Das könnte Ihnen auch gefallen

- Template Emudhra Authorization Letter PDFDokument1 SeiteTemplate Emudhra Authorization Letter PDFnishi vatsNoch keine Bewertungen

- Sample ResumeDokument3 SeitenSample Resumeapi-380209683% (6)

- 2015 UBS IB Challenge Corporate Finance OverviewDokument23 Seiten2015 UBS IB Challenge Corporate Finance Overviewkevin100% (1)

- Budget Worksheet: Monthly Net IncomeDokument1 SeiteBudget Worksheet: Monthly Net IncomeErnestKalamboNoch keine Bewertungen

- Youthonomics Global Index 101315Dokument57 SeitenYouthonomics Global Index 101315Leonardo GuittonNoch keine Bewertungen

- Pharmacovigilance DefinationsDokument32 SeitenPharmacovigilance DefinationsKadir AmirNoch keine Bewertungen

- 0 Asmipl-Msod-11 04Dokument13 Seiten0 Asmipl-Msod-11 04vbmaccountsNoch keine Bewertungen

- Computer BasicDokument12 SeitenComputer BasicanamikapariharNoch keine Bewertungen

- Daily Duas in The Month ofDokument258 SeitenDaily Duas in The Month ofTransforNoch keine Bewertungen

- Resistant Hypertension. AHADokument38 SeitenResistant Hypertension. AHAEderEmmanuelMartinezRuiz100% (1)

- 14) PPT ROMAN Salah Training - StudentsDokument342 Seiten14) PPT ROMAN Salah Training - Studentsamer sohailNoch keine Bewertungen

- Important Plants in Kerala Ayurveda Industry: Tree CropsDokument2 SeitenImportant Plants in Kerala Ayurveda Industry: Tree Cropsajeez86Noch keine Bewertungen

- TELEKOMUNIKASI DAN KOMPUTER RANGKAIANDokument19 SeitenTELEKOMUNIKASI DAN KOMPUTER RANGKAIANAmer IkhwanNoch keine Bewertungen

- General Diet PlanDokument1 SeiteGeneral Diet PlanAzmat HusainNoch keine Bewertungen

- Key Board Short CutDokument6 SeitenKey Board Short CutChaitanya KumarNoch keine Bewertungen

- Widal Agglutination Test PDFDokument5 SeitenWidal Agglutination Test PDFशशांक तिवारीNoch keine Bewertungen

- Vitamin Deficiency and Food Recommendation System Using Machine LearningDokument10 SeitenVitamin Deficiency and Food Recommendation System Using Machine LearningIJRASETPublicationsNoch keine Bewertungen

- Prospectus: Programmes OfferedDokument70 SeitenProspectus: Programmes OfferedPrajwal MkNoch keine Bewertungen

- Common Diseases, Vol II - 1223Dokument214 SeitenCommon Diseases, Vol II - 1223Farruh K100% (1)

- 7 Lessons From A Prophet's WidowDokument27 Seiten7 Lessons From A Prophet's WidowÀbáyòmí Ìbítómi100% (1)

- Shaykh Uthaymeen On Khwaarij NDV120006 PDFDokument12 SeitenShaykh Uthaymeen On Khwaarij NDV120006 PDFabdulNoch keine Bewertungen

- A Brief of Islamic LawDokument137 SeitenA Brief of Islamic Lawwww.alhassanain.org.englishNoch keine Bewertungen

- Stock StatementDokument4 SeitenStock StatementPavani PrasadNoch keine Bewertungen

- Echo Scan ProfileDokument15 SeitenEcho Scan Profileyousrazeidan1979Noch keine Bewertungen

- Carbohydrate Metabolism Disorders Stom 10-11Dokument61 SeitenCarbohydrate Metabolism Disorders Stom 10-11Artem GrigoryanNoch keine Bewertungen

- ACL Injury: Does It Require Surgery?: Anterior Cruciate Ligament (ACL) InjuriesDokument5 SeitenACL Injury: Does It Require Surgery?: Anterior Cruciate Ligament (ACL) InjuriessnottlebieNoch keine Bewertungen

- Medical Examination Form For KASDokument15 SeitenMedical Examination Form For KASMj PayalNoch keine Bewertungen

- Al-Istighfaar (Seeking Forgiveness)Dokument8 SeitenAl-Istighfaar (Seeking Forgiveness)MOHAMAD HANIM BIN MOHAMAD ISANoch keine Bewertungen

- Types of Common Knee Injuries ExplainedDokument6 SeitenTypes of Common Knee Injuries ExplainedSagarNoch keine Bewertungen

- Fagerstrom Questionnaire PDFDokument2 SeitenFagerstrom Questionnaire PDFPamela0% (1)

- Stock StatementDokument5 SeitenStock StatementPraveen S. VastradNoch keine Bewertungen

- I3nformal Hearing TestDokument9 SeitenI3nformal Hearing TestteacherdenNoch keine Bewertungen

- Who Guidelines On Physical Activity and Sedentary BehaviourDokument24 SeitenWho Guidelines On Physical Activity and Sedentary BehaviourLuiz BalioliNoch keine Bewertungen

- Accounting Terms ExplainedDokument6 SeitenAccounting Terms ExplainedSiddharth OjhaNoch keine Bewertungen

- SEM - I Study Material on Basic Accounting ConceptsDokument62 SeitenSEM - I Study Material on Basic Accounting Conceptssagar sheralNoch keine Bewertungen

- Balance SheetDokument5 SeitenBalance Sheet114-CHE-TANMOY PATRANoch keine Bewertungen

- Notes-N-Unit-2-Starting To Cash Book (ALL) - .Dokument93 SeitenNotes-N-Unit-2-Starting To Cash Book (ALL) - .happy lifeNoch keine Bewertungen

- Understanding Basic Accounting TermsDokument17 SeitenUnderstanding Basic Accounting TermsShoryamann SharmaNoch keine Bewertungen

- Accounting PDFDokument10 SeitenAccounting PDFRI AZNoch keine Bewertungen

- Accounting and Financial MangementDokument25 SeitenAccounting and Financial MangementSHASHINoch keine Bewertungen

- Accounting TermsDokument8 SeitenAccounting TermsIshrit GuptaNoch keine Bewertungen

- Financial Accounting: Accounting Basics: Branches of AccountingDokument7 SeitenFinancial Accounting: Accounting Basics: Branches of AccountingLucky HartanNoch keine Bewertungen

- CMBE 2 - Lesson 3 ModuleDokument12 SeitenCMBE 2 - Lesson 3 ModuleEunice AmbrocioNoch keine Bewertungen

- Explaining Financial AccountingDokument6 SeitenExplaining Financial AccountinganishtomanishNoch keine Bewertungen

- A. Under Statement of Financial Position: Typical Account Titles UsedDokument6 SeitenA. Under Statement of Financial Position: Typical Account Titles UsedAshlyn MaeNoch keine Bewertungen

- Introduction To Accounting Introduction To Accounting Introduction To AccountingDokument23 SeitenIntroduction To Accounting Introduction To Accounting Introduction To AccountingAsitha AjayanNoch keine Bewertungen

- Accounting BasicsDokument7 SeitenAccounting BasicsGovind SharmaNoch keine Bewertungen

- Introduction To Accounting, Journal, Ledger, Trial BalanceDokument74 SeitenIntroduction To Accounting, Journal, Ledger, Trial Balanceagustinn agustinNoch keine Bewertungen

- Accounting - DefinitionsDokument4 SeitenAccounting - DefinitionsYashi SharmaNoch keine Bewertungen

- Basics of Accounting: Mba (HRD) Delhi School of Economics Department of Commerce University of DelhiDokument15 SeitenBasics of Accounting: Mba (HRD) Delhi School of Economics Department of Commerce University of DelhiMukesh DroliaNoch keine Bewertungen

- The Accounting EquationDokument5 SeitenThe Accounting EquationHuskyNoch keine Bewertungen

- Basic Terms in AccountingDokument24 SeitenBasic Terms in AccountingVineet SanwalNoch keine Bewertungen

- Basic Accounting TermsDokument8 SeitenBasic Accounting Termsjosephinemusopelo1Noch keine Bewertungen

- HandoutDokument4 SeitenHandoutZack CullenNoch keine Bewertungen

- Accounting Equation: Ads by GoogleDokument9 SeitenAccounting Equation: Ads by GoogleOliver HarmonNoch keine Bewertungen

- MC1404 - Unit 2Dokument111 SeitenMC1404 - Unit 2Senthil KumarNoch keine Bewertungen

- Download the original attachment - The complete basics of accountingDokument32 SeitenDownload the original attachment - The complete basics of accountingvijayNoch keine Bewertungen

- Lesson 3 AccountingDokument12 SeitenLesson 3 AccountingDrin BaliteNoch keine Bewertungen

- Basic Accounting Terminology: Tangible AssetsDokument4 SeitenBasic Accounting Terminology: Tangible Assetskavya guptaNoch keine Bewertungen

- SITXFIN002 Interpret Financial InformationDokument12 SeitenSITXFIN002 Interpret Financial Informationsampath lewkeNoch keine Bewertungen

- Financial AccountingDokument16 SeitenFinancial AccountingSNoch keine Bewertungen

- Fundamentals of Accounting 1 CDokument6 SeitenFundamentals of Accounting 1 CAle EalNoch keine Bewertungen

- UNIT II The Accounting Process Service and TradingDokument22 SeitenUNIT II The Accounting Process Service and TradingAlezandra SantelicesNoch keine Bewertungen

- AP 59 FinPB - 5.06Dokument8 SeitenAP 59 FinPB - 5.06Anonymous Lih1laaxNoch keine Bewertungen

- Bank Mandiri: Growing A High Yield Loan BookDokument7 SeitenBank Mandiri: Growing A High Yield Loan Bookagustus.septNoch keine Bewertungen

- Motion For Extention James As FiledDokument6 SeitenMotion For Extention James As FiledTerry ScannellNoch keine Bewertungen

- 11Dokument16 Seiten11Dennis AleaNoch keine Bewertungen

- Answer Collection Sum of Money - Nelie Consebit PDFDokument5 SeitenAnswer Collection Sum of Money - Nelie Consebit PDFSam Maulana100% (1)

- Home Office Agency and Branch FinancialsDokument11 SeitenHome Office Agency and Branch FinancialsRaraj100% (1)

- Mcleod Vs NLRCDokument2 SeitenMcleod Vs NLRCAnonymous DCagBqFZsNoch keine Bewertungen

- Lukas Foutz - w6 Personal Finance Project - 5375624Dokument12 SeitenLukas Foutz - w6 Personal Finance Project - 5375624api-393000194Noch keine Bewertungen

- Notes On SalesDokument17 SeitenNotes On Saleskenn anoberNoch keine Bewertungen

- SBI Project Report on Loans and AdvancesDokument85 SeitenSBI Project Report on Loans and AdvancesshahidafzalsyedNoch keine Bewertungen

- Monopolystic CompetitionDokument4 SeitenMonopolystic CompetitionKrishna KediaNoch keine Bewertungen

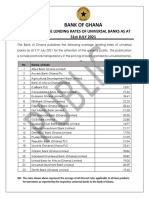

- Average Lending Rates As at July 2021Dokument1 SeiteAverage Lending Rates As at July 2021Fuaad DodooNoch keine Bewertungen

- Project Report - PNBDokument81 SeitenProject Report - PNBabirwadhwa6027100% (1)

- Sir Syed Institute of Sciences and CommerceDokument3 SeitenSir Syed Institute of Sciences and CommerceMian Hidayat ShahNoch keine Bewertungen

- Introduction of Group Accounts A122 1Dokument53 SeitenIntroduction of Group Accounts A122 1Mei Chien YapNoch keine Bewertungen

- Comparative Analysis of Customer Behaviour in Standard Chartered Bank & Barclays BankDokument72 SeitenComparative Analysis of Customer Behaviour in Standard Chartered Bank & Barclays Bankyash guptaNoch keine Bewertungen

- As 16Dokument11 SeitenAs 16Harsh PatelNoch keine Bewertungen

- Airtel Zain AcquisitionDokument14 SeitenAirtel Zain AcquisitionAshish Sharma100% (1)

- 5 Major Sources of Rural Credit in IndiaDokument5 Seiten5 Major Sources of Rural Credit in IndiaParimita Sarma0% (1)

- Chp8 3edition PDFDokument21 SeitenChp8 3edition PDFAbarajithan RajendranNoch keine Bewertungen

- 3&4 Marks Q&A 2018-19Dokument7 Seiten3&4 Marks Q&A 2018-19Mamatha PNoch keine Bewertungen

- Yavantu DocusDokument3 SeitenYavantu DocusEnock MuntuNoch keine Bewertungen

- Answer: Disqualification, Directors, Trustees or Officers. - A Person ShallDokument5 SeitenAnswer: Disqualification, Directors, Trustees or Officers. - A Person ShallJC HilarioNoch keine Bewertungen

- Break Even AnalysysDokument12 SeitenBreak Even Analysysrashmi sahooNoch keine Bewertungen

- Obligations: A. Solutio Indebiti - Undue Payment. B. Negotiorum Gestio - UnauthorizedDokument21 SeitenObligations: A. Solutio Indebiti - Undue Payment. B. Negotiorum Gestio - UnauthorizedJamesCarlSantiago100% (1)

- DPC PRJCT 9th SemDokument8 SeitenDPC PRJCT 9th SemStuti BaradiaNoch keine Bewertungen

- Bond Pricing and Yields ExplainedDokument3 SeitenBond Pricing and Yields ExplainedAchmad Syafi'iNoch keine Bewertungen