Das könnte Ihnen auch gefallen

- Life, Accident and Health Insurance in the United StatesVon EverandLife, Accident and Health Insurance in the United StatesBewertung: 5 von 5 Sternen5/5 (1)

- Asian Crusader Life Insurance Ruling Analyzes Material ConcealmentDokument13 SeitenAsian Crusader Life Insurance Ruling Analyzes Material ConcealmentArahbells100% (1)

- Vocabulary For The TOEIC Test FDokument13 SeitenVocabulary For The TOEIC Test FLouis SmithNoch keine Bewertungen

- 04 2019 Up LMT Boc Taxation LawDokument36 Seiten04 2019 Up LMT Boc Taxation LawMikee PortesNoch keine Bewertungen

- Digests Assignment in InsuranceDokument10 SeitenDigests Assignment in InsuranceMary Flor GuzmanNoch keine Bewertungen

- Deductions From Gross IncomeDokument66 SeitenDeductions From Gross IncomeGet BurnNoch keine Bewertungen

- Perez v. CA, 323 SCRA 613 (2000)Dokument5 SeitenPerez v. CA, 323 SCRA 613 (2000)KristineSherikaChyNoch keine Bewertungen

- People v. Mallari DigestDokument1 SeitePeople v. Mallari DigestVon Lee De LunaNoch keine Bewertungen

- Tax Appeal SuspensionDokument1 SeiteTax Appeal SuspensionVon Lee De LunaNoch keine Bewertungen

- 2020 Mock Exam - LIIIDokument143 Seiten2020 Mock Exam - LIIISteph O100% (2)

- Rule 130, Section 40, (One of The Execptions To The Hearsay Rule) ProvidesDokument2 SeitenRule 130, Section 40, (One of The Execptions To The Hearsay Rule) ProvidesVon Lee De LunaNoch keine Bewertungen

- The Free Usage of Which of The Following Items Is Exempt From Fringe Benefit TaxDokument8 SeitenThe Free Usage of Which of The Following Items Is Exempt From Fringe Benefit TaxGIRLNoch keine Bewertungen

- SMALL CLAIMS ReviewerDokument5 SeitenSMALL CLAIMS ReviewerVon Lee De LunaNoch keine Bewertungen

- PAL v. NLRCDokument2 SeitenPAL v. NLRCVon Lee De LunaNoch keine Bewertungen

- People v. Tano DigestDokument2 SeitenPeople v. Tano DigestVon Lee De LunaNoch keine Bewertungen

- 67 Winebrenner v. CIRDokument2 Seiten67 Winebrenner v. CIRVon Lee De LunaNoch keine Bewertungen

- Syllabus Personal FinanceDokument23 SeitenSyllabus Personal FinanceShahanie Joy Reyes50% (4)

- 01.00 RFP - F50B1600006 - Innovative - Work - Force - 11102020Dokument73 Seiten01.00 RFP - F50B1600006 - Innovative - Work - Force - 11102020Aravinda KrishnanNoch keine Bewertungen

- Perez Vs CA DIGESTDokument1 SeitePerez Vs CA DIGESTReginaNoch keine Bewertungen

- Insurance Contract Not PerfectedDokument3 SeitenInsurance Contract Not PerfectedMarry LasherasNoch keine Bewertungen

- Francisco V. People G.R. No. 146584 July 12, 2004Dokument2 SeitenFrancisco V. People G.R. No. 146584 July 12, 2004Von Lee De LunaNoch keine Bewertungen

- GREAT PACIFIC LIFE ASSURANCE COMPANY, Petitioner, vs. HONORABLE COURT OF APPEALS, RespondentsDokument2 SeitenGREAT PACIFIC LIFE ASSURANCE COMPANY, Petitioner, vs. HONORABLE COURT OF APPEALS, RespondentsWilliam AzucenaNoch keine Bewertungen

- SPS. BIESTERBOS V. CA, EFREN BARTOLOMEDokument1 SeiteSPS. BIESTERBOS V. CA, EFREN BARTOLOMEVon Lee De LunaNoch keine Bewertungen

- Bank liability for lost titles in safety deposit boxDokument2 SeitenBank liability for lost titles in safety deposit boxiwamawi100% (1)

- Perez vs. CADokument12 SeitenPerez vs. CAisaaabelrfNoch keine Bewertungen

- 20 - Virginia Perez Vs CADokument7 Seiten20 - Virginia Perez Vs CAVincent OngNoch keine Bewertungen

- Perez vs. Court of AppealsDokument3 SeitenPerez vs. Court of AppealsnathNoch keine Bewertungen

- 3) Perez vs. Court of Appeals, 323 SCRA 613, G.R. No. 112329 January 28, 2000Dokument7 Seiten3) Perez vs. Court of Appeals, 323 SCRA 613, G.R. No. 112329 January 28, 2000Alexiss Mace JuradoNoch keine Bewertungen

- 2 Perez v. CADokument11 Seiten2 Perez v. CARaymund CallejaNoch keine Bewertungen

- Perez v. CA and BF LifemanDokument8 SeitenPerez v. CA and BF LifemanArnold BagalanteNoch keine Bewertungen

- Perez v. CADokument11 SeitenPerez v. CAmonagbayaniNoch keine Bewertungen

- Great Pacific Life Assurance Company vs. Court of AppealsDokument12 SeitenGreat Pacific Life Assurance Company vs. Court of AppealsHeidiNoch keine Bewertungen

- VOL. 89, APRIL 30, 1979 543 Great Pacific Life Assurance Company vs. Court of AppealsDokument11 SeitenVOL. 89, APRIL 30, 1979 543 Great Pacific Life Assurance Company vs. Court of AppealsdanexrainierNoch keine Bewertungen

- Perez Vs CADokument8 SeitenPerez Vs CADenise Jane DuenasNoch keine Bewertungen

- Case DigestDokument8 SeitenCase DigestARCHIE AJIASNoch keine Bewertungen

- Virginia A Perez Vs CA and BF Lifeman Insurance Corp 323 SCRA 613 DigestDokument3 SeitenVirginia A Perez Vs CA and BF Lifeman Insurance Corp 323 SCRA 613 Digestemmaniago08Noch keine Bewertungen

- Insurance Contract Not PerfectedDokument5 SeitenInsurance Contract Not PerfectedDanica Irish RevillaNoch keine Bewertungen

- ErgsdgsdgsdgDokument1 SeiteErgsdgsdgsdgPatrickHidalgoNoch keine Bewertungen

- Insurance Contract Not Perfected Due to Insured's Death Before Policy ApprovalDokument3 SeitenInsurance Contract Not Perfected Due to Insured's Death Before Policy ApprovalRal CaldiNoch keine Bewertungen

- R131S1 - Pioneer Insurance & Surety Corp VS YapDokument11 SeitenR131S1 - Pioneer Insurance & Surety Corp VS YapAllyza SantosNoch keine Bewertungen

- Great Pacific Life Ass. Co - Vs CA FTDokument4 SeitenGreat Pacific Life Ass. Co - Vs CA FTDianne YcoNoch keine Bewertungen

- 11-Regina L. Edillon vs. Manila Bankers Life Insurance Corporation, G.R. No. L-34200, 30 September 1982Dokument4 Seiten11-Regina L. Edillon vs. Manila Bankers Life Insurance Corporation, G.R. No. L-34200, 30 September 1982Jopan SJNoch keine Bewertungen

- Edillon Vs Manila Bankers 34200Dokument4 SeitenEdillon Vs Manila Bankers 34200Alvin-Evelyn GuloyNoch keine Bewertungen

- GrepavCADokument15 SeitenGrepavCAMorphuesNoch keine Bewertungen

- Puno (C.J., Chairperson), Carpio, Corona Petition Denied, Assailed Decision AffirmedDokument10 SeitenPuno (C.J., Chairperson), Carpio, Corona Petition Denied, Assailed Decision AffirmedAaron CarinoNoch keine Bewertungen

- Perez v. CADokument4 SeitenPerez v. CAMICAELA NIALANoch keine Bewertungen

- (B. Parties To The Contract) Great Pacific Life Assurance Corp. vs. Court of Appeals, 316 SCRA 677, G.R. No. 113899 October 13, 1999Dokument9 Seiten(B. Parties To The Contract) Great Pacific Life Assurance Corp. vs. Court of Appeals, 316 SCRA 677, G.R. No. 113899 October 13, 1999Alexiss Mace JuradoNoch keine Bewertungen

- Perez V CA & BF LifemanDokument6 SeitenPerez V CA & BF Lifemanfjl_302711Noch keine Bewertungen

- Supreme Court: 1âwphi1.nêtDokument5 SeitenSupreme Court: 1âwphi1.nêtbingkydoodle1012Noch keine Bewertungen

- Edillon v. Manila Bankers Life, 117 SCRA 187 (1982)Dokument4 SeitenEdillon v. Manila Bankers Life, 117 SCRA 187 (1982)Justine UyNoch keine Bewertungen

- K.V. Faylona For Petitioners-Appellants. L. L. Reyes For Respondents-AppelleesDokument3 SeitenK.V. Faylona For Petitioners-Appellants. L. L. Reyes For Respondents-AppelleesTin LicoNoch keine Bewertungen

- 550 Supreme Court Reports Annotated: Gulf Resorts, Inc. vs. Philippine Charter Insurance CorporationDokument28 Seiten550 Supreme Court Reports Annotated: Gulf Resorts, Inc. vs. Philippine Charter Insurance Corporationbrida athenaNoch keine Bewertungen

- Excellent Quality Apparel vs. Visayan SuretyDokument17 SeitenExcellent Quality Apparel vs. Visayan SuretyDenzel Edward CariagaNoch keine Bewertungen

- Insurance Batch 3Dokument44 SeitenInsurance Batch 3Radel LlagasNoch keine Bewertungen

- Eternal Gardens v. PHILAMLIFEDokument3 SeitenEternal Gardens v. PHILAMLIFESophiaFrancescaEspinosaNoch keine Bewertungen

- Insurance Last BatchDokument139 SeitenInsurance Last BatchEarl ConcepcionNoch keine Bewertungen

- Great Pacific Life Assu Vs CA April 30, 1979Dokument2 SeitenGreat Pacific Life Assu Vs CA April 30, 1979Alvin-Evelyn GuloyNoch keine Bewertungen

- United Merchants Corporation, Petitioner, vs. Country Bankers Insurance Corporation, RespondentDokument22 SeitenUnited Merchants Corporation, Petitioner, vs. Country Bankers Insurance Corporation, RespondentdanexrainierNoch keine Bewertungen

- Petitioners vs. vs. Respondents Alfredo I. Raya Ambrocio Padilla, Mempin & Reyes Law OfficesDokument10 SeitenPetitioners vs. vs. Respondents Alfredo I. Raya Ambrocio Padilla, Mempin & Reyes Law OfficesBeya AmaroNoch keine Bewertungen

- DBP Vs CaDokument28 SeitenDBP Vs CaYe Seul DvngrcNoch keine Bewertungen

- Tang vs. CADokument8 SeitenTang vs. CAAdelyn Joy SalvadorNoch keine Bewertungen

- 2.phil Phoenix Surety vs. Woordworks, Inc.Dokument9 Seiten2.phil Phoenix Surety vs. Woordworks, Inc.Russel LaquiNoch keine Bewertungen

- 4 - Insurance CasesDokument13 Seiten4 - Insurance CasesFRANCIS CEDRIC KHONoch keine Bewertungen

- 13 - Perla Vs CADokument8 Seiten13 - Perla Vs CAVincent OngNoch keine Bewertungen

- Aug 2 Collated With No. 14Dokument19 SeitenAug 2 Collated With No. 14dwight yuNoch keine Bewertungen

- Perez vs. Court of AppealsDokument22 SeitenPerez vs. Court of AppealsKate HizonNoch keine Bewertungen

- G. Rescisision of Insurance Contracts 1. Concealment: Ruling: 1. NO. The Receipt Was Intended To Be Merely ADokument20 SeitenG. Rescisision of Insurance Contracts 1. Concealment: Ruling: 1. NO. The Receipt Was Intended To Be Merely AChristine MontefalconNoch keine Bewertungen

- Virginia V CADokument5 SeitenVirginia V CAGabe BedanaNoch keine Bewertungen

- G.R. No. L-25317 Phil Phoenix Surety & Insurance Co., Inc., v. Woodworks, IncDokument4 SeitenG.R. No. L-25317 Phil Phoenix Surety & Insurance Co., Inc., v. Woodworks, IncJane FrioloNoch keine Bewertungen

- Petitioner vs. vs. Respondents: First DivisionDokument6 SeitenPetitioner vs. vs. Respondents: First Divisionjames lebronNoch keine Bewertungen

- Perez Vs CA-digestDokument1 SeitePerez Vs CA-digestElsie CayetanoNoch keine Bewertungen

- Philippine Phoenix V Woodworks PDFDokument5 SeitenPhilippine Phoenix V Woodworks PDFRobert LastrillaNoch keine Bewertungen

- IngdsDokument3 SeitenIngdsIt'sRalph MondayNoch keine Bewertungen

- Supreme Court Rules Unpaid Insurance Premium Not EnforceableDokument4 SeitenSupreme Court Rules Unpaid Insurance Premium Not EnforceableShiena Lou B. Amodia-RabacalNoch keine Bewertungen

- Great Pacific Life v. CADokument6 SeitenGreat Pacific Life v. CABeya AmaroNoch keine Bewertungen

- 129336-1992-New Life Enterprises v. Court of Appeals20210424-14-Vaie7cDokument11 Seiten129336-1992-New Life Enterprises v. Court of Appeals20210424-14-Vaie7cKarl OdroniaNoch keine Bewertungen

- Geagonia vs. Court of AppealsDokument18 SeitenGeagonia vs. Court of AppealsdelbertcruzNoch keine Bewertungen

- LBP v. KhoDokument2 SeitenLBP v. KhoVon Lee De LunaNoch keine Bewertungen

- 2 - UNION BANK v. CA - de LunaDokument2 Seiten2 - UNION BANK v. CA - de LunaVon Lee De LunaNoch keine Bewertungen

- Almeda v. CA: G.R. No. 113412, April 17, 1996, 256 SCRA 292 FactsDokument1 SeiteAlmeda v. CA: G.R. No. 113412, April 17, 1996, 256 SCRA 292 FactsCza PeñaNoch keine Bewertungen

- Case Facts Issue Held: Classified As Mineral, Forest, Residential, Commercial or Industrial Land."Dokument2 SeitenCase Facts Issue Held: Classified As Mineral, Forest, Residential, Commercial or Industrial Land."Von Lee De LunaNoch keine Bewertungen

- People vs. BontuyanDokument1 SeitePeople vs. BontuyanVon Lee De LunaNoch keine Bewertungen

- 96 - CIR v. Next Mobile - de LunaDokument2 Seiten96 - CIR v. Next Mobile - de LunaVon Lee De LunaNoch keine Bewertungen

- 223 - GSIS v. City Treasurer - de LunaDokument2 Seiten223 - GSIS v. City Treasurer - de LunaVon Lee De LunaNoch keine Bewertungen

- 13 - PhilAm Life v. CIR - de LunaDokument1 Seite13 - PhilAm Life v. CIR - de LunaVon Lee De LunaNoch keine Bewertungen

- YULO GUILTY OF BOUNCING CHECKSDokument1 SeiteYULO GUILTY OF BOUNCING CHECKSVon Lee De LunaNoch keine Bewertungen

- Amla Bar Q&aDokument3 SeitenAmla Bar Q&aVon Lee De LunaNoch keine Bewertungen

- CIR VDokument1 SeiteCIR VKhay DheeNoch keine Bewertungen

- Intimacies Between Husband and Wife Do Not Justify The Act of ZuluetaDokument1 SeiteIntimacies Between Husband and Wife Do Not Justify The Act of ZuluetaVon Lee De LunaNoch keine Bewertungen

- PNB Liable for Failing to Verify Property StatusDokument2 SeitenPNB Liable for Failing to Verify Property StatusVon Lee De LunaNoch keine Bewertungen

- 10 - Guevarra v. TCLC - de LunaDokument2 Seiten10 - Guevarra v. TCLC - de LunaVon Lee De LunaNoch keine Bewertungen

- MB Resolution Suspending Savings Association Directors UpheldDokument2 SeitenMB Resolution Suspending Savings Association Directors UpheldVon Lee De LunaNoch keine Bewertungen

- Alemar's Sibal & Sons, Inc. v. Hon. Elbinias, Yupangco & Co. DoctrineDokument1 SeiteAlemar's Sibal & Sons, Inc. v. Hon. Elbinias, Yupangco & Co. DoctrineVon Lee De LunaNoch keine Bewertungen

- Ang v. PNBDokument2 SeitenAng v. PNBVon Lee De LunaNoch keine Bewertungen

- E Children's School Tuition Fees, Real Estate Taxes and Other NecessitiesDokument1 SeiteE Children's School Tuition Fees, Real Estate Taxes and Other NecessitiesVon Lee De LunaNoch keine Bewertungen

- 13 CIR v. ERONDokument1 Seite13 CIR v. ERONVon Lee De LunaNoch keine Bewertungen

- People v. CampuhanDokument2 SeitenPeople v. CampuhanVon Lee De LunaNoch keine Bewertungen

- Sukhwinder Fortuneelite 24527 1671441783110Dokument6 SeitenSukhwinder Fortuneelite 24527 1671441783110Harish SharmaNoch keine Bewertungen

- Flmi PDFDokument76 SeitenFlmi PDFSybil KronNoch keine Bewertungen

- Bank of The Philippine IslandsDokument40 SeitenBank of The Philippine IslandsRed Christian PalustreNoch keine Bewertungen

- Annex I: Please Delete Whichever Is InappropriateDokument21 SeitenAnnex I: Please Delete Whichever Is InappropriateVintonius Raffaele PRIMUSNoch keine Bewertungen

- Motor & Fire Insurance ExplainedDokument7 SeitenMotor & Fire Insurance ExplainedabcdNoch keine Bewertungen

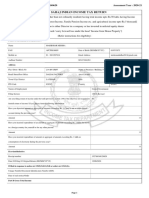

- Itr-1 Sahaj Indian Income Tax Return: Acknowledgement Number: 353838160140620 Assessment Year: 2020-21Dokument7 SeitenItr-1 Sahaj Indian Income Tax Return: Acknowledgement Number: 353838160140620 Assessment Year: 2020-21ADITYA KUMAR MISHRANoch keine Bewertungen

- The High Cost of Cheap Health Insurance - Consumer ReportsDokument12 SeitenThe High Cost of Cheap Health Insurance - Consumer Reportslitnant writersNoch keine Bewertungen

- Term I Xii Eng Board Exam Revision MaterialDokument43 SeitenTerm I Xii Eng Board Exam Revision MaterialYogesh ReddyNoch keine Bewertungen

- GAISANO CAGAYAN INC. v. INSURANCE COMPANY OF N.A.Dokument3 SeitenGAISANO CAGAYAN INC. v. INSURANCE COMPANY OF N.A.Tricia CornelioNoch keine Bewertungen

- 2017 Spring PDFDokument56 Seiten2017 Spring PDF駱晏而Noch keine Bewertungen

- 10 Year Questions Issue of SharesDokument34 Seiten10 Year Questions Issue of Sharesoldtaxi9Noch keine Bewertungen

- Law of Agency Case StudyDokument1 SeiteLaw of Agency Case StudyAzizah Hassan100% (2)

- 5.gsis VS Simeon TanedoDokument13 Seiten5.gsis VS Simeon TanedoViolet BlueNoch keine Bewertungen

- Financial IntermediariesDokument63 SeitenFinancial Intermediariesjustin razonNoch keine Bewertungen

- Residence and Travel QuestionnaireDokument2 SeitenResidence and Travel Questionnaireyasirkazmi856100% (1)

- Long-Term Care Insurance ExplainedDokument23 SeitenLong-Term Care Insurance Explainedswaminathan1Noch keine Bewertungen

- Desertation TopicsDokument25 SeitenDesertation TopicsKarthik MorabadNoch keine Bewertungen

- Venki ProjectDokument89 SeitenVenki ProjectRocking VenkiNoch keine Bewertungen

- IRDA Project - Akanksha - LLMDokument9 SeitenIRDA Project - Akanksha - LLMPULKIT KHANDELWALNoch keine Bewertungen

- Uploads EFILE FileUploads Print Noting1633605009742Dokument80 SeitenUploads EFILE FileUploads Print Noting1633605009742bmohangplNoch keine Bewertungen

- Analysis of SHCIL's Depository ServicesDokument67 SeitenAnalysis of SHCIL's Depository ServicespradeepNoch keine Bewertungen

- Optima Restore Brochure 1Dokument8 SeitenOptima Restore Brochure 1abhi_1mehrotaNoch keine Bewertungen

- Fact Sheet - For Student Exchange-InHADokument3 SeitenFact Sheet - For Student Exchange-InHATeepo08Noch keine Bewertungen