Das könnte Ihnen auch gefallen

- Hedging Foreign Exchange Risk with Forwards and OptionsDokument2 SeitenHedging Foreign Exchange Risk with Forwards and OptionsPrethivi RajNoch keine Bewertungen

- Derivados-Ejercicios Resueltos 1Dokument8 SeitenDerivados-Ejercicios Resueltos 1patriciaNoch keine Bewertungen

- Companies Swap Rates to Match NeedsDokument4 SeitenCompanies Swap Rates to Match NeedsHana LeeNoch keine Bewertungen

- KLCI Futures Contracts AnalysisDokument63 SeitenKLCI Futures Contracts AnalysisSidharth ChoudharyNoch keine Bewertungen

- BF - 307: Derivative Securities January 19, 2012 Homework Assignment 1 Suman Banerjee InstructionsDokument3 SeitenBF - 307: Derivative Securities January 19, 2012 Homework Assignment 1 Suman Banerjee Instructionssamurai_87Noch keine Bewertungen

- Nanyang Business School AB1201 Financial Management Tutorial 5: Risk and Rates of Return (Common Questions)Dokument3 SeitenNanyang Business School AB1201 Financial Management Tutorial 5: Risk and Rates of Return (Common Questions)asdsadsaNoch keine Bewertungen

- Time Value of MoneyDokument10 SeitenTime Value of MoneyAbasi masoudNoch keine Bewertungen

- Summer 2021 FIN 6055 New Test 2Dokument2 SeitenSummer 2021 FIN 6055 New Test 2Michael Pirone0% (1)

- Calculate China's foreign exchange intervention and sterilizationDokument5 SeitenCalculate China's foreign exchange intervention and sterilizationFagbola Oluwatobi OmolajaNoch keine Bewertungen

- MBFinance Chap06-Pbms-finalDokument20 SeitenMBFinance Chap06-Pbms-finalLinda YuNoch keine Bewertungen

- Chapter 12 SolutionsDokument11 SeitenChapter 12 SolutionsEdmond ZNoch keine Bewertungen

- Examples WACC Project RiskDokument4 SeitenExamples WACC Project Risk979044775Noch keine Bewertungen

- Tutorial 5 Exercises TemplateDokument17 SeitenTutorial 5 Exercises TemplateHà VânNoch keine Bewertungen

- Chapter 11: Forward and Futures Hedging, Spread, and Target StrategiesDokument9 SeitenChapter 11: Forward and Futures Hedging, Spread, and Target StrategiesNam MaiNoch keine Bewertungen

- COMM 324 A4 SolutionsDokument6 SeitenCOMM 324 A4 SolutionsdorianNoch keine Bewertungen

- Practice MC - Exam PDFDokument72 SeitenPractice MC - Exam PDFChanduNoch keine Bewertungen

- Chapter 06: Dividend Decision: ................ Md. Jobayair Ibna Rafiq.............Dokument62 SeitenChapter 06: Dividend Decision: ................ Md. Jobayair Ibna Rafiq.............Mohammad Salim Hossain0% (1)

- BFC5935 - Tutorial 9 SolutionsDokument6 SeitenBFC5935 - Tutorial 9 SolutionsXue XuNoch keine Bewertungen

- Chapter 9Dokument7 SeitenChapter 9sylbluebubblesNoch keine Bewertungen

- OFOD7 e Test Bank CH 03Dokument2 SeitenOFOD7 e Test Bank CH 03Danny NgNoch keine Bewertungen

- Bus 322 Tutorial 5-SolutionDokument20 SeitenBus 322 Tutorial 5-Solutionbvni50% (2)

- Spring03 Final SolutionDokument14 SeitenSpring03 Final SolutionrgrtNoch keine Bewertungen

- Min-Variance Portfolio & Optimal Risky PortfolioDokument4 SeitenMin-Variance Portfolio & Optimal Risky PortfolioHelen B. EvansNoch keine Bewertungen

- Week 2 Tutorial QuestionsDokument4 SeitenWeek 2 Tutorial QuestionsWOP INVESTNoch keine Bewertungen

- IfDokument14 SeitenIfĐặng Thuỳ HươngNoch keine Bewertungen

- Practice Questions: Problem 1.1Dokument6 SeitenPractice Questions: Problem 1.1Chekralla HannaNoch keine Bewertungen

- Assignment 8 AnswersDokument6 SeitenAssignment 8 AnswersMyaNoch keine Bewertungen

- Bbmf3123 International Finance: Mds-Wealth-Shrinks-Over-Rm1b-Paper-After-Audit-IssuesDokument8 SeitenBbmf3123 International Finance: Mds-Wealth-Shrinks-Over-Rm1b-Paper-After-Audit-IssuesSharon ChinNoch keine Bewertungen

- Econ 132 Problems For Chapter 1-3, and 5Dokument5 SeitenEcon 132 Problems For Chapter 1-3, and 5jononfireNoch keine Bewertungen

- J CFM StudyText Chapter 6 PDFDokument16 SeitenJ CFM StudyText Chapter 6 PDFgizzarNoch keine Bewertungen

- Week 4 Tutorial QuestionsDokument2 SeitenWeek 4 Tutorial QuestionsThomas Kong Ying LiNoch keine Bewertungen

- OPT SolutionDokument52 SeitenOPT SolutionbocfetNoch keine Bewertungen

- Chapter 4Dokument14 SeitenChapter 4Selena JungNoch keine Bewertungen

- Chapter4 (Money and Banking)Dokument2 SeitenChapter4 (Money and Banking)ibraheemNoch keine Bewertungen

- Past Exam Questions - InvestmentDokument14 SeitenPast Exam Questions - InvestmentTalia simonNoch keine Bewertungen

- Jun 2005 - Qns Mod BDokument14 SeitenJun 2005 - Qns Mod BHubbak KhanNoch keine Bewertungen

- Lesson Five HomeworkDokument3 SeitenLesson Five HomeworkLiam100% (1)

- Tutorial 6 - TRMDokument9 SeitenTutorial 6 - TRMHằngg ĐỗNoch keine Bewertungen

- 2.BMMF5103 - EQ Formattedl May 2012Dokument7 Seiten2.BMMF5103 - EQ Formattedl May 2012thaingtNoch keine Bewertungen

- Case 78, "Beatrice Peabody"Dokument8 SeitenCase 78, "Beatrice Peabody"seethurya0% (1)

- Chapter 13 - Class Notes PDFDokument33 SeitenChapter 13 - Class Notes PDFJilynn SeahNoch keine Bewertungen

- Ch8 Practice ProblemsDokument5 SeitenCh8 Practice Problemsvandung19Noch keine Bewertungen

- CH 11 HW SolutionsDokument9 SeitenCH 11 HW SolutionsAriefka Sari DewiNoch keine Bewertungen

- Chapter 11Dokument2 SeitenChapter 11atuanaini0% (1)

- Transaction Exposure Chapter 11Dokument57 SeitenTransaction Exposure Chapter 11armando.chappell1005Noch keine Bewertungen

- Topic G ExercisesDokument8 SeitenTopic G ExercisesAustin Joseph100% (1)

- Swaps Cms CMTDokument7 SeitenSwaps Cms CMTmarketfolly.comNoch keine Bewertungen

- TM Tut 13 Credit Derivatives Revision PDFDokument5 SeitenTM Tut 13 Credit Derivatives Revision PDFQuynh Ngoc DangNoch keine Bewertungen

- Fm202 Exam Questions 2013Dokument12 SeitenFm202 Exam Questions 2013Grace VersoniNoch keine Bewertungen

- MID-TERM REVIEW TIPS AND PRACTICEDokument29 SeitenMID-TERM REVIEW TIPS AND PRACTICEChou mỡNoch keine Bewertungen

- Week 8 Class ExercisesDokument3 SeitenWeek 8 Class ExercisesChinhoong Ong100% (1)

- Chapter 3 - Tutorial - With Solutions 2023Dokument34 SeitenChapter 3 - Tutorial - With Solutions 2023Jared Herber100% (1)

- First National Bank interest rate risk analysisDokument4 SeitenFirst National Bank interest rate risk analysisRoohani WadhwaNoch keine Bewertungen

- Forecasting of Financial StatementsDokument9 SeitenForecasting of Financial StatementssamaanNoch keine Bewertungen

- Calculate Present and Future Values of Cash Flows Using Discounting and CompoundingDokument4 SeitenCalculate Present and Future Values of Cash Flows Using Discounting and CompoundingKritika SrivastavaNoch keine Bewertungen

- Solutions Topic4Dokument4 SeitenSolutions Topic4Thirusha balamuraliNoch keine Bewertungen

- Commercial Bank Management Midsem NotesDokument12 SeitenCommercial Bank Management Midsem NotesWinston WongNoch keine Bewertungen

- Week 4 Solutions To ExercisesDokument5 SeitenWeek 4 Solutions To ExercisesBerend van RoozendaalNoch keine Bewertungen

- Problem 1.35Dokument8 SeitenProblem 1.35zmm45x7sjtNoch keine Bewertungen

- 0417 Forward QuestionsDokument1 Seite0417 Forward QuestionsTạNgọcMaiNoch keine Bewertungen

- FIN 30013 - Assignment - Written ReportDokument5 SeitenFIN 30013 - Assignment - Written ReportAiyoo JessyNoch keine Bewertungen

- Aca AllDokument19 SeitenAca AllAiyoo JessyNoch keine Bewertungen

- A Report For Bright Lance LTDDokument2 SeitenA Report For Bright Lance LTDAiyoo JessyNoch keine Bewertungen

- Merry Bun 100063948: England, It Was Held That Confidentiality Was An Implied Term in The Customer'sDokument9 SeitenMerry Bun 100063948: England, It Was Held That Confidentiality Was An Implied Term in The Customer'sAiyoo JessyNoch keine Bewertungen

- Merry Bun 100063948: England, It Was Held That Confidentiality Was An Implied Term in The Customer'sDokument9 SeitenMerry Bun 100063948: England, It Was Held That Confidentiality Was An Implied Term in The Customer'sAiyoo JessyNoch keine Bewertungen

- FIDMDokument23 SeitenFIDMAiyoo JessyNoch keine Bewertungen

- Session 2 Portfolio AnalysisDokument33 SeitenSession 2 Portfolio Analysispvkoganti1Noch keine Bewertungen

- Pathway To Financial Success: Autonomy Through Financial Education in IndiaDokument15 SeitenPathway To Financial Success: Autonomy Through Financial Education in IndiaKirtyNoch keine Bewertungen

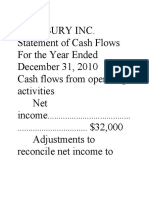

- Lansbury Inc cash flow analysisDokument10 SeitenLansbury Inc cash flow analysis/// MASTER DOGENoch keine Bewertungen

- Fin Heads-0212 From Nagesh VNDokument11 SeitenFin Heads-0212 From Nagesh VNDevanathan HbkNoch keine Bewertungen

- A Sukuk Is An Islamic Financial CertificateDokument11 SeitenA Sukuk Is An Islamic Financial CertificateAbbasi WritesNoch keine Bewertungen

- 2023 Global Market Outlook Full ReportDokument16 Seiten2023 Global Market Outlook Full ReportMimi KamilNoch keine Bewertungen

- Lemelson Capital Featured in HFMWeekDokument32 SeitenLemelson Capital Featured in HFMWeekamvona100% (1)

- Law Final GauriDokument10 SeitenLaw Final GauriPoonam KhondNoch keine Bewertungen

- Literature ReviewDokument13 SeitenLiterature ReviewSukhraj Kaur Chhina100% (5)

- Ambit - Strategy - ERr GRP - The Rebooting of IndiaDokument25 SeitenAmbit - Strategy - ERr GRP - The Rebooting of Indiaomkarb87Noch keine Bewertungen

- Chap 004Dokument24 SeitenChap 004Hiep LuuNoch keine Bewertungen

- B7110-001 Financial Statement Analysis and Valuation PDFDokument3 SeitenB7110-001 Financial Statement Analysis and Valuation PDFLittleBlondie0% (2)

- Titan Company 01 01 2023 KhanDokument8 SeitenTitan Company 01 01 2023 Khansaran21Noch keine Bewertungen

- Mutual Fund: An OverviewDokument54 SeitenMutual Fund: An Overviewnikitashah14Noch keine Bewertungen

- Liquidity RiskDokument24 SeitenLiquidity RiskTing YangNoch keine Bewertungen

- Blij - Back-Testing Magic - 2011Dokument63 SeitenBlij - Back-Testing Magic - 2011Jens GruNoch keine Bewertungen

- Financial Statements and Ratio AnalysisDokument81 SeitenFinancial Statements and Ratio AnalysisHattori HanzoNoch keine Bewertungen

- Marriott Cost of CapitalDokument3 SeitenMarriott Cost of Capitalanmolsaini01Noch keine Bewertungen

- Jonathan Barrett Resume - Harlem Link Charter School Board Application - Vol 2 of 3 - PG 431-432Dokument2 SeitenJonathan Barrett Resume - Harlem Link Charter School Board Application - Vol 2 of 3 - PG 431-432Fuzzy PandaNoch keine Bewertungen

- FIN 400 Midterm Review QuestionDokument4 SeitenFIN 400 Midterm Review Questionlinh trangNoch keine Bewertungen

- C14 External Loss FinancingDokument38 SeitenC14 External Loss FinancingPham Hong VanNoch keine Bewertungen

- How I Helped To Make Fischer Black Wealthier 1996Dokument5 SeitenHow I Helped To Make Fischer Black Wealthier 1996JTNoch keine Bewertungen

- Solved Mila Purchased A Zaffre Corporation 100 000 Bond 10 Years AgoDokument1 SeiteSolved Mila Purchased A Zaffre Corporation 100 000 Bond 10 Years AgoAnbu jaromiaNoch keine Bewertungen

- Basel Accords and Framework CombineDokument30 SeitenBasel Accords and Framework Combinelmmh100% (1)

- LVMH ModelDokument63 SeitenLVMH ModelJosé Manuel EstebanNoch keine Bewertungen

- For Classroom Discussion: SolutionDokument4 SeitenFor Classroom Discussion: SolutionMisherene MagpileNoch keine Bewertungen

- Stock Market ForecastingDokument10 SeitenStock Market ForecastingRui Isaac FernandoNoch keine Bewertungen

- Thesis Report - Highrise Constrxn PDFDokument108 SeitenThesis Report - Highrise Constrxn PDFNancy TessNoch keine Bewertungen

- SM ch10Dokument67 SeitenSM ch10Rendy KurniawanNoch keine Bewertungen

- Weath ManagementDokument116 SeitenWeath ManagementKalpeshNoch keine Bewertungen