Das könnte Ihnen auch gefallen

- A Summer Internship Report On Study of CDokument3 SeitenA Summer Internship Report On Study of CVarshik FlashNoch keine Bewertungen

- Ergonomics For The BlindDokument8 SeitenErgonomics For The BlindShruthi PandulaNoch keine Bewertungen

- CogAT 7 PlanningImplemGd v4.1 PDFDokument112 SeitenCogAT 7 PlanningImplemGd v4.1 PDFBahrouniNoch keine Bewertungen

- Average Waves in Unprotected Waters by Anne Tyler - Summary PDFDokument1 SeiteAverage Waves in Unprotected Waters by Anne Tyler - Summary PDFRK PADHI0% (1)

- Dividend Practices of Islamic Banks in Bangladesh (Shariah Compliances) by Hasan Asif SouravDokument21 SeitenDividend Practices of Islamic Banks in Bangladesh (Shariah Compliances) by Hasan Asif SouravHasan Asif SouravNoch keine Bewertungen

- 12 Chapter4Dokument25 Seiten12 Chapter4Raj barnwalNoch keine Bewertungen

- Chapter - Iii Customer Satisfaction in The Banking Industry - An OverviewDokument49 SeitenChapter - Iii Customer Satisfaction in The Banking Industry - An Overviewvahid desaiNoch keine Bewertungen

- POs Pre Joining Study Material PDFDokument152 SeitenPOs Pre Joining Study Material PDFKushagra Pratap SinghNoch keine Bewertungen

- Comparative Study of BanksDokument8 SeitenComparative Study of BanksSaurabh RajNoch keine Bewertungen

- Dividend Yielding StocksDokument2 SeitenDividend Yielding StocksleninbapujiNoch keine Bewertungen

- Non-Performing AssetsDokument20 SeitenNon-Performing AssetsSagar PawarNoch keine Bewertungen

- What Ails Indian Banking SectorDokument9 SeitenWhat Ails Indian Banking SectorparthiNoch keine Bewertungen

- IFB Ethiopia Report PDFDokument3 SeitenIFB Ethiopia Report PDFfeyselNoch keine Bewertungen

- A Study On Financial Analysis of State Bank of India and Its AssociatesDokument12 SeitenA Study On Financial Analysis of State Bank of India and Its Associatesmusik loveNoch keine Bewertungen

- Performance Analysis of Public Sector Banks in India: March 2015Dokument12 SeitenPerformance Analysis of Public Sector Banks in India: March 2015Abhijeet JaiswalNoch keine Bewertungen

- Analysis of Banking Industry: - Presented By-Santanu Banik Gourab Biswas Asish Kr. RoyDokument18 SeitenAnalysis of Banking Industry: - Presented By-Santanu Banik Gourab Biswas Asish Kr. RoybgourabNoch keine Bewertungen

- Annex 258 AU1514Dokument4 SeitenAnnex 258 AU1514madhavjadhav2018Noch keine Bewertungen

- Findings Conclusion ArefeenDokument6 SeitenFindings Conclusion ArefeenTridib DebnathNoch keine Bewertungen

- Net NPA As Percentage of Net Advance Public & Private Sector BanksDokument1 SeiteNet NPA As Percentage of Net Advance Public & Private Sector BanksPankaj MaryeNoch keine Bewertungen

- Submitted By: Parth D. DalalDokument43 SeitenSubmitted By: Parth D. Dalalrahulshah86Noch keine Bewertungen

- Annexure - 2 (A) - IDokument12 SeitenAnnexure - 2 (A) - IUttamJainNoch keine Bewertungen

- DM22118 - Dinakaran SDokument11 SeitenDM22118 - Dinakaran SDinakaranNoch keine Bewertungen

- Market Share of Top 5 Banks in IndiaDokument6 SeitenMarket Share of Top 5 Banks in Indiamayank shridharNoch keine Bewertungen

- Sbi Annual Report 2012 13Dokument190 SeitenSbi Annual Report 2012 13udit_mca_blyNoch keine Bewertungen

- Maths ProjectDokument15 SeitenMaths Projecttmbcreditdummy50% (2)

- PAT As % TI Public & Private Sector BanksDokument1 SeitePAT As % TI Public & Private Sector BanksPankaj MaryeNoch keine Bewertungen

- Banking Theory and Practice: Digital Assignment 1Dokument5 SeitenBanking Theory and Practice: Digital Assignment 1muthu kumaranNoch keine Bewertungen

- Banking Weekly Newsletter April 13 2012Dokument7 SeitenBanking Weekly Newsletter April 13 2012abhishekrungta1984Noch keine Bewertungen

- Banking Sector of BangladeshDokument8 SeitenBanking Sector of BangladeshIftekhar Abid FahimNoch keine Bewertungen

- Topic 11 (Money, Banking)Dokument35 SeitenTopic 11 (Money, Banking)a191318Noch keine Bewertungen

- Consolidation in Indian Banking: Bachelor's Party!!!Dokument20 SeitenConsolidation in Indian Banking: Bachelor's Party!!!Kavita DaraNoch keine Bewertungen

- Ijmra 13137Dokument6 SeitenIjmra 13137sanjug2772Noch keine Bewertungen

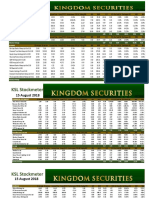

- KSL StockmeterDokument5 SeitenKSL StockmeterAn AntonyNoch keine Bewertungen

- Types of Mutual Fund 1Dokument14 SeitenTypes of Mutual Fund 1Sneha BhuwalkaNoch keine Bewertungen

- CASA Ratio Research StudyDokument17 SeitenCASA Ratio Research StudyMahesh Satapathy0% (1)

- Npa Analysis For 15 Years of Different Banking SectorsDokument6 SeitenNpa Analysis For 15 Years of Different Banking SectorsBhanu Pratap SolankiNoch keine Bewertungen

- Bank Analysis WorkingDokument21 SeitenBank Analysis WorkingNajmus SakibNoch keine Bewertungen

- Presented By: Hidayat Kusamanto 207.02.018Dokument22 SeitenPresented By: Hidayat Kusamanto 207.02.018Hidayat KusamantoNoch keine Bewertungen

- FM 2 ProjectDokument7 SeitenFM 2 ProjectNiket AmanNoch keine Bewertungen

- Merger of State Bank of India WITH StateDokument20 SeitenMerger of State Bank of India WITH StateShilpa WasnikNoch keine Bewertungen

- Data Presentation and AnalysisDokument13 SeitenData Presentation and AnalysisViru PatelNoch keine Bewertungen

- Assignment On FIN211Dokument18 SeitenAssignment On FIN211Muhtasin Monir GemNoch keine Bewertungen

- Banking: CHAPTER A: Brief About The Indian Banking SectorDokument63 SeitenBanking: CHAPTER A: Brief About The Indian Banking SectorDevang ParabNoch keine Bewertungen

- UntitledDokument4 SeitenUntitledSakshi KumariNoch keine Bewertungen

- Mba 3042F: Management of Banks Cia 1: Description: Financial Performance Analysis of A Central Bank and AXIS BankDokument15 SeitenMba 3042F: Management of Banks Cia 1: Description: Financial Performance Analysis of A Central Bank and AXIS BankNehal SharmaNoch keine Bewertungen

- Fixed Deposit Interest Rates - Best FD Rates of Top Banks in IndiaDokument15 SeitenFixed Deposit Interest Rates - Best FD Rates of Top Banks in IndiaebeanandeNoch keine Bewertungen

- Ratio Analysis of Co-Operative Bank of Surat: Manisha D. PatelDokument11 SeitenRatio Analysis of Co-Operative Bank of Surat: Manisha D. Patels.muthuNoch keine Bewertungen

- Presentation ON Corporate Story of Sbi: FROM:-GROUP 10. Varun Anand Vikas Shukla Vivek Singh Parul Shukla Pooja DeepDokument16 SeitenPresentation ON Corporate Story of Sbi: FROM:-GROUP 10. Varun Anand Vikas Shukla Vivek Singh Parul Shukla Pooja DeepVarun AnandNoch keine Bewertungen

- Quarterly Return of Selected Funds During The Past Five YearsDokument6 SeitenQuarterly Return of Selected Funds During The Past Five YearsNidhi RaiNoch keine Bewertungen

- Financial Analysis of The Surat Mercantile Co-Op. Bank LTD."Dokument19 SeitenFinancial Analysis of The Surat Mercantile Co-Op. Bank LTD."Ankur MeruliyaNoch keine Bewertungen

- A Comparative Study of Loan Performance SandraDokument23 SeitenA Comparative Study of Loan Performance SandraSandra DennyNoch keine Bewertungen

- SBI Becomes First Japan Group To List in HKDokument8 SeitenSBI Becomes First Japan Group To List in HKishan_mishra85Noch keine Bewertungen

- Xim University, Bhubaneswar: Financial Institutions and MarketsDokument13 SeitenXim University, Bhubaneswar: Financial Institutions and MarketsSattwik rathNoch keine Bewertungen

- Capital StructureDokument6 SeitenCapital StructuredsgoudNoch keine Bewertungen

- Earnings Projection of BanksDokument2 SeitenEarnings Projection of Banksmahfuz69Noch keine Bewertungen

- CamelDokument10 SeitenCamelSimki JainNoch keine Bewertungen

- Assignment of Fundamentals of Financial ManagementDokument10 SeitenAssignment of Fundamentals of Financial ManagementShashwat ShuklaNoch keine Bewertungen

- Bank FinstatementDokument19 SeitenBank FinstatementCool BuddyNoch keine Bewertungen

- Current Banking Scenario in IndiaDokument46 SeitenCurrent Banking Scenario in Indiamukeshsomani1Noch keine Bewertungen

- NIM Public & Private Sector BanksDokument1 SeiteNIM Public & Private Sector BanksPankaj MaryeNoch keine Bewertungen

- HDFC CASE STUDY Part 2Dokument53 SeitenHDFC CASE STUDY Part 2sourav khandelwalNoch keine Bewertungen

- Introduction Sutex BankDokument14 SeitenIntroduction Sutex BankRonakNoch keine Bewertungen

- Asia Small and Medium-Sized Enterprise Monitor 2021: Volume I—Country and Regional ReviewsVon EverandAsia Small and Medium-Sized Enterprise Monitor 2021: Volume I—Country and Regional ReviewsNoch keine Bewertungen

- Papadakos PHD 2013Dokument203 SeitenPapadakos PHD 2013Panagiotis PapadakosNoch keine Bewertungen

- Hydrogen Peroxide DripDokument13 SeitenHydrogen Peroxide DripAya100% (1)

- E 05-03-2022 Power Interruption Schedule FullDokument22 SeitenE 05-03-2022 Power Interruption Schedule FullAda Derana100% (2)

- Sentence Connectors: 1.contrast 1. A. Direct OppositionDokument8 SeitenSentence Connectors: 1.contrast 1. A. Direct OppositionCathy siganNoch keine Bewertungen

- Lesson Plan MP-2Dokument7 SeitenLesson Plan MP-2VeereshGodiNoch keine Bewertungen

- Anti-Epileptic Drugs: - Classification of SeizuresDokument31 SeitenAnti-Epileptic Drugs: - Classification of SeizuresgopscharanNoch keine Bewertungen

- Layos vs. VillanuevaDokument2 SeitenLayos vs. VillanuevaLaura MangantulaoNoch keine Bewertungen

- Contracts 2 Special ContractsDokument11 SeitenContracts 2 Special ContractsAbhikaamNoch keine Bewertungen

- Aff Col MA Part IIDokument90 SeitenAff Col MA Part IIAkanksha DubeyNoch keine Bewertungen

- PSYC1111 Ogden Psychology of Health and IllnessDokument108 SeitenPSYC1111 Ogden Psychology of Health and IllnessAleNoch keine Bewertungen

- Michel Agier - Between War and CityDokument25 SeitenMichel Agier - Between War and CityGonjack Imam100% (1)

- 2nd Form Sequence of WorkDokument7 Seiten2nd Form Sequence of WorkEustace DavorenNoch keine Bewertungen

- Echnical Ocational Ivelihood: Edia and Nformation IteracyDokument12 SeitenEchnical Ocational Ivelihood: Edia and Nformation IteracyKrystelle Marie AnteroNoch keine Bewertungen

- Binary SearchDokument13 SeitenBinary SearchASasSNoch keine Bewertungen

- The Final Bible of Christian SatanismDokument309 SeitenThe Final Bible of Christian SatanismLucifer White100% (1)

- TOPIC I: Moral and Non-Moral ProblemsDokument6 SeitenTOPIC I: Moral and Non-Moral ProblemsHaydee Christine SisonNoch keine Bewertungen

- Respiratory Examination OSCE GuideDokument33 SeitenRespiratory Examination OSCE GuideBasmah 7Noch keine Bewertungen

- Lets Install Cisco ISEDokument8 SeitenLets Install Cisco ISESimon GarciaNoch keine Bewertungen

- CV Michael Naughton 2019Dokument2 SeitenCV Michael Naughton 2019api-380850234Noch keine Bewertungen

- Simple Past TenselDokument3 SeitenSimple Past TenselPutra ViskellaNoch keine Bewertungen

- Arctic Beacon Forbidden Library - Winkler-The - Thousand - Year - Conspiracy PDFDokument196 SeitenArctic Beacon Forbidden Library - Winkler-The - Thousand - Year - Conspiracy PDFJames JohnsonNoch keine Bewertungen

- Bagon-Taas Adventist Youth ConstitutionDokument11 SeitenBagon-Taas Adventist Youth ConstitutionJoseph Joshua A. PaLaparNoch keine Bewertungen

- Cruz-Arevalo v. Layosa DigestDokument2 SeitenCruz-Arevalo v. Layosa DigestPatricia Ann RueloNoch keine Bewertungen

- 2,3,5 Aqidah Dan QHDokument5 Seiten2,3,5 Aqidah Dan QHBang PaingNoch keine Bewertungen

- Personal Philosophy of Education-Exemplar 1Dokument2 SeitenPersonal Philosophy of Education-Exemplar 1api-247024656Noch keine Bewertungen

- India: SupplyDokument6 SeitenIndia: SupplyHarish NathanNoch keine Bewertungen

- Ivler vs. Republic, G.R. No. 172716Dokument23 SeitenIvler vs. Republic, G.R. No. 172716Joey SalomonNoch keine Bewertungen