Das könnte Ihnen auch gefallen

- Schaum's Outline of Principles of Accounting I, Fifth EditionVon EverandSchaum's Outline of Principles of Accounting I, Fifth EditionBewertung: 5 von 5 Sternen5/5 (3)

- Control Account Class QuestionDokument3 SeitenControl Account Class QuestionAbdulqadir MalindiwallaNoch keine Bewertungen

- A Comparative Analysis of Tax Administration in Asia and the Pacific: 2020 EditionVon EverandA Comparative Analysis of Tax Administration in Asia and the Pacific: 2020 EditionNoch keine Bewertungen

- Institute of Business Management: Lms Based Finalexaminations-Summer 2020 Analytical PartDokument3 SeitenInstitute of Business Management: Lms Based Finalexaminations-Summer 2020 Analytical PartSafi SheikhNoch keine Bewertungen

- Computerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionVon EverandComputerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionNoch keine Bewertungen

- Accounting document analysisDokument3 SeitenAccounting document analysisRazib Das RaazNoch keine Bewertungen

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineVon EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNoch keine Bewertungen

- Accounting Practice QuestionsDokument17 SeitenAccounting Practice QuestionsJanhvi AroraNoch keine Bewertungen

- Corporate Accounting Ii-1Dokument4 SeitenCorporate Accounting Ii-1ARAVIND V KNoch keine Bewertungen

- Accounts Solution Mock 2 12-11Dokument21 SeitenAccounts Solution Mock 2 12-11Foundation Group tuitionNoch keine Bewertungen

- 2019 7005 3C Financial AccountingDokument4 Seiten2019 7005 3C Financial AccountingGERALD ANGYENoch keine Bewertungen

- 4 CO4CRT11 - Corporate Accounting II (T) (1)Dokument5 Seiten4 CO4CRT11 - Corporate Accounting II (T) (1)emildaraisonNoch keine Bewertungen

- Preparing Financial StatementsDokument14 SeitenPreparing Financial StatementsAUDITOR97Noch keine Bewertungen

- May 2016 Professional Examination Financial Accounting (1.1) Examiner'S Report, Questions and Marking SchemeDokument24 SeitenMay 2016 Professional Examination Financial Accounting (1.1) Examiner'S Report, Questions and Marking SchemeMartn Carldazo DrogbaNoch keine Bewertungen

- (CBCS) (Repeaters) Commerce Paper - 3.5: Accounting For Specialised InstitutionsDokument4 Seiten(CBCS) (Repeaters) Commerce Paper - 3.5: Accounting For Specialised InstitutionsSanaullah M SultanpurNoch keine Bewertungen

- 3Dokument4 Seiten3shahisonal02Noch keine Bewertungen

- Accounts Mega ModelDokument8 SeitenAccounts Mega Modellekha ram100% (1)

- CA Foundation Accounts A MTP 2 June 2023Dokument12 SeitenCA Foundation Accounts A MTP 2 June 2023Vranda RastogiNoch keine Bewertungen

- FARAP-4518Dokument3 SeitenFARAP-4518Accounting StuffNoch keine Bewertungen

- Bcoc-131: Financial Accounting Tutor Marked AssignmentDokument17 SeitenBcoc-131: Financial Accounting Tutor Marked AssignmentRajni KumariNoch keine Bewertungen

- Practice Questions FADokument13 SeitenPractice Questions FApeacegracie140% (1)

- F&A Level II (Paper B)Dokument6 SeitenF&A Level II (Paper B)almmohamed294Noch keine Bewertungen

- Chapter 1 - Correction of ErrorsDokument3 SeitenChapter 1 - Correction of ErrorsHairizal Harun100% (1)

- FYJC Book Keeping and Accuntancy Topic Final AccountDokument4 SeitenFYJC Book Keeping and Accuntancy Topic Final AccountRavichandraNoch keine Bewertungen

- PDF Midterm Exam Ast With Answers CompressDokument15 SeitenPDF Midterm Exam Ast With Answers CompressSarah Del RosarioNoch keine Bewertungen

- PSBA A.R. Handout SolvedDokument13 SeitenPSBA A.R. Handout SolvedMikka100% (2)

- Accounts Receivable Chapter 4 Study GuideDokument4 SeitenAccounts Receivable Chapter 4 Study GuideSano ManjiroNoch keine Bewertungen

- By: Vinit Mishra Sir: Ca IntermediateDokument128 SeitenBy: Vinit Mishra Sir: Ca IntermediategimNoch keine Bewertungen

- Final Account WorksheetDokument4 SeitenFinal Account Worksheetravikumarbadass0Noch keine Bewertungen

- Model-Financial Accounting - Set1 - CZ21ADokument4 SeitenModel-Financial Accounting - Set1 - CZ21AJuli SunNoch keine Bewertungen

- Recording Business Transactions: Student Name Student ID Course ID DateDokument8 SeitenRecording Business Transactions: Student Name Student ID Course ID DateSami Ur RehmanNoch keine Bewertungen

- +1 Accountancy ONLINE Final Examination 2021Dokument5 Seiten+1 Accountancy ONLINE Final Examination 2021Rajwinder BansalNoch keine Bewertungen

- RT and Co. Basic Accounting Wizard EasyDokument12 SeitenRT and Co. Basic Accounting Wizard EasyJoseph SalidoNoch keine Bewertungen

- Answer On AccountingDokument6 SeitenAnswer On AccountingShahid MahmudNoch keine Bewertungen

- Contentitemfile Clakzwt9mx9sk0a212lma0ytv PDFDokument4 SeitenContentitemfile Clakzwt9mx9sk0a212lma0ytv PDFJoseph OndariNoch keine Bewertungen

- Accountancy - 2020 - Set - 8Dokument34 SeitenAccountancy - 2020 - Set - 8Saurav PandeyNoch keine Bewertungen

- 2009 S3 Ase2007Dokument15 Seiten2009 S3 Ase2007May CcmNoch keine Bewertungen

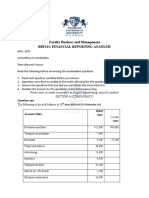

- Faculty Business and Management Bbf211: Financial Reporting AnanlsisDokument7 SeitenFaculty Business and Management Bbf211: Financial Reporting AnanlsisMichael AronNoch keine Bewertungen

- Mca Accounts Model QuestionDokument2 SeitenMca Accounts Model QuestionAnonymous 1ClGHbiT0JNoch keine Bewertungen

- Financial Accounting Control AccountsDokument4 SeitenFinancial Accounting Control AccountsKubenderarubban BalachantharNoch keine Bewertungen

- Financial Accounting AssignentDokument8 SeitenFinancial Accounting AssignentHitesh LodayaNoch keine Bewertungen

- Solution AldineDokument8 SeitenSolution AldineAkshay TulshyanNoch keine Bewertungen

- Group Assignment On Fundamentals of Accounting IDokument6 SeitenGroup Assignment On Fundamentals of Accounting IKaleab ShimelsNoch keine Bewertungen

- AfB1 Tutorial Questions For Week 3Dokument3 SeitenAfB1 Tutorial Questions For Week 3zhaok0610Noch keine Bewertungen

- Financial Accounting and Reporting Iii (Reviewer) : Name: Date: Professor: Section: ScoreDokument18 SeitenFinancial Accounting and Reporting Iii (Reviewer) : Name: Date: Professor: Section: ScoreAnirban Roy ChowdhuryNoch keine Bewertungen

- Problem Solving 1-4Dokument11 SeitenProblem Solving 1-4Romina LopezNoch keine Bewertungen

- Financial Accounting and Reporting ReviewDokument17 SeitenFinancial Accounting and Reporting ReviewAnonymousWriter34870% (10)

- Date Debit Note No. Name of Supplier L.F. Amount: © The Institute of Chartered Accountants of IndiaDokument9 SeitenDate Debit Note No. Name of Supplier L.F. Amount: © The Institute of Chartered Accountants of IndiaShubham PadolNoch keine Bewertungen

- Financial Accounting and Reporting Iii (Reviewer) : Name: Date: Professor: Section: ScoreDokument16 SeitenFinancial Accounting and Reporting Iii (Reviewer) : Name: Date: Professor: Section: ScoreShane TorrieNoch keine Bewertungen

- CBM 514-3 Question 3Dokument3 SeitenCBM 514-3 Question 3hafsamohmd793Noch keine Bewertungen

- B. Com I All PapersnDokument14 SeitenB. Com I All Papersnrahim Abbas aliNoch keine Bewertungen

- Partnership QsDokument3 SeitenPartnership QsJAYARAJALAKSHMI IlangoNoch keine Bewertungen

- Advanced Taxation QuestionsDokument7 SeitenAdvanced Taxation QuestionsObeng CliffNoch keine Bewertungen

- Test 5 Solutions AccountsDokument9 SeitenTest 5 Solutions AccountsVijayasri KumaravelNoch keine Bewertungen

- Frq-Acc-Grade 11-Set 05Dokument3 SeitenFrq-Acc-Grade 11-Set 05itzmellowteaNoch keine Bewertungen

- MBA Accounting Exam: Multiple Choice, Journal Entries, Ratios & DepreciationDokument3 SeitenMBA Accounting Exam: Multiple Choice, Journal Entries, Ratios & DepreciationPacific TigerNoch keine Bewertungen

- Departmental Profits After Manager CommissionDokument29 SeitenDepartmental Profits After Manager CommissionbinuNoch keine Bewertungen

- Accounting policies and bank reconciliationDokument5 SeitenAccounting policies and bank reconciliationHorace IvanNoch keine Bewertungen

- ACCA Pilot Paper Int PPQDokument19 SeitenACCA Pilot Paper Int PPQqaisar1982Noch keine Bewertungen

- BJL 4109 - Public Relations, Society and Culture CAT - FinalDokument13 SeitenBJL 4109 - Public Relations, Society and Culture CAT - FinalCy RusNoch keine Bewertungen

- Bit4201 Mobile Computing CatDokument5 SeitenBit4201 Mobile Computing CatCy RusNoch keine Bewertungen

- MKU BBM Principles of Marketing Course OverviewDokument13 SeitenMKU BBM Principles of Marketing Course OverviewCy RusNoch keine Bewertungen

- Baf1101 CatDokument7 SeitenBaf1101 CatCy RusNoch keine Bewertungen

- BBM 1101Dokument11 SeitenBBM 1101Cy RusNoch keine Bewertungen

- Mount Kenya University Business Statistics IIDokument9 SeitenMount Kenya University Business Statistics IICy RusNoch keine Bewertungen

- Fa IiDokument3 SeitenFa IiCy RusNoch keine Bewertungen

- Materi Ace Hardware 1Dokument47 SeitenMateri Ace Hardware 1250587Noch keine Bewertungen

- HVS - HVS-Anarock-India-Hospitality-Industry-Review-2018Dokument18 SeitenHVS - HVS-Anarock-India-Hospitality-Industry-Review-2018Vinod PatelNoch keine Bewertungen

- Genuine Agrarian Reform Program Vs Comprehensive Agrarian Reform ProgramDokument6 SeitenGenuine Agrarian Reform Program Vs Comprehensive Agrarian Reform ProgramYeyen M. EvoraNoch keine Bewertungen

- Eligibility Criteria OTE & GTEDokument1 SeiteEligibility Criteria OTE & GTEnoopsNoch keine Bewertungen

- Bank Comfort Letter SampleDokument1 SeiteBank Comfort Letter SampleSunar Anom Arya Ganda100% (1)

- Earn Profits: "Goodwill Is Nothing More Than The Probability That The Old Customer Will Resort To The Old Place."Dokument4 SeitenEarn Profits: "Goodwill Is Nothing More Than The Probability That The Old Customer Will Resort To The Old Place."MayurRawoolNoch keine Bewertungen

- TMEICDokument2 SeitenTMEICGunjan KhutNoch keine Bewertungen

- 911 Social Security Death Index, Tail Numbers, Daniel Lewin, Flight 77Dokument44 Seiten911 Social Security Death Index, Tail Numbers, Daniel Lewin, Flight 77anonymou5100% (1)

- BEL 36 X 10 KVA Oct19 PDFDokument10 SeitenBEL 36 X 10 KVA Oct19 PDFShyamNoch keine Bewertungen

- LSSGB - Project 3 - Improving Bank Call Center Operations - ProblemDokument7 SeitenLSSGB - Project 3 - Improving Bank Call Center Operations - ProblemKhyle Laurenz Duro17% (6)

- Zachary Lewis ResumeDokument1 SeiteZachary Lewis Resumeapi-268735873Noch keine Bewertungen

- Accounting Postulates, Concepts and PrinciplesDokument4 SeitenAccounting Postulates, Concepts and PrinciplesKkaran ShethNoch keine Bewertungen

- Resource Levelling RulesDokument17 SeitenResource Levelling Rulesreno100% (1)

- 3 - Analysis of Financial Statements 2Dokument2 Seiten3 - Analysis of Financial Statements 2Axce1996Noch keine Bewertungen

- Economics Problems PDFDokument31 SeitenEconomics Problems PDFev xvNoch keine Bewertungen

- Rule Based-Principal BasedDokument10 SeitenRule Based-Principal BasedYuri AnnisaNoch keine Bewertungen

- General Terms Conditions For Goods Purchase-Sale ContractDokument3 SeitenGeneral Terms Conditions For Goods Purchase-Sale ContractBelal AhmadNoch keine Bewertungen

- R12 Trading CommunityDokument6 SeitenR12 Trading Communitymani@pfizerNoch keine Bewertungen

- Customer Acceptance Order Management R12Dokument5 SeitenCustomer Acceptance Order Management R12Naveen Shankar MauwalaNoch keine Bewertungen

- MASTER IN MANAGEMENT AT HEC PARISDokument7 SeitenMASTER IN MANAGEMENT AT HEC PARISabhay chaudharyNoch keine Bewertungen

- FAC3702 Question Bank 2015Dokument105 SeitenFAC3702 Question Bank 2015Itumeleng KekanaNoch keine Bewertungen

- 1b. Sustainment Unit Capability PE - Available Sustainment Units (v1)Dokument2 Seiten1b. Sustainment Unit Capability PE - Available Sustainment Units (v1)Steve RichardsNoch keine Bewertungen

- Importance of Strategic and Tactical Planning for Organizational SuccessDokument5 SeitenImportance of Strategic and Tactical Planning for Organizational SuccessAman KumarNoch keine Bewertungen

- RBC CaseAnswers Group13Dokument4 SeitenRBC CaseAnswers Group13Shikha Gupta100% (1)

- Project Quality Plan - 039700 REV D ONLY (5868)Dokument42 SeitenProject Quality Plan - 039700 REV D ONLY (5868)JaseelKanhirathinkal100% (1)

- Lit ReviewDokument15 SeitenLit Reviewapi-385119016Noch keine Bewertungen

- Nishant Bhaskar PortfolioDokument9 SeitenNishant Bhaskar PortfolioN. BhaskarNoch keine Bewertungen

- Atswa Cost AccountingDokument504 SeitenAtswa Cost AccountingIbrahim MuyeNoch keine Bewertungen

- Promethean Insulation Technology v. Energy Efficient SolutionsDokument22 SeitenPromethean Insulation Technology v. Energy Efficient SolutionsPriorSmartNoch keine Bewertungen

- Marketing StrtegiesDokument10 SeitenMarketing StrtegieshaseebNoch keine Bewertungen