Das könnte Ihnen auch gefallen

- FinalsDokument205 SeitenFinalsall in one67% (3)

- Nestle GlobalizationDokument30 SeitenNestle GlobalizationDaryll Peter Griffith60% (5)

- Financial Management 16th Edition Chapter 7Dokument32 SeitenFinancial Management 16th Edition Chapter 7drcoolzNoch keine Bewertungen

- Foundations of Financial Management Canadian 11th Edition Block Solutions ManualDokument39 SeitenFoundations of Financial Management Canadian 11th Edition Block Solutions Manualchristinareedfkrbmpajxs100% (27)

- Treasury Alliance Cash Pooling White PaperDokument16 SeitenTreasury Alliance Cash Pooling White PaperShilpa KogantiNoch keine Bewertungen

- Buuga Barashada Darawalnimada ONE 11Dokument97 SeitenBuuga Barashada Darawalnimada ONE 11Mahad Khadar75% (4)

- Look Beyond ERP - Introducing The DOPDokument10 SeitenLook Beyond ERP - Introducing The DOPolsontd100% (1)

- Rate Rebasing Concepts For Public Consultation, MWSSDokument13 SeitenRate Rebasing Concepts For Public Consultation, MWSSImperator FuriosaNoch keine Bewertungen

- Adwords Fundamental Exam Questions Answers 2016Dokument21 SeitenAdwords Fundamental Exam Questions Answers 2016Avinash VermaNoch keine Bewertungen

- Jcpenney Analysis: Background StoryDokument13 SeitenJcpenney Analysis: Background StoryAakarshan MundraNoch keine Bewertungen

- Ch7 HW AnswersDokument31 SeitenCh7 HW Answerscourtdubs78% (9)

- Document 1113 9704Dokument52 SeitenDocument 1113 9704javierwarrenqswgiefjynNoch keine Bewertungen

- Foundations of Financial Management 16th Edition Block Solutions ManualDokument31 SeitenFoundations of Financial Management 16th Edition Block Solutions Manualnorianenclasphxnu100% (29)

- QuestionsDokument30 SeitenQuestionsArra VillanuevaNoch keine Bewertungen

- Capital ManagementDokument32 SeitenCapital ManagementAngel TumamaoNoch keine Bewertungen

- Foundations of Financial Management Canadian 10th Edition Block Solutions Manual DownloadDokument33 SeitenFoundations of Financial Management Canadian 10th Edition Block Solutions Manual DownloadPeter Coffey100% (22)

- Foundations of Financial Management Canadian 10th Edition Block Solutions ManualDokument33 SeitenFoundations of Financial Management Canadian 10th Edition Block Solutions Manualnorianenclasphxnu100% (24)

- Foundations of Financial Management Canadian 11Th Edition Block Solutions Manual Full Chapter PDFDokument60 SeitenFoundations of Financial Management Canadian 11Th Edition Block Solutions Manual Full Chapter PDFweickumralphie100% (10)

- Seminar Questions Set III A-2Dokument3 SeitenSeminar Questions Set III A-2fanuel kijojiNoch keine Bewertungen

- IMChap 018Dokument12 SeitenIMChap 018MaiNguyenNoch keine Bewertungen

- Untitled DocumentDokument4 SeitenUntitled DocumentLizzy MondiaNoch keine Bewertungen

- Chapter5 ExercisesDokument3 SeitenChapter5 ExercisesTrần Hoài LinhNoch keine Bewertungen

- Some ExercisesDokument3 SeitenSome ExercisesMinh Tâm NguyễnNoch keine Bewertungen

- Chapter Review and Self-Test Problem: 692 Part SevenDokument15 SeitenChapter Review and Self-Test Problem: 692 Part SevenRony RahmanNoch keine Bewertungen

- CH17Dokument7 SeitenCH17mnbzxcpoiqweNoch keine Bewertungen

- Exercises of Cash Liquidity ManagementDokument8 SeitenExercises of Cash Liquidity ManagementTâm ThuNoch keine Bewertungen

- 06 Current Assets ManagementDokument2 Seiten06 Current Assets ManagementQamber AbbasNoch keine Bewertungen

- Cash DisbursementsDokument5 SeitenCash DisbursementsMiracle SalvadorNoch keine Bewertungen

- Cash DisbursementsDokument5 SeitenCash DisbursementsMiracle SalvadorNoch keine Bewertungen

- Tutorial 5 & 6 - SolutionDokument6 SeitenTutorial 5 & 6 - SolutionHamza IftekharNoch keine Bewertungen

- Cash ManagementDokument18 SeitenCash ManagementJoshua CabinasNoch keine Bewertungen

- Cash and Marketable Securities Management SOLUTIONSDokument10 SeitenCash and Marketable Securities Management SOLUTIONSJack Herer100% (2)

- Chapter 17 Liquidity Risk Math Problems and SolutionsDokument4 SeitenChapter 17 Liquidity Risk Math Problems and SolutionsRiyad100% (1)

- Problem Set 7 - FINS3630 (Solutions)Dokument4 SeitenProblem Set 7 - FINS3630 (Solutions)DWdeNoch keine Bewertungen

- Assignment # 4 26 CH 22Dokument6 SeitenAssignment # 4 26 CH 22Ibrahim AbdallahNoch keine Bewertungen

- International Cash ManagementDokument21 SeitenInternational Cash ManagementSushil Regmi71% (7)

- Fin103 LT2 2004 - JTA-1Dokument4 SeitenFin103 LT2 2004 - JTA-1JARED DARREN ONGNoch keine Bewertungen

- Blcok 5 MCO 7 Unit 2Dokument12 SeitenBlcok 5 MCO 7 Unit 2Tushar SharmaNoch keine Bewertungen

- Chapter 6 - Cash Management: Learning ObjectivesDokument5 SeitenChapter 6 - Cash Management: Learning Objectives132345usdfghjNoch keine Bewertungen

- Week 4 Tutorial QuestionsDokument5 SeitenWeek 4 Tutorial QuestionsJess XueNoch keine Bewertungen

- Financial Institutions Management - Chap017Dokument11 SeitenFinancial Institutions Management - Chap017Abhilash PattanaikNoch keine Bewertungen

- Financial Markets Institutions and Money 3Rd Edition Kidwell Solutions Manual Full Chapter PDFDokument27 SeitenFinancial Markets Institutions and Money 3Rd Edition Kidwell Solutions Manual Full Chapter PDFalicebellamyq3yj100% (12)

- Liquidity RiskDokument25 SeitenLiquidity RiskWakas Khalid100% (1)

- CF Chap027Dokument16 SeitenCF Chap027AgnesNoch keine Bewertungen

- FM - Working Capital MGMTDokument6 SeitenFM - Working Capital MGMTSam Sasuman100% (1)

- Cash and Liquidity Management: Answers To Concepts Review and Critical Thinking Questions 1Dokument13 SeitenCash and Liquidity Management: Answers To Concepts Review and Critical Thinking Questions 1Shiny NatividadNoch keine Bewertungen

- Working Capital ManagementDokument9 SeitenWorking Capital ManagementEmmanuelNoch keine Bewertungen

- Use The Data Below To Answer The Next 2 Requirements:: Case I Cash Conversion Cycle/ Cash Operating Cycle AdoptedDokument4 SeitenUse The Data Below To Answer The Next 2 Requirements:: Case I Cash Conversion Cycle/ Cash Operating Cycle AdoptedShiela Mae BautistaNoch keine Bewertungen

- Working Capital Management: Delivered By: Dr. Shakeel Iqbal AwanDokument48 SeitenWorking Capital Management: Delivered By: Dr. Shakeel Iqbal AwanMuhammad Abdul Wajid RaiNoch keine Bewertungen

- Chapter SixDokument47 SeitenChapter SixAlmaz Getachew0% (1)

- Chapter SixDokument47 SeitenChapter SixAshenafi ZelekeNoch keine Bewertungen

- Credit Memorandum: Situation OverviewDokument2 SeitenCredit Memorandum: Situation OverviewAlbert JonesNoch keine Bewertungen

- Facets of Cash ManagementDokument6 SeitenFacets of Cash Managementjustin lytanNoch keine Bewertungen

- University of Tunis Tunis Business School: Corporate FinanceDokument3 SeitenUniversity of Tunis Tunis Business School: Corporate FinanceArbi ChaimaNoch keine Bewertungen

- Cash ManagementDokument5 SeitenCash ManagementVote btsNoch keine Bewertungen

- The Role of Working CapitalDokument9 SeitenThe Role of Working CapitalAbuBakarSiddiqueNoch keine Bewertungen

- International Financial Management 9Dokument38 SeitenInternational Financial Management 9胡依然100% (3)

- Financial Management: Week 10Dokument10 SeitenFinancial Management: Week 10sanjeev parajuliNoch keine Bewertungen

- Credit Memorandum: Situation OverviewDokument2 SeitenCredit Memorandum: Situation OverviewAlbert JonesNoch keine Bewertungen

- Ec103 Week 07 and 08 s14Dokument31 SeitenEc103 Week 07 and 08 s14юрий локтионовNoch keine Bewertungen

- BA303-Tutorial 11Dokument2 SeitenBA303-Tutorial 11Vin ShyangNoch keine Bewertungen

- Part 1: Multiple Choice 2 Points Each /140 Points 5 Points Deduction For Every 5 Items Answered IncorectlyDokument22 SeitenPart 1: Multiple Choice 2 Points Each /140 Points 5 Points Deduction For Every 5 Items Answered IncorectlyDanna Karen MallariNoch keine Bewertungen

- Making Money Simple: The Complete Guide to Getting Your Financial House in Order and Keeping It That Way ForeverVon EverandMaking Money Simple: The Complete Guide to Getting Your Financial House in Order and Keeping It That Way ForeverNoch keine Bewertungen

- Rcial Banking Management: CommeDokument31 SeitenRcial Banking Management: Commemohamed saedNoch keine Bewertungen

- Establishing New Banks, Branches & AtmsDokument13 SeitenEstablishing New Banks, Branches & Atmsmohamed saedNoch keine Bewertungen

- Chapter Seven: Risk Management For Changing Interest Rates: Asset-Liability Management and Duration TechniquesDokument47 SeitenChapter Seven: Risk Management For Changing Interest Rates: Asset-Liability Management and Duration Techniquesmohamed saedNoch keine Bewertungen

- QuestionaireDokument22 SeitenQuestionaireRANNY CAMERONNoch keine Bewertungen

- Elizabeth Wairimu Waiyaki Emod 2017Dokument92 SeitenElizabeth Wairimu Waiyaki Emod 2017Priska ParamitaNoch keine Bewertungen

- Dokumen - Tips Chapter 12 HomeworkDokument6 SeitenDokumen - Tips Chapter 12 Homeworkmohamed saedNoch keine Bewertungen

- Major Duties and Responsibilities of Central BankDokument25 SeitenMajor Duties and Responsibilities of Central BankUyên PhươngNoch keine Bewertungen

- "The Ecommerce Business Plan": March 2019Dokument2 Seiten"The Ecommerce Business Plan": March 2019mohamed saedNoch keine Bewertungen

- Basic Concepts of Financial AccountingDokument107 SeitenBasic Concepts of Financial AccountingVidyadhar Raju VarakaviNoch keine Bewertungen

- Accounting: BasicsDokument18 SeitenAccounting: Basicsdany2884bcNoch keine Bewertungen

- Accounting: BasicsDokument18 SeitenAccounting: Basicsdany2884bcNoch keine Bewertungen

- Leadership Styles Questionnaire: PurposeDokument2 SeitenLeadership Styles Questionnaire: PurposeAi Ling TanNoch keine Bewertungen

- Financial Accounting PDFDokument43 SeitenFinancial Accounting PDFJaya SudhakarNoch keine Bewertungen

- Start-Up Sample BPDokument54 SeitenStart-Up Sample BPsteven100% (1)

- Logistics HandbookDokument174 SeitenLogistics HandbookNeel KanthNoch keine Bewertungen

- Basic Concepts of Financial AccountingDokument107 SeitenBasic Concepts of Financial AccountingVidyadhar Raju VarakaviNoch keine Bewertungen

- International Marketing 16th Edition by Cateora Gilly and Graham Solution Manual PDFDokument9 SeitenInternational Marketing 16th Edition by Cateora Gilly and Graham Solution Manual PDFmohamed saedNoch keine Bewertungen

- Answer KeyDokument52 SeitenAnswer KeyDevonNoch keine Bewertungen

- MGMT172 Chapter2Dokument33 SeitenMGMT172 Chapter2mohamed saedNoch keine Bewertungen

- Best Ice Cream Business Plan WTH Financials PDFDokument11 SeitenBest Ice Cream Business Plan WTH Financials PDFSana SaleemNoch keine Bewertungen

- Sport RetailDokument6 SeitenSport RetailWong Wei ZhenNoch keine Bewertungen

- Sources of Business FinanceDokument26 SeitenSources of Business FinancePrashanthChauhanNoch keine Bewertungen

- Chapter One:: 1: Definition of Management Information SystemDokument3 SeitenChapter One:: 1: Definition of Management Information Systemmohamed saedNoch keine Bewertungen

- Agenda of Meeting 1: Student Performance DeclineDokument2 SeitenAgenda of Meeting 1: Student Performance Declinemohamed saedNoch keine Bewertungen

- Ice Cream Business PlanDokument72 SeitenIce Cream Business PlanRukshar Ahmed Khan100% (1)

- Nternational Arketing: Business 1670 Fall Semester 2012Dokument8 SeitenNternational Arketing: Business 1670 Fall Semester 2012mohamed saedNoch keine Bewertungen

- Start-Up Sample BPDokument54 SeitenStart-Up Sample BPsteven100% (1)

- Sample Food Business PlanDokument17 SeitenSample Food Business PlanTapan Jain100% (1)

- Chapter One:: 1: Definition of Management Information SystemDokument3 SeitenChapter One:: 1: Definition of Management Information Systemmohamed saedNoch keine Bewertungen

- Etrade 1.5M 21082020Dokument3 SeitenEtrade 1.5M 21082020zayar ooNoch keine Bewertungen

- SBIR Program OverviewDokument13 SeitenSBIR Program OverviewFernie1Noch keine Bewertungen

- Self-Instructional Manual (SIM) For Self-Directed Learning (SDL)Dokument34 SeitenSelf-Instructional Manual (SIM) For Self-Directed Learning (SDL)sunny amarillo100% (1)

- Glenda Lee Resume 2Dokument2 SeitenGlenda Lee Resume 2api-516194049Noch keine Bewertungen

- Auditing and Investigation Acc 412Dokument7 SeitenAuditing and Investigation Acc 412saidsulaiman2095Noch keine Bewertungen

- Project ManagementxxDokument34 SeitenProject ManagementxxAli Akand AsifNoch keine Bewertungen

- Developing Agro-Industries For Employment Generation in Rural AreasDokument2 SeitenDeveloping Agro-Industries For Employment Generation in Rural AreasRaj RudrapaaNoch keine Bewertungen

- Application of ComputerDokument5 SeitenApplication of ComputerKavita SinghNoch keine Bewertungen

- Agility Vs FlexibilityDokument13 SeitenAgility Vs FlexibilityDeepakNoch keine Bewertungen

- Unit 5 - Partnership ActDokument28 SeitenUnit 5 - Partnership ActNataraj PNoch keine Bewertungen

- FTCXSXSXSP - Seminar 8 - AnswersDokument4 SeitenFTCXSXSXSP - Seminar 8 - AnswersLewis FergusonNoch keine Bewertungen

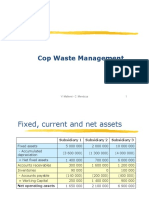

- Cop Waste Management SolutionDokument5 SeitenCop Waste Management SolutionPaul GhanimehNoch keine Bewertungen

- Competency Model BooksDokument4 SeitenCompetency Model Bookshoa quynh anhNoch keine Bewertungen

- Cost FuctionDokument59 SeitenCost FuctionShubham AggarwalNoch keine Bewertungen

- Chap01 Tutorial QuestionsDokument3 SeitenChap01 Tutorial QuestionsThắng Nguyễn HuyNoch keine Bewertungen

- Distributor Sales Force Performance ManagementDokument15 SeitenDistributor Sales Force Performance ManagementTomy Utomo75% (4)

- TOPCA Statement Re Public Process WVP Brownfield Site March 10 2017Dokument1 SeiteTOPCA Statement Re Public Process WVP Brownfield Site March 10 2017Sen HuNoch keine Bewertungen

- HR E1 - Project ManagementDokument2 SeitenHR E1 - Project ManagementAlelei BungalanNoch keine Bewertungen

- Thesis Intellectual Property RightsDokument7 SeitenThesis Intellectual Property Rightsvaivuggld100% (2)

- Answer - CHAPTER 7 FUTURES AND OPTIONS ON FOREIGN EXCHANGEDokument7 SeitenAnswer - CHAPTER 7 FUTURES AND OPTIONS ON FOREIGN EXCHANGETRÂM BÙI THỊ MAINoch keine Bewertungen

- Sify'S Sap Services Capabilities Around Cloud Adoption: 15 February 2021Dokument40 SeitenSify'S Sap Services Capabilities Around Cloud Adoption: 15 February 2021Jitesh M NairNoch keine Bewertungen

- Income Taxation - Final Taxes and CGTDokument3 SeitenIncome Taxation - Final Taxes and CGTDrew BanlutaNoch keine Bewertungen

- Q&A InvestorDokument2 SeitenQ&A Investorjns1992Noch keine Bewertungen

- World Greatest Strategists - Warren BuffetDokument2 SeitenWorld Greatest Strategists - Warren Buffetjojie dador100% (1)

- Performance Evaluation FormDokument6 SeitenPerformance Evaluation FormBhushan100% (1)