitenAuditing Problems v1 2018 CompressMr. CopernicusNoch keine Bewertungen

- Date Debit CreditDokument7 SeitenDate Debit CreditVincent SampianoNoch keine Bewertungen

- Institute of Accountancy Arusha Department of Accounting and Finance Principles of Accounts (Aft 05101) SEMINAR QUESTIONS - 2021/2022Dokument44 SeitenInstitute of Accountancy Arusha Department of Accounting and Finance Principles of Accounts (Aft 05101) SEMINAR QUESTIONS - 2021/2022AnithaNoch keine Bewertungen

- Bank Reconciliation Practice ProblemDokument2 SeitenBank Reconciliation Practice ProblemMikee RizonNoch keine Bewertungen

- Problem 1 - Dallas CorporationDokument6 SeitenProblem 1 - Dallas CorporationKatherine Cabading InocandoNoch keine Bewertungen

- Sweet Beginnings Co - XLSX CASE STUDY ANSWERDokument11 SeitenSweet Beginnings Co - XLSX CASE STUDY ANSWERYna AlfonsoNoch keine Bewertungen

- Lembar Kerja Pt. Aldenio Jurnal KhususDokument73 SeitenLembar Kerja Pt. Aldenio Jurnal KhususSalsabila Syifa AriesfiaNoch keine Bewertungen

- Lembar KerjaDokument70 SeitenLembar KerjaSalsabila Syifa AriesfiaNoch keine Bewertungen

- Aquarius Company Worksheet August 31, 2018: Unadjusted Trial Balance Debit CreditDokument35 SeitenAquarius Company Worksheet August 31, 2018: Unadjusted Trial Balance Debit CreditAdam Cuenca100% (1)

- Ms - MuffDokument17 SeitenMs - MuffDayuman LagasiNoch keine Bewertungen

- Parcial2 - Actividades de La Semana 4Dokument23 SeitenParcial2 - Actividades de La Semana 4Luis Eduardo Meunier MendezNoch keine Bewertungen

- LEMBAR KERJA PT. ALDENIO Sampai BALANCE SHEETDokument76 SeitenLEMBAR KERJA PT. ALDENIO Sampai BALANCE SHEETSalsabila Syifa AriesfiaNoch keine Bewertungen

- Enter Data in Yellow Fields Workings: 723,658 Slab Amount (Old)Dokument9 SeitenEnter Data in Yellow Fields Workings: 723,658 Slab Amount (Old)HarryNoch keine Bewertungen

- Parcial2 - Actividades de La Semana 4 KevvDokument23 SeitenParcial2 - Actividades de La Semana 4 KevvLuis Eduardo Meunier MendezNoch keine Bewertungen

- Lembar Kerja KosongDokument46 SeitenLembar Kerja Kosonglisa oktaviaNoch keine Bewertungen

- Assignment 1Dokument12 SeitenAssignment 1Ira YbanezNoch keine Bewertungen

- For The Year Ended Year 1 Year 2 Year 3 Year 4: Income Statement ParticularsDokument5 SeitenFor The Year Ended Year 1 Year 2 Year 3 Year 4: Income Statement ParticularsTanya SinghNoch keine Bewertungen

- Petty Cash FormDokument12 SeitenPetty Cash FormJustiniel JimenezNoch keine Bewertungen

- AnswerDokument23 SeitenAnswerYousaf BhuttaNoch keine Bewertungen

- Net Present ValueDokument6 SeitenNet Present ValueIshita KapadiaNoch keine Bewertungen

- Final Daily Cash (AutoRecovered)Dokument47 SeitenFinal Daily Cash (AutoRecovered)Isabella MichelliaNoch keine Bewertungen

- Bac 204 - Cat 1Dokument4 SeitenBac 204 - Cat 1duncanmaina204Noch keine Bewertungen

- Current YearcurrDokument4 SeitenCurrent YearcurrSanjay SinghNoch keine Bewertungen

- Benefits Per EmployeeDokument4 SeitenBenefits Per Employeeapi-3740993Noch keine Bewertungen

- 740 BasisallotmentDokument1 Seite740 BasisallotmentzainalNoch keine Bewertungen

- Capital Budgeting Practices A Study of Companies Listed On The Colombo Stock Exchange Sri LankaDokument9 SeitenCapital Budgeting Practices A Study of Companies Listed On The Colombo Stock Exchange Sri LankamhldcnNoch keine Bewertungen

- Finex ServicesDokument3 SeitenFinex Servicesggn08Noch keine Bewertungen

- Cash Management-Models: Baumol Model Miller-Orr Model Orgler's ModelDokument5 SeitenCash Management-Models: Baumol Model Miller-Orr Model Orgler's ModelnarayanNoch keine Bewertungen

- Ssi FinancingDokument7 SeitenSsi FinancingAnanya ChoudharyNoch keine Bewertungen

- Perpetual Inventory SystemDokument8 SeitenPerpetual Inventory SystemChristianne Joyse MerreraNoch keine Bewertungen

- Recruitment Selection Process in HDFCDokument102 SeitenRecruitment Selection Process in HDFCaccord123100% (2)

- Global Risk Risk Methodology - Model Validation Risk Stress TestingDokument4 SeitenGlobal Risk Risk Methodology - Model Validation Risk Stress TestingRaj AgarwalNoch keine Bewertungen

- Insurance For Specific EventsDokument1 SeiteInsurance For Specific Eventsihsan nawawiNoch keine Bewertungen

- Midterm I 2022 KEYDokument17 SeitenMidterm I 2022 KEYkuo zoeNoch keine Bewertungen

- Far270 July2022Dokument8 SeitenFar270 July2022Nur Fatin AmirahNoch keine Bewertungen

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Dokument1 SeiteTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)raviNoch keine Bewertungen

- Desirable Corporate Governance: A CodeDokument16 SeitenDesirable Corporate Governance: A CodesiddharthanandNoch keine Bewertungen

- Pledge-Contract Act: Simar MakkarDokument8 SeitenPledge-Contract Act: Simar MakkarPearl LalwaniNoch keine Bewertungen

- Central Banking and Financial RegulationsDokument9 SeitenCentral Banking and Financial RegulationsHasibul IslamNoch keine Bewertungen

- Quote - Q2045201Dokument2 SeitenQuote - Q2045201makhanyasibusisiwe7Noch keine Bewertungen

- Econ282 F11 PS5 AnswersDokument7 SeitenEcon282 F11 PS5 AnswersVishesh GuptaNoch keine Bewertungen

- NPS BrochureDokument21 SeitenNPS BrochureEsther Leihang100% (1)

- INSURANCE TambasacanDokument80 SeitenINSURANCE Tambasacanlee50% (2)

- Tally PracticeDokument16 SeitenTally PracticeArko Banerjee100% (3)

- IB - 19 - PetitionerDokument30 SeitenIB - 19 - PetitionerKushagra TolambiaNoch keine Bewertungen

- Welcome To Presentation On Discharge of SuretyDokument18 SeitenWelcome To Presentation On Discharge of SuretyAmit Gurav94% (16)

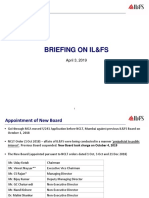

- ILFS Briefing (April 2019)Dokument15 SeitenILFS Briefing (April 2019)Richard DierdreNoch keine Bewertungen

- Week 1 MSTA Notes PDFDokument93 SeitenWeek 1 MSTA Notes PDFMohd Najmi HuzaiNoch keine Bewertungen

- Solved Twelve Years Ago Marilyn Purchased Two Lots in An UndevelopedDokument1 SeiteSolved Twelve Years Ago Marilyn Purchased Two Lots in An UndevelopedAnbu jaromiaNoch keine Bewertungen

- Fin Ca2 FinalDokument6 SeitenFin Ca2 FinalVaishali SonareNoch keine Bewertungen

- UPSA 2019 Tutorial Questions Fs WITH ANSWERSDokument14 SeitenUPSA 2019 Tutorial Questions Fs WITH ANSWERSLaud ListowellNoch keine Bewertungen

- Introduction To Asset Liability and Risk MGMTDokument147 SeitenIntroduction To Asset Liability and Risk MGMTMani ManandharNoch keine Bewertungen

- Statement 1688358203630Dokument3 SeitenStatement 1688358203630Chinmay RajNoch keine Bewertungen

- 705 - PGBP AdjustmentsDokument10 Seiten705 - PGBP AdjustmentsKumar SwamyNoch keine Bewertungen