Das könnte Ihnen auch gefallen

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- ACCT 328 - Assignment 2Dokument7 SeitenACCT 328 - Assignment 2MalekNoch keine Bewertungen

- Ch02 SolutionDokument6 SeitenCh02 SolutionMalekNoch keine Bewertungen

- Chapter 1 - Conceptual and Case Analysis Frameworks For Financial ReportingDokument1 SeiteChapter 1 - Conceptual and Case Analysis Frameworks For Financial ReportingMalekNoch keine Bewertungen

- Accounting 281 Practice Final ExamDokument13 SeitenAccounting 281 Practice Final ExamMalekNoch keine Bewertungen

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

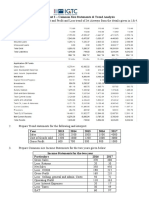

- Problem Sheet 2 - Common Size Statements & Trend AnalysisDokument3 SeitenProblem Sheet 2 - Common Size Statements & Trend AnalysisAkshita KapoorNoch keine Bewertungen

- Fundsmith Prospectus 2020Dokument84 SeitenFundsmith Prospectus 2020Kris WongNoch keine Bewertungen

- Master Budget ProblemDokument2 SeitenMaster Budget ProblemCillian ReevesNoch keine Bewertungen

- 9706 Accounting: MARK SCHEME For The May/June 2014 SeriesDokument6 Seiten9706 Accounting: MARK SCHEME For The May/June 2014 SeriesDanny DrinkwaterNoch keine Bewertungen

- The Goals and Functions of Financial Management: Mcgraw-Hill/IrwinDokument30 SeitenThe Goals and Functions of Financial Management: Mcgraw-Hill/IrwinanhtungocNoch keine Bewertungen

- Capital Asset Pricing ModelDokument25 SeitenCapital Asset Pricing ModelShiv Deep Sharma 20mmb087Noch keine Bewertungen

- Capital Budgeting FinalDokument78 SeitenCapital Budgeting FinalHarnitNoch keine Bewertungen

- Sample Financial Analysis ReportDokument19 SeitenSample Financial Analysis Reportdk1020100% (2)

- Dividend Policy Multiple Choice: True/FalseDokument28 SeitenDividend Policy Multiple Choice: True/FalseRica RegorisNoch keine Bewertungen

- Public Offering Regulations 2017Dokument55 SeitenPublic Offering Regulations 2017ayeshajamilafridi100% (1)

- ch12 SolutionsDokument49 Seitench12 Solutionsaboodyuae2000Noch keine Bewertungen

- Financial Modeling-A Valuation Model of Boeing Co.Dokument49 SeitenFinancial Modeling-A Valuation Model of Boeing Co.Shahid AliNoch keine Bewertungen

- Chapter 2-2Dokument74 SeitenChapter 2-2teniesha.davisNoch keine Bewertungen

- Cheat Sheet For ValuationDokument4 SeitenCheat Sheet For ValuationRISHAV BAIDNoch keine Bewertungen

- Capital Budgeting Practice TestDokument3 SeitenCapital Budgeting Practice TestYanii CapuyanNoch keine Bewertungen

- Costing Homework SolutionsDokument97 SeitenCosting Homework SolutionsKunal BhansaliNoch keine Bewertungen

- Fundamentals of Financial Accounting Canadian Canadian 4th Edition Phillips Solutions ManualDokument17 SeitenFundamentals of Financial Accounting Canadian Canadian 4th Edition Phillips Solutions ManualJacobFloresxbpcn100% (51)

- MPERS Article - A Comparative Analysis of PERS MPERS and MFRS FrameworksDokument59 SeitenMPERS Article - A Comparative Analysis of PERS MPERS and MFRS FrameworksHaron BadrulNoch keine Bewertungen

- Depreciation and Fixed AssetsDokument10 SeitenDepreciation and Fixed AssetssiddharthdileepkamatNoch keine Bewertungen

- Hibiscus Petroleum BHD - Delivering Value From Higher O&Amp G Prices and Asset AcquisitionsDokument5 SeitenHibiscus Petroleum BHD - Delivering Value From Higher O&Amp G Prices and Asset Acquisitionshomeng .nguardianNoch keine Bewertungen

- University of Mauritius: Faculty of Law and ManagementDokument10 SeitenUniversity of Mauritius: Faculty of Law and ManagementMîñåk ŞhïïNoch keine Bewertungen

- Greenply Industries: Plywood Business Growing in Single-DigitsDokument8 SeitenGreenply Industries: Plywood Business Growing in Single-Digitssaran21Noch keine Bewertungen

- Busi97318 Corporate Finance Tutorial 7: MSC Finance and AccountingDokument48 SeitenBusi97318 Corporate Finance Tutorial 7: MSC Finance and AccountingSamir IsmailNoch keine Bewertungen

- Junaid Ass 3Dokument3 SeitenJunaid Ass 3Junaid AhmadNoch keine Bewertungen

- KNM Group Annual Report 2017 PDFDokument170 SeitenKNM Group Annual Report 2017 PDFgjangNoch keine Bewertungen

- Exam Practice Question Glori Fried Chicken Rima Puri v2 WZ AnswersDokument4 SeitenExam Practice Question Glori Fried Chicken Rima Puri v2 WZ AnswersJœ œNoch keine Bewertungen

- Studocu 12137811-1Dokument31 SeitenStudocu 12137811-1kristinejoy pacalNoch keine Bewertungen

- Public Final ExamDokument5 SeitenPublic Final Examsenbetotilahun8Noch keine Bewertungen

- The July 31Dokument4 SeitenThe July 31Douglas M. DougyNoch keine Bewertungen

- How To Prepare Projected Financial StatementsDokument4 SeitenHow To Prepare Projected Financial StatementsNamy Lyn GumameraNoch keine Bewertungen