Das könnte Ihnen auch gefallen

- Audit of Shareholders EquityDokument5 SeitenAudit of Shareholders EquityAldwin LlevaNoch keine Bewertungen

- Mindanao State University College of Business Administration and Accountancy Marawi CityDokument7 SeitenMindanao State University College of Business Administration and Accountancy Marawi CityHasmin Saripada AmpatuaNoch keine Bewertungen

- Audit of Property, Plant and EquipmentDokument13 SeitenAudit of Property, Plant and EquipmentHijabwear BizNoch keine Bewertungen

- Audit of LiabilityDokument8 SeitenAudit of LiabilityMark Lord Morales Bumagat50% (2)

- AUDProb TEST BANKDokument28 SeitenAUDProb TEST BANKFrancine HollerNoch keine Bewertungen

- CHAPTER 2 Caselette - Correction of ErrorsDokument37 SeitenCHAPTER 2 Caselette - Correction of Errorsmjc24100% (4)

- CHAPTER 8 - Audit of Liabilities: Problem 1Dokument27 SeitenCHAPTER 8 - Audit of Liabilities: Problem 1Mikaela Gale CatabayNoch keine Bewertungen

- AP.2808 - Audit of Equity MAY 2020: Auditing Problems Ocampo/Cabarles/Soliman/OcampoDokument5 SeitenAP.2808 - Audit of Equity MAY 2020: Auditing Problems Ocampo/Cabarles/Soliman/OcampoMay Grethel Joy PeranteNoch keine Bewertungen

- Accounting 14 - Applied Auditing OkDokument12 SeitenAccounting 14 - Applied Auditing OkNico evansNoch keine Bewertungen

- Audit of Investments 1Dokument2 SeitenAudit of Investments 1Raz MahariNoch keine Bewertungen

- Far Test BankDokument37 SeitenFar Test BankheyheyNoch keine Bewertungen

- Audit of PPE 2Dokument2 SeitenAudit of PPE 2Raz MahariNoch keine Bewertungen

- Applied Auditing Audit of Intangibles and Correction of ErrorsDokument2 SeitenApplied Auditing Audit of Intangibles and Correction of ErrorsCar Mae La67% (3)

- Cash To Accrual Basis, Single Entry and Error CorrectionDokument7 SeitenCash To Accrual Basis, Single Entry and Error CorrectionHasmin Saripada AmpatuaNoch keine Bewertungen

- Intermacc Inventories and Bio Assets Postlec WaDokument2 SeitenIntermacc Inventories and Bio Assets Postlec WaClarice Awa-aoNoch keine Bewertungen

- AP 08 Substantive Audit Tests of EquityDokument2 SeitenAP 08 Substantive Audit Tests of EquityJobby JaranillaNoch keine Bewertungen

- May 2020 - AP Drill 2 (PPE and Intangibles) - Answer KeyDokument8 SeitenMay 2020 - AP Drill 2 (PPE and Intangibles) - Answer KeyROMAR A. PIGANoch keine Bewertungen

- College of Accountancy and Finance: 1st Semester, S.Y. 2018-2019 Page 1 of 4 Prof. GMDokument4 SeitenCollege of Accountancy and Finance: 1st Semester, S.Y. 2018-2019 Page 1 of 4 Prof. GMPpp BbbNoch keine Bewertungen

- First QuizDokument4 SeitenFirst QuizArn HicoNoch keine Bewertungen

- Audit-Of Inventory ACHA - KJDokument47 SeitenAudit-Of Inventory ACHA - KJKhrisna Joy AchaNoch keine Bewertungen

- Audit of InventoriesDokument4 SeitenAudit of InventoriesMc Gavriel VillenaNoch keine Bewertungen

- Problem No. 1: Practice Set Property Plant and EquipmentDokument4 SeitenProblem No. 1: Practice Set Property Plant and EquipmentFiona MoralesNoch keine Bewertungen

- Audit of EquityDokument5 SeitenAudit of EquityKarlo Jude Acidera0% (1)

- Auditing Problems Midterm - 2021 - DDokument17 SeitenAuditing Problems Midterm - 2021 - DjasfNoch keine Bewertungen

- VALIX - Chapter 5Dokument28 SeitenVALIX - Chapter 5glenn langcuyan100% (1)

- AP.2807 Liabilities.Dokument7 SeitenAP.2807 Liabilities.May Grethel Joy PeranteNoch keine Bewertungen

- Audit of Liabilities Problem No. 1: Auditing ProblemsDokument8 SeitenAudit of Liabilities Problem No. 1: Auditing ProblemsSailah DimakutaNoch keine Bewertungen

- Audit of Property, Plant and Equipment (PPE) : Auditing Problems AP.0102Dokument8 SeitenAudit of Property, Plant and Equipment (PPE) : Auditing Problems AP.0102Mae0% (1)

- Chapter 16Dokument18 SeitenChapter 16Clarize R. Mabiog100% (1)

- Audit of Intangible AssetsDokument8 SeitenAudit of Intangible AssetsMikaela Graciel AnneNoch keine Bewertungen

- Aud Application 2 - Handout 7 Wasting Asset (UST)Dokument5 SeitenAud Application 2 - Handout 7 Wasting Asset (UST)RNoch keine Bewertungen

- Auditing JPIADokument18 SeitenAuditing JPIAAken Lieram Ats AnaNoch keine Bewertungen

- Module 5 - Audit of InventoriesDokument23 SeitenModule 5 - Audit of InventoriesIvan LandaosNoch keine Bewertungen

- Quiz - Intangible Assets With QuestionsDokument3 SeitenQuiz - Intangible Assets With Questionsjanus lopezNoch keine Bewertungen

- AUDITING PROBLEM - From Audit of InvestmentDokument60 SeitenAUDITING PROBLEM - From Audit of InvestmentMa. Hazel Donita Diaz100% (1)

- Chapter 5 Audit of InventoryDokument10 SeitenChapter 5 Audit of InventoryMarkie GrabilloNoch keine Bewertungen

- Liabilities Deferred TaxDokument3 SeitenLiabilities Deferred TaxHikari0% (1)

- Audit of Shareholders' Equity: Auditing ProblemsDokument4 SeitenAudit of Shareholders' Equity: Auditing ProblemsKenneth Adrian AlabadoNoch keine Bewertungen

- Unit 6 AUDIT OF INTANGIBLE ASSETS Lecture Notes 2020Dokument11 SeitenUnit 6 AUDIT OF INTANGIBLE ASSETS Lecture Notes 2020Marynelle Labrador Sevilla100% (1)

- FinACt 5 Foreign Currency TransactionsDokument2 SeitenFinACt 5 Foreign Currency TransactionsBedynz Mark Pimentel100% (2)

- Audit of Investments - Set BDokument4 SeitenAudit of Investments - Set BZyrah Mae Saez0% (1)

- PPE NotesDokument4 SeitenPPE Notesaldric taclanNoch keine Bewertungen

- The Risk-Based Audit ProcessDokument16 SeitenThe Risk-Based Audit ProcessCarlo manejaNoch keine Bewertungen

- Auditing Problems Finals Exam 2020Dokument9 SeitenAuditing Problems Finals Exam 2020VictorioLazaro0% (1)

- Practical Accounting 1: 2011 National Cpa Mock Board ExaminationDokument7 SeitenPractical Accounting 1: 2011 National Cpa Mock Board Examinationcacho cielo graceNoch keine Bewertungen

- Far-1 4Dokument3 SeitenFar-1 4Raymundo Eirah100% (1)

- Shareholder S Equity ReviewerDokument20 SeitenShareholder S Equity ReviewerKarlovy DalinNoch keine Bewertungen

- QUIZ7 Audit of LiabilitiesDokument3 SeitenQUIZ7 Audit of LiabilitiesCarmela GulapaNoch keine Bewertungen

- Thery of AccountsDokument13 SeitenThery of AccountsTerrence Von KnightNoch keine Bewertungen

- Audprob Final Exam 1Dokument26 SeitenAudprob Final Exam 1Joody CatacutanNoch keine Bewertungen

- Audt3 - Applied Auditing Complete ModuleDokument232 SeitenAudt3 - Applied Auditing Complete ModuleDominique Anne BenozaNoch keine Bewertungen

- EquityDokument4 SeitenEquityZairah FranciscoNoch keine Bewertungen

- Ap 200Dokument9 SeitenAp 200Christine Jane AbangNoch keine Bewertungen

- Handouts 169Dokument15 SeitenHandouts 169Rio Cyrel CelleroNoch keine Bewertungen

- AP-100Q: Financing Cycle: A S ' E: Udit of Tockholders QuityDokument12 SeitenAP-100Q: Financing Cycle: A S ' E: Udit of Tockholders QuityShiela RengelNoch keine Bewertungen

- Audit of SHEDokument13 SeitenAudit of SHEChristian QuintansNoch keine Bewertungen

- Ap She Exam ProbDokument3 SeitenAp She Exam Problois martinNoch keine Bewertungen

- Chapter 8-SHEDokument77 SeitenChapter 8-SHEVip Bigbang100% (1)

- M36 - Quizzer 4Dokument5 SeitenM36 - Quizzer 4Joshua DaarolNoch keine Bewertungen

- EquityDokument2 SeitenEquityjethro carlobos0% (1)

- Berkenkotter vs. Cu Unjieng, Mabalacat Sugar, and Sheriff of Pampanga G.R. No. L-41643, July 31, 1935Dokument1 SeiteBerkenkotter vs. Cu Unjieng, Mabalacat Sugar, and Sheriff of Pampanga G.R. No. L-41643, July 31, 1935Edeniel CambarihanNoch keine Bewertungen

- Bookkeeping NC 3 Review GuideDokument6 SeitenBookkeeping NC 3 Review GuideCatherine Hidalgo100% (1)

- MGMT 702 Fall 2021 Research and Case Analysis No. 1 (10%) Part B (Warren Buffett and Berkshire Hathaway Inc.) - QuestionsDokument5 SeitenMGMT 702 Fall 2021 Research and Case Analysis No. 1 (10%) Part B (Warren Buffett and Berkshire Hathaway Inc.) - QuestionsJesus D. RiosNoch keine Bewertungen

- IR Presentation: Mitsubishi UFJ Financial Group, IncDokument90 SeitenIR Presentation: Mitsubishi UFJ Financial Group, IncyolandaNoch keine Bewertungen

- Debt Deception: How Debt Buyers Abuse The Legal System To Prey On Lower-Income New Yorkers (2010)Dokument36 SeitenDebt Deception: How Debt Buyers Abuse The Legal System To Prey On Lower-Income New Yorkers (2010)Jillian Sheridan100% (1)

- Becoming Market SmithDokument82 SeitenBecoming Market SmithTu D.Noch keine Bewertungen

- Classification of AccountsDokument12 SeitenClassification of AccountsNaurah Atika DinaNoch keine Bewertungen

- Job Advert-Financial Accounting ManagerDokument3 SeitenJob Advert-Financial Accounting ManagerTawanda ZimbiziNoch keine Bewertungen

- Almarai Annual Report enDokument128 SeitenAlmarai Annual Report enHassen AbidiNoch keine Bewertungen

- University of The Cordilleras Accounting 1/2 Lecture AidDokument3 SeitenUniversity of The Cordilleras Accounting 1/2 Lecture AidJesseca JosafatNoch keine Bewertungen

- Certificado Id182139 Cl329487 InboxMail370538 CopyFrom 20140201-405-19186 DocOK PDFDokument65 SeitenCertificado Id182139 Cl329487 InboxMail370538 CopyFrom 20140201-405-19186 DocOK PDFFernando ArdenghiNoch keine Bewertungen

- Mutual Funds Investment India - Save Taxes & Grow Wealth Online - ClearTax InvestDokument7 SeitenMutual Funds Investment India - Save Taxes & Grow Wealth Online - ClearTax InvestDevaraja DNoch keine Bewertungen

- Risk ManagementDokument1 SeiteRisk ManagementThảo NguyễnNoch keine Bewertungen

- Cost of New Investment-OS 3,250k: Undervalued Equipment P100k X 40% Ownership P40k/5 P8kDokument1 SeiteCost of New Investment-OS 3,250k: Undervalued Equipment P100k X 40% Ownership P40k/5 P8kQueenie ValleNoch keine Bewertungen

- Green Banking Practices in BangladeshDokument6 SeitenGreen Banking Practices in BangladeshIOSRjournal100% (1)

- Slip Accomodation Dan TransportationDokument5 SeitenSlip Accomodation Dan Transportationbovan28Noch keine Bewertungen

- 9 Basics of Capital Expenditure DecisionsDokument37 Seiten9 Basics of Capital Expenditure DecisionsHarishYadavNoch keine Bewertungen

- 0088470515-Premium Deposit Acknowledgement PDFDokument1 Seite0088470515-Premium Deposit Acknowledgement PDFjayanandaNoch keine Bewertungen

- Yes Bank 2004-05Dokument133 SeitenYes Bank 2004-05Sagar ShawNoch keine Bewertungen

- Chapter 5-Merchandising OperationsDokument46 SeitenChapter 5-Merchandising OperationsSina RahimiNoch keine Bewertungen

- Obligasi - PembahasanDokument18 SeitenObligasi - Pembahasangaffar aimNoch keine Bewertungen

- Blackrock Quarterly UpdateDokument11 SeitenBlackrock Quarterly UpdateZorrays JunaidNoch keine Bewertungen

- Shapiro Chapter 07 SolutionsDokument12 SeitenShapiro Chapter 07 SolutionsRuiting Chen100% (1)

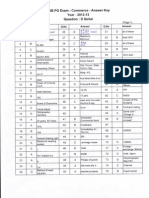

- TRB Commerce - PG - Answer Key 2012Dokument2 SeitenTRB Commerce - PG - Answer Key 2012babu4in1Noch keine Bewertungen

- HUKUM SekuritisasiDokument17 SeitenHUKUM SekuritisasiAninditaNoch keine Bewertungen

- CFA-Chapter 7 Relative ValuationDokument62 SeitenCFA-Chapter 7 Relative ValuationNoman MaqsoodNoch keine Bewertungen

- Final Report Financial Institution OperationsDokument13 SeitenFinal Report Financial Institution OperationsyeohzynguanNoch keine Bewertungen

- Background To IPSAS Implementation in NigeriaDokument28 SeitenBackground To IPSAS Implementation in NigeriaAkinmulewo Ayodele67% (3)

- Front Office Accounting System TerminologyDokument6 SeitenFront Office Accounting System TerminologypranithNoch keine Bewertungen

- Market Report Q4 2023 VietnamDokument17 SeitenMarket Report Q4 2023 VietnamchienNoch keine Bewertungen

- Here, Right Matters: An American StoryVon EverandHere, Right Matters: An American StoryBewertung: 4 von 5 Sternen4/5 (24)

- Perversion of Justice: The Jeffrey Epstein StoryVon EverandPerversion of Justice: The Jeffrey Epstein StoryBewertung: 4.5 von 5 Sternen4.5/5 (10)

- For the Thrill of It: Leopold, Loeb, and the Murder That Shocked Jazz Age ChicagoVon EverandFor the Thrill of It: Leopold, Loeb, and the Murder That Shocked Jazz Age ChicagoBewertung: 4 von 5 Sternen4/5 (97)

- University of Berkshire Hathaway: 30 Years of Lessons Learned from Warren Buffett & Charlie Munger at the Annual Shareholders MeetingVon EverandUniversity of Berkshire Hathaway: 30 Years of Lessons Learned from Warren Buffett & Charlie Munger at the Annual Shareholders MeetingBewertung: 4.5 von 5 Sternen4.5/5 (98)

- Reasonable Doubts: The O.J. Simpson Case and the Criminal Justice SystemVon EverandReasonable Doubts: The O.J. Simpson Case and the Criminal Justice SystemBewertung: 4 von 5 Sternen4/5 (25)

- Lady Killers: Deadly Women Throughout HistoryVon EverandLady Killers: Deadly Women Throughout HistoryBewertung: 4 von 5 Sternen4/5 (155)

- Dean Corll: The True Story of The Houston Mass MurdersVon EverandDean Corll: The True Story of The Houston Mass MurdersBewertung: 4 von 5 Sternen4/5 (29)

- Summary: Surrounded by Idiots: The Four Types of Human Behavior and How to Effectively Communicate with Each in Business (and in Life) by Thomas Erikson: Key Takeaways, Summary & AnalysisVon EverandSummary: Surrounded by Idiots: The Four Types of Human Behavior and How to Effectively Communicate with Each in Business (and in Life) by Thomas Erikson: Key Takeaways, Summary & AnalysisBewertung: 4 von 5 Sternen4/5 (2)

- Hunting Whitey: The Inside Story of the Capture & Killing of America's Most Wanted Crime BossVon EverandHunting Whitey: The Inside Story of the Capture & Killing of America's Most Wanted Crime BossBewertung: 3.5 von 5 Sternen3.5/5 (6)

- The Law of the Land: The Evolution of Our Legal SystemVon EverandThe Law of the Land: The Evolution of Our Legal SystemBewertung: 4.5 von 5 Sternen4.5/5 (11)

- Reading the Constitution: Why I Chose Pragmatism, not TextualismVon EverandReading the Constitution: Why I Chose Pragmatism, not TextualismBewertung: 4 von 5 Sternen4/5 (1)

- The Killer Across the Table: Unlocking the Secrets of Serial Killers and Predators with the FBI's Original MindhunterVon EverandThe Killer Across the Table: Unlocking the Secrets of Serial Killers and Predators with the FBI's Original MindhunterBewertung: 4.5 von 5 Sternen4.5/5 (456)

- Nine Black Robes: Inside the Supreme Court's Drive to the Right and Its Historic ConsequencesVon EverandNine Black Robes: Inside the Supreme Court's Drive to the Right and Its Historic ConsequencesNoch keine Bewertungen

- The Edge of Innocence: The Trial of Casper BennettVon EverandThe Edge of Innocence: The Trial of Casper BennettBewertung: 4.5 von 5 Sternen4.5/5 (3)

- The ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!Von EverandThe ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!Bewertung: 4.5 von 5 Sternen4.5/5 (14)

- Free & Clear, Standing & Quiet Title: 11 Possible Ways to Get Rid of Your MortgageVon EverandFree & Clear, Standing & Quiet Title: 11 Possible Ways to Get Rid of Your MortgageBewertung: 2 von 5 Sternen2/5 (3)

- All You Need to Know About the Music Business: Eleventh EditionVon EverandAll You Need to Know About the Music Business: Eleventh EditionNoch keine Bewertungen

- The Articulate Advocate: Persuasive Skills for Lawyers in Trials, Appeals, Arbitrations, and MotionsVon EverandThe Articulate Advocate: Persuasive Skills for Lawyers in Trials, Appeals, Arbitrations, and MotionsBewertung: 5 von 5 Sternen5/5 (5)

- Insider's Guide To Your First Year Of Law School: A Student-to-Student Handbook from a Law School SurvivorVon EverandInsider's Guide To Your First Year Of Law School: A Student-to-Student Handbook from a Law School SurvivorBewertung: 3.5 von 5 Sternen3.5/5 (3)

- Buffettology: The Previously Unexplained Techniques That Have Made Warren Buffett American's Most Famous InvestorVon EverandBuffettology: The Previously Unexplained Techniques That Have Made Warren Buffett American's Most Famous InvestorBewertung: 4.5 von 5 Sternen4.5/5 (132)

- Beyond the Body Farm: A Legendary Bone Detective Explores Murders, Mysteries, and the Revolution in Forensic ScienceVon EverandBeyond the Body Farm: A Legendary Bone Detective Explores Murders, Mysteries, and the Revolution in Forensic ScienceBewertung: 4 von 5 Sternen4/5 (107)

- Learning to Disagree: The Surprising Path to Navigating Differences with Empathy and RespectVon EverandLearning to Disagree: The Surprising Path to Navigating Differences with Empathy and RespectNoch keine Bewertungen

- A Contractor's Guide to the FIDIC Conditions of ContractVon EverandA Contractor's Guide to the FIDIC Conditions of ContractNoch keine Bewertungen

- We Were Once a Family: A Story of Love, Death, and Child Removal in AmericaVon EverandWe Were Once a Family: A Story of Love, Death, and Child Removal in AmericaBewertung: 4.5 von 5 Sternen4.5/5 (53)

- Construction Claims and Responses: Effective Writing and PresentationVon EverandConstruction Claims and Responses: Effective Writing and PresentationNoch keine Bewertungen