Das könnte Ihnen auch gefallen

- Sale Price of Replaced Equipment P 40,000Dokument15 SeitenSale Price of Replaced Equipment P 40,000Jay GamboaNoch keine Bewertungen

- Acctg 15 - Midterm ExamDokument6 SeitenAcctg 15 - Midterm ExamAngelo LabiosNoch keine Bewertungen

- Audit Committee Responsibilities and Review QuestionsDokument3 SeitenAudit Committee Responsibilities and Review QuestionsHads LunaNoch keine Bewertungen

- Chapter 7 - Conversion Cycle P4Dokument26 SeitenChapter 7 - Conversion Cycle P4Joana TrinidadNoch keine Bewertungen

- Chapter 5Dokument19 SeitenChapter 5Rochelle Esquivel ManaloNoch keine Bewertungen

- C36 Planning-W RevisionsDokument23 SeitenC36 Planning-W RevisionsNicole Johnson100% (1)

- Strategic Business Analysis - MidtermDokument123 SeitenStrategic Business Analysis - MidtermlorriejaneNoch keine Bewertungen

- Mikong Due MARCH 30 Hospital and HmosDokument6 SeitenMikong Due MARCH 30 Hospital and HmosCoke Aidenry SaludoNoch keine Bewertungen

- Chapter 14Dokument4 SeitenChapter 14Jomer FernandezNoch keine Bewertungen

- ToA Quizzer 1 - Intro To PFRS (3TAY1617)Dokument6 SeitenToA Quizzer 1 - Intro To PFRS (3TAY1617)Kyle ParisNoch keine Bewertungen

- Success Today Is No Guarantee of Success Tomorrow!Dokument8 SeitenSuccess Today Is No Guarantee of Success Tomorrow!Ammad MaqboolNoch keine Bewertungen

- Risk Management Principles and Capital Structure AnalysisDokument11 SeitenRisk Management Principles and Capital Structure AnalysisnevadNoch keine Bewertungen

- Interactive Model of An EconomyDokument142 SeitenInteractive Model of An Economyrajraj999Noch keine Bewertungen

- Test Bank Management 8th Edition BatemanDokument40 SeitenTest Bank Management 8th Edition BatemanIris DescentNoch keine Bewertungen

- Midterm Exams at University of San Jose RecoletosDokument5 SeitenMidterm Exams at University of San Jose RecoletosMa. Kristine Laurice Amancio100% (1)

- Level Up - Conceptual Framework ReviewerDokument15 SeitenLevel Up - Conceptual Framework Reviewerazithethird100% (1)

- Unit Iv Assessment Part Ii Internal Control A Tool in Managing RiskDokument3 SeitenUnit Iv Assessment Part Ii Internal Control A Tool in Managing RiskLaiven Ryle100% (1)

- Ais - Chapter 1Dokument54 SeitenAis - Chapter 1LumongtadJoanMaeNoch keine Bewertungen

- Fa 3 Chapter 2 Statement of Financial PositionDokument22 SeitenFa 3 Chapter 2 Statement of Financial PositionKristine Florence TolentinoNoch keine Bewertungen

- Financial Accounting 1 Valix Part 1Dokument2 SeitenFinancial Accounting 1 Valix Part 1AkiNoch keine Bewertungen

- AC13.1.1 Module 1 - Provisions, Contingencies, and Other LiabilitiesDokument15 SeitenAC13.1.1 Module 1 - Provisions, Contingencies, and Other LiabilitiesRenelle HabacNoch keine Bewertungen

- BDO Unibank 2020 Annual Report Financial SupplementsDokument236 SeitenBDO Unibank 2020 Annual Report Financial SupplementsDanNoch keine Bewertungen

- Chapter 7 Pull Strategy and IMCDokument15 SeitenChapter 7 Pull Strategy and IMCJehan Marie GiananNoch keine Bewertungen

- Financial Management Part 2: Analyzing ReportsDokument36 SeitenFinancial Management Part 2: Analyzing ReportsJudy Anne RamirezNoch keine Bewertungen

- Strategic Management IntroductionDokument4 SeitenStrategic Management Introductionkim che100% (1)

- MANAGEMENT ACCOUNTING SOLUTIONS CHAPTER 14 RESPONSIBILITY ACCOUNTINGDokument24 SeitenMANAGEMENT ACCOUNTING SOLUTIONS CHAPTER 14 RESPONSIBILITY ACCOUNTINGAang GrandeNoch keine Bewertungen

- Psa 510Dokument9 SeitenPsa 510Rico Jon Hilario GarciaNoch keine Bewertungen

- Governance Review Questions ExplainedDokument2 SeitenGovernance Review Questions ExplainedShane Tabunggao100% (1)

- FinMan Theories 2Dokument6 SeitenFinMan Theories 2Marie GonzalesNoch keine Bewertungen

- CHAPTER 17-scmDokument15 SeitenCHAPTER 17-scmZsisum Meroo1Noch keine Bewertungen

- AP Quiz No. 1 Auditing and The Audit ProcessDokument12 SeitenAP Quiz No. 1 Auditing and The Audit ProcessJeremiah MadlangsakayNoch keine Bewertungen

- Effectiveness of Internal Conrol Sysyems in Safeguarding InventoryDokument9 SeitenEffectiveness of Internal Conrol Sysyems in Safeguarding Inventoryraymart copiarNoch keine Bewertungen

- New Era University: Financial Accounting & Reporting (Acctg01-19) Course PlanDokument7 SeitenNew Era University: Financial Accounting & Reporting (Acctg01-19) Course PlanEj UlangNoch keine Bewertungen

- CH 13Dokument18 SeitenCH 13xxxxxxxxxNoch keine Bewertungen

- Module 13 Regular Deductions 3Dokument16 SeitenModule 13 Regular Deductions 3Donna Mae FernandezNoch keine Bewertungen

- CFAS INTRo1Dokument14 SeitenCFAS INTRo1Hannah Pamela LegaspiNoch keine Bewertungen

- Form of A List of Risks Exercise People With An Extensive Knowledge of The Program or Process That Will Be Analyzed To Use A Prepared ListDokument4 SeitenForm of A List of Risks Exercise People With An Extensive Knowledge of The Program or Process That Will Be Analyzed To Use A Prepared ListKeanne ArmstrongNoch keine Bewertungen

- Understanding Threats and Safeguards in AccountancyDokument20 SeitenUnderstanding Threats and Safeguards in AccountancyKezNoch keine Bewertungen

- Internal Audit PhilosophyDokument2 SeitenInternal Audit Philosophy44abc100% (1)

- Chap 1 IntlmktDokument46 SeitenChap 1 IntlmktAlexis RoxasNoch keine Bewertungen

- MA Cabrera 2010 - SolManDokument4 SeitenMA Cabrera 2010 - SolManCarla Francisco Domingo40% (5)

- CFAS - Lec. 1 OVERVIEW OF ACCOUNTINGDokument17 SeitenCFAS - Lec. 1 OVERVIEW OF ACCOUNTINGlatte aeri100% (1)

- Decentralized and Segment ReportingDokument44 SeitenDecentralized and Segment ReportingShaina Santiago AlejoNoch keine Bewertungen

- Chapter 1 - MCQDokument2 SeitenChapter 1 - MCQHads LunaNoch keine Bewertungen

- Chapter 2Dokument12 SeitenChapter 2Cassandra KarolinaNoch keine Bewertungen

- Saint Mary's University: Accounting Knowledge and Skills of Selected Barangay Treasurers in A Second Class MunicipalityDokument10 SeitenSaint Mary's University: Accounting Knowledge and Skills of Selected Barangay Treasurers in A Second Class MunicipalityVia MontemayorNoch keine Bewertungen

- Quizbowl M7&M8Dokument54 SeitenQuizbowl M7&M8Ann Christine C. ChuaNoch keine Bewertungen

- Auditing Theory SyllabusDokument7 SeitenAuditing Theory Syllabusrajahmati_28Noch keine Bewertungen

- People Development Policies Chapter SummaryDokument22 SeitenPeople Development Policies Chapter SummaryJoongNoch keine Bewertungen

- Job Costing Finished Goods InventoryDokument46 SeitenJob Costing Finished Goods InventoryNavindra JaggernauthNoch keine Bewertungen

- Metrobank Case Involving Maria Victoria LopezDokument9 SeitenMetrobank Case Involving Maria Victoria LopezGray JavierNoch keine Bewertungen

- Advanced Financial Accounting Midterm: For Questions 2-4Dokument13 SeitenAdvanced Financial Accounting Midterm: For Questions 2-4Mister MysteriousNoch keine Bewertungen

- Lyceum-Northwestern University: L-NU AA-23-02-01-18Dokument8 SeitenLyceum-Northwestern University: L-NU AA-23-02-01-18Amie Jane MirandaNoch keine Bewertungen

- Value Chain Management Capability A Complete Guide - 2020 EditionVon EverandValue Chain Management Capability A Complete Guide - 2020 EditionNoch keine Bewertungen

- Asset Allocation: Balancing Financial Risk, Fifth Edition: Balancing Financial Risk, Fifth EditionVon EverandAsset Allocation: Balancing Financial Risk, Fifth Edition: Balancing Financial Risk, Fifth EditionBewertung: 4 von 5 Sternen4/5 (13)

- Management Accounting & Services GuideDokument4 SeitenManagement Accounting & Services GuideIvan ChiuNoch keine Bewertungen

- Strategic Cost ManagementDokument3 SeitenStrategic Cost ManagementKim Taehyung100% (1)

- Management Accounting NotesDokument24 SeitenManagement Accounting NotesRengeline LucasNoch keine Bewertungen

- Management Accounting Basic ConceptsDokument5 SeitenManagement Accounting Basic ConceptsAlexandra Nicole IsaacNoch keine Bewertungen

- MGT4 1Dokument2 SeitenMGT4 1InserahNoch keine Bewertungen

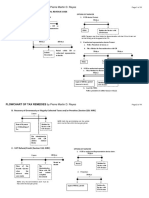

- Flowchart of Tax Remedies 2017 Update PRDokument11 SeitenFlowchart of Tax Remedies 2017 Update PRMarjorie Kate CresciniNoch keine Bewertungen

- IFRS Handbook 2013-14Dokument116 SeitenIFRS Handbook 2013-14Kyaw Htin WinNoch keine Bewertungen

- Systematic Study of Behavior for Evidence-Based ManagementDokument2 SeitenSystematic Study of Behavior for Evidence-Based ManagementInserahNoch keine Bewertungen

- FAR Test BankDokument36 SeitenFAR Test BankMangoStarr Aibelle VegasNoch keine Bewertungen

- ResearchDokument10 SeitenResearchElijah ColicoNoch keine Bewertungen

- Economic indicators and policy instrumentsDokument1 SeiteEconomic indicators and policy instrumentsThaminah ThassimNoch keine Bewertungen

- Joint Stock CompanyDokument12 SeitenJoint Stock CompanyVishnuNadarNoch keine Bewertungen

- Financial Accounting - Diploma (ABE)Dokument298 SeitenFinancial Accounting - Diploma (ABE)Ishmael OneyaNoch keine Bewertungen

- Project On Freight Cost Working Capital AnalysisDokument75 SeitenProject On Freight Cost Working Capital AnalysisGajendra BhoirNoch keine Bewertungen

- Shapiro CapBgt IMDokument76 SeitenShapiro CapBgt IMjhouvanNoch keine Bewertungen

- CONCEPTUAL FRAMEWORK UNDERLYING FINANCIAL ACCOUNTINGDokument4 SeitenCONCEPTUAL FRAMEWORK UNDERLYING FINANCIAL ACCOUNTINGjoemel09119050% (2)

- Manish AcknowledgementDokument8 SeitenManish AcknowledgementAmol GadkarNoch keine Bewertungen

- Post Office Monthly Income Scheme (MIS)Dokument2 SeitenPost Office Monthly Income Scheme (MIS)rupesh_kanabar1604100% (1)

- Current Assets Exercises II PDFDokument16 SeitenCurrent Assets Exercises II PDFMd Mobasshir Iqubal100% (1)

- CH 09Dokument78 SeitenCH 09Jeep RajNoch keine Bewertungen

- Accounting Concepts and Principles GRADE11 FUNDA1Dokument30 SeitenAccounting Concepts and Principles GRADE11 FUNDA1Jhana Mae BandosaNoch keine Bewertungen

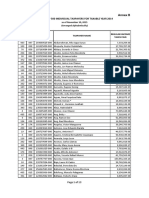

- Top Taxpayers in 2014Dokument13 SeitenTop Taxpayers in 2014GMA News OnlineNoch keine Bewertungen

- The Rise and Strategies of Global CorporationsDokument28 SeitenThe Rise and Strategies of Global Corporationskim leonida0% (3)

- In The Matter of Guarantee Acceptance Corporation, Debtor-Appellant v. Fidelity Mortgage Investors, 544 F.2d 449, 10th Cir. (1976)Dokument5 SeitenIn The Matter of Guarantee Acceptance Corporation, Debtor-Appellant v. Fidelity Mortgage Investors, 544 F.2d 449, 10th Cir. (1976)Scribd Government DocsNoch keine Bewertungen

- My SIP ProjectDokument62 SeitenMy SIP ProjectRahul WajeNoch keine Bewertungen

- Lesson 7: The First World War and The Interwar CrisisDokument45 SeitenLesson 7: The First World War and The Interwar Crisisupf123Noch keine Bewertungen

- Moving AveragesDokument2 SeitenMoving Averagesapi-3831404Noch keine Bewertungen

- Guidelines For Handling Investor Enquiries: Tpsa TpsaDokument37 SeitenGuidelines For Handling Investor Enquiries: Tpsa TpsaG ENoch keine Bewertungen

- What is ASEAN and its purposeDokument12 SeitenWhat is ASEAN and its purposem3r0k050% (2)

- Writting Assignement Unit 6Dokument3 SeitenWritting Assignement Unit 6Paw Akou-edi100% (1)

- Cost Accounting Standard DisclosuresDokument10 SeitenCost Accounting Standard DisclosuresrajdeeppawarNoch keine Bewertungen

- PARTNERSHIP1Dokument27 SeitenPARTNERSHIP1Christine Mae Mata100% (3)

- Symfonie P2P Lending FundDokument29 SeitenSymfonie P2P Lending FundSymfonie CapitalNoch keine Bewertungen

- Credtrans Commodatum and MutuumDokument49 SeitenCredtrans Commodatum and MutuumCeCe Em100% (2)

- PLAN KEYFACTS ORIGINAL Feb 2020 AMBITIOUSDokument1 SeitePLAN KEYFACTS ORIGINAL Feb 2020 AMBITIOUSbobsmith26Noch keine Bewertungen

- House Hearing, 109TH Congress - Financial Services Regulatory Relief: The Regulators' ViewsDokument301 SeitenHouse Hearing, 109TH Congress - Financial Services Regulatory Relief: The Regulators' ViewsScribd Government DocsNoch keine Bewertungen

- Y5 Pioneer English DLY 05-10-2017 Epaper@Yk InfoDokument16 SeitenY5 Pioneer English DLY 05-10-2017 Epaper@Yk InfoAkNoch keine Bewertungen

- TIPS Vs TreasuriesDokument8 SeitenTIPS Vs TreasurieszdfgbsfdzcgbvdfcNoch keine Bewertungen

- Energy 2030 - Horizon PowerDokument31 SeitenEnergy 2030 - Horizon PowerEli BernsteinNoch keine Bewertungen