Das könnte Ihnen auch gefallen

- Process Costing: True / False QuestionsDokument226 SeitenProcess Costing: True / False QuestionsElaine Gimarino100% (1)

- Introduction To CSEC POADokument13 SeitenIntroduction To CSEC POAItz Mi AriNoch keine Bewertungen

- Strategic Business Reporting (SBR-INT) : Syllabus and Study GuideDokument19 SeitenStrategic Business Reporting (SBR-INT) : Syllabus and Study GuidendifrekeNoch keine Bewertungen

- Variable Costing and Absorption CostingDokument15 SeitenVariable Costing and Absorption CostingRomilCledoro100% (1)

- CA4 Just in Time and Backlush AccountingDokument9 SeitenCA4 Just in Time and Backlush AccountinghellokittysaranghaeNoch keine Bewertungen

- Process Costing - ReviewerDokument8 SeitenProcess Costing - Reviewergilgil29Noch keine Bewertungen

- Variable Costing and Absorption CostingDokument2 SeitenVariable Costing and Absorption CostingPauline Bogador Mayordomo0% (1)

- Units 1 and 2 TextbookDokument360 SeitenUnits 1 and 2 TextbookCuong Duong100% (1)

- MidtermExam CostingDokument9 SeitenMidtermExam CostingUnknownNoch keine Bewertungen

- Midterm Reviewer Cost AccountingDokument14 SeitenMidterm Reviewer Cost AccountingPrecious AnneNoch keine Bewertungen

- HRSG Competency DictionaryDokument14 SeitenHRSG Competency Dictionarypusdiklat pasarjayaNoch keine Bewertungen

- Quiz Process Costing CompleteDokument4 SeitenQuiz Process Costing CompleteVea Abegail GarciaNoch keine Bewertungen

- University of Caloocan City Cost Accounting & Control Midterm ExaminationDokument8 SeitenUniversity of Caloocan City Cost Accounting & Control Midterm ExaminationAlexandra Nicole IsaacNoch keine Bewertungen

- Cost2 - Finals SY 2020 21 PDFDokument10 SeitenCost2 - Finals SY 2020 21 PDFshengNoch keine Bewertungen

- EG Study Guide 16a PDFDokument488 SeitenEG Study Guide 16a PDFbertlaxinaNoch keine Bewertungen

- Financial Statement Analysis QUIZZERDokument10 SeitenFinancial Statement Analysis QUIZZERBRYLL RODEL PONTINONoch keine Bewertungen

- Corrective Maintenance (BH1) - Process DiagramsDokument2 SeitenCorrective Maintenance (BH1) - Process DiagramsAsfar100% (1)

- Factory Overhead VarianceDokument8 SeitenFactory Overhead VarianceLovely Mae LariosaNoch keine Bewertungen

- Process Cost System: University of Santo Tomas Ust - Alfredo M. Velayo College of Accountancy SECOND TERM AY 2019-2020Dokument17 SeitenProcess Cost System: University of Santo Tomas Ust - Alfredo M. Velayo College of Accountancy SECOND TERM AY 2019-2020allNoch keine Bewertungen

- AFAR Test BankDokument57 SeitenAFAR Test BankandengNoch keine Bewertungen

- PrelimA2 - CVP AnalysisDokument8 SeitenPrelimA2 - CVP AnalysishppddlNoch keine Bewertungen

- Reorganization and Troubled Debt Restructuring - 2Dokument32 SeitenReorganization and Troubled Debt Restructuring - 2Marie GarpiaNoch keine Bewertungen

- JIT & BackflushDokument7 SeitenJIT & BackflushAnis AbdullahNoch keine Bewertungen

- Mas Test Bank QuestionDokument20 SeitenMas Test Bank QuestionAsnor RandyNoch keine Bewertungen

- CVP AnalysisDokument51 SeitenCVP AnalysisMonaliza MalapitNoch keine Bewertungen

- Quiz COST ACCOUNTING AND CONTROLDokument2 SeitenQuiz COST ACCOUNTING AND CONTROLSamelyn SabadoNoch keine Bewertungen

- Mas 02 - Variable Absorption Costing & BudgetingDokument11 SeitenMas 02 - Variable Absorption Costing & BudgetingCriane DomineusNoch keine Bewertungen

- CFAS-MC Ques - Review of The Acctg. ProcessDokument5 SeitenCFAS-MC Ques - Review of The Acctg. ProcessKristine Elaine RocoNoch keine Bewertungen

- Case 1. Landers CompanyDokument3 SeitenCase 1. Landers CompanyMavel DesamparadoNoch keine Bewertungen

- ACYCST Cost Accounting Quiz ReviewerDokument123 SeitenACYCST Cost Accounting Quiz ReviewerelelaiNoch keine Bewertungen

- Joint Products and By-ProductsDokument16 SeitenJoint Products and By-ProductsAnmol AgalNoch keine Bewertungen

- Joint and by - Product CostingDokument22 SeitenJoint and by - Product CostingTamanna ThomasNoch keine Bewertungen

- IAS 23 Borrowing CostsDokument6 SeitenIAS 23 Borrowing CostsSelva Bavani SelwaduraiNoch keine Bewertungen

- HO3 - Cost Concepts and Estimation PDFDokument9 SeitenHO3 - Cost Concepts and Estimation PDFPATRICIA PEREZNoch keine Bewertungen

- Ex2 Accounting For MaterialsDokument6 SeitenEx2 Accounting For MaterialsCHACHACHA100% (1)

- AIS ReviewerDokument20 SeitenAIS ReviewerkimmibanezNoch keine Bewertungen

- 1Bdc Cpa Review Institute: Cost AccountingDokument8 Seiten1Bdc Cpa Review Institute: Cost AccountingJason BautistaNoch keine Bewertungen

- Variable Costing - Lecture NotesDokument22 SeitenVariable Costing - Lecture NotesRaghavNoch keine Bewertungen

- Impairment of AssetsDokument19 SeitenImpairment of AssetsTareq SojolNoch keine Bewertungen

- Property, Plant and EquipmentDokument6 SeitenProperty, Plant and EquipmenthemantbaidNoch keine Bewertungen

- Activity-Based CostingDokument75 SeitenActivity-Based CostingmrnttdpnchngNoch keine Bewertungen

- High Low MethodDokument4 SeitenHigh Low MethodSamreen LodhiNoch keine Bewertungen

- Chapter 04Dokument9 SeitenChapter 04adarshNoch keine Bewertungen

- Diagnostic in Basic AccountingDokument5 SeitenDiagnostic in Basic Accountingjapvivi cece100% (2)

- Activity-Based Costing True-False StatementsDokument5 SeitenActivity-Based Costing True-False StatementsSuman Paul ChowdhuryNoch keine Bewertungen

- IAS-36 (Impairment of Assets)Dokument10 SeitenIAS-36 (Impairment of Assets)Nazmul HaqueNoch keine Bewertungen

- Variable CostingDokument4 SeitenVariable CostingdamdamNoch keine Bewertungen

- Acct 203 - CH 6 DqsDokument2 SeitenAcct 203 - CH 6 Dqsapi-340301334100% (1)

- Assignment - Cost BehaviorsDokument11 SeitenAssignment - Cost BehaviorsMary Antonette LastimosaNoch keine Bewertungen

- 03 Receivables PDFDokument13 Seiten03 Receivables PDFReyn Saplad PeralesNoch keine Bewertungen

- Process Costing and Hybrid Product-Costing SystemsDokument17 SeitenProcess Costing and Hybrid Product-Costing SystemsWailNoch keine Bewertungen

- 04 Relevant CostingDokument5 Seiten04 Relevant CostingMarielle CastañedaNoch keine Bewertungen

- Process Costing ReviewerDokument46 SeitenProcess Costing ReviewerAko Si Cynthia100% (1)

- Joint Cost and by Products PDFDokument20 SeitenJoint Cost and by Products PDFJhoana HernandezNoch keine Bewertungen

- Cengage Eco Dev Chapter 3 - Growth and The Asian ExperienceDokument50 SeitenCengage Eco Dev Chapter 3 - Growth and The Asian ExperienceAnna WilliamsNoch keine Bewertungen

- Cost and Cost ClassificationDokument10 SeitenCost and Cost ClassificationAmod YadavNoch keine Bewertungen

- Test Bank TOCDokument1 SeiteTest Bank TOCAkai Senshi No TenshiNoch keine Bewertungen

- Cost and ManagementDokument38 SeitenCost and ManagementKang JoonNoch keine Bewertungen

- Chapter 1 - Introduction ToDokument30 SeitenChapter 1 - Introduction ToCostAcct1Noch keine Bewertungen

- Multiple ChoiceDokument4 SeitenMultiple ChoiceCarlo ParasNoch keine Bewertungen

- 19 ACDCExerciseIIDokument14 Seiten19 ACDCExerciseIIJohnnoff BagacinaNoch keine Bewertungen

- Drill Prelim To FinalsDokument7 SeitenDrill Prelim To FinalsMila Casandra CastañedaNoch keine Bewertungen

- AC and VCDokument3 SeitenAC and VCMila Casandra CastañedaNoch keine Bewertungen

- Standard Costing EditedDokument13 SeitenStandard Costing Editedking justinNoch keine Bewertungen

- Acdc MCQDokument4 SeitenAcdc MCQCherryjane RuizNoch keine Bewertungen

- Acdc MCQDokument4 SeitenAcdc MCQReyna Mae MartinezNoch keine Bewertungen

- SSB Advertisement 001.2015Dokument11 SeitenSSB Advertisement 001.2015Chandrika DasNoch keine Bewertungen

- Accounting Professionalism-They Just Don't Get It!: Arthur R. WyattDokument10 SeitenAccounting Professionalism-They Just Don't Get It!: Arthur R. WyattFabian QuincheNoch keine Bewertungen

- Internship Report On District Comptroller of Accounts HaripurDokument75 SeitenInternship Report On District Comptroller of Accounts HaripurFaisal AwanNoch keine Bewertungen

- Test Bank For Auditing and Assurance A Business Risk Approach 3rd Edition by JubbDokument19 SeitenTest Bank For Auditing and Assurance A Business Risk Approach 3rd Edition by Jubba878091955Noch keine Bewertungen

- Covid-19-Related Rent Concessions Beyond 30 June 2021 (Amendment To IFRS 16) - Written ReportDokument11 SeitenCovid-19-Related Rent Concessions Beyond 30 June 2021 (Amendment To IFRS 16) - Written ReportSophia GabuatNoch keine Bewertungen

- The Ontario Curriculum Grades 9 - 12 - Financial Literacy, Scope and Sequence of ExpectationsDokument207 SeitenThe Ontario Curriculum Grades 9 - 12 - Financial Literacy, Scope and Sequence of ExpectationsCP Mario Pérez López100% (1)

- ANOVA Step by StepDokument258 SeitenANOVA Step by StepVinothNoch keine Bewertungen

- CH 1 - TemplatesDokument7 SeitenCH 1 - TemplatesadibbahNoch keine Bewertungen

- Ar LMSH 2020Dokument216 SeitenAr LMSH 2020Khairuman NawawiNoch keine Bewertungen

- Internal Audit 3rd CADokument13 SeitenInternal Audit 3rd CAVijaya KumarNoch keine Bewertungen

- P2P AccountingDokument22 SeitenP2P AccountingHimanshu MadanNoch keine Bewertungen

- Indoco Annual Report FY16Dokument160 SeitenIndoco Annual Report FY16Ishaan MittalNoch keine Bewertungen

- Budgetary and Taxation LawDokument8 SeitenBudgetary and Taxation LawGezim Sh JakupiNoch keine Bewertungen

- Fa1 Notes Chapter Four PDFDokument3 SeitenFa1 Notes Chapter Four PDFPrincess ThaabeNoch keine Bewertungen

- Public Sector Accounting AssignmentDokument9 SeitenPublic Sector Accounting AssignmentitulejamesNoch keine Bewertungen

- ch14 Managerial AccountingDokument36 Seitench14 Managerial AccountingMNoch keine Bewertungen

- Accounting (Paper 1) Total Marks: 100 Section A: Class IxDokument12 SeitenAccounting (Paper 1) Total Marks: 100 Section A: Class IxOtaconNoch keine Bewertungen

- Bidco Foods Inc (Solution)Dokument2 SeitenBidco Foods Inc (Solution)avinesh13Noch keine Bewertungen

- CV Sadiq 2010Dokument4 SeitenCV Sadiq 2010Tijani Raheemot AjedoyinNoch keine Bewertungen

- Career Research Paper PDFDokument29 SeitenCareer Research Paper PDFLeonor MendezNoch keine Bewertungen

- Course Structure: Semester-IDokument26 SeitenCourse Structure: Semester-IPrince KatiyarNoch keine Bewertungen

- Thẻ Ghi Nhớ - Accounting 201 Final Exam - QuizletDokument3 SeitenThẻ Ghi Nhớ - Accounting 201 Final Exam - QuizletAn Ngoc CồNoch keine Bewertungen

- Aim vs. Oum: Revenue RecognitionDokument3 SeitenAim vs. Oum: Revenue RecognitionbalajicivNoch keine Bewertungen

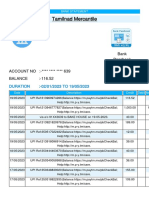

- Tamilnad Mercantile1684550531048Dokument25 SeitenTamilnad Mercantile1684550531048Miracle KhordsNoch keine Bewertungen