Das könnte Ihnen auch gefallen

- Foundational Theories and Techniques for Risk Management, A Guide for Professional Risk Managers in Financial Services - Part II - Financial InstrumentsVon EverandFoundational Theories and Techniques for Risk Management, A Guide for Professional Risk Managers in Financial Services - Part II - Financial InstrumentsNoch keine Bewertungen

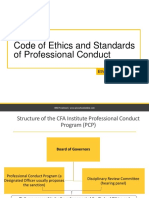

- Registered Prep Provider of CFA InstituteDokument18 SeitenRegistered Prep Provider of CFA InstituteSergiu CrisanNoch keine Bewertungen

- Accounting for Derivatives: Advanced Hedging under IFRSVon EverandAccounting for Derivatives: Advanced Hedging under IFRSNoch keine Bewertungen

- Usgaap, Igaap & IfrsDokument7 SeitenUsgaap, Igaap & IfrsdhangarsachinNoch keine Bewertungen

- Certified Risk Analyst A Complete Guide - 2020 EditionVon EverandCertified Risk Analyst A Complete Guide - 2020 EditionNoch keine Bewertungen

- FinQuiz - Curriculum Note, Study Session 2, Reading 5Dokument1 SeiteFinQuiz - Curriculum Note, Study Session 2, Reading 5Sankalp Jain0% (1)

- SERIES 24 EXAM STUDY GUIDE 2021 + TEST BANKVon EverandSERIES 24 EXAM STUDY GUIDE 2021 + TEST BANKNoch keine Bewertungen

- CFA Exercise With Solution - Chap 15Dokument5 SeitenCFA Exercise With Solution - Chap 15Fagbola Oluwatobi OmolajaNoch keine Bewertungen

- QM Learning Module: 1 The Time Value of Money: Nominal Risk-Free Rate Real Risk-Free Interest Rate +Dokument198 SeitenQM Learning Module: 1 The Time Value of Money: Nominal Risk-Free Rate Real Risk-Free Interest Rate +Xi Wei100% (2)

- Video Series CFA FRMDokument10 SeitenVideo Series CFA FRMShivgan JoshiNoch keine Bewertungen

- CFA Level II Mock Exam 5 - Solutions (AM)Dokument60 SeitenCFA Level II Mock Exam 5 - Solutions (AM)Sardonna FongNoch keine Bewertungen

- Level I Volume 5 2019 IFT NotesDokument258 SeitenLevel I Volume 5 2019 IFT NotesNoor QamarNoch keine Bewertungen

- CFA III-Performance Evaluation关键词清单Dokument9 SeitenCFA III-Performance Evaluation关键词清单Thanh NguyenNoch keine Bewertungen

- FRM Currency FutureDokument48 SeitenFRM Currency FutureParvez KhanNoch keine Bewertungen

- FRM NotesDokument13 SeitenFRM NotesNeeraj LowanshiNoch keine Bewertungen

- Cfa Level 1 LOS Command WordsDokument0 SeitenCfa Level 1 LOS Command WordsHummingbird11688Noch keine Bewertungen

- GARP FRM Practice Exam 2011 Level2Dokument63 SeitenGARP FRM Practice Exam 2011 Level2Kelvin TanNoch keine Bewertungen

- Level III: Taxes and Private Wealth Management in A Global ContextDokument29 SeitenLevel III: Taxes and Private Wealth Management in A Global ContextRayBrianCasazolaNoch keine Bewertungen

- FRM Essential FormulaeDokument1 SeiteFRM Essential FormulaeSiddhu SaiNoch keine Bewertungen

- CFA - L2 - Quicksheet Sample PDFDokument1 SeiteCFA - L2 - Quicksheet Sample PDFMohit PrasadNoch keine Bewertungen

- FRM Assignment 2Dokument7 SeitenFRM Assignment 2ALI REHMANNoch keine Bewertungen

- A-Plus Study Notes: CFA 2013 Level I CertificationDokument687 SeitenA-Plus Study Notes: CFA 2013 Level I CertificationNguyễn Quốc Thắng100% (1)

- CFA Level 1 ResultsDokument1 SeiteCFA Level 1 ResultsrecoNoch keine Bewertungen

- ACCA F9 Lecture 2Dokument37 SeitenACCA F9 Lecture 2Fathimath Azmath AliNoch keine Bewertungen

- CFA III-Asset Allocation关键词清单Dokument27 SeitenCFA III-Asset Allocation关键词清单Lê Chấn PhongNoch keine Bewertungen

- Ed - 16wchap07sln For 30 Jan 2018Dokument7 SeitenEd - 16wchap07sln For 30 Jan 2018MarinaNoch keine Bewertungen

- CFA Results - FinalDokument35 SeitenCFA Results - FinalJon doeNoch keine Bewertungen

- FRM Presentation 2Dokument20 SeitenFRM Presentation 2Paul BanerjeeNoch keine Bewertungen

- Financial Reporting For Financial Institutions MUTUAL FUNDS & NBFC'sDokument77 SeitenFinancial Reporting For Financial Institutions MUTUAL FUNDS & NBFC'sParvesh Aghi0% (1)

- R36 Evaluating Portfolio PerformanceDokument65 SeitenR36 Evaluating Portfolio PerformanceRayBrianCasazolaNoch keine Bewertungen

- Answer: eDokument17 SeitenAnswer: eMary Benedict AbraganNoch keine Bewertungen

- Samlpe Questions FMP FRM IDokument6 SeitenSamlpe Questions FMP FRM IShreyans Jain0% (1)

- R55 Understanding Fixed-Income Risk and Return Q BankDokument20 SeitenR55 Understanding Fixed-Income Risk and Return Q BankAhmedNoch keine Bewertungen

- Section A: Multiple Choice Questions - Single Option: This Section Has 70 Questions Worth 1 Mark Each (Total of 70 Marks)Dokument24 SeitenSection A: Multiple Choice Questions - Single Option: This Section Has 70 Questions Worth 1 Mark Each (Total of 70 Marks)Kenny HoNoch keine Bewertungen

- Session 7: Estimating Cash Flows: Aswath DamodaranDokument15 SeitenSession 7: Estimating Cash Flows: Aswath Damodaranthomas94josephNoch keine Bewertungen

- Cfa Level 1 EthicsDokument6 SeitenCfa Level 1 EthicsSurendra PandeyNoch keine Bewertungen

- 2016 CFA Level III ErrataDokument1 Seite2016 CFA Level III ErrataimvavNoch keine Bewertungen

- CFA Level II Formula Sheet CFA Level II Formula Sheet: Finance (Harvard University) Finance (Harvard University)Dokument5 SeitenCFA Level II Formula Sheet CFA Level II Formula Sheet: Finance (Harvard University) Finance (Harvard University)smith100% (1)

- SOA FM Sample Derivatives QuestionsDokument17 SeitenSOA FM Sample Derivatives QuestionsMonica MckinneyNoch keine Bewertungen

- 2011FRM金程模拟考题Dokument50 Seiten2011FRM金程模拟考题Liu ZhilinNoch keine Bewertungen

- L1.2011.garp Practice Questions & ErrataDokument76 SeitenL1.2011.garp Practice Questions & Erratabhabani34850% (2)

- 2016 FRM Part I Practice ExamDokument129 Seiten2016 FRM Part I Practice ExamSiddharth JainNoch keine Bewertungen

- Derivatives and Risk ManagementDokument30 SeitenDerivatives and Risk Managementkashan khanNoch keine Bewertungen

- Module 2Dokument12 SeitenModule 2zoyaNoch keine Bewertungen

- Cfa QuantsDokument102 SeitenCfa QuantsANASNoch keine Bewertungen

- Currency Exchange Rates: Determination and Forecasting: Presenter's Name Presenter's Title DD Month YyyyDokument39 SeitenCurrency Exchange Rates: Determination and Forecasting: Presenter's Name Presenter's Title DD Month YyyybingoNoch keine Bewertungen

- FinQuiz Level1Mock2016Version1JuneAMQuestions PDFDokument39 SeitenFinQuiz Level1Mock2016Version1JuneAMQuestions PDFAnimesh ChoubeyNoch keine Bewertungen

- 2014 Mock Exam - AM - QuestionDokument30 Seiten2014 Mock Exam - AM - Question12jdNoch keine Bewertungen

- Ap 3Dokument397 SeitenAp 3Ayush SharmaNoch keine Bewertungen

- FRM Part1Dokument1 SeiteFRM Part1Nimisha SharmaNoch keine Bewertungen

- FRM - Financial Risk Management: Overview of FRM ExamDokument2 SeitenFRM - Financial Risk Management: Overview of FRM ExamficochandNoch keine Bewertungen

- IIIrd Sem 2012 All Questionpapers in This Word FileDokument16 SeitenIIIrd Sem 2012 All Questionpapers in This Word FileAkhil RupaniNoch keine Bewertungen

- Fama MacbethDokument9 SeitenFama MacbethanishmenonNoch keine Bewertungen

- R01 Ethics and Trust in The Investment Profession: Instructor's NoteDokument26 SeitenR01 Ethics and Trust in The Investment Profession: Instructor's NoteMani ManandharNoch keine Bewertungen

- FinQuiz - Smart Summary - Study Session 15 - Reading 52Dokument5 SeitenFinQuiz - Smart Summary - Study Session 15 - Reading 52RafaelNoch keine Bewertungen

- Mock 1 - Afternoon - AnswersDokument27 SeitenMock 1 - Afternoon - Answerspagis31861Noch keine Bewertungen

- Empirical Studies in FinanceDokument8 SeitenEmpirical Studies in FinanceAhmedMalikNoch keine Bewertungen

- Cfa Level2 ExamDokument74 SeitenCfa Level2 ExamLynn Hollenbeck BreindelNoch keine Bewertungen

- March 2008 CAIA Level II Sample Questions: Chartered Alternative Investment AnalystDokument35 SeitenMarch 2008 CAIA Level II Sample Questions: Chartered Alternative Investment AnalystAnubhav Srivastava100% (1)

- Ion - Why Is It Necessary - How It WorksDokument7 SeitenIon - Why Is It Necessary - How It WorksPankaj D. DaniNoch keine Bewertungen

- Comparative Study of Financial Report of Three Indian Banks (IIMT) Project FileDokument95 SeitenComparative Study of Financial Report of Three Indian Banks (IIMT) Project Filedeepak GuptaNoch keine Bewertungen

- Chapter ThreeDokument19 SeitenChapter ThreeTULSI MAHANTO IPM 2020 -25 BatchNoch keine Bewertungen

- Elements of Typical LBO Operation: The First StageDokument8 SeitenElements of Typical LBO Operation: The First StageEmila DeyNoch keine Bewertungen

- Separate and Consolidated QuizDokument6 SeitenSeparate and Consolidated QuizAllyssa Kassandra LucesNoch keine Bewertungen

- Dwnload Full Fundamentals of Advanced Accounting 7th Edition Hoyle Solutions Manual PDFDokument35 SeitenDwnload Full Fundamentals of Advanced Accounting 7th Edition Hoyle Solutions Manual PDFjacobriceiv100% (4)

- Intacct3: Assignment Item #1: (JG Company)Dokument5 SeitenIntacct3: Assignment Item #1: (JG Company)Kristen StewartNoch keine Bewertungen

- Elective - I - 506 Financial Markets and Services (F)Dokument13 SeitenElective - I - 506 Financial Markets and Services (F)dominic wurdaNoch keine Bewertungen

- 1Z0-960 Exam QuestionsDokument7 Seiten1Z0-960 Exam QuestionsBill Hopes100% (1)

- Additional Case - Urban Chic DesignersDokument2 SeitenAdditional Case - Urban Chic DesignersNaman MantriNoch keine Bewertungen

- Audit and AssuranceDokument222 SeitenAudit and AssuranceQudsia ZulfiqarNoch keine Bewertungen

- Receivable Financing ReviewerDokument3 SeitenReceivable Financing ReviewerWinnie ToribioNoch keine Bewertungen

- SABB Signature Visa CC User Guide - Jan. 23Dokument29 SeitenSABB Signature Visa CC User Guide - Jan. 23amirNoch keine Bewertungen

- Financial Statement Analysis of Suzuki MotorsDokument21 SeitenFinancial Statement Analysis of Suzuki MotorsMuhammad AliNoch keine Bewertungen

- Eastern Bank Limited: Name: ID: American International University of Bangladesh Course Name: Faculty Name: Due DateDokument6 SeitenEastern Bank Limited: Name: ID: American International University of Bangladesh Course Name: Faculty Name: Due DateTasheen MahabubNoch keine Bewertungen

- 2023-10-28 Sub Prime Mortgage Crisis V0.02amDokument13 Seiten2023-10-28 Sub Prime Mortgage Crisis V0.02amb23036Noch keine Bewertungen

- UNIT 3 InsuranceDokument10 SeitenUNIT 3 InsuranceAroop PalNoch keine Bewertungen

- Govt. Securities Market in India: Presentation OnDokument19 SeitenGovt. Securities Market in India: Presentation OnHitesh PandeyNoch keine Bewertungen

- Arvind Kumar SoniDokument1 SeiteArvind Kumar SoniAngad MundraNoch keine Bewertungen

- Suncoast Bank StatementDokument3 SeitenSuncoast Bank StatementolaNoch keine Bewertungen

- A Summer Training Report On HDFC LifeDokument30 SeitenA Summer Training Report On HDFC LifeOwais LatiefNoch keine Bewertungen

- Your 9mobile Bill Statement: MR Kpanja MichaelDokument3 SeitenYour 9mobile Bill Statement: MR Kpanja MichaelSpikeNoch keine Bewertungen

- The Global EconomyDokument2 SeitenThe Global EconomyJean P.Noch keine Bewertungen

- Pointers (Notes) BankingDokument3 SeitenPointers (Notes) BankingGen GrajoNoch keine Bewertungen

- Public Sector Accounting AssignmentDokument9 SeitenPublic Sector Accounting AssignmentitulejamesNoch keine Bewertungen

- Osceola County Real Property Records Forensic ExaminationDokument759 SeitenOsceola County Real Property Records Forensic ExaminationStephen Dibert100% (2)

- Car FinanceDokument32 SeitenCar FinanceAshish V MeshramNoch keine Bewertungen

- Answer Key Quiz 1Dokument8 SeitenAnswer Key Quiz 1Shaira Mae ManalastasNoch keine Bewertungen

- Analysis of Indian Debt MarketDokument45 SeitenAnalysis of Indian Debt Marketmichelle_susan_dsa100% (1)

- 909Dokument2 Seiten909Kashif SiddiquiNoch keine Bewertungen

- When Are CountryWide Notes Endorsed and Excerpt of Deposition Transcript of SjolanderDokument18 SeitenWhen Are CountryWide Notes Endorsed and Excerpt of Deposition Transcript of Sjolander83jjmack100% (8)

- Beginning AutoCAD® 2022 Exercise Workbook: For Windows®Von EverandBeginning AutoCAD® 2022 Exercise Workbook: For Windows®Noch keine Bewertungen

- AutoCAD 2010 Tutorial Series: Drawing Dimensions, Elevations and SectionsVon EverandAutoCAD 2010 Tutorial Series: Drawing Dimensions, Elevations and SectionsNoch keine Bewertungen

- Autodesk Fusion 360: A Power Guide for Beginners and Intermediate Users (3rd Edition)Von EverandAutodesk Fusion 360: A Power Guide for Beginners and Intermediate Users (3rd Edition)Bewertung: 5 von 5 Sternen5/5 (2)

- From Vision to Version - Step by step guide for crafting and aligning your product vision, strategy and roadmap: Strategy Framework for Digital Product Management RockstarsVon EverandFrom Vision to Version - Step by step guide for crafting and aligning your product vision, strategy and roadmap: Strategy Framework for Digital Product Management RockstarsNoch keine Bewertungen

- SolidWorks 2015 Learn by doing-Part 1Von EverandSolidWorks 2015 Learn by doing-Part 1Bewertung: 4.5 von 5 Sternen4.5/5 (11)

- Certified Solidworks Professional Advanced Surface Modeling Exam PreparationVon EverandCertified Solidworks Professional Advanced Surface Modeling Exam PreparationBewertung: 5 von 5 Sternen5/5 (1)