Das könnte Ihnen auch gefallen

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Godrej Group Portfolio AnalysisDokument16 SeitenGodrej Group Portfolio AnalysisEina GuptaNoch keine Bewertungen

- 3 Hank Kolb, Director, Quality AssuranceDokument3 Seiten3 Hank Kolb, Director, Quality AssuranceEina Gupta100% (1)

- Godrej Group Portfolio AnalysisDokument16 SeitenGodrej Group Portfolio AnalysisEina GuptaNoch keine Bewertungen

- 2 Donner CompanyDokument1 Seite2 Donner CompanyEina GuptaNoch keine Bewertungen

- Assignment 1 - TerraCogDokument6 SeitenAssignment 1 - TerraCogEina GuptaNoch keine Bewertungen

- Sampa Video G3 - SecBDokument3 SeitenSampa Video G3 - SecBEina GuptaNoch keine Bewertungen

- One Flew Over Cuckoo's NestDokument15 SeitenOne Flew Over Cuckoo's NestEina GuptaNoch keine Bewertungen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5795)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1091)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Advance Account MCQ BookDokument78 SeitenAdvance Account MCQ Bookcloudstorage567Noch keine Bewertungen

- Corp Law Outline 5 - 2020Dokument4 SeitenCorp Law Outline 5 - 2020Effy SantosNoch keine Bewertungen

- IFRS Edition (2nd) : Plant Assets, Natural Resources, and Intangible AssetsDokument62 SeitenIFRS Edition (2nd) : Plant Assets, Natural Resources, and Intangible Assetsmajestic accounting100% (1)

- Advanced Acctg Chapter 2 MWUDokument97 SeitenAdvanced Acctg Chapter 2 MWUhabtamuNoch keine Bewertungen

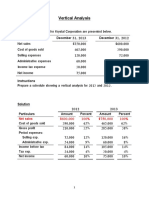

- Vertical Analysis SolutionsDokument5 SeitenVertical Analysis SolutionsSamer IsmaelNoch keine Bewertungen

- June 2022 Module 1 (Candidate Script)Dokument9 SeitenJune 2022 Module 1 (Candidate Script)damian gonzalezNoch keine Bewertungen

- Prelims Reviewer Corpo Momo Eats Et - Al 1 1Dokument73 SeitenPrelims Reviewer Corpo Momo Eats Et - Al 1 1Francois Amos PalomoNoch keine Bewertungen

- Financial PlanDokument54 SeitenFinancial PlanTeku ThwalaNoch keine Bewertungen

- 11 SM Accountancy em 2022 23Dokument368 Seiten11 SM Accountancy em 2022 23Mohd JamaluddinNoch keine Bewertungen

- Session 04 - Exercise - AnswersDokument4 SeitenSession 04 - Exercise - AnswersMavisNoch keine Bewertungen

- Activity 07 CH14Dokument4 SeitenActivity 07 CH14Dandreb SuaybaguioNoch keine Bewertungen

- On July 1 2014 Melanie Thornhill Began Her Third MonthDokument1 SeiteOn July 1 2014 Melanie Thornhill Began Her Third MonthTaimour HassanNoch keine Bewertungen

- Share Capital DebentureDokument17 SeitenShare Capital DebentureNAGARAJACHARI KAMMARANoch keine Bewertungen

- Acctg 330 Ch1Dokument2 SeitenAcctg 330 Ch1agm25Noch keine Bewertungen

- Reviewer Acca 102Dokument12 SeitenReviewer Acca 102Nicole FidelsonNoch keine Bewertungen

- Interim Financial ReportDokument30 SeitenInterim Financial ReportVIRGIL KIT AUGUSTIN ABANILLANoch keine Bewertungen

- Unit of Production MethodDokument2 SeitenUnit of Production MethodNiño Rey LopezNoch keine Bewertungen

- Risk and ReturnDokument40 SeitenRisk and ReturnJudeNoch keine Bewertungen

- 2BIS Companies (Tue - 14-11-2023) - Final Mid-TermDokument32 Seiten2BIS Companies (Tue - 14-11-2023) - Final Mid-TermahmedNoch keine Bewertungen

- Pradipta Kumar Pattnaik DataDokument770 SeitenPradipta Kumar Pattnaik DatamanasNoch keine Bewertungen

- Exercises - Chapter 11Dokument19 SeitenExercises - Chapter 11Jhoni Lim67% (3)

- College Accounting Chapters 15th Edition by Price Haddock and Farina ISBN Solution ManualDokument11 SeitenCollege Accounting Chapters 15th Edition by Price Haddock and Farina ISBN Solution Manualmark100% (22)

- Listado de Beneficiarios Rpec para Web Julio2022Dokument44 SeitenListado de Beneficiarios Rpec para Web Julio2022bordisNoch keine Bewertungen

- Market CapDokument13 SeitenMarket CapVikas JaiswalNoch keine Bewertungen

- Test Bank Chapter18 Fs AnalysisDokument83 SeitenTest Bank Chapter18 Fs Analysiskris mNoch keine Bewertungen

- ParCor 2019 Chapter 4Dokument8 SeitenParCor 2019 Chapter 4Layla MainNoch keine Bewertungen

- Topic Three: Bases of Public Sector Accounting and ReportingDokument20 SeitenTopic Three: Bases of Public Sector Accounting and ReportingProf. SchleidenNoch keine Bewertungen

- PL Financial Accounting and Reporting IFRS Exam June 2019Dokument10 SeitenPL Financial Accounting and Reporting IFRS Exam June 2019scottNoch keine Bewertungen

- What Is A Distribution Channel - Types and Examples Explained - Definition From TechTargetDokument3 SeitenWhat Is A Distribution Channel - Types and Examples Explained - Definition From TechTargetrj34dilrajmeenaNoch keine Bewertungen

- Problems - Partnership LiquidationDokument8 SeitenProblems - Partnership LiquidationBrunxAlabastro56% (9)