Das könnte Ihnen auch gefallen

- Regional Rural Banks of India: Evolution, Performance and ManagementVon EverandRegional Rural Banks of India: Evolution, Performance and ManagementNoch keine Bewertungen

- Retail Banking Front Office Management Activity For HDFC Bank by Nisha Wadekar This Project Is Very Useful To StudentDokument51 SeitenRetail Banking Front Office Management Activity For HDFC Bank by Nisha Wadekar This Project Is Very Useful To Studentganeshkhale7052Noch keine Bewertungen

- Literature ReviewDokument7 SeitenLiterature ReviewAshu SharmaNoch keine Bewertungen

- Summer Internship Report On DIGITAL BANKING - HDFC Bank Ltd.Dokument24 SeitenSummer Internship Report On DIGITAL BANKING - HDFC Bank Ltd.Nayana ChuriwalaNoch keine Bewertungen

- Analysis of Product & Services of HDFC BANK LTD.Dokument93 SeitenAnalysis of Product & Services of HDFC BANK LTD.Sami ZamaNoch keine Bewertungen

- Comprative Analysis of Services Provided by HDFC and Axis BankDokument58 SeitenComprative Analysis of Services Provided by HDFC and Axis BankNitinAgnihotriNoch keine Bewertungen

- Project Report on"CASA" in HDFCDokument42 SeitenProject Report on"CASA" in HDFCRoshan Friendsforever100% (5)

- TJSBDokument59 SeitenTJSBMonik Maru Fakra He63% (8)

- Executive Summary: Siddheswar Co-Operative Bank, BijapurDokument13 SeitenExecutive Summary: Siddheswar Co-Operative Bank, BijapurSachin UmbarajeNoch keine Bewertungen

- Retail Banking An Over View of HDFC BankDokument69 SeitenRetail Banking An Over View of HDFC BankPrashant Patil0% (1)

- Axis BankDokument16 SeitenAxis BankRoshan KamathNoch keine Bewertungen

- "Financial Analysis of HDFC Bank": Symbiosis Centre For Distance Learning, PuneDokument69 Seiten"Financial Analysis of HDFC Bank": Symbiosis Centre For Distance Learning, PuneBheeshm Singh100% (1)

- THEJASWINI ProjectDokument112 SeitenTHEJASWINI Projectswamy yashuNoch keine Bewertungen

- SBI Internship ReportDokument14 SeitenSBI Internship ReportMashum AliNoch keine Bewertungen

- Credit Risk Management HDFC Project Report Mba FinanceDokument102 SeitenCredit Risk Management HDFC Project Report Mba FinanceNishant Kuradia0% (1)

- Corporate Identificatio and Competition Analysis: A Project Report ONDokument77 SeitenCorporate Identificatio and Competition Analysis: A Project Report ONmustkeem_qureshi7089Noch keine Bewertungen

- SBI Bank ProjectDokument150 SeitenSBI Bank Projectee23258Noch keine Bewertungen

- HDFC Bank LoansDokument75 SeitenHDFC Bank LoansSahil Sethi100% (2)

- CP of Sbi BankDokument4 SeitenCP of Sbi Bankharman singh0% (1)

- Bharti Summer Internship ReportDokument70 SeitenBharti Summer Internship ReportBhumika GuptaNoch keine Bewertungen

- Study On Retail Banking Transformations in India MBA FinaceDokument17 SeitenStudy On Retail Banking Transformations in India MBA FinaceChetan ChanneNoch keine Bewertungen

- HDFC Black Book - Print PDFDokument42 SeitenHDFC Black Book - Print PDFShruti PalekarNoch keine Bewertungen

- Union Bank of IndiaDokument53 SeitenUnion Bank of IndiaSonu DhangarNoch keine Bewertungen

- Comparative Study of Private and Public Sector BankDokument21 SeitenComparative Study of Private and Public Sector BankbuddysmbdNoch keine Bewertungen

- Bank of IndiaDokument49 SeitenBank of IndiaJasmeet Singh100% (1)

- Advance Product of SbiDokument20 SeitenAdvance Product of SbiSeKha RudiThongerNoch keine Bewertungen

- Literature ReviewDokument5 SeitenLiterature ReviewKiran VarsaniNoch keine Bewertungen

- A Study On Customer Satisfaction Towards The Net Banking Services of HDFC Bank in Lucknow CityDokument7 SeitenA Study On Customer Satisfaction Towards The Net Banking Services of HDFC Bank in Lucknow CityChandan Srivastava0% (1)

- HDFC Black Book 3 PDFDokument64 SeitenHDFC Black Book 3 PDFKarishma ThakurNoch keine Bewertungen

- HDFC ProfileDokument10 SeitenHDFC ProfilePunitha AradhyaNoch keine Bewertungen

- Sbi ProjectDokument91 SeitenSbi ProjectSanjeev BhatiaNoch keine Bewertungen

- HDFC Bank PPT 2Dokument18 SeitenHDFC Bank PPT 2Shri Mohan Chaudhary100% (2)

- Profile of SBIDokument15 SeitenProfile of SBIkarthikrishnaNoch keine Bewertungen

- Banking Project Topics-2Dokument4 SeitenBanking Project Topics-2Mike KukrejaNoch keine Bewertungen

- HDFCDokument61 SeitenHDFCpatyal20100% (1)

- A Project Report On History of SbiDokument57 SeitenA Project Report On History of SbiMitali AmagdavNoch keine Bewertungen

- Working Management of Axis BankDokument53 SeitenWorking Management of Axis BankAayushi Sharma50% (2)

- Project Report On HDFC BankDokument77 SeitenProject Report On HDFC BankRobin Arora100% (1)

- SUMMER TRAINING PROJECT REPORT ON Idbi BankDokument53 SeitenSUMMER TRAINING PROJECT REPORT ON Idbi BankTRAUN KULSHRESTHA86% (22)

- Bank of Baroda Summer Intership Project7Dokument78 SeitenBank of Baroda Summer Intership Project7Binita Kumari83% (6)

- Report On IDBI BankDokument9 SeitenReport On IDBI BankParth patelNoch keine Bewertungen

- Consumer Satisfaction On Nashik Merchamt BankDokument40 SeitenConsumer Satisfaction On Nashik Merchamt BankKunal Hire-Patil100% (2)

- A Compre Hensive Proje CT Re PortDokument126 SeitenA Compre Hensive Proje CT Re PortKAUSHLESH CHOUDHARYNoch keine Bewertungen

- An Analytical Study of "Financial Performance of Housing Development Financial Corporation (HDFC) "Dokument8 SeitenAn Analytical Study of "Financial Performance of Housing Development Financial Corporation (HDFC) "Kunal BagdeNoch keine Bewertungen

- Retail Loans ProjectDokument43 SeitenRetail Loans ProjectLeo SamNoch keine Bewertungen

- Retail Banking at HDFCDokument56 SeitenRetail Banking at HDFCutkarsh jaiswalNoch keine Bewertungen

- Report On Marketing at Central Bank of IndiaDokument51 SeitenReport On Marketing at Central Bank of IndiaArup SarkarNoch keine Bewertungen

- Impact of Digitalization For Customers of HDFC Bank: Post Graduate Diploma in ManagementDokument42 SeitenImpact of Digitalization For Customers of HDFC Bank: Post Graduate Diploma in ManagementJASMEET SINGHNoch keine Bewertungen

- DIGITALIZATION IN BANK HDFC BANk Final AditiDokument90 SeitenDIGITALIZATION IN BANK HDFC BANk Final AditiMaster PrintersNoch keine Bewertungen

- BIKRAM - Digital Banking-1Dokument86 SeitenBIKRAM - Digital Banking-1Anand GuptaNoch keine Bewertungen

- SCOPE OF DIGITALIZATION IN BANKING' HDFCDokument75 SeitenSCOPE OF DIGITALIZATION IN BANKING' HDFCMaster PrintersNoch keine Bewertungen

- E BankingDokument57 SeitenE BankingNitin HoodaNoch keine Bewertungen

- Kaveri - Online Banking - HDFCDokument43 SeitenKaveri - Online Banking - HDFCNaveen KNoch keine Bewertungen

- Contribution of Digital Towards Re-Kyc Bills and UfdDokument59 SeitenContribution of Digital Towards Re-Kyc Bills and UfdsachidanandNoch keine Bewertungen

- Study of Online Services Offered by BanksDokument34 SeitenStudy of Online Services Offered by Bankssarvesh dhatrakNoch keine Bewertungen

- Project WorkDokument33 SeitenProject WorkNAVEEN TYAGINoch keine Bewertungen

- HDFC NetBanking SynopsisDokument5 SeitenHDFC NetBanking SynopsisPranavi Paul Pandey100% (1)

- Research Project (Prateek Gulati)Dokument82 SeitenResearch Project (Prateek Gulati)prateekNoch keine Bewertungen

- Consumer Perception Towards E-Banking Services - 081252-1Dokument81 SeitenConsumer Perception Towards E-Banking Services - 081252-1prathamNoch keine Bewertungen

- Animals in SportDokument12 SeitenAnimals in SportAYUSHI GABANoch keine Bewertungen

- Ola and Uber Vs MeruDokument14 SeitenOla and Uber Vs MeruAYUSHI GABANoch keine Bewertungen

- Ayushi Gaba 18pgdm 010Dokument4 SeitenAyushi Gaba 18pgdm 010AYUSHI GABANoch keine Bewertungen

- British AirwaysDokument7 SeitenBritish AirwaysAYUSHI GABANoch keine Bewertungen

- EconomicsDokument11 SeitenEconomicsAYUSHI GABANoch keine Bewertungen

- Ayushi Gaba 18pgdm 010Dokument4 SeitenAyushi Gaba 18pgdm 010AYUSHI GABANoch keine Bewertungen

- Ayushi Gaba 18pgdm 010Dokument4 SeitenAyushi Gaba 18pgdm 010AYUSHI GABANoch keine Bewertungen

- Ayushi GabaDokument1 SeiteAyushi GabaAYUSHI GABANoch keine Bewertungen

- ''HR Outsourcing in India ResearchDokument77 Seiten''HR Outsourcing in India ResearchSami Zama100% (2)

- Doors Offer Il BagnoDokument1 SeiteDoors Offer Il Bagnosellitt ngNoch keine Bewertungen

- 2221 - Acct6328039 - Lkfa - TP1-W2-S3-R2 - 2602285150 - Amama Ira Amalia PriyonoDokument11 Seiten2221 - Acct6328039 - Lkfa - TP1-W2-S3-R2 - 2602285150 - Amama Ira Amalia PriyonoAmama AI APNoch keine Bewertungen

- Cerc 1Dokument53 SeitenCerc 1kasturishivaNoch keine Bewertungen

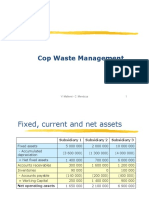

- Cop Waste Management SolutionDokument5 SeitenCop Waste Management SolutionPaul GhanimehNoch keine Bewertungen

- Trade Secrets PPT (By Aditya)Dokument19 SeitenTrade Secrets PPT (By Aditya)Aditya AgrawalNoch keine Bewertungen

- Case StudyDokument2 SeitenCase StudyCindy Graze EscaleraNoch keine Bewertungen

- BridgestoneDokument1 SeiteBridgestoneRam JainNoch keine Bewertungen

- 20 How Business Is Transacted Instock ExchangeDokument14 Seiten20 How Business Is Transacted Instock ExchangeSimranjeet SinghNoch keine Bewertungen

- Entrepreneurship and Economic DevelopmentDokument44 SeitenEntrepreneurship and Economic Developmentgosaye desalegn100% (1)

- 3 - Book of Prime EntryDokument69 Seiten3 - Book of Prime Entrynurzbiet8587Noch keine Bewertungen

- Software Project Management Unit-4 - 6 PDFDokument2 SeitenSoftware Project Management Unit-4 - 6 PDFgambler yeagerNoch keine Bewertungen

- Ifrs Us Gaap Ind As and Indian Gaap Similarities and DifferencesDokument4 SeitenIfrs Us Gaap Ind As and Indian Gaap Similarities and DifferencesDrpranav SaraswatNoch keine Bewertungen

- Nike Marketing MixDokument9 SeitenNike Marketing MixHarshit MaheshwariNoch keine Bewertungen

- Hapter 10: © 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/SteinbartDokument134 SeitenHapter 10: © 2008 Prentice Hall Business Publishing Accounting Information Systems, 11/e Romney/SteinbartRoristua PandianganNoch keine Bewertungen

- Ardelyn Madamecila TrabillaDokument3 SeitenArdelyn Madamecila TrabillaArdelyn TrabillaNoch keine Bewertungen

- Social Media Advertising by Niharika DagaDokument13 SeitenSocial Media Advertising by Niharika DagaNiharika dagaNoch keine Bewertungen

- The Systems Development Environment: True-False QuestionsDokument262 SeitenThe Systems Development Environment: True-False Questionslouisa_wanNoch keine Bewertungen

- 2023 BusinessKids Convention ReportDokument18 Seiten2023 BusinessKids Convention ReportClaudia Isabel MirelesNoch keine Bewertungen

- Substantive Procedures For Sales RevenueDokument5 SeitenSubstantive Procedures For Sales RevenuePubg DonNoch keine Bewertungen

- Globalisation and International MarketingDokument3 SeitenGlobalisation and International Marketinglovestruckboy04Noch keine Bewertungen

- GFR Chapter 6,7,8Dokument19 SeitenGFR Chapter 6,7,8asteeshNoch keine Bewertungen

- NTT 2011 CSR ReportDokument261 SeitenNTT 2011 CSR ReportcattleyajenNoch keine Bewertungen

- Human Resource Management (UST AY 2013-2014)Dokument3 SeitenHuman Resource Management (UST AY 2013-2014)Jie Lim Jareta100% (1)

- Letter of Motivation - ICLEIDokument1 SeiteLetter of Motivation - ICLEIZahara ApNoch keine Bewertungen

- T3TMD - Miscellaneous Deals - R10Dokument78 SeitenT3TMD - Miscellaneous Deals - R10KLB USERNoch keine Bewertungen

- Sub Contract AgreementDokument15 SeitenSub Contract AgreementJenifer Londeka NgcoboNoch keine Bewertungen

- ACCEPTANCE Nego 11.11.223Dokument10 SeitenACCEPTANCE Nego 11.11.223Rebecca TatadNoch keine Bewertungen

- Libro Azul de ApproDokument46 SeitenLibro Azul de ApproEduard MartiNoch keine Bewertungen

- 3 - Solution Guide - Short Term Budgeting AssignmentDokument3 Seiten3 - Solution Guide - Short Term Budgeting AssignmentEdward Glenn BaguiNoch keine Bewertungen