Das könnte Ihnen auch gefallen

- TUGAS AKMEN UciiiDokument24 SeitenTUGAS AKMEN UciiiFadhliyaFNoch keine Bewertungen

- HiyasDokument6 SeitenHiyasnilo VillablancaNoch keine Bewertungen

- Assets LiabilitiesDokument4 SeitenAssets LiabilitiesSneha DasNoch keine Bewertungen

- Statement of Account: Name: Pineda, Robert Stall: C Dry 29Dokument4 SeitenStatement of Account: Name: Pineda, Robert Stall: C Dry 29Ransey Ace AndalloNoch keine Bewertungen

- Fra en 2024Dokument1 SeiteFra en 2024bahraui saifeNoch keine Bewertungen

- Loida Page 2Dokument3 SeitenLoida Page 2Aina HermoNoch keine Bewertungen

- Problem 1: Customer Balance Comments From Customer Audit FindingsDokument5 SeitenProblem 1: Customer Balance Comments From Customer Audit FindingsReginald ValenciaNoch keine Bewertungen

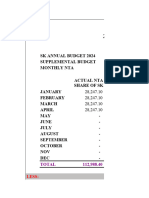

- Dangcol New SK Monitoring For Year 2024Dokument9 SeitenDangcol New SK Monitoring For Year 2024Katherine Anne SantosNoch keine Bewertungen

- DownloadDokument2 SeitenDownloads1u2m3a4n5giriNoch keine Bewertungen

- Summary of Payables To PadsiDokument5 SeitenSummary of Payables To Padsiandrea BernardoNoch keine Bewertungen

- Trading Profit & LossDokument3 SeitenTrading Profit & LossKunal ChaudharyNoch keine Bewertungen

- Bank Statement Bank SEPTEMBERDokument6 SeitenBank Statement Bank SEPTEMBERDamara ArfianNoch keine Bewertungen

- Practice SetDokument100 SeitenPractice SetZamantha Oliveros100% (1)

- Ink Books SuppliesDokument63 SeitenInk Books SuppliesZamantha Oliveros100% (1)

- Ink Books SuppliesDokument81 SeitenInk Books SuppliesZamantha Oliveros100% (1)

- Ink Books Supplies 2Dokument94 SeitenInk Books Supplies 2Zamantha Oliveros100% (1)

- KHF Dec-JanDokument13 SeitenKHF Dec-Janlloydmarkagris143Noch keine Bewertungen

- Chewens-Minimart Income Statement April 2022Dokument8 SeitenChewens-Minimart Income Statement April 2022Dv Accounting100% (1)

- Turritopsis Dohrnii Teo en Ming's CPF Contribution History Jun 2020 To Aug 2021Dokument1 SeiteTurritopsis Dohrnii Teo en Ming's CPF Contribution History Jun 2020 To Aug 2021Turritopsis Dohrnii Teo En MingNoch keine Bewertungen

- Neraca Penyesuaian - Timotius Siagian 1 C3Dokument38 SeitenNeraca Penyesuaian - Timotius Siagian 1 C3Timotius SiagianNoch keine Bewertungen

- RSV Dragonfruit-LedgerDokument4 SeitenRSV Dragonfruit-LedgerRoger VenturaNoch keine Bewertungen

- 12) December 2021 ParDokument22 Seiten12) December 2021 ParMaria Rubie CoranezNoch keine Bewertungen

- Statement of Account Argentina As at 31 August 2020: Receivable Outstanding 4,154,353 4,360,233Dokument1 SeiteStatement of Account Argentina As at 31 August 2020: Receivable Outstanding 4,154,353 4,360,233shahid2opuNoch keine Bewertungen

- Bills Payment DuedateDokument2 SeitenBills Payment DuedateKiemer Terrence SechicoNoch keine Bewertungen

- For Rent HeheDokument19 SeitenFor Rent HeheGabriel AfricaNoch keine Bewertungen

- Rent StatementDokument2 SeitenRent StatementJonathan Seagull LivingstonNoch keine Bewertungen

- ExportDokument6 SeitenExportAhmed MohamedNoch keine Bewertungen

- Quiz Audit of CashDokument3 SeitenQuiz Audit of CashwesNoch keine Bewertungen

- Dockers Inc Proof of CashDokument1 SeiteDockers Inc Proof of CashJoemar LegresoNoch keine Bewertungen

- Ersonal Budget Stephano Chobwe Kanyinji-2022Dokument8 SeitenErsonal Budget Stephano Chobwe Kanyinji-2022Chobwe Stephano KanyinjiNoch keine Bewertungen

- BTVN Chapter 6 New 1Dokument21 SeitenBTVN Chapter 6 New 1hangptt214051Noch keine Bewertungen

- FAMILLY LAUNDRY INVOICE 30 AgustusDokument1 SeiteFAMILLY LAUNDRY INVOICE 30 AgustusakswtkNoch keine Bewertungen

- Auditing Problems: Let'S Go!Dokument8 SeitenAuditing Problems: Let'S Go!AiahNoch keine Bewertungen

- Accounting Payroll February.4.2022-Releasing ReceiptDokument8 SeitenAccounting Payroll February.4.2022-Releasing Receiptcherish nicole lopezNoch keine Bewertungen

- Principles of AccountingDokument7 SeitenPrinciples of AccountingDanish MuradNoch keine Bewertungen

- Total: Remaining BalanceDokument7 SeitenTotal: Remaining Balancemarissa pallananNoch keine Bewertungen

- 2017-2020 BALANCE SHEET: Non-Current AssetsDokument10 Seiten2017-2020 BALANCE SHEET: Non-Current AssetsFrancois MarcialNoch keine Bewertungen

- BTVN Chapter 6 NewDokument22 SeitenBTVN Chapter 6 Newhangptt214051Noch keine Bewertungen

- Arce - Chan Accounting FirmDokument38 SeitenArce - Chan Accounting FirmshaneNoch keine Bewertungen

- Quiz No. 2Dokument5 SeitenQuiz No. 2VernnNoch keine Bewertungen

- Audit of Cash and Cash EquivalentsDokument5 SeitenAudit of Cash and Cash Equivalentsdummy accountNoch keine Bewertungen

- PF Contribution 06 2021Dokument1 SeitePF Contribution 06 2021Mehraj PashaNoch keine Bewertungen

- PINK .E Lease End StatementDokument2 SeitenPINK .E Lease End StatementBilly MainaNoch keine Bewertungen

- Integrated Accounting 2Dokument10 SeitenIntegrated Accounting 2EeuhNoch keine Bewertungen

- The Enhancement Program Handouts - Far PDFDokument36 SeitenThe Enhancement Program Handouts - Far PDFRica Jane Lloren0% (1)

- Advanced Accounting PDokument4 SeitenAdvanced Accounting PMaurice Agbayani100% (1)

- 10 Premium BookkeepingDokument1.029 Seiten10 Premium BookkeepingmaryhenthornphdNoch keine Bewertungen

- PF Contribution 01 2021Dokument1 SeitePF Contribution 01 2021srajive169Noch keine Bewertungen

- Accounting (AutoRecovered)Dokument11 SeitenAccounting (AutoRecovered)ernest mwandihiNoch keine Bewertungen

- Class ExerciseDokument1 SeiteClass ExerciseChristina KaukareNoch keine Bewertungen

- Fttbts Mindanao TrackerDokument436 SeitenFttbts Mindanao TrackerCarl Jhesfer TarataraNoch keine Bewertungen

- Class Exercise SolutionDokument10 SeitenClass Exercise SolutionChristina KaukareNoch keine Bewertungen

- 6021-P2-Lembar KerjaDokument46 Seiten6021-P2-Lembar KerjarudiNoch keine Bewertungen

- Business Report Nila & Ferdi Periode 2023: Achievement/day - 23,391,144 RP 86,110,000 RP 54,320,000Dokument24 SeitenBusiness Report Nila & Ferdi Periode 2023: Achievement/day - 23,391,144 RP 86,110,000 RP 54,320,000Ferdi PutraNoch keine Bewertungen

- Business Report Nila & Ferdi Periode 2023: Achievement/day - 23,391,144 RP 86,110,000 RP 54,320,000Dokument16 SeitenBusiness Report Nila & Ferdi Periode 2023: Achievement/day - 23,391,144 RP 86,110,000 RP 54,320,000Ferdi PutraNoch keine Bewertungen

- Loan Schedule 2021-2022Dokument4 SeitenLoan Schedule 2021-2022Kevin AlvarezNoch keine Bewertungen

- Antonio, Ysa Elaine - 3A8Dokument2 SeitenAntonio, Ysa Elaine - 3A8Elaine AntonioNoch keine Bewertungen

- GPP Calendar of Activities 2022 23 SdoDokument5 SeitenGPP Calendar of Activities 2022 23 SdoRomel GarciaNoch keine Bewertungen

- Full Project LibraryDokument77 SeitenFull Project LibraryChala Geta0% (1)

- Magic Bullet Theory - PPTDokument5 SeitenMagic Bullet Theory - PPTThe Bengal ChariotNoch keine Bewertungen

- Culture 2007 2013 Projects Overview 2018-03-18Dokument133 SeitenCulture 2007 2013 Projects Overview 2018-03-18PontesDeboraNoch keine Bewertungen

- Nantai Catalog NewDokument30 SeitenNantai Catalog Newspalomos100% (1)

- A Literature Review of Retailing Sector and BusineDokument21 SeitenA Literature Review of Retailing Sector and BusineSid MichaelNoch keine Bewertungen

- 25 Middlegame Concepts Every Chess Player Must KnowDokument2 Seiten25 Middlegame Concepts Every Chess Player Must KnowKasparicoNoch keine Bewertungen

- Hockney-Falco Thesis: 1 Setup of The 2001 PublicationDokument6 SeitenHockney-Falco Thesis: 1 Setup of The 2001 PublicationKurayami ReijiNoch keine Bewertungen

- Arithmetic QuestionsDokument2 SeitenArithmetic QuestionsAmir KhanNoch keine Bewertungen

- Day6 7Dokument11 SeitenDay6 7Abu Al-FarouqNoch keine Bewertungen

- Federalist Papers 10 51 ExcerptsDokument2 SeitenFederalist Papers 10 51 Excerptsapi-292351355Noch keine Bewertungen

- Modular Q1 WK3-4Dokument3 SeitenModular Q1 WK3-4JENIFFER DE LEONNoch keine Bewertungen

- Noise and DB Calculations: Smart EDGE ECE Review SpecialistDokument2 SeitenNoise and DB Calculations: Smart EDGE ECE Review SpecialistLM BecinaNoch keine Bewertungen

- Sample Learning Module As PatternDokument23 SeitenSample Learning Module As PatternWilliam BulliganNoch keine Bewertungen

- Yetta Company ProfileDokument6 SeitenYetta Company ProfileAfizi GhazaliNoch keine Bewertungen

- Based On PSA 700 Revised - The Independent Auditor's Report On A Complete Set of General Purpose Financial StatementsDokument12 SeitenBased On PSA 700 Revised - The Independent Auditor's Report On A Complete Set of General Purpose Financial Statementsbobo kaNoch keine Bewertungen

- Johnson & Johnson Equity Research ReportDokument13 SeitenJohnson & Johnson Equity Research ReportPraveen R V100% (3)

- Central University of Karnataka: Entrance Examinations Results 2016Dokument4 SeitenCentral University of Karnataka: Entrance Examinations Results 2016Saurabh ShubhamNoch keine Bewertungen

- Application of The Strain Energy To Estimate The Rock Load in Non-Squeezing Ground ConditionDokument17 SeitenApplication of The Strain Energy To Estimate The Rock Load in Non-Squeezing Ground ConditionAmit Kumar GautamNoch keine Bewertungen

- SDSSSSDDokument1 SeiteSDSSSSDmirfanjpcgmailcomNoch keine Bewertungen

- Importance of Skill Based Education-2994Dokument5 SeitenImportance of Skill Based Education-2994João Neto0% (1)

- Engleza Referat-Pantilimonescu IonutDokument13 SeitenEngleza Referat-Pantilimonescu IonutAilenei RazvanNoch keine Bewertungen

- DIR-819 A1 Manual v1.02WW PDFDokument172 SeitenDIR-819 A1 Manual v1.02WW PDFSerginho Jaafa ReggaeNoch keine Bewertungen

- CHARACTER FORMATION 1 PrelimDokument15 SeitenCHARACTER FORMATION 1 PrelimAiza Minalabag100% (1)

- Borges, The SouthDokument4 SeitenBorges, The Southdanielg233100% (1)

- Catheter Related InfectionsDokument581 SeitenCatheter Related InfectionshardboneNoch keine Bewertungen

- The Palestinian Centipede Illustrated ExcerptsDokument58 SeitenThe Palestinian Centipede Illustrated ExcerptsWael HaidarNoch keine Bewertungen

- Introduction CompilerDokument47 SeitenIntroduction CompilerHarshit SinghNoch keine Bewertungen

- Tuma Research ManualDokument57 SeitenTuma Research ManualKashinde Learner Centered Mandari100% (1)

- Saiva Dharma ShastrasDokument379 SeitenSaiva Dharma ShastrasfunnybizNoch keine Bewertungen