Das könnte Ihnen auch gefallen

- Certified Construction Inspection OfficerVon EverandCertified Construction Inspection OfficerBewertung: 5 von 5 Sternen5/5 (1)

- Certificate Program in Financial Analysis, Valuation and Risk ManagementDokument21 SeitenCertificate Program in Financial Analysis, Valuation and Risk ManagementKapil ManglaNoch keine Bewertungen

- Risk in CBDokument11 SeitenRisk in CBRajesh TvsNoch keine Bewertungen

- I. Concept Notes: Return DefinedDokument7 SeitenI. Concept Notes: Return DefinedDanica Christele AlfaroNoch keine Bewertungen

- Credit Rating MatrixDokument12 SeitenCredit Rating MatrixNaman SharmaNoch keine Bewertungen

- Start Up Valuation: EntrepreneurDokument8 SeitenStart Up Valuation: EntrepreneurRuchitha PrakashNoch keine Bewertungen

- Sales TrainingDokument19 SeitenSales TrainingAashish PardeshiNoch keine Bewertungen

- PIFM 2-3 - MergedDokument108 SeitenPIFM 2-3 - Mergedchilukuri sandeepNoch keine Bewertungen

- Fundamentals of Stock AnalysisDokument39 SeitenFundamentals of Stock Analysisraveendhar.k100% (4)

- Saim Unit-1Dokument26 SeitenSaim Unit-1jiny benNoch keine Bewertungen

- CAIIB BFM Module B PDF Paper 2 RISK MANAGEMENT by Ambitious BabaDokument91 SeitenCAIIB BFM Module B PDF Paper 2 RISK MANAGEMENT by Ambitious Babaundru syamtejaNoch keine Bewertungen

- Risk ManagementDokument44 SeitenRisk ManagementJane GavinoNoch keine Bewertungen

- FM - 1Dokument15 SeitenFM - 1akesingsNoch keine Bewertungen

- Risk-Return AnalysisDokument48 SeitenRisk-Return Analysisld464121Noch keine Bewertungen

- Invt. and Portfolio Mgmt.Dokument31 SeitenInvt. and Portfolio Mgmt.Ashwini.S SNoch keine Bewertungen

- Security Analysis AND Portfolio Management: Mba Iii Semester PristDokument15 SeitenSecurity Analysis AND Portfolio Management: Mba Iii Semester PristSingh CharuNoch keine Bewertungen

- Summer InternshipDokument17 SeitenSummer InternshipAnkit PalNoch keine Bewertungen

- SBI ESG Portfolio Mar 2023Dokument21 SeitenSBI ESG Portfolio Mar 2023SabSab MukNoch keine Bewertungen

- Strischek Dev Edited Gs ApprovedDokument45 SeitenStrischek Dev Edited Gs ApprovedthannNoch keine Bewertungen

- ch03 LRDokument25 Seitench03 LRMargaretta LiangNoch keine Bewertungen

- FRM一级百题 风险管理基础Dokument67 SeitenFRM一级百题 风险管理基础bertie RNoch keine Bewertungen

- Experience Summary: Educational Qualifications Career ObjectiveDokument2 SeitenExperience Summary: Educational Qualifications Career ObjectiveRajesh VeeragandhamNoch keine Bewertungen

- Evaluation of Financial FeasibilityDokument25 SeitenEvaluation of Financial FeasibilityDr Sarbesh Mishra86% (7)

- Project Credit Rating & Risk Based PricingDokument13 SeitenProject Credit Rating & Risk Based Pricingrupeshmba2018Noch keine Bewertungen

- Summer InternshipDokument17 SeitenSummer InternshipAnkit Pal100% (1)

- SAPM PDF NotesDokument146 SeitenSAPM PDF Notesprashanth.pranith884Noch keine Bewertungen

- Module 1-Introduction-MergedDokument99 SeitenModule 1-Introduction-MergedKevin MehtaNoch keine Bewertungen

- FINA2209 Financial Planning: Week 4: Client Preferences and Behavioural FinanceDokument34 SeitenFINA2209 Financial Planning: Week 4: Client Preferences and Behavioural FinanceDylan AdrianNoch keine Bewertungen

- Credit Rating AgenciesDokument40 SeitenCredit Rating AgenciesSmriti DurehaNoch keine Bewertungen

- CH 1 SlidesDokument40 SeitenCH 1 SlidesMuhammad AkbarNoch keine Bewertungen

- Lecture 10 - Credit Risk - W23Dokument41 SeitenLecture 10 - Credit Risk - W23siennaNoch keine Bewertungen

- Project Risk: Amity Business SchoolDokument35 SeitenProject Risk: Amity Business SchooltuktukmajiNoch keine Bewertungen

- Types of Risks in Banking Sector: DR - SMDokument30 SeitenTypes of Risks in Banking Sector: DR - SMPriya DharshiniNoch keine Bewertungen

- Investments & RiskDokument20 SeitenInvestments & RiskravaladityaNoch keine Bewertungen

- Risk Management Short Note Lyst5393Dokument28 SeitenRisk Management Short Note Lyst5393Utkarsh SinghalNoch keine Bewertungen

- Debt Analysis and ManagementDokument47 SeitenDebt Analysis and ManagementRahul AtodariaNoch keine Bewertungen

- M. ComDokument31 SeitenM. ComFlip Thirty threeNoch keine Bewertungen

- Certificate Program in Financial Analysis, Valuation & Risk ManagementDokument16 SeitenCertificate Program in Financial Analysis, Valuation & Risk ManagementCharvi SaxenaNoch keine Bewertungen

- Board Perspectives On Risk OversightDokument4 SeitenBoard Perspectives On Risk OversightJulieNoch keine Bewertungen

- BusinessDokument54 SeitenBusinesschitkarashellyNoch keine Bewertungen

- FM Class Capital BudgetingDokument39 SeitenFM Class Capital BudgetingEviya Jerrin KoodalyNoch keine Bewertungen

- Credit Rating at MBDokument26 SeitenCredit Rating at MBGitanjali JoshiNoch keine Bewertungen

- Portfolio Management and Wealth Planning - Cheat SheetDokument14 SeitenPortfolio Management and Wealth Planning - Cheat Sheetlahari kadimicherlaNoch keine Bewertungen

- Credit Rating 1Dokument31 SeitenCredit Rating 1S.r. MohantyNoch keine Bewertungen

- Financing Decision: Dr. D.Shoba MBA, M.Phil, PH.DDokument20 SeitenFinancing Decision: Dr. D.Shoba MBA, M.Phil, PH.DKesava RajanNoch keine Bewertungen

- Investment Analysis and Portfolio Management: Prof Rajiv U KDokument27 SeitenInvestment Analysis and Portfolio Management: Prof Rajiv U Kakanksha raghavNoch keine Bewertungen

- Investor Risk Profile - Report: (Applicable For Unit Linked Insurance Plans)Dokument2 SeitenInvestor Risk Profile - Report: (Applicable For Unit Linked Insurance Plans)miteshNoch keine Bewertungen

- Credit Rating FmsDokument16 SeitenCredit Rating Fmsdurgesh choudharyNoch keine Bewertungen

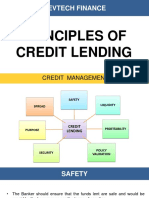

- Principles of Credit LendingDokument10 SeitenPrinciples of Credit LendingRa'fat JalladNoch keine Bewertungen

- PWC UK AIMS - Vacancy DescriptionDokument14 SeitenPWC UK AIMS - Vacancy DescriptionJyotirmoy BhattaNoch keine Bewertungen

- Module - 2 Banking System and Operations: Rajneesh MishraDokument51 SeitenModule - 2 Banking System and Operations: Rajneesh MishramarianmadhurNoch keine Bewertungen

- PWC AIMS - Vacancy DescriptionDokument14 SeitenPWC AIMS - Vacancy DescriptionDurga Prasad HNoch keine Bewertungen

- Sip Presentation in Idbi FederalDokument16 SeitenSip Presentation in Idbi FederalPratik GuptaNoch keine Bewertungen

- BTF and UnemplomentDokument65 SeitenBTF and UnemplomentEl Arch AssmaNoch keine Bewertungen

- 4 - Project Appraisal CompiledDokument6 Seiten4 - Project Appraisal CompiledgetkhosaNoch keine Bewertungen

- A Study On Fixed Income Securities and Their Awareness Among Indian InvestorsDokument82 SeitenA Study On Fixed Income Securities and Their Awareness Among Indian InvestorsSourav LodhaNoch keine Bewertungen

- Bond Port MGMT HandoutDokument7 SeitenBond Port MGMT HandoutAaryan SarupriaNoch keine Bewertungen

- Financial Risk ManagementDokument194 SeitenFinancial Risk ManagementAkanksha Sethi100% (1)

- Credit RatingDokument3 SeitenCredit Ratingsanjay parmar100% (4)

- Risk & Risk Management:: Role of Financial DerivativesDokument24 SeitenRisk & Risk Management:: Role of Financial DerivativesChirag ParakhNoch keine Bewertungen

- MSC ACFN2 RD4 ClassDokument25 SeitenMSC ACFN2 RD4 Classmengistu jiloNoch keine Bewertungen

- ICU General Admission Orders: OthersDokument2 SeitenICU General Admission Orders: OthersHANIMNoch keine Bewertungen

- As-Built Commercial BLDG.1Dokument11 SeitenAs-Built Commercial BLDG.1John Rom CabadonggaNoch keine Bewertungen

- Thermodynamic c106Dokument120 SeitenThermodynamic c106Драгослав БјелицаNoch keine Bewertungen

- Household: Ucsp11/12Hsoiii-20Dokument2 SeitenHousehold: Ucsp11/12Hsoiii-20Igorota SheanneNoch keine Bewertungen

- Contemp Person Act.1Dokument1 SeiteContemp Person Act.1Luisa Jane De LunaNoch keine Bewertungen

- Chapter 24 - The Solar SystemDokument36 SeitenChapter 24 - The Solar SystemHeather Blackwell100% (1)

- 1st Problem Solving Assignment - Barrels of Apples - M383 Sp22.docx-2Dokument4 Seiten1st Problem Solving Assignment - Barrels of Apples - M383 Sp22.docx-2Kor16Noch keine Bewertungen

- The Serious Student of HistoryDokument5 SeitenThe Serious Student of HistoryCrisanto King CortezNoch keine Bewertungen

- Gmail - ICICI BANK I PROCESS HIRING FOR BACKEND - OPERATION PDFDokument2 SeitenGmail - ICICI BANK I PROCESS HIRING FOR BACKEND - OPERATION PDFDeepankar ChoudhuryNoch keine Bewertungen

- Watch One Piece English SubDub Online Free On Zoro - ToDokument1 SeiteWatch One Piece English SubDub Online Free On Zoro - ToSadeusuNoch keine Bewertungen

- Marieb ch3dDokument20 SeitenMarieb ch3dapi-229554503Noch keine Bewertungen

- ProspDokument146 SeitenProspRajdeep BharatiNoch keine Bewertungen

- Laudon - Mis16 - PPT - ch11 - KL - CE (Updated Content For 2021) - Managing Knowledge and Artificial IntelligenceDokument45 SeitenLaudon - Mis16 - PPT - ch11 - KL - CE (Updated Content For 2021) - Managing Knowledge and Artificial IntelligenceSandaru RathnayakeNoch keine Bewertungen

- Assignment RoadDokument14 SeitenAssignment RoadEsya ImanNoch keine Bewertungen

- Ice 3101: Modern Control THEORY (3 1 0 4) : State Space AnalysisDokument15 SeitenIce 3101: Modern Control THEORY (3 1 0 4) : State Space AnalysisBipin KrishnaNoch keine Bewertungen

- SAP HR - Legacy System Migration Workbench (LSMW)Dokument5 SeitenSAP HR - Legacy System Migration Workbench (LSMW)Bharathk KldNoch keine Bewertungen

- Heirs of Vinluan Estate in Pangasinan Charged With Tax Evasion For Unsettled Inheritance Tax CaseDokument2 SeitenHeirs of Vinluan Estate in Pangasinan Charged With Tax Evasion For Unsettled Inheritance Tax CaseAlvin Dela CruzNoch keine Bewertungen

- Datos Adjuntos Sin Título 00013Dokument3 SeitenDatos Adjuntos Sin Título 00013coyana9652Noch keine Bewertungen

- CL200 PLCDokument158 SeitenCL200 PLCJavierRuizThorrensNoch keine Bewertungen

- GA Power Capsule For SBI Clerk Mains 2024 (Part-2)Dokument82 SeitenGA Power Capsule For SBI Clerk Mains 2024 (Part-2)aa1904bbNoch keine Bewertungen

- Antifraud PlaybookDokument60 SeitenAntifraud PlaybookDani UsmarNoch keine Bewertungen

- C++ Program To Create A Student Database - My Computer ScienceDokument10 SeitenC++ Program To Create A Student Database - My Computer ScienceSareeya ShreNoch keine Bewertungen

- Economizer DesignDokument2 SeitenEconomizer Designandremalta09100% (4)

- LYNX 40 Drilling Mud DecanterDokument2 SeitenLYNX 40 Drilling Mud DecanterPierluigi Ciampiconi0% (1)

- A Process Reference Model For Claims Management in Construction Supply Chains The Contractors PerspectiveDokument20 SeitenA Process Reference Model For Claims Management in Construction Supply Chains The Contractors Perspectivejadal khanNoch keine Bewertungen

- Shaqlawa Technical College: IT DepartmentDokument20 SeitenShaqlawa Technical College: IT Departmentbilind_mustafaNoch keine Bewertungen

- Saif Powertec Limited Project "Standard Operating Process" As-Is DocumentDokument7 SeitenSaif Powertec Limited Project "Standard Operating Process" As-Is DocumentAbhishekChowdhuryNoch keine Bewertungen

- Cheerios Media KitDokument9 SeitenCheerios Media Kitapi-300473748Noch keine Bewertungen

- Mobile Services: Your Account Summary This Month'S ChargesDokument3 SeitenMobile Services: Your Account Summary This Month'S Chargeskumarvaibhav301745Noch keine Bewertungen