Das könnte Ihnen auch gefallen

- Income Tax Banggawan2019 Ch9Dokument13 SeitenIncome Tax Banggawan2019 Ch9Noreen Ledda83% (6)

- Tax Banggawan2019 Ch15BDokument17 SeitenTax Banggawan2019 Ch15BNoreen Ledda100% (1)

- Chapter5-Self-Test ExercisesDokument10 SeitenChapter5-Self-Test ExercisesNeighvestNoch keine Bewertungen

- Banggawan ExercisesDokument100 SeitenBanggawan ExercisesPeter Piper100% (1)

- IncomeTax Chapter 8Dokument17 SeitenIncomeTax Chapter 8Marie Frances Sayson50% (2)

- IncomeTax Banggawan2019 Ch10Dokument10 SeitenIncomeTax Banggawan2019 Ch10Noreen Ledda100% (1)

- IncomeTax Banggawan2019 Ch12Dokument15 SeitenIncomeTax Banggawan2019 Ch12Noreen Ledda0% (1)

- IncomeTax Banggawan2019 Ch13Dokument19 SeitenIncomeTax Banggawan2019 Ch13Noreen Ledda100% (1)

- IncomeTax Banggawan2019 Ch4Dokument15 SeitenIncomeTax Banggawan2019 Ch4Noreen Ledda50% (8)

- Income-Tax Banggawan2019 CR7Dokument10 SeitenIncome-Tax Banggawan2019 CR7Noreen Ledda11% (9)

- IncomeTax Banggawan Ch11Dokument9 SeitenIncomeTax Banggawan Ch11Noreen Ledda33% (9)

- IncomeTax Banggawan2019 Ch13cDokument12 SeitenIncomeTax Banggawan2019 Ch13cNoreen Ledda33% (3)

- IncomeTaxation Banggawan2019 Ch13BDokument9 SeitenIncomeTaxation Banggawan2019 Ch13BNoreen Ledda0% (2)

- Real Estate Taxation True or False QuizDokument15 SeitenReal Estate Taxation True or False QuizNoreen Ledda25% (4)

- Individual Income Taxation RulesDokument12 SeitenIndividual Income Taxation RulesNoreen Ledda0% (1)

- IncomeTax Banggawan2019 CH3Dokument13 SeitenIncomeTax Banggawan2019 CH3Noreen Ledda50% (4)

- Income Taxation 2019 Chapter 13A 13C 14 BanggawanDokument8 SeitenIncome Taxation 2019 Chapter 13A 13C 14 BanggawanEricka Einjhel Lachama100% (8)

- Tax Banggawan2019 Ch.15-ADokument12 SeitenTax Banggawan2019 Ch.15-ANoreen LeddaNoch keine Bewertungen

- Name: Santiago II, Cipriano Jeffrey F.: Homework 2 - Tax 1101 - Topic Income Tax - Corporation Part 2Dokument3 SeitenName: Santiago II, Cipriano Jeffrey F.: Homework 2 - Tax 1101 - Topic Income Tax - Corporation Part 2うん こ100% (1)

- Chapter 11 12Dokument29 SeitenChapter 11 12Add All31% (13)

- PSW2 Tax1 SetbDokument1 SeitePSW2 Tax1 Setb'Bhandamme ParagasNoch keine Bewertungen

- INCOTAX - Multiple Choices - Problems Part 1Dokument3 SeitenINCOTAX - Multiple Choices - Problems Part 1Harvey100% (1)

- IncomeTax Banggawan2019 Ch2Dokument10 SeitenIncomeTax Banggawan2019 Ch2Noreen LeddaNoch keine Bewertungen

- Chapt-7 Dealings in PropDokument14 SeitenChapt-7 Dealings in Prophumnarvios0% (1)

- False False True True True FalseDokument7 SeitenFalse False True True True Falsegazer beam100% (1)

- TaxDokument3 SeitenTaxArven FrancoNoch keine Bewertungen

- Income Tax TestbankanssssDokument17 SeitenIncome Tax TestbankanssssAirille Carlos67% (3)

- Income TaxationDokument28 SeitenIncome TaxationJessa Gay Cartagena TorresNoch keine Bewertungen

- Income-Tax-Assignment No. 3 SolutionDokument18 SeitenIncome-Tax-Assignment No. 3 SolutionAuralin UbaldoNoch keine Bewertungen

- Quiz Dealings in Properties TAXATIONDokument10 SeitenQuiz Dealings in Properties TAXATIONAngela Nicole NobletaNoch keine Bewertungen

- TAX 1.docx KeyDokument94 SeitenTAX 1.docx Keymario1962Noch keine Bewertungen

- Gross IncomeDokument68 SeitenGross IncomeNour Aira NaoNoch keine Bewertungen

- HQ04 - Final Income TaxationDokument5 SeitenHQ04 - Final Income TaxationJimmyChaoNoch keine Bewertungen

- Tax 06-Tax On IndividualsDokument12 SeitenTax 06-Tax On IndividualsDin Rose Gonzales80% (5)

- Income Tax - Capital Gain and Final TaxesDokument4 SeitenIncome Tax - Capital Gain and Final TaxesAnie Martinez0% (1)

- IncomeTax Banggawan2019 Ch1Dokument22 SeitenIncomeTax Banggawan2019 Ch1Noreen Ledda100% (2)

- Taxation Notes on Gross Income Defined and ExclusionsDokument5 SeitenTaxation Notes on Gross Income Defined and ExclusionsSamantha Nicole HoyNoch keine Bewertungen

- Individual Income Tax ComputationDokument19 SeitenIndividual Income Tax ComputationShane Sigua-Salcedo100% (2)

- MC theory exam reviewDokument10 SeitenMC theory exam reviewlili60% (10)

- Final and Capital Gains TaxDokument7 SeitenFinal and Capital Gains TaxElla Marie LopezNoch keine Bewertungen

- Multiple-Choice Problems on Business TaxationDokument6 SeitenMultiple-Choice Problems on Business TaxationKatKat Olarte0% (1)

- Compensation and Fringe Benefits TaxDokument10 SeitenCompensation and Fringe Benefits TaxJane TuazonNoch keine Bewertungen

- Quiz Tax OPTDokument5 SeitenQuiz Tax OPTAnonymous 7HGskN0% (1)

- Individual Income TaxDokument4 SeitenIndividual Income TaxCristopher Romero Danlog0% (1)

- Business and Transfer Taxation Chapter 1 Answer KeyDokument3 SeitenBusiness and Transfer Taxation Chapter 1 Answer KeyJames100% (4)

- Gains & Losses From Dealing in PropertyDokument72 SeitenGains & Losses From Dealing in PropertyJoyce Nalzaro100% (2)

- Exclusion From Gross IncomeDokument8 SeitenExclusion From Gross IncomeRonna Mae DungogNoch keine Bewertungen

- CPA tax review questionsDokument10 SeitenCPA tax review questionsRalph SantosNoch keine Bewertungen

- CHAPTER 8 (AutoRecovered)Dokument58 SeitenCHAPTER 8 (AutoRecovered)Isabel MalicdanNoch keine Bewertungen

- ACC 311 Income Tax ReviewDokument6 SeitenACC 311 Income Tax ReviewRussel Jay CardeñoNoch keine Bewertungen

- Taxation 1 Final Exam Multiple ChoiceDokument5 SeitenTaxation 1 Final Exam Multiple ChoiceYamateNoch keine Bewertungen

- CPA Reviewer Multiple Choice Questions TaxationDokument38 SeitenCPA Reviewer Multiple Choice Questions TaxationCookie Pookie BallerShopNoch keine Bewertungen

- Taxation of Individuals QuizzerDokument37 SeitenTaxation of Individuals QuizzerCharry Ramos62% (13)

- PRELIM Chapter 9 10 11Dokument37 SeitenPRELIM Chapter 9 10 11Bisag AsaNoch keine Bewertungen

- Final Examination in Income TaxationDokument6 SeitenFinal Examination in Income TaxationJoyce Ann Cortez100% (2)

- Take Home Quiz Income TaxationDokument5 SeitenTake Home Quiz Income TaxationMae Astoveza100% (3)

- Income Tax MCQDokument10 SeitenIncome Tax MCQGlem Maquiling JosolNoch keine Bewertungen

- Taxation PDFDokument15 SeitenTaxation PDFJaneNoch keine Bewertungen

- True or FalseDokument76 SeitenTrue or FalsepangytpangytNoch keine Bewertungen

- Tax - Midterm NTC 2017Dokument12 SeitenTax - Midterm NTC 2017Red YuNoch keine Bewertungen

- IncomeTax Banggawan2019 Ch13Dokument19 SeitenIncomeTax Banggawan2019 Ch13Noreen Ledda100% (1)

- IncomeTax Banggawan2019 Ch2Dokument10 SeitenIncomeTax Banggawan2019 Ch2Noreen LeddaNoch keine Bewertungen

- IncomeTax Banggawan2019 Ch10Dokument10 SeitenIncomeTax Banggawan2019 Ch10Noreen Ledda100% (1)

- IncomeTax Banggawan2019 Ch1Dokument22 SeitenIncomeTax Banggawan2019 Ch1Noreen Ledda100% (2)

- IncomeTax Banggawan2019 CH3Dokument13 SeitenIncomeTax Banggawan2019 CH3Noreen Ledda50% (4)

- Individual Income Taxation RulesDokument12 SeitenIndividual Income Taxation RulesNoreen Ledda0% (1)

- IncomeTax Banggawan2019 Ch13cDokument12 SeitenIncomeTax Banggawan2019 Ch13cNoreen Ledda33% (3)

- IncomeTax Banggawan2019 Ch12Dokument15 SeitenIncomeTax Banggawan2019 Ch12Noreen Ledda0% (1)

- IADokument7 SeitenIANoreen Ledda100% (1)

- Real Estate Taxation True or False QuizDokument15 SeitenReal Estate Taxation True or False QuizNoreen Ledda25% (4)

- IncomeTax Banggawan2019 Ch4Dokument15 SeitenIncomeTax Banggawan2019 Ch4Noreen Ledda50% (8)

- IncomeTax Banggawan Ch11Dokument9 SeitenIncomeTax Banggawan Ch11Noreen Ledda33% (9)

- Real Estate Taxation True or False QuizDokument15 SeitenReal Estate Taxation True or False QuizNoreen Ledda25% (4)

- Tax Banggawan2019 Ch.15-ADokument12 SeitenTax Banggawan2019 Ch.15-ANoreen LeddaNoch keine Bewertungen

- Income-Tax Banggawan2019 CR7Dokument10 SeitenIncome-Tax Banggawan2019 CR7Noreen Ledda11% (9)

- IncomeTaxation Banggawan2019 Ch13BDokument9 SeitenIncomeTaxation Banggawan2019 Ch13BNoreen Ledda0% (2)

- Obligations and Quasi-Contracts ExplainedDokument3 SeitenObligations and Quasi-Contracts ExplainedNoreen LeddaNoch keine Bewertungen

- Tax Banggawan2019 Ch.15-ADokument12 SeitenTax Banggawan2019 Ch.15-ANoreen LeddaNoch keine Bewertungen

- IADokument7 SeitenIANoreen Ledda100% (1)

- Airish Noreen a-PEOPLEDokument3 SeitenAirish Noreen a-PEOPLENoreen LeddaNoch keine Bewertungen

- Work Performance of Part-Time Instructors at URS Binangonan CampusDokument12 SeitenWork Performance of Part-Time Instructors at URS Binangonan CampusNoreen LeddaNoch keine Bewertungen

- Law 1 Study Guide 2Dokument2 SeitenLaw 1 Study Guide 2Noreen LeddaNoch keine Bewertungen

- IncomeTax Banggawan2019 Ch1Dokument22 SeitenIncomeTax Banggawan2019 Ch1Noreen Ledda100% (2)

- Audit Risk FactorsDokument4 SeitenAudit Risk Factorsmariko1234Noch keine Bewertungen

- Chapter 13 WorksheetDokument4 SeitenChapter 13 WorksheetSy HimNoch keine Bewertungen

- HEIRS OF DR. INTAC vs. CADokument3 SeitenHEIRS OF DR. INTAC vs. CAmiles1280100% (3)

- AUD Quizmaster'sDokument22 SeitenAUD Quizmaster'sjessa marie virayNoch keine Bewertungen

- Account Determination MM en USDokument81 SeitenAccount Determination MM en USkamal_dipNoch keine Bewertungen

- TVM Spring 2015Dokument2 SeitenTVM Spring 2015Kamran RaufNoch keine Bewertungen

- Https WWW - Irctc.co - in Eticketing PrintTicketDokument1 SeiteHttps WWW - Irctc.co - in Eticketing PrintTicketKalyan UppadaNoch keine Bewertungen

- For Payments Other Than Imports and Remittances Covering Intermediary TradeDokument3 SeitenFor Payments Other Than Imports and Remittances Covering Intermediary TradeBgrj AjitNoch keine Bewertungen

- Curtain InvoiceDokument1 SeiteCurtain Invoicebilalahmad566Noch keine Bewertungen

- MCWQS For All XamsDokument97 SeitenMCWQS For All Xamsvini_anj3980Noch keine Bewertungen

- Chapter 1 - Introduction To BookkeepingDokument3 SeitenChapter 1 - Introduction To BookkeepingDaniel Tan KtNoch keine Bewertungen

- Final Exam-Auditing Theory 2015Dokument16 SeitenFinal Exam-Auditing Theory 2015Red YuNoch keine Bewertungen

- Introduction To AuditingDokument21 SeitenIntroduction To AuditingKul ShresthaNoch keine Bewertungen

- Curriculum Vitae OF Munyaradzi Mare Makwate Village, Mahalapye, BotswanaDokument7 SeitenCurriculum Vitae OF Munyaradzi Mare Makwate Village, Mahalapye, BotswanaAnonymous 4RLKj1Noch keine Bewertungen

- The Sunday Times - UBS Global Warming Index - Ilija Murisic - May 07Dokument2 SeitenThe Sunday Times - UBS Global Warming Index - Ilija Murisic - May 07akasaka99Noch keine Bewertungen

- Understanding Financial Leverage RatiosDokument17 SeitenUnderstanding Financial Leverage RatiosChristian Jasper M. LigsonNoch keine Bewertungen

- Sub Order LabelsDokument2 SeitenSub Order LabelsZeeshan naseemNoch keine Bewertungen

- IAS 33 Earnings Per Share: (Conceptual Framework and Standards)Dokument8 SeitenIAS 33 Earnings Per Share: (Conceptual Framework and Standards)Joyce ManaloNoch keine Bewertungen

- Case Study MMDokument4 SeitenCase Study MMMehdi TaseerNoch keine Bewertungen

- COM203 AmalgamationDokument10 SeitenCOM203 AmalgamationLogeshNoch keine Bewertungen

- Flow Valuation, Case #KEL778Dokument20 SeitenFlow Valuation, Case #KEL778SreeHarshaKazaNoch keine Bewertungen

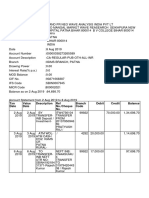

- TXN Date Value Date Description Ref No./Cheque No. Branch Code Debit Credit BalanceDokument3 SeitenTXN Date Value Date Description Ref No./Cheque No. Branch Code Debit Credit BalanceNishi GuptaNoch keine Bewertungen

- Benefits of International Financial Integration IIFDokument21 SeitenBenefits of International Financial Integration IIFKarann SehgalNoch keine Bewertungen

- Test 2 FarDokument3 SeitenTest 2 FarMa Jodelyn RosinNoch keine Bewertungen

- Quantitative Techniques For Decision Making - CasesDokument6 SeitenQuantitative Techniques For Decision Making - CasesPragya SinghNoch keine Bewertungen

- PRINCIPLES OF APPRAISAL PRACTICE AND CODE OF ETHICSDokument20 SeitenPRINCIPLES OF APPRAISAL PRACTICE AND CODE OF ETHICSnaren_3456Noch keine Bewertungen

- The Concepts and Practice of Mathematical Finance: Second EditionDokument8 SeitenThe Concepts and Practice of Mathematical Finance: Second EditionChâu GiangNoch keine Bewertungen

- REVIEW OF LITERATURE - Asset and Liability ManagementDokument3 SeitenREVIEW OF LITERATURE - Asset and Liability ManagementSherl AugustNoch keine Bewertungen