Das könnte Ihnen auch gefallen

- Cost AccountingDokument57 SeitenCost AccountingM.K. TongNoch keine Bewertungen

- Process Cost: Excel Professional ServicesDokument45 SeitenProcess Cost: Excel Professional ServicesDiane PascualNoch keine Bewertungen

- Chapter 7 Costing Systems SummaryDokument24 SeitenChapter 7 Costing Systems SummaryCharlene BalderaNoch keine Bewertungen

- Acctg 7 Assignment No. 3Dokument5 SeitenAcctg 7 Assignment No. 3John Kenneth Escober BentirNoch keine Bewertungen

- Cost Accounting and Control: Process CostingDokument14 SeitenCost Accounting and Control: Process CostingAloha Bu-ucan100% (2)

- 2021 Answer Chapter 5Dokument15 Seiten2021 Answer Chapter 5prettyjessyNoch keine Bewertungen

- Garcia, Phoebe Stephane C. Cost Accounting BS Accountancy 1-A CHAPTER 10: Process Costing True or FalseDokument26 SeitenGarcia, Phoebe Stephane C. Cost Accounting BS Accountancy 1-A CHAPTER 10: Process Costing True or FalsePeabeeNoch keine Bewertungen

- Cost Accounting Chapter 7 PDFDokument8 SeitenCost Accounting Chapter 7 PDFCaren GerebitNoch keine Bewertungen

- 2809 Process Costing PDFDokument80 Seiten2809 Process Costing PDFPhoeza Espinosa VillanuevaNoch keine Bewertungen

- 2021 Answer Chapter 5 PDFDokument19 Seiten2021 Answer Chapter 5 PDFRianne NavidadNoch keine Bewertungen

- Cost Accounting (1105) : Activity 1 Problem 1 Problem 2Dokument10 SeitenCost Accounting (1105) : Activity 1 Problem 1 Problem 2Krisha Joselle MilloNoch keine Bewertungen

- Cost Accounting Chapter 8 CompressDokument7 SeitenCost Accounting Chapter 8 Compressandreyaanne06Noch keine Bewertungen

- Ansay, Allyson Charissa T. - BSA 2 - Process Costing SystemDokument4 SeitenAnsay, Allyson Charissa T. - BSA 2 - Process Costing Systemカイ みゆきNoch keine Bewertungen

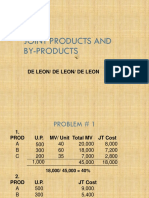

- Joint Products-By ProductsDokument19 SeitenJoint Products-By ProductsKenneth Christian WilburNoch keine Bewertungen

- Cost Accounting - Chapter 10Dokument14 SeitenCost Accounting - Chapter 10xxxxxxxxx67% (6)

- SummaryDokument30 SeitenSummaryAkira Marantal Valdez0% (1)

- Answers To Cost Accounting Chapter 10Dokument15 SeitenAnswers To Cost Accounting Chapter 10Raffy Roncales100% (2)

- Chapter 10-SolManDokument15 SeitenChapter 10-SolManJulyanneErikaMigriñoMeñuzaNoch keine Bewertungen

- F2 Mock1 AnsDokument8 SeitenF2 Mock1 AnsHajra ZahraNoch keine Bewertungen

- Juarez, Jenny Brozas - Activity 2 MidtermDokument4 SeitenJuarez, Jenny Brozas - Activity 2 MidtermJenny Brozas JuarezNoch keine Bewertungen

- DocDokument3 SeitenDocWansy Ferrer BallesterosNoch keine Bewertungen

- 2713-Joint-And-By-Product-Costing 2Dokument19 Seiten2713-Joint-And-By-Product-Costing 2Guen SilverioNoch keine Bewertungen

- Process Costing Quiz Spoiled UnitsDokument3 SeitenProcess Costing Quiz Spoiled UnitsRafael Capunpon VallejosNoch keine Bewertungen

- Costco1 - Assign 5Dokument7 SeitenCostco1 - Assign 5Deryl GalveNoch keine Bewertungen

- Frias - Chapter 2Dokument5 SeitenFrias - Chapter 2Lars FriasNoch keine Bewertungen

- FA Feb 2021Dokument3 SeitenFA Feb 2021paan tiktokNoch keine Bewertungen

- Answers To Multiple Choices - TheoreticalDokument29 SeitenAnswers To Multiple Choices - TheoreticalMaica GarciaNoch keine Bewertungen

- 2021 Answer Chapter 3 PDFDokument11 Seiten2021 Answer Chapter 3 PDFRianne NavidadNoch keine Bewertungen

- Chapters 1 3Dokument112 SeitenChapters 1 3julygg0710Noch keine Bewertungen

- Cost Accounting 7 & 8Dokument26 SeitenCost Accounting 7 & 8Kyrara79% (19)

- Answer Key (SW1 To SW3)Dokument6 SeitenAnswer Key (SW1 To SW3)MA. CRISSANDRA BUSTAMANTENoch keine Bewertungen

- Accounting for Factory Overhead ProblemsDokument29 SeitenAccounting for Factory Overhead ProblemsKyrara70% (20)

- 2813 Joint and By-Product CostingDokument23 Seiten2813 Joint and By-Product Costingmarianocastro1593Noch keine Bewertungen

- Business Economics TestDokument4 SeitenBusiness Economics TestViệt HùngNoch keine Bewertungen

- Problems Process Costing SOLUTIONDokument12 SeitenProblems Process Costing SOLUTIONPatDabz67% (3)

- Answer Key Midterm Exam Cost Acounting With Solutions PART IIDokument7 SeitenAnswer Key Midterm Exam Cost Acounting With Solutions PART IINoel Carpio100% (1)

- Managerial Accounting: SectionDokument17 SeitenManagerial Accounting: SectionNostecNoch keine Bewertungen

- Mexico Company manufacturing weighted average FIFO process costingDokument6 SeitenMexico Company manufacturing weighted average FIFO process costingC XNoch keine Bewertungen

- Practice Questions 1Dokument5 SeitenPractice Questions 1Div_nNoch keine Bewertungen

- JOINT PRODUCTION COST ALLOCATIONDokument17 SeitenJOINT PRODUCTION COST ALLOCATIONMay Grethel Joy PeranteNoch keine Bewertungen

- Lecture Note - Overhead Variances 2078-08-19Dokument6 SeitenLecture Note - Overhead Variances 2078-08-19Sarose ThapaNoch keine Bewertungen

- Problem 4 Process CostingDokument3 SeitenProblem 4 Process CostingKloie SanoriaNoch keine Bewertungen

- Quiz 6 Process Costing SolutionsDokument7 SeitenQuiz 6 Process Costing SolutionsralphalonzoNoch keine Bewertungen

- Process Costing ProblemsDokument9 SeitenProcess Costing ProblemsAries Bautista67% (3)

- Chapter 11 - Average and FIFO Costing ProblemsDokument11 SeitenChapter 11 - Average and FIFO Costing ProblemspoNoch keine Bewertungen

- Illustration Ex. 1Dokument7 SeitenIllustration Ex. 1Nigussie BerhanuNoch keine Bewertungen

- Normal and Abnormal SpoilageDokument6 SeitenNormal and Abnormal SpoilageJanina CabatinganNoch keine Bewertungen

- AFAR First Preboard 93 - SolutionsDokument12 SeitenAFAR First Preboard 93 - SolutionsEpfie SanchesNoch keine Bewertungen

- Electronics 3 Checkbook: The Checkbooks SeriesVon EverandElectronics 3 Checkbook: The Checkbooks SeriesBewertung: 5 von 5 Sternen5/5 (1)

- Electrical and Electronic Principles 3 Checkbook: The Checkbook SeriesVon EverandElectrical and Electronic Principles 3 Checkbook: The Checkbook SeriesNoch keine Bewertungen

- Photonics, Volume 4: Biomedical Photonics, Spectroscopy, and MicroscopyVon EverandPhotonics, Volume 4: Biomedical Photonics, Spectroscopy, and MicroscopyNoch keine Bewertungen

- Solution Manual for an Introduction to Equilibrium ThermodynamicsVon EverandSolution Manual for an Introduction to Equilibrium ThermodynamicsNoch keine Bewertungen

- Combustion of Pulverised Coal in a Mixture of Oxygen and Recycled Flue GasVon EverandCombustion of Pulverised Coal in a Mixture of Oxygen and Recycled Flue GasNoch keine Bewertungen

- Physics and Technology of Crystalline Oxide Semiconductor CAAC-IGZO: Application to DisplaysVon EverandPhysics and Technology of Crystalline Oxide Semiconductor CAAC-IGZO: Application to DisplaysNoch keine Bewertungen

- Revised Corporation CodeDokument15 SeitenRevised Corporation CodeM.K. TongNoch keine Bewertungen

- Material 6 Inventories Other Investments.. Lucky Version Part 1Dokument5 SeitenMaterial 6 Inventories Other Investments.. Lucky Version Part 1M.K. TongNoch keine Bewertungen

- Auditing Theory Test BankDokument7 SeitenAuditing Theory Test BankjaysonNoch keine Bewertungen

- Auditing Theory Test BankDokument7 SeitenAuditing Theory Test BankjaysonNoch keine Bewertungen

- Finance: From Wikipedia, The Free Encyclopedia For Other Uses, SeeDokument3 SeitenFinance: From Wikipedia, The Free Encyclopedia For Other Uses, SeeM.K. TongNoch keine Bewertungen

- PDFDokument10 SeitenPDFM.K. TongNoch keine Bewertungen

- Revised Corporation Code: Key Changes to Philippine Company LawDokument10 SeitenRevised Corporation Code: Key Changes to Philippine Company LawM.K. TongNoch keine Bewertungen

- Auditing Theory Test BankDokument7 SeitenAuditing Theory Test BankjaysonNoch keine Bewertungen

- Auditing Theory Test BankDokument7 SeitenAuditing Theory Test BankM.K. TongNoch keine Bewertungen

- Chapter 6 Mas Short Term BudgetingDokument18 SeitenChapter 6 Mas Short Term BudgetingLauren Obrien67% (3)

- Auditing Theory Test BankDokument7 SeitenAuditing Theory Test BankjaysonNoch keine Bewertungen

- Balanced Scorecard of Ahon Ministries IN Brgy. Ambago, Agusan Del NorteDokument4 SeitenBalanced Scorecard of Ahon Ministries IN Brgy. Ambago, Agusan Del NorteM.K. TongNoch keine Bewertungen

- Chapter 2Dokument15 SeitenChapter 2M.K. TongNoch keine Bewertungen

- Organizational Adaptation TheoryDokument1 SeiteOrganizational Adaptation TheoryM.K. Tong100% (1)

- Measure System Performance with Queuing ModelsDokument36 SeitenMeasure System Performance with Queuing ModelsM.K. TongNoch keine Bewertungen

- Maria Krista Fe M. Tong SGV & Co. Senior Auditor ResumeDokument1 SeiteMaria Krista Fe M. Tong SGV & Co. Senior Auditor ResumeM.K. TongNoch keine Bewertungen

- MVP: PLDT Expects Lower Income For 'Horrible' 2016Dokument3 SeitenMVP: PLDT Expects Lower Income For 'Horrible' 2016M.K. TongNoch keine Bewertungen

- Apple Business Strategy 2012Dokument5 SeitenApple Business Strategy 2012M.K. TongNoch keine Bewertungen

- The Little Black Book of Billionaire SecretsDokument4 SeitenThe Little Black Book of Billionaire SecretsM.K. TongNoch keine Bewertungen

- Failure of Governance - From Kashmir To Karnataka: 19 September 2016, New Delhi, Amulya GanguliDokument2 SeitenFailure of Governance - From Kashmir To Karnataka: 19 September 2016, New Delhi, Amulya GanguliM.K. TongNoch keine Bewertungen

- Copernicus Model Gained Acceptance Over Ptolemaic Model Due to Simplicity (39Dokument3 SeitenCopernicus Model Gained Acceptance Over Ptolemaic Model Due to Simplicity (39M.K. TongNoch keine Bewertungen

- Chapter 4 - Deductions From Gross Estate2013Dokument9 SeitenChapter 4 - Deductions From Gross Estate2013incubus_yeah90% (10)

- Accounting or Accountancy Is The MeasurementDokument3 SeitenAccounting or Accountancy Is The MeasurementM.K. TongNoch keine Bewertungen

- Jollibee Foods Corporation: An Analysis of the Largest Fast Food Chain in the PhilippinesDokument15 SeitenJollibee Foods Corporation: An Analysis of the Largest Fast Food Chain in the PhilippinesM.K. Tong78% (9)

- Good Governance and Its ComponentsDokument1 SeiteGood Governance and Its ComponentsM.K. TongNoch keine Bewertungen

- What Are The Main Characteristics of Good Governance?Dokument2 SeitenWhat Are The Main Characteristics of Good Governance?Jessica HunterNoch keine Bewertungen

- Good Governance and Its ComponentsDokument1 SeiteGood Governance and Its ComponentsM.K. TongNoch keine Bewertungen

- IP Dect AP 8340 R150 DatasheetDokument3 SeitenIP Dect AP 8340 R150 DatasheetAsnake TegenawNoch keine Bewertungen

- AcctIS10E - Ch04 - CE - PART 1 - FOR CLASSDokument32 SeitenAcctIS10E - Ch04 - CE - PART 1 - FOR CLASSLance CaveNoch keine Bewertungen

- Flygt 3202 PDFDokument137 SeitenFlygt 3202 PDFEduardo50% (2)

- Factors Supporting ICT Use in ClassroomsDokument24 SeitenFactors Supporting ICT Use in ClassroomsSeshaadhrisTailoringNoch keine Bewertungen

- Competition Patriotism and Collaboratio PDFDokument22 SeitenCompetition Patriotism and Collaboratio PDFAngga PrianggaraNoch keine Bewertungen

- Prova ScrumDokument11 SeitenProva ScrumJoanna de Cassia ValadaresNoch keine Bewertungen

- Data Sheet 3VA2225-5HL32-0AA0: ModelDokument7 SeitenData Sheet 3VA2225-5HL32-0AA0: ModelJENNYNoch keine Bewertungen

- Advance NewsletterDokument14 SeitenAdvance Newsletterapi-206881299Noch keine Bewertungen

- Sp8300 Part CatalogoDokument111 SeitenSp8300 Part CatalogoLeonard FreitasNoch keine Bewertungen

- Neeraj Kumar: Nokia Siemens Networks (Global SDC Chennai)Dokument4 SeitenNeeraj Kumar: Nokia Siemens Networks (Global SDC Chennai)Kuldeep SharmaNoch keine Bewertungen

- IELTS Writing Task 1 Combined Graphs Line Graph and Table 1Dokument6 SeitenIELTS Writing Task 1 Combined Graphs Line Graph and Table 1Sugeng RiadiNoch keine Bewertungen

- Tucker Northlake SLUPsDokument182 SeitenTucker Northlake SLUPsZachary HansenNoch keine Bewertungen

- Agency Certificate of Compliance: IGHRS Update As of June 30, 2022Dokument2 SeitenAgency Certificate of Compliance: IGHRS Update As of June 30, 2022Dacanay RexNoch keine Bewertungen

- A New High Drive Class-AB FVF Based Second Generation Voltage ConveyorDokument5 SeitenA New High Drive Class-AB FVF Based Second Generation Voltage ConveyorShwetaGautamNoch keine Bewertungen

- Using Acupressure On Yourself For Pain Relief in LabourDokument3 SeitenUsing Acupressure On Yourself For Pain Relief in LabourNiki MavrakiNoch keine Bewertungen

- (OBIEE11g) Integrating Oracle Business Intelligence Applications With Oracle E-Business Suite - Oracle Bi SolutionsDokument11 Seiten(OBIEE11g) Integrating Oracle Business Intelligence Applications With Oracle E-Business Suite - Oracle Bi SolutionsVenkatesh Ramiya Krishna MoorthyNoch keine Bewertungen

- Chapter 3 Views in ASP - NET CoreDokument23 SeitenChapter 3 Views in ASP - NET Coremohammadabusaleh628Noch keine Bewertungen

- 26 27 16 Electrical Cabinets and EnclosuresDokument3 Seiten26 27 16 Electrical Cabinets and EnclosureskaichosanNoch keine Bewertungen

- Haulmax HaulTruck 11.21.13 FINALDokument2 SeitenHaulmax HaulTruck 11.21.13 FINALjogremaurNoch keine Bewertungen

- Ceramic Disc Brakes: Haneesh James S ME8 Roll No: 20Dokument23 SeitenCeramic Disc Brakes: Haneesh James S ME8 Roll No: 20Anil GöwđaNoch keine Bewertungen

- DigitalForensics 05 NOV2010Dokument84 SeitenDigitalForensics 05 NOV2010hhhzineNoch keine Bewertungen

- Chapter Three Business PlanDokument14 SeitenChapter Three Business PlanBethelhem YetwaleNoch keine Bewertungen

- Basics of Directional-Control ValvesDokument11 SeitenBasics of Directional-Control ValvesJosh LeBlancNoch keine Bewertungen

- BS Iec 61643-32-2017 - (2020-05-04 - 04-32-37 Am)Dokument46 SeitenBS Iec 61643-32-2017 - (2020-05-04 - 04-32-37 Am)Shaiful ShazwanNoch keine Bewertungen

- Final IEQC MICRODokument10 SeitenFinal IEQC MICROWMG NINJANoch keine Bewertungen

- Student Name Student Number Assessment Title Module Title Module Code Module Coordinator Tutor (If Applicable)Dokument32 SeitenStudent Name Student Number Assessment Title Module Title Module Code Module Coordinator Tutor (If Applicable)Exelligent Academic SolutionsNoch keine Bewertungen

- Emergency Incidents AssignmentDokument4 SeitenEmergency Incidents Assignmentnickoh28Noch keine Bewertungen

- (Lecture 10 & 11) - Gearing & Capital StructureDokument18 Seiten(Lecture 10 & 11) - Gearing & Capital StructureAjay Kumar TakiarNoch keine Bewertungen

- En 12485Dokument184 SeitenEn 12485vishalmisalNoch keine Bewertungen

- Public Arrest Report For 22jan2016Dokument4 SeitenPublic Arrest Report For 22jan2016api-214091549Noch keine Bewertungen