Das könnte Ihnen auch gefallen

- Taxation Law: I. General PrinciplesDokument11 SeitenTaxation Law: I. General PrinciplesCnfsr KayceNoch keine Bewertungen

- 2019 Bar Examinations TAXATION LAWDokument10 Seiten2019 Bar Examinations TAXATION LAWEric RamilNoch keine Bewertungen

- Bar Bulletin 6Dokument11 SeitenBar Bulletin 6Adrian CabanaNoch keine Bewertungen

- CPA Paper 6Dokument20 SeitenCPA Paper 6sanu sayed100% (1)

- Taxation Law Notes 2020Dokument9 SeitenTaxation Law Notes 2020Kim WaNoch keine Bewertungen

- ACCTAX3 SyllabusDokument5 SeitenACCTAX3 SyllabusEi Ar TaradjiNoch keine Bewertungen

- Iv. Tax Remedies Under The National Internal Revenue CodeDokument3 SeitenIv. Tax Remedies Under The National Internal Revenue CodeRenzil BalicudcudNoch keine Bewertungen

- 2019 Tax SyllabusDokument11 Seiten2019 Tax SyllabusLowie SantiaguelNoch keine Bewertungen

- 2020 Bar Exam Syllabus in Taxation LawDokument11 Seiten2020 Bar Exam Syllabus in Taxation LawMyBias KimSeokJinNoch keine Bewertungen

- Taxation Law SyllabusDokument10 SeitenTaxation Law SyllabusLost StudentNoch keine Bewertungen

- TAXATION LAW REVIEW TopicsDokument13 SeitenTAXATION LAW REVIEW TopicsKimberly RamosNoch keine Bewertungen

- Taxrev SyllabusDokument12 SeitenTaxrev SyllabusDiane JulianNoch keine Bewertungen

- 2009 Taxation Law ReviewerDokument203 Seiten2009 Taxation Law ReviewerDoctorGreyNoch keine Bewertungen

- 4 - Taxation LawDokument10 Seiten4 - Taxation LawNikkiAndradeNoch keine Bewertungen

- 11 CPA TAXATION Paper 11Dokument8 Seiten11 CPA TAXATION Paper 11Kiwalabye OsephNoch keine Bewertungen

- Proposed Syllabus Taxation 1 Atty. SaniDokument13 SeitenProposed Syllabus Taxation 1 Atty. SaniZubair BatuaNoch keine Bewertungen

- Taxation LawDokument16 SeitenTaxation LawBryan Clark ZacariasNoch keine Bewertungen

- Bar 2020 Syllabus - TAXDokument9 SeitenBar 2020 Syllabus - TAXSBCA Legal Aid CenterNoch keine Bewertungen

- Tax Final ExamDokument7 SeitenTax Final ExamJulienne UntalascoNoch keine Bewertungen

- Upreme !court: L/Epublic of Tbe T) Bilippineg FfranilaDokument11 SeitenUpreme !court: L/Epublic of Tbe T) Bilippineg FfranilaPbftNoch keine Bewertungen

- Taxation Law Review SyllabusDokument14 SeitenTaxation Law Review SyllabusRoxanne Peña100% (2)

- Syllabus For Taxation Bar Exam 2019Dokument5 SeitenSyllabus For Taxation Bar Exam 2019Vebsie De la CruzNoch keine Bewertungen

- I. General PrinciplesDokument8 SeitenI. General PrinciplesJed LipaNoch keine Bewertungen

- Syllabus. Income Tax. Mvavjanuary 15, 2018Dokument6 SeitenSyllabus. Income Tax. Mvavjanuary 15, 2018Christine Ang CaminadeNoch keine Bewertungen

- Adzu Tax02 A Learning Packet 1 Orientation and Business TaxesDokument4 SeitenAdzu Tax02 A Learning Packet 1 Orientation and Business TaxesJustine Paul Pangasi-anNoch keine Bewertungen

- Barops Taxation 2020Dokument241 SeitenBarops Taxation 2020Gerry Ombrog100% (1)

- TAXREV SANTOSsyllabusDokument7 SeitenTAXREV SANTOSsyllabusJoma CoronaNoch keine Bewertungen

- Accounting For Income Taxes ExercisessDokument5 SeitenAccounting For Income Taxes ExercisessdorothyannvillamoraaNoch keine Bewertungen

- 17 CPA ADVANCED TAXATION Paper 17Dokument9 Seiten17 CPA ADVANCED TAXATION Paper 17kabendejunior4Noch keine Bewertungen

- Course-Outline Taxation 2Dokument16 SeitenCourse-Outline Taxation 2QueenVictoriaAshleyPrietoNoch keine Bewertungen

- Law 124 Common Outline 1st Sem 15-16 (AAM Approved)Dokument10 SeitenLaw 124 Common Outline 1st Sem 15-16 (AAM Approved)Arrah Mae DavinNoch keine Bewertungen

- Tax Law Syllabus 2021Dokument4 SeitenTax Law Syllabus 2021Francisco BanguisNoch keine Bewertungen

- Taxation LAW: I. General PrinciplesDokument5 SeitenTaxation LAW: I. General PrinciplesclarizzzNoch keine Bewertungen

- Tax Syllabus 2019Dokument6 SeitenTax Syllabus 2019Diding BorromeoNoch keine Bewertungen

- Incom e Tax & Sales Tax La WS: Live Online ClassesDokument3 SeitenIncom e Tax & Sales Tax La WS: Live Online ClassesMashhood AhmedNoch keine Bewertungen

- TaxRev Bar OutlneDokument43 SeitenTaxRev Bar OutlneTricia GrafiloNoch keine Bewertungen

- Accounting For Income TaxesDokument17 SeitenAccounting For Income TaxesKenn Adam Johan Gajudo70% (10)

- Post Graduate Certificate in Finance: (Taxation Laws) - PGCF (TL) ProgramcurriculumDokument1 SeitePost Graduate Certificate in Finance: (Taxation Laws) - PGCF (TL) ProgramcurriculumSanjayNoch keine Bewertungen

- Adzu Tax02 A Course OutlineDokument3 SeitenAdzu Tax02 A Course OutlineJustine Paul Pangasi-anNoch keine Bewertungen

- Level 4 ThoeryDokument4 SeitenLevel 4 ThoeryElias TesfayeNoch keine Bewertungen

- Project MPCBDokument16 SeitenProject MPCBJuliana WaniwanNoch keine Bewertungen

- TAX 2 SyllabusDokument5 SeitenTAX 2 SyllabusSarah Jeane CardonaNoch keine Bewertungen

- Taxation Pilot QuestionsxDokument14 SeitenTaxation Pilot QuestionsxEmmanuel ObafemmyNoch keine Bewertungen

- Quiz 4Dokument4 SeitenQuiz 4cece ceceNoch keine Bewertungen

- Far 6 Accounting For Income TaxDokument3 SeitenFar 6 Accounting For Income TaxanndyNoch keine Bewertungen

- TAX Quiz 2Dokument8 SeitenTAX Quiz 2Pearl Jade YecyecNoch keine Bewertungen

- TAX Final-PreBoard-ExamDokument12 SeitenTAX Final-PreBoard-ExamCovi LokuNoch keine Bewertungen

- Tax Rev SyllabusDokument14 SeitenTax Rev SyllabusIanLightPajaroNoch keine Bewertungen

- Accounting For Income Tax ExamDokument6 SeitenAccounting For Income Tax ExamAnn Christine C. Chua100% (2)

- CPAR B94 TAX Final PB Exam - QuestionsDokument14 SeitenCPAR B94 TAX Final PB Exam - QuestionsSilver LilyNoch keine Bewertungen

- Taxation Material 1Dokument11 SeitenTaxation Material 1Shaira Bugayong100% (1)

- Wk14 Summary Quizzer 2 - Set BDokument5 SeitenWk14 Summary Quizzer 2 - Set Bmariesteinsher0Noch keine Bewertungen

- Taxes Tax and Tax AdministrationDokument20 SeitenTaxes Tax and Tax AdministrationHoney OmosuraNoch keine Bewertungen

- Advance Taxation Fy 2076Dokument340 SeitenAdvance Taxation Fy 2076Anil ShahNoch keine Bewertungen

- VAT ExemptionDokument3 SeitenVAT ExemptionJusefNoch keine Bewertungen

- Our ServicesDokument2 SeitenOur ServicesJusefNoch keine Bewertungen

- Taxation 1 Carag SyllabusDokument4 SeitenTaxation 1 Carag SyllabusdiwalikhaNoch keine Bewertungen

- ARW Online Long Exam Part 3 PDFDokument12 SeitenARW Online Long Exam Part 3 PDFMansour HamjaNoch keine Bewertungen

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineVon EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNoch keine Bewertungen

- A Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionVon EverandA Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionNoch keine Bewertungen

- PS 2 Additions in UnitsDokument1 SeitePS 2 Additions in UnitsKelvin CulajaráNoch keine Bewertungen

- PS 1 Process Costing Answer KeyDokument56 SeitenPS 1 Process Costing Answer KeyKelvin CulajaráNoch keine Bewertungen

- PS 1Dokument2 SeitenPS 1Kelvin CulajaráNoch keine Bewertungen

- Module 1 - Cost Concept and Terminology - With AnswersDokument21 SeitenModule 1 - Cost Concept and Terminology - With AnswersKelvin CulajaráNoch keine Bewertungen

- Assignment 3: Spoilage in Weighted Average and FIFO Cost Flow MethodDokument3 SeitenAssignment 3: Spoilage in Weighted Average and FIFO Cost Flow MethodKelvin CulajaráNoch keine Bewertungen

- Transpo Actions and DamagesDokument17 SeitenTranspo Actions and DamagesKelvin CulajaráNoch keine Bewertungen

- Succession Law Case ProblemsDokument2 SeitenSuccession Law Case ProblemsKelvin CulajaráNoch keine Bewertungen

- 3 Estate Tax, Part 2Dokument3 Seiten3 Estate Tax, Part 2Kelvin CulajaráNoch keine Bewertungen

- Module 2 - Cost Behavior and Estimation - With AnswersDokument6 SeitenModule 2 - Cost Behavior and Estimation - With AnswersKelvin CulajaráNoch keine Bewertungen

- Corporation Code of The Philippines Finals Reviewer Pt. 1Dokument37 SeitenCorporation Code of The Philippines Finals Reviewer Pt. 1Kelvin CulajaráNoch keine Bewertungen

- Corporation Code Diagram ReviewerDokument2 SeitenCorporation Code Diagram ReviewerKelvin CulajaráNoch keine Bewertungen

- Constitutional Law Ii and Criminal ProcedureDokument5 SeitenConstitutional Law Ii and Criminal ProcedureKelvin CulajaráNoch keine Bewertungen

- 9 Secrecy of Bank Deposits LawDokument3 Seiten9 Secrecy of Bank Deposits LawKelvin CulajaráNoch keine Bewertungen

- 7 Negotiable InstrumentsDokument11 Seiten7 Negotiable InstrumentsKelvin CulajaráNoch keine Bewertungen

- 8 Batas Pambansa Blg. 22 and EstafaDokument2 Seiten8 Batas Pambansa Blg. 22 and EstafaKelvin CulajaráNoch keine Bewertungen

- 2 Estate Tax, Part 1Dokument9 Seiten2 Estate Tax, Part 1Kelvin CulajaráNoch keine Bewertungen

- 5 Real Estate MortgageDokument5 Seiten5 Real Estate MortgageKelvin CulajaráNoch keine Bewertungen

- Civil Procedure Annotation ReviewerDokument7 SeitenCivil Procedure Annotation ReviewerKelvin CulajaráNoch keine Bewertungen

- Guevarra vs. EalaDokument5 SeitenGuevarra vs. EalaKelvin CulajaráNoch keine Bewertungen

- 1 General PrinciplesDokument7 Seiten1 General PrinciplesKelvin CulajaráNoch keine Bewertungen

- LEC 2 Additions, Spoilage, Rework, and ScrapDokument37 SeitenLEC 2 Additions, Spoilage, Rework, and ScrapKelvin CulajaráNoch keine Bewertungen

- RA 7942 ReportDokument4 SeitenRA 7942 ReportKelvin CulajaráNoch keine Bewertungen

- LEC 5.2 Standard Costing and Variance AnalysisDokument32 SeitenLEC 5.2 Standard Costing and Variance AnalysisKelvin Culajará100% (1)

- Main Point:: Trillanes V. Castillo-Marigomen G.R. NO. 223451, MARCH 14, 2018Dokument13 SeitenMain Point:: Trillanes V. Castillo-Marigomen G.R. NO. 223451, MARCH 14, 2018Kelvin CulajaráNoch keine Bewertungen

- Linsangan vs. TolentinoDokument2 SeitenLinsangan vs. TolentinoKelvin CulajaráNoch keine Bewertungen

- Financial Reporting For Non-Profit OrganizationsDokument46 SeitenFinancial Reporting For Non-Profit OrganizationsKelvin CulajaráNoch keine Bewertungen

- LEC 3 Joint and By-Product CostingDokument11 SeitenLEC 3 Joint and By-Product CostingKelvin CulajaráNoch keine Bewertungen

- The Philippine Mining Act of 1995Dokument9 SeitenThe Philippine Mining Act of 1995Kelvin CulajaráNoch keine Bewertungen

- LEC 5 Standard Costing and Variance AnalysisDokument33 SeitenLEC 5 Standard Costing and Variance AnalysisKelvin CulajaráNoch keine Bewertungen

- Cagayan State University Aparri, Cagayan: Preliminary Examination - Transfer and Business Tax IDokument3 SeitenCagayan State University Aparri, Cagayan: Preliminary Examination - Transfer and Business Tax IJenelyn BeltranNoch keine Bewertungen

- Avenue E-Commerce Limited: 00009595951004031712 Crate IdDokument2 SeitenAvenue E-Commerce Limited: 00009595951004031712 Crate IdAbhishek LodhaNoch keine Bewertungen

- Accounting VoucherDokument1 SeiteAccounting VoucherDaksh BavawalaNoch keine Bewertungen

- Example of Excel-PayrollDokument1 SeiteExample of Excel-PayrollXia SolanoNoch keine Bewertungen

- Professor Jose Gabilondo Federal Income Tax Florida International University College of LawDokument89 SeitenProfessor Jose Gabilondo Federal Income Tax Florida International University College of Lawjfeyg100% (1)

- TXT %/L - V: Subject To ofDokument1 SeiteTXT %/L - V: Subject To ofCarlu YooNoch keine Bewertungen

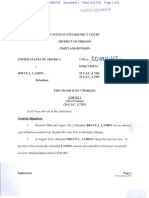

- US v. Lamon Indictment PDFDokument6 SeitenUS v. Lamon Indictment PDFAaron BrecherNoch keine Bewertungen

- Siyona Cost SheetDokument4 SeitenSiyona Cost SheetsharmaabhayNoch keine Bewertungen

- SalarySlip 1 - 2023Dokument1 SeiteSalarySlip 1 - 2023Rizham IbniNoch keine Bewertungen

- OLA A Ramesh: Fare Breakup Tax BreakupDokument1 SeiteOLA A Ramesh: Fare Breakup Tax Breakupsasenthil243640Noch keine Bewertungen

- Wa0094 PDFDokument1 SeiteWa0094 PDFBalraj BawaNoch keine Bewertungen

- Diversion of IncomeDokument11 SeitenDiversion of IncomeSrivathsan NambiraghavanNoch keine Bewertungen

- Form No. Requirement Deadline For Manual FilersDokument1 SeiteForm No. Requirement Deadline For Manual FilersLhyraNoch keine Bewertungen

- Tax Invoice: MR - Selvam Chennai State Name: Tamil Nadu, Code: 33Dokument1 SeiteTax Invoice: MR - Selvam Chennai State Name: Tamil Nadu, Code: 33Poornima PalanisamyNoch keine Bewertungen

- Tutorial 3 (Q)Dokument4 SeitenTutorial 3 (Q)szh saNoch keine Bewertungen

- Filipinas Synthetic Fiber Corporation V CADokument2 SeitenFilipinas Synthetic Fiber Corporation V CACedrick TanNoch keine Bewertungen

- Hesco Online Bill PDFDokument1 SeiteHesco Online Bill PDFBLACK SQUADNoch keine Bewertungen

- Chapter 7&8 ProblemsDokument5 SeitenChapter 7&8 ProblemsAngeline Aquino LaroaNoch keine Bewertungen

- Onett Developer TemplateDokument6 SeitenOnett Developer Templatejoeye louieNoch keine Bewertungen

- Wage and Income - THOM - 102746942918Dokument12 SeitenWage and Income - THOM - 102746942918Mark ThomasNoch keine Bewertungen

- Notice: Agency Information Collection Activities Proposals, Submissions, and ApprovalsDokument6 SeitenNotice: Agency Information Collection Activities Proposals, Submissions, and ApprovalsJustia.comNoch keine Bewertungen

- Capital Allowance 1. Condition To Get The Capital AllowanceDokument2 SeitenCapital Allowance 1. Condition To Get The Capital AllowanceDilah PhsNoch keine Bewertungen

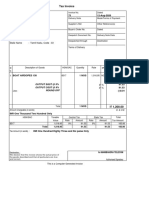

- Kenny Delight Inv 375 30 KGS PistaDokument2 SeitenKenny Delight Inv 375 30 KGS Pistavinay sainiNoch keine Bewertungen

- Benefits of Wage Earner, Taxable and Non-Taxable BenefitsDokument33 SeitenBenefits of Wage Earner, Taxable and Non-Taxable BenefitsCassandra Dianne Ferolino MacadoNoch keine Bewertungen

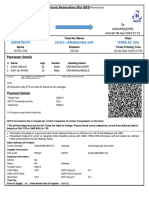

- Tirumala Tirupati Devasthanams (Official Booking Portal)Dokument1 SeiteTirumala Tirupati Devasthanams (Official Booking Portal)Chb RamasasthryNoch keine Bewertungen

- Tez Ticket PrintDokument1 SeiteTez Ticket Printosama amjad.hy8ggNoch keine Bewertungen

- Basic Appraisal For Real Estate BrokersDokument12 SeitenBasic Appraisal For Real Estate BrokersElannie CabatbatNoch keine Bewertungen

- Prelim TaskDokument4 SeitenPrelim TaskJohn Francis RosasNoch keine Bewertungen

- IRS Stimulus ChecksDokument1 SeiteIRS Stimulus Checkszaitrimairuv399Noch keine Bewertungen

- Tax Invoice Eureka Forbes Limited: Original For RecipientDokument2 SeitenTax Invoice Eureka Forbes Limited: Original For RecipientNilanjan GhoshNoch keine Bewertungen