Das könnte Ihnen auch gefallen

- Pre Week - Torts. Tababa 1008 - RevisedDokument8 SeitenPre Week - Torts. Tababa 1008 - RevisedMarielle SantiagoNoch keine Bewertungen

- Pre Week - TortsDokument6 SeitenPre Week - TortsMarielle SantiagoNoch keine Bewertungen

- Remedies: Procedural Requirements Related To DelinquencyDokument13 SeitenRemedies: Procedural Requirements Related To DelinquencyMarielle SantiagoNoch keine Bewertungen

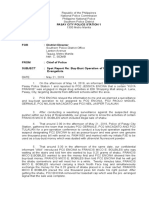

- Police Report SampleDokument4 SeitenPolice Report SampleMarielle SantiagoNoch keine Bewertungen

- Caterpillar, Inc. vs. Samson, 808 SCRA 309, G.R. No. 205972, G.R. No. 164352 November 9, 2016Dokument13 SeitenCaterpillar, Inc. vs. Samson, 808 SCRA 309, G.R. No. 205972, G.R. No. 164352 November 9, 2016Marielle SantiagoNoch keine Bewertungen

- Sales Digests by 2ADokument223 SeitenSales Digests by 2AMarielle Santiago100% (3)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Centurian Park RetailDokument2 SeitenCenturian Park Retailprachi_sipi1830Noch keine Bewertungen

- BIR RULING NO. 1102-18: Tata Consultancy Services (Philippines), IncDokument3 SeitenBIR RULING NO. 1102-18: Tata Consultancy Services (Philippines), IncKathleen Leynes100% (1)

- Find Buyers For Your Export BusinessDokument2 SeitenFind Buyers For Your Export BusinessЛилия ХовракNoch keine Bewertungen

- Indirect Tax Laws (New)Dokument892 SeitenIndirect Tax Laws (New)Mayank Jain100% (5)

- Tax Alert: The Transfer Pricing Guidelines, 2020Dokument5 SeitenTax Alert: The Transfer Pricing Guidelines, 2020musaNoch keine Bewertungen

- 2011 Pub 4491WDokument208 Seiten2011 Pub 4491WRefundOhioNoch keine Bewertungen

- Chapter 16Dokument13 SeitenChapter 16Andi Luo100% (1)

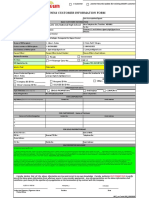

- Business Customer Information FormDokument3 SeitenBusiness Customer Information Formpretty mangayNoch keine Bewertungen

- List of Importables ExcelDokument4 SeitenList of Importables ExcelRACNoch keine Bewertungen

- Iloilo Bottlers vs. City of IloiloDokument5 SeitenIloilo Bottlers vs. City of IloiloCeline GarciaNoch keine Bewertungen

- Akash Flight BookingDokument3 SeitenAkash Flight BookingAkash GuptaNoch keine Bewertungen

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Dokument1 SeiteTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Anku KumarNoch keine Bewertungen

- Aranda Vs Rep - DigestDokument2 SeitenAranda Vs Rep - DigestAnna Marie Dayanghirang100% (2)

- The Collector of Internal Revenue vs. Suyoc Consolidated Mining Company, Et AlDokument3 SeitenThe Collector of Internal Revenue vs. Suyoc Consolidated Mining Company, Et AlDaLe AparejadoNoch keine Bewertungen

- Book Review Executive Salaries in South Africa PDFDokument4 SeitenBook Review Executive Salaries in South Africa PDFTabokaNoch keine Bewertungen

- Final Plan BekurDokument48 SeitenFinal Plan BekurDagmawi TesfayeNoch keine Bewertungen

- Technology and Livelihood Education Home Economics Module 3Dokument17 SeitenTechnology and Livelihood Education Home Economics Module 3Mario EstrellaNoch keine Bewertungen

- Part III PDFDokument53 SeitenPart III PDFRandolph QuilingNoch keine Bewertungen

- "A Study On GST Implementation in FMCG Sector" Table of ContentsDokument49 Seiten"A Study On GST Implementation in FMCG Sector" Table of ContentsPravallika0% (2)

- Service Charges in Commercial Property Second EditionDokument88 SeitenService Charges in Commercial Property Second EditionChris Gonzales100% (1)

- IRBs Public Ruling No 5 of 2019 - Employee Buy Out Payments Taxable As Perquisites LHAG Update 20200221Dokument4 SeitenIRBs Public Ruling No 5 of 2019 - Employee Buy Out Payments Taxable As Perquisites LHAG Update 20200221Ann YeoNoch keine Bewertungen

- 9347 Single CustomsDokument8 Seiten9347 Single CustomsKalpesh RathodNoch keine Bewertungen

- Auditing Arens Chapter 20Dokument30 SeitenAuditing Arens Chapter 20MARLINNoch keine Bewertungen

- GST Scope Post Release DocumentDokument22 SeitenGST Scope Post Release DocumentRajesh KumarNoch keine Bewertungen

- Transfer Deed Government of PakistanDokument3 SeitenTransfer Deed Government of Pakistanapi-3803246Noch keine Bewertungen

- DigestDokument87 SeitenDigestAira Mae BorrasNoch keine Bewertungen

- RG146 Pocket GuideDokument30 SeitenRG146 Pocket GuideMentor RG146Noch keine Bewertungen

- Foundations - Tax Exempt Foundations Their Impact On Our Economy US Gov 1962 140pgs PDFDokument140 SeitenFoundations - Tax Exempt Foundations Their Impact On Our Economy US Gov 1962 140pgs PDFjulianbreNoch keine Bewertungen

- Palma Development Corporation vs. Municipality of Malangas, Zamboanga Del SurDokument7 SeitenPalma Development Corporation vs. Municipality of Malangas, Zamboanga Del SurPamela L. FallerNoch keine Bewertungen

- Agile ManufacturingDokument17 SeitenAgile Manufacturingkaushalsingh20Noch keine Bewertungen