Das könnte Ihnen auch gefallen

- YMCA v. CIR, 298 SCRA - THE LIFEBLOOD DOCTRINE - DigestDokument2 SeitenYMCA v. CIR, 298 SCRA - THE LIFEBLOOD DOCTRINE - DigestKate GaroNoch keine Bewertungen

- Eastern Theatrical Vs AlfonsoDokument2 SeitenEastern Theatrical Vs AlfonsoKirsten Denise B. Habawel-Vega67% (3)

- City of Baguio v. Fortunato de Leon GR L-24756Dokument1 SeiteCity of Baguio v. Fortunato de Leon GR L-24756Charles Roger RayaNoch keine Bewertungen

- Tan vs. Del Rosario and CIR, G.R. No. 109289, October 3, 1994Dokument3 SeitenTan vs. Del Rosario and CIR, G.R. No. 109289, October 3, 1994Maria Fiona Duran MerquitaNoch keine Bewertungen

- Pepsi-Cola v. TanauanDokument2 SeitenPepsi-Cola v. TanauanIshNoch keine Bewertungen

- Coll. v. Henderson, 1 SCRA 649Dokument2 SeitenColl. v. Henderson, 1 SCRA 649Homer SimpsonNoch keine Bewertungen

- Digest CIR Vs PinedaDokument2 SeitenDigest CIR Vs PinedaLoraine Ferrer100% (1)

- Hilado vs. CIRDokument2 SeitenHilado vs. CIRAlan Gultia100% (2)

- CN Hogdes v. Mun Board of IloiloDokument2 SeitenCN Hogdes v. Mun Board of IloiloMirellaNoch keine Bewertungen

- CIR Vs CA & CastanedaDokument1 SeiteCIR Vs CA & CastanedaArmstrong BosantogNoch keine Bewertungen

- Philippine Acetylene Co. Inc vs. CirDokument2 SeitenPhilippine Acetylene Co. Inc vs. Cirbrendamanganaan100% (1)

- Davao Gulf Lumber Corp V CIRDokument3 SeitenDavao Gulf Lumber Corp V CIRAiken Alagban LadinesNoch keine Bewertungen

- Marcos II v. CA DigestsDokument2 SeitenMarcos II v. CA Digestspinkblush717Noch keine Bewertungen

- Consti2Digest - Juan Luna Subdivisio, Inc. Vs M. Sarmiento, Et Al, GR L-3538, (28 May 1952Dokument3 SeitenConsti2Digest - Juan Luna Subdivisio, Inc. Vs M. Sarmiento, Et Al, GR L-3538, (28 May 1952Lu CasNoch keine Bewertungen

- CIR Vs The Estate of TodaDokument3 SeitenCIR Vs The Estate of TodaLDNoch keine Bewertungen

- CITY OF BAGUIO V. FORTUNATO DE LEON, 25 SCRA 938 - PUBLIC PURPOSE - EQUAL PROTECTION - DigestDokument1 SeiteCITY OF BAGUIO V. FORTUNATO DE LEON, 25 SCRA 938 - PUBLIC PURPOSE - EQUAL PROTECTION - DigestKate GaroNoch keine Bewertungen

- PLDT v. Davao City Case DigestDokument1 SeitePLDT v. Davao City Case DigestFlorence Rosete100% (3)

- City of Baguio vs. de Leon DigestDokument2 SeitenCity of Baguio vs. de Leon DigestKath Leen100% (1)

- Western Minolco v. CommissionerDokument2 SeitenWestern Minolco v. CommissionerEva TrinidadNoch keine Bewertungen

- CIR Vs PLDT DigestDokument3 SeitenCIR Vs PLDT DigestKath Leen100% (3)

- Domingo vs. Garlitos Case DigestDokument1 SeiteDomingo vs. Garlitos Case DigestAdhara CelerianNoch keine Bewertungen

- Mod1 - 5 - G.R. No. L-19342 Ona V CIRDokument2 SeitenMod1 - 5 - G.R. No. L-19342 Ona V CIROjie SantillanNoch keine Bewertungen

- Caltex v. COA DigestDokument2 SeitenCaltex v. COA Digestpinkblush717100% (1)

- People of The Philippines, Petitioners, SANDIGANBAYAN (Fourth Division) and BIENVENIDO A. TAN JR., RespondentDokument2 SeitenPeople of The Philippines, Petitioners, SANDIGANBAYAN (Fourth Division) and BIENVENIDO A. TAN JR., RespondentJoshua Erik Madria100% (1)

- Taganito vs. Commissioner (1995)Dokument2 SeitenTaganito vs. Commissioner (1995)cmv mendozaNoch keine Bewertungen

- 3 - Realization TestDokument15 Seiten3 - Realization TestPaula BitorNoch keine Bewertungen

- CIR v. Algue, Inc., G.R. No. L-28896Dokument1 SeiteCIR v. Algue, Inc., G.R. No. L-28896fay garneth buscato100% (2)

- Limpan Investment Corporation v. Commissioner of Internal RevenueDokument1 SeiteLimpan Investment Corporation v. Commissioner of Internal RevenueEmmanuel YrreverreNoch keine Bewertungen

- Aguinaldo Industries Corporation vs. Commissioner of Internal Revenue Services Actually RenderedDokument2 SeitenAguinaldo Industries Corporation vs. Commissioner of Internal Revenue Services Actually RenderedCharmila SiplonNoch keine Bewertungen

- MERALCO V Province of LagunaDokument2 SeitenMERALCO V Province of LagunaJaz Sumalinog100% (1)

- Serafica v. City Treasurer of OrmocDokument1 SeiteSerafica v. City Treasurer of OrmocEarl LarroderNoch keine Bewertungen

- 11 NDC V CIRDokument3 Seiten11 NDC V CIRTricia MontoyaNoch keine Bewertungen

- Cir vs. Pineda, 21 Scra 105 PDFDokument1 SeiteCir vs. Pineda, 21 Scra 105 PDFJo DevisNoch keine Bewertungen

- Sison Vs AnchetaDokument2 SeitenSison Vs AnchetadasfghkjlNoch keine Bewertungen

- CIR v. PLDTDokument2 SeitenCIR v. PLDTKing Badong100% (1)

- Cagayan Electric Power V CommissionerDokument1 SeiteCagayan Electric Power V CommissionerTon Ton Cananea100% (1)

- Vegetable Oil Corp. V Trinidad, G.R. No. 21475, March 26, 1924, 45 Phil. 822Dokument2 SeitenVegetable Oil Corp. V Trinidad, G.R. No. 21475, March 26, 1924, 45 Phil. 822Maria Fiona Duran MerquitaNoch keine Bewertungen

- MARUBENI Vs CIR TAXDokument2 SeitenMARUBENI Vs CIR TAXLemuel Angelo M. EleccionNoch keine Bewertungen

- Association of Customs Brokers Inc Vs The Municipality Board City of ManilaDokument2 SeitenAssociation of Customs Brokers Inc Vs The Municipality Board City of ManilaYvon Baguio67% (3)

- SISON V ANCHETADokument4 SeitenSISON V ANCHETAMayflor BalinuyusNoch keine Bewertungen

- Diaz Vs Secretary of FinanceDokument3 SeitenDiaz Vs Secretary of FinanceJoshua Shin100% (5)

- Compania Vs City of ManilaDokument1 SeiteCompania Vs City of ManilaJf ManejaNoch keine Bewertungen

- LTO v. City of Butuan DigestDokument2 SeitenLTO v. City of Butuan DigestKai128100% (1)

- YMCA vs. CIRDokument2 SeitenYMCA vs. CIRMichelle100% (1)

- Fisher V TrinidadDokument2 SeitenFisher V TrinidadEva Marie Gutierrez Cantero100% (1)

- PILMICO v. CIRDokument2 SeitenPILMICO v. CIRPat EspinozaNoch keine Bewertungen

- Aguinaldo Industries v. CIRDokument1 SeiteAguinaldo Industries v. CIRTon Ton CananeaNoch keine Bewertungen

- First Lepanto Taisho Insurance Corp. V CIRDokument1 SeiteFirst Lepanto Taisho Insurance Corp. V CIRGillian CalpitoNoch keine Bewertungen

- Commissioner of Internal Revenue Vs Soriano y CIADokument1 SeiteCommissioner of Internal Revenue Vs Soriano y CIAAmor5678Noch keine Bewertungen

- Kapatiran NF Mga NAglilingkod Sa Pamahalaan NG Pilipinas, Inc. Vs Tan DigestDokument2 SeitenKapatiran NF Mga NAglilingkod Sa Pamahalaan NG Pilipinas, Inc. Vs Tan DigestRalph Mark Joseph100% (2)

- Tax Case Digest - Commissioner of Internal Revenue Vs Algue Inc GR No L-28896Dokument2 SeitenTax Case Digest - Commissioner of Internal Revenue Vs Algue Inc GR No L-28896Anthony Pineda100% (1)

- A - Pirovano Vs CIRDokument1 SeiteA - Pirovano Vs CIRceilo coboNoch keine Bewertungen

- COMMISSIONER OF INTERNAL REVENUE, Petitioner, vs. CITYTRUST INVESTMENT PHILS., INC., Respondent.Dokument1 SeiteCOMMISSIONER OF INTERNAL REVENUE, Petitioner, vs. CITYTRUST INVESTMENT PHILS., INC., Respondent.Charles Roger Raya100% (1)

- Aguinaldo Vs CIR #Tax-1Dokument2 SeitenAguinaldo Vs CIR #Tax-1Earl TagraNoch keine Bewertungen

- Pepsi Cola v. City of Butuan DigestDokument2 SeitenPepsi Cola v. City of Butuan DigestAnonymous PbYTL9zzco100% (1)

- Taganito Mining Corp. vs. CIR CTA 04702 (Full Text)Dokument14 SeitenTaganito Mining Corp. vs. CIR CTA 04702 (Full Text)Ritzchalle Garcia-Oalin100% (1)

- Tax 1 - Dean's Circle 2019 27Dokument1 SeiteTax 1 - Dean's Circle 2019 27Romeo G. Labador Jr.Noch keine Bewertungen

- Vera vs. FernandezDokument2 SeitenVera vs. FernandezKlarence Orjalo100% (1)

- Remrev 2 (Specpro 2) CasesDokument174 SeitenRemrev 2 (Specpro 2) Casesart villarinoNoch keine Bewertungen

- Vera Vs FernandezDokument6 SeitenVera Vs FernandezPaolo Antonio EscalonaNoch keine Bewertungen

- CIR vs. Standard Insurance: SummaryDokument4 SeitenCIR vs. Standard Insurance: SummaryIshNoch keine Bewertungen

- PSALM Vs CIRDokument2 SeitenPSALM Vs CIRIshNoch keine Bewertungen

- 10 OCEANIC WIRELESS NETWORK Vs CIRDokument3 Seiten10 OCEANIC WIRELESS NETWORK Vs CIRIsh100% (1)

- 16 Republic Vs GMCC United Development CorpDokument2 Seiten16 Republic Vs GMCC United Development CorpIsh100% (1)

- 58 MACEDA Vs MACARAIGDokument3 Seiten58 MACEDA Vs MACARAIGIshNoch keine Bewertungen

- Sum of MoneyDokument5 SeitenSum of MoneyIshNoch keine Bewertungen

- 18 M Lhuillier Vs CIRDokument2 Seiten18 M Lhuillier Vs CIRIshNoch keine Bewertungen

- 38 CIR Vs SEA GATEDokument4 Seiten38 CIR Vs SEA GATEIshNoch keine Bewertungen

- 48 PH Natl Police Cooperative Vs CIRDokument2 Seiten48 PH Natl Police Cooperative Vs CIRIshNoch keine Bewertungen

- Cir Vs Sekisui Jushi PH: Doctrine/SDokument2 SeitenCir Vs Sekisui Jushi PH: Doctrine/SIshNoch keine Bewertungen

- 46-Quezon City Vs BayantelDokument3 Seiten46-Quezon City Vs BayantelIshNoch keine Bewertungen

- Phil. Guaranty Co. v. CIRDokument2 SeitenPhil. Guaranty Co. v. CIRIshNoch keine Bewertungen

- Justo Vs GalingDokument1 SeiteJusto Vs GalingIshNoch keine Bewertungen

- Lutz Vs AranetaDokument1 SeiteLutz Vs AranetaIshNoch keine Bewertungen

- Atlas Consolidated Mining Development Corp. v. CIRDokument1 SeiteAtlas Consolidated Mining Development Corp. v. CIRIshNoch keine Bewertungen

- NTC Vs CA and PLDTDokument2 SeitenNTC Vs CA and PLDTIsh100% (2)

- NPC Vs AlbayDokument1 SeiteNPC Vs AlbayIshNoch keine Bewertungen

- Chevron Philippines, Inc. vs. Bases Conversion Development Authority and Clark Development Corporation, G.R. No. 173863, September 15, 2010Dokument1 SeiteChevron Philippines, Inc. vs. Bases Conversion Development Authority and Clark Development Corporation, G.R. No. 173863, September 15, 2010Jeselle Ann VegaNoch keine Bewertungen

- CBK Power Co LTD Vs CIRDokument2 SeitenCBK Power Co LTD Vs CIRIshNoch keine Bewertungen

- MARCOS II Vs CADokument2 SeitenMARCOS II Vs CAIshNoch keine Bewertungen

- CIR v. BPIDokument2 SeitenCIR v. BPIIshNoch keine Bewertungen

- The Roman Catholic Bishop of Tuguegarao Vs PrudencioDokument2 SeitenThe Roman Catholic Bishop of Tuguegarao Vs PrudencioIshNoch keine Bewertungen

- Heirs of Roger Jarque Vs Marcial JarqueDokument2 SeitenHeirs of Roger Jarque Vs Marcial JarqueIsh100% (3)

- Gender Bias in Tax Systems:: The Example of GhanaDokument22 SeitenGender Bias in Tax Systems:: The Example of GhanaDangyi GodSeesNoch keine Bewertungen

- Qesco Online BillDokument2 SeitenQesco Online BillFazal TanhaNoch keine Bewertungen

- Karnataka Prohibition On Beggary ActDokument14 SeitenKarnataka Prohibition On Beggary Actusha242004Noch keine Bewertungen

- Cash Management: Why Organisations Hold CashDokument15 SeitenCash Management: Why Organisations Hold CashAjay Kumar TakiarNoch keine Bewertungen

- South Middleton School District, Teacher Contract NegotiationDokument18 SeitenSouth Middleton School District, Teacher Contract NegotiationPennLiveNoch keine Bewertungen

- RMC No. 16-2021Dokument1 SeiteRMC No. 16-2021nathalie velasquezNoch keine Bewertungen

- Labuan TrustDokument41 SeitenLabuan TrustShahrani KassimNoch keine Bewertungen

- Ein Digital ArtDokument2 SeitenEin Digital ArtErik ElseaNoch keine Bewertungen

- 21.secretary Vs LazatinDokument11 Seiten21.secretary Vs LazatinClyde KitongNoch keine Bewertungen

- When Is A Notice of Donation Needed?: NEDA - National Economic Development AuthorityDokument4 SeitenWhen Is A Notice of Donation Needed?: NEDA - National Economic Development AuthorityJonabelle BiliganNoch keine Bewertungen

- Entrepreneur 5Dokument22 SeitenEntrepreneur 5Emelyn isaac MalillinNoch keine Bewertungen

- Business Acquisition Checklist PDFDokument3 SeitenBusiness Acquisition Checklist PDFGhassan Qutob100% (3)

- Olive Green Mint Green Modular Abstract Business Case Study and Report Business PresentationDokument14 SeitenOlive Green Mint Green Modular Abstract Business Case Study and Report Business PresentationLokesh GautamNoch keine Bewertungen

- Unit 1 Notes TaxDokument14 SeitenUnit 1 Notes TaxSuryansh MunjalNoch keine Bewertungen

- STD XII Class Note 1 NATIONAL INCOME 2021 22Dokument19 SeitenSTD XII Class Note 1 NATIONAL INCOME 2021 22BE SANATANINoch keine Bewertungen

- Estate TaxDokument32 SeitenEstate TaxANDREA SEVERINONoch keine Bewertungen

- CPAR Final Pre-Board With AnswersjjjjDokument8 SeitenCPAR Final Pre-Board With AnswersjjjjMacwin KiatNoch keine Bewertungen

- Royalty 3Dokument16 SeitenRoyalty 3Gamers 4 lyfNoch keine Bewertungen

- Instructions: Financial Accounting and Reporting IIDokument2 SeitenInstructions: Financial Accounting and Reporting IIROB101512Noch keine Bewertungen

- Bill Cum Receipt - Ms Humki Devi .Dokument1 SeiteBill Cum Receipt - Ms Humki Devi .Rahul SsdotraNoch keine Bewertungen

- Charge Slip - 1708623292755Dokument8 SeitenCharge Slip - 1708623292755Sachin ChaudharyNoch keine Bewertungen

- Rent Amount Received Which Is Rs. 2,40,000/ - (Rupees Two Lakh Forty Thousand Only)Dokument4 SeitenRent Amount Received Which Is Rs. 2,40,000/ - (Rupees Two Lakh Forty Thousand Only)deepa parabNoch keine Bewertungen

- M&A Due Diligence Guide PDFDokument20 SeitenM&A Due Diligence Guide PDFRuliani Putri Sinaga100% (3)

- 3 Months Study Plan With A, B, C Analysis CS Executive Dec-23 Old SyllabusDokument42 Seiten3 Months Study Plan With A, B, C Analysis CS Executive Dec-23 Old SyllabusGungun ChetaniNoch keine Bewertungen

- Coverage For Business Law and Taxation: A. Introduction To LawDokument2 SeitenCoverage For Business Law and Taxation: A. Introduction To Lawmarjorie sarsabaNoch keine Bewertungen

- Scope of Cyber LawsDokument4 SeitenScope of Cyber Lawsrajat kanoiNoch keine Bewertungen

- Test Structure Sample QuestionDokument5 SeitenTest Structure Sample QuestionDnyaneshwar MaskeNoch keine Bewertungen

- Purging America of The Matrix PDFDokument49 SeitenPurging America of The Matrix PDFPaul Kasper100% (1)

- Soal Pas Bhs. Inggris KLS Xi Paket CDokument9 SeitenSoal Pas Bhs. Inggris KLS Xi Paket CZayn Danish Aruna ShanumNoch keine Bewertungen

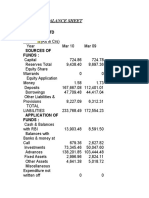

- Balance Sheet: JK Cement LTDDokument3 SeitenBalance Sheet: JK Cement LTDHimanshu SharmaNoch keine Bewertungen