Das könnte Ihnen auch gefallen

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- 0202 - RGTECH - QR - 2020-12-31 - Radiant Globaltech Berhad - Quarterly Results - 31.12.2020 - 670632592Dokument20 Seiten0202 - RGTECH - QR - 2020-12-31 - Radiant Globaltech Berhad - Quarterly Results - 31.12.2020 - 670632592Iqbal YusufNoch keine Bewertungen

- Choo Bee Metal Industries Berhad (10587-A)Dokument18 SeitenChoo Bee Metal Industries Berhad (10587-A)Iqbal YusufNoch keine Bewertungen

- SiTime Third Quarter 2020 Financial Results-Transcript (Web)Dokument12 SeitenSiTime Third Quarter 2020 Financial Results-Transcript (Web)Iqbal YusufNoch keine Bewertungen

- Unaudited Condensed Consolidated Financial Statement For The Financial Year 2021 Fourth Quarter Ended 31 March 2021Dokument21 SeitenUnaudited Condensed Consolidated Financial Statement For The Financial Year 2021 Fourth Quarter Ended 31 March 2021Iqbal YusufNoch keine Bewertungen

- Supermax Corp (SUCB MK) : Regional Morning NotesDokument5 SeitenSupermax Corp (SUCB MK) : Regional Morning NotesIqbal YusufNoch keine Bewertungen

- First Supplementary Information Memorandum Dated 8 April 2021 in Respect of Amchina A-SharesDokument75 SeitenFirst Supplementary Information Memorandum Dated 8 April 2021 in Respect of Amchina A-SharesIqbal YusufNoch keine Bewertungen

- JHM Consolidation: MalaysiaDokument6 SeitenJHM Consolidation: MalaysiaIqbal YusufNoch keine Bewertungen

- Configuration: Getting Started GuDokument24 SeitenConfiguration: Getting Started GuIqbal YusufNoch keine Bewertungen

- MISC Berhad Outperform : Weaker Core Earnings in 1QFY21Dokument5 SeitenMISC Berhad Outperform : Weaker Core Earnings in 1QFY21Iqbal YusufNoch keine Bewertungen

- Public Investment Bank: Publicinvest Research DailyDokument9 SeitenPublic Investment Bank: Publicinvest Research DailyIqbal YusufNoch keine Bewertungen

- Johore Tin (Johotin-Ku) : Average ScoreDokument11 SeitenJohore Tin (Johotin-Ku) : Average ScoreIqbal YusufNoch keine Bewertungen

- FCFE CalculationDokument23 SeitenFCFE CalculationIqbal YusufNoch keine Bewertungen

- Country GDP (In Billions) Moody's Rating Adj. Default Spread Malaysia 314.5 A3 1.35% United Kingdom 2622.43 Aa2 0.56% United States 19390.6 Aaa 0.00%Dokument2 SeitenCountry GDP (In Billions) Moody's Rating Adj. Default Spread Malaysia 314.5 A3 1.35% United Kingdom 2622.43 Aa2 0.56% United States 19390.6 Aaa 0.00%Iqbal YusufNoch keine Bewertungen

- Under Armour Valuation and Forecasts Spreadsheet Completed On 7/1/2019Dokument14 SeitenUnder Armour Valuation and Forecasts Spreadsheet Completed On 7/1/2019Iqbal YusufNoch keine Bewertungen

- Debate: Abortion: Should Abortions of Any Kind Be Permitted? Background and ContextDokument39 SeitenDebate: Abortion: Should Abortions of Any Kind Be Permitted? Background and ContextIqbal YusufNoch keine Bewertungen

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Investment AppraisalDokument18 SeitenInvestment AppraisalKwasi MmehNoch keine Bewertungen

- Presentation-Advanced Organizer Quick PlanDokument2 SeitenPresentation-Advanced Organizer Quick Planapi-273088531Noch keine Bewertungen

- CitiGroup 2002Dokument34 SeitenCitiGroup 2002Coco CiaoNoch keine Bewertungen

- CIVABTech66829BrEstrAP - Valuation NumericalsDokument3 SeitenCIVABTech66829BrEstrAP - Valuation NumericalsAditiNoch keine Bewertungen

- Pertemuan 6 - Disposisi Properti, Pabrik Dan PeralatanDokument20 SeitenPertemuan 6 - Disposisi Properti, Pabrik Dan PeralatanTawang Deni WijayaNoch keine Bewertungen

- Introduction To Financial Accounting: Suggested Answers Foundation Examinations - Spring 2011Dokument5 SeitenIntroduction To Financial Accounting: Suggested Answers Foundation Examinations - Spring 2011adnanNoch keine Bewertungen

- Accountancy 12th SPSDokument4 SeitenAccountancy 12th SPSMahesh TandonNoch keine Bewertungen

- Accounting 9 Final Term 1Dokument9 SeitenAccounting 9 Final Term 1Mike ChindaNoch keine Bewertungen

- Chapter 2-GST Part B - Value of SupplyDokument7 SeitenChapter 2-GST Part B - Value of SupplyPooja D AcharyaNoch keine Bewertungen

- E StatementDokument3 SeitenE StatementVarun Kumar BawaNoch keine Bewertungen

- 04 2013-2014 Financial AgreementDokument2 Seiten04 2013-2014 Financial Agreementapi-234678525Noch keine Bewertungen

- Collection of ChequesDokument7 SeitenCollection of Cheques28-RPavan raj. BNoch keine Bewertungen

- Fintech Insights Q2 2022 Quarterly: FT Partners ResearchDokument110 SeitenFintech Insights Q2 2022 Quarterly: FT Partners ResearchngothientaiNoch keine Bewertungen

- Chapter 8: Cash and Bank Management Daily Procedures: ObjectivesDokument26 SeitenChapter 8: Cash and Bank Management Daily Procedures: ObjectivesArturo GonzalezNoch keine Bewertungen

- 2 - Afraseab Aor Umro Ky KarnamayDokument390 Seiten2 - Afraseab Aor Umro Ky KarnamaySaim Younis100% (1)

- Eco401 Final Term NotesDokument5 SeitenEco401 Final Term NotesLALANoch keine Bewertungen

- GU215RG Post To Home Address: SurreyDokument1 SeiteGU215RG Post To Home Address: SurreyhelikacarvalhoNoch keine Bewertungen

- Sample MCQsDokument6 SeitenSample MCQsRubal GargNoch keine Bewertungen

- Caiib Paper 4 Banking Regulations and Business Laws Capsule AmbitiousDokument223 SeitenCaiib Paper 4 Banking Regulations and Business Laws Capsule AmbitiouselliaCruzNoch keine Bewertungen

- FX Get DoneDokument2 SeitenFX Get DoneDev GogoiNoch keine Bewertungen

- The Fall of The House of Credit PDFDokument382 SeitenThe Fall of The House of Credit PDFRichard JohnNoch keine Bewertungen

- Tutorial Letter 108/0/2023: TAX4861 NTA4861Dokument75 SeitenTutorial Letter 108/0/2023: TAX4861 NTA4861ByouNoch keine Bewertungen

- This Is A System-Generated Statement. Hence, It Does Not Require Any SignatureDokument6 SeitenThis Is A System-Generated Statement. Hence, It Does Not Require Any SignatureSachinNoch keine Bewertungen

- Nps One PagerDokument2 SeitenNps One PagerldorayaNoch keine Bewertungen

- Chapter 3 Economic Study MethodsDokument62 SeitenChapter 3 Economic Study MethodsJohn Fretz AbelardeNoch keine Bewertungen

- UntitledDokument8 SeitenUntitledRae SlaughterNoch keine Bewertungen

- The Performance of Diversified Emerging Market Equity FundsDokument16 SeitenThe Performance of Diversified Emerging Market Equity FundsMuhammad RoqibunNoch keine Bewertungen

- CR Ma 21Dokument22 SeitenCR Ma 21Sharif MahmudNoch keine Bewertungen

- 23.+Other+Percentage+Tax-REVISED+2023-classroom+discussion - Students 2Dokument55 Seiten23.+Other+Percentage+Tax-REVISED+2023-classroom+discussion - Students 2Aristeia NotesNoch keine Bewertungen

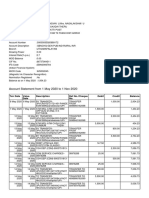

- Account Statement From 1 May 2020 To 1 Nov 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDokument9 SeitenAccount Statement From 1 May 2020 To 1 Nov 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceChellapandiNoch keine Bewertungen