Das könnte Ihnen auch gefallen

- Coca Cola vs. CIRDokument1 SeiteCoca Cola vs. CIRmenlyn100% (4)

- 3M PhilippinesDokument2 Seiten3M PhilippinesKarl Vincent Raso100% (1)

- Eastern Telecommunications Phil Inc V CIR - DigestDokument1 SeiteEastern Telecommunications Phil Inc V CIR - DigestKate GaroNoch keine Bewertungen

- Cir Vs SC Johnson DigestDokument3 SeitenCir Vs SC Johnson DigestMarvin MagaipoNoch keine Bewertungen

- CIR v. CA and Castaneda GR 96016 October 17, 1991Dokument1 SeiteCIR v. CA and Castaneda GR 96016 October 17, 1991Vel JuneNoch keine Bewertungen

- Cir v. MeralcoDokument2 SeitenCir v. MeralcoKhaiye De Asis AggabaoNoch keine Bewertungen

- CIR Vs Seagate, GR 153866Dokument3 SeitenCIR Vs Seagate, GR 153866Mar Develos100% (1)

- 11 NDC V CIRDokument3 Seiten11 NDC V CIRTricia MontoyaNoch keine Bewertungen

- China Banking Corporation vs. CADokument1 SeiteChina Banking Corporation vs. CAArmstrong BosantogNoch keine Bewertungen

- Exxonmobil Petroleum and Chemical Holdings, Inc. - Phil. Branch vs. Commissioner of Internal RevenueDokument2 SeitenExxonmobil Petroleum and Chemical Holdings, Inc. - Phil. Branch vs. Commissioner of Internal Revenueiwamawi100% (1)

- CIR Vs Bank of CommerceDokument2 SeitenCIR Vs Bank of CommerceAster Beane AranetaNoch keine Bewertungen

- City of Baguio v. Fortunato de Leon GR L-24756Dokument1 SeiteCity of Baguio v. Fortunato de Leon GR L-24756Charles Roger RayaNoch keine Bewertungen

- Fisher V TrinidadDokument2 SeitenFisher V TrinidadEva Marie Gutierrez Cantero100% (1)

- Vidal de Roces vs. Posadas (Case Digest)Dokument1 SeiteVidal de Roces vs. Posadas (Case Digest)Vince Leido100% (2)

- CIR vs. CTA (And Smith Kline & French Overseas Co.)Dokument1 SeiteCIR vs. CTA (And Smith Kline & French Overseas Co.)scartoneros_1Noch keine Bewertungen

- PAPER INDUSTRIES CORPORATION OF THE PHILIPPINES (PICOP) v. CA, CIR and CTA, G.R. Nos. 106949-50 (1995)Dokument2 SeitenPAPER INDUSTRIES CORPORATION OF THE PHILIPPINES (PICOP) v. CA, CIR and CTA, G.R. Nos. 106949-50 (1995)Elaine Belle OgayonNoch keine Bewertungen

- Tang Ho Vs The Board of Tax AppealsDokument2 SeitenTang Ho Vs The Board of Tax AppealsRea RomeroNoch keine Bewertungen

- Cir vs. Pineda, 21 Scra 105 PDFDokument1 SeiteCir vs. Pineda, 21 Scra 105 PDFJo DevisNoch keine Bewertungen

- Vidal de Roces Vs PosadasDokument3 SeitenVidal de Roces Vs PosadasMark Gabriel B. MarangaNoch keine Bewertungen

- CIR Vs CA & CastanedaDokument1 SeiteCIR Vs CA & CastanedaArmstrong BosantogNoch keine Bewertungen

- Aguinaldo Industries v. CIRDokument1 SeiteAguinaldo Industries v. CIRTon Ton CananeaNoch keine Bewertungen

- MARUBENI Vs CIR TAXDokument2 SeitenMARUBENI Vs CIR TAXLemuel Angelo M. EleccionNoch keine Bewertungen

- Delpher Trades Corporation vs. IACDokument1 SeiteDelpher Trades Corporation vs. IACGeoanne Battad Beringuela100% (1)

- CIR v. LEDNICKY, G.R. Nos. L-18169, L-18262 & L-21434, 11 SCRA 603, 31 July 1964Dokument3 SeitenCIR v. LEDNICKY, G.R. Nos. L-18169, L-18262 & L-21434, 11 SCRA 603, 31 July 1964Pamela Camille Barredo100% (1)

- G.R. No. L-53961Dokument1 SeiteG.R. No. L-53961Jannie Ann DayandayanNoch keine Bewertungen

- Collector v. LaraDokument2 SeitenCollector v. LaraJaypoll DiazNoch keine Bewertungen

- 24 Pirovano v. CIR (14 SCRA 232)Dokument8 Seiten24 Pirovano v. CIR (14 SCRA 232)Perry YapNoch keine Bewertungen

- Team Sual Corporation v. CIRDokument2 SeitenTeam Sual Corporation v. CIRAlyk Tumayan Calion100% (1)

- 13 Vegetable Oil Corp V TrinidadDokument2 Seiten13 Vegetable Oil Corp V TrinidadRocky GuzmanNoch keine Bewertungen

- 05 - Dison vs. PosadasDokument2 Seiten05 - Dison vs. Posadascool_peach100% (1)

- CM Hoskins V CIRDokument2 SeitenCM Hoskins V CIRSui100% (4)

- Coll. v. Henderson, 1 SCRA 649Dokument2 SeitenColl. v. Henderson, 1 SCRA 649Homer SimpsonNoch keine Bewertungen

- CIR v. Mirant PagbilaoDokument4 SeitenCIR v. Mirant Pagbilaoamareia yap100% (1)

- Panasonic Imaging Corp. Vs CIRDokument1 SeitePanasonic Imaging Corp. Vs CIRbrendamanganaanNoch keine Bewertungen

- Gutierrez vs. CIR 1957: Taxation I Case Digest CompilationDokument2 SeitenGutierrez vs. CIR 1957: Taxation I Case Digest CompilationGyrsyl Jaisa GuerreroNoch keine Bewertungen

- Dizon Vs Posadas JRDokument1 SeiteDizon Vs Posadas JRArahbells100% (1)

- Bantillo - CIR Vs PNBDokument3 SeitenBantillo - CIR Vs PNBAto TejaNoch keine Bewertungen

- Roxas v. CTADokument2 SeitenRoxas v. CTAJf ManejaNoch keine Bewertungen

- Hilado vs. CIRDokument1 SeiteHilado vs. CIRAlan GultiaNoch keine Bewertungen

- Collector v. de LaraDokument3 SeitenCollector v. de Larajehua100% (1)

- IBC Vs Amarilla Tax Case DigestDokument3 SeitenIBC Vs Amarilla Tax Case DigestCJNoch keine Bewertungen

- CIR V Pilipinas ShellDokument4 SeitenCIR V Pilipinas ShellCedric Enriquez100% (2)

- COMMISSIONER OF INTERNAL REVENUE, Petitioner, vs. CITYTRUST INVESTMENT PHILS., INC., Respondent.Dokument1 SeiteCOMMISSIONER OF INTERNAL REVENUE, Petitioner, vs. CITYTRUST INVESTMENT PHILS., INC., Respondent.Charles Roger Raya100% (1)

- Cir V Benguet DigestDokument1 SeiteCir V Benguet DigestAgnes GamboaNoch keine Bewertungen

- CIR V SolidbankDokument14 SeitenCIR V Solidbankrj_guzmanNoch keine Bewertungen

- Basilan Estates vs. CirDokument1 SeiteBasilan Estates vs. CirLizzy WayNoch keine Bewertungen

- Madrigal Vs RaffertyDokument2 SeitenMadrigal Vs RaffertyKirs Tie100% (1)

- Aguinaldo Industries Corporation vs. Commissioner of Internal Revenue Services Actually RenderedDokument2 SeitenAguinaldo Industries Corporation vs. Commissioner of Internal Revenue Services Actually RenderedCharmila SiplonNoch keine Bewertungen

- Bpi V Cir DigestDokument3 SeitenBpi V Cir DigestkathrynmaydevezaNoch keine Bewertungen

- Borja Vs GellaDokument4 SeitenBorja Vs Gelladwight yuNoch keine Bewertungen

- C.M. Hoskins & Co., Inc. vs. Commissioner of Internal RevenueDokument1 SeiteC.M. Hoskins & Co., Inc. vs. Commissioner of Internal RevenueAlljun SerenadoNoch keine Bewertungen

- Bonifacio Water Corp V CIR. Case DigestDokument2 SeitenBonifacio Water Corp V CIR. Case DigestIan Jala CalmaresNoch keine Bewertungen

- CIR vs. Pilipinas ShellDokument3 SeitenCIR vs. Pilipinas ShellArchie Torres88% (8)

- CIR v. Isabela Cultural Corp.Dokument4 SeitenCIR v. Isabela Cultural Corp.kathrynmaydevezaNoch keine Bewertungen

- Philamlife vs. CIRDokument1 SeitePhilamlife vs. CIRMona LizaNoch keine Bewertungen

- Philippine Acetylene Co. Inc vs. CirDokument2 SeitenPhilippine Acetylene Co. Inc vs. Cirbrendamanganaan100% (1)

- Pirovano V CommissionerDokument5 SeitenPirovano V CommissionerGale Calaycay LaenoNoch keine Bewertungen

- Pirovano-vs.-Commissioner-of-Internal-RevenueDokument19 SeitenPirovano-vs.-Commissioner-of-Internal-RevenueChristle CorpuzNoch keine Bewertungen

- Petitioners-Appellants Respondent-Appellee Angel S. Gamboa Solicitor GeneralDokument8 SeitenPetitioners-Appellants Respondent-Appellee Angel S. Gamboa Solicitor GeneralHazel SegoviaNoch keine Bewertungen

- 2 Pirovana Vs CIRDokument7 Seiten2 Pirovana Vs CIRAnonymous kCX0FoNoch keine Bewertungen

- F - CIR Vs LaraDokument1 SeiteF - CIR Vs Laraceilo cobo50% (2)

- C - Tang Ho Vs CA CirDokument1 SeiteC - Tang Ho Vs CA Circeilo coboNoch keine Bewertungen

- H - Gallardo Vs MoralesDokument1 SeiteH - Gallardo Vs Moralesceilo coboNoch keine Bewertungen

- Special Proceedings Cases PG 1 To 100Dokument244 SeitenSpecial Proceedings Cases PG 1 To 100ceilo coboNoch keine Bewertungen

- GR 191495 CaseDokument9 SeitenGR 191495 Caseceilo coboNoch keine Bewertungen

- Sunga-Chan V CADokument3 SeitenSunga-Chan V CAceilo coboNoch keine Bewertungen

- 2nd CasesDokument16 Seiten2nd Casesceilo coboNoch keine Bewertungen

- Special Proceedings Cases # 167,168,169,170, and 171Dokument4 SeitenSpecial Proceedings Cases # 167,168,169,170, and 171ceilo cobo0% (1)

- Public Forests Reforestation Charges Nature of Fund CollectedDokument4 SeitenPublic Forests Reforestation Charges Nature of Fund Collectedceilo coboNoch keine Bewertungen

- Printed Digest Maceda vs. Macaraig, G.R. No. 88291Dokument5 SeitenPrinted Digest Maceda vs. Macaraig, G.R. No. 88291ceilo coboNoch keine Bewertungen

- Succession Tolentino Balane PDFDokument90 SeitenSuccession Tolentino Balane PDFceilo coboNoch keine Bewertungen

- A1 CIR V Eastern TelecommunicationDokument8 SeitenA1 CIR V Eastern Telecommunicationceilo coboNoch keine Bewertungen

- Word Analogy TestDokument1 SeiteWord Analogy Testceilo coboNoch keine Bewertungen

- 5837 Gallemit V TabiliranDokument2 Seiten5837 Gallemit V Tabiliranceilo coboNoch keine Bewertungen

- Verendia vs. Court of Appeals: 418 Supreme Court Reports AnnotatedDokument6 SeitenVerendia vs. Court of Appeals: 418 Supreme Court Reports Annotatedceilo coboNoch keine Bewertungen

- A9 COCOFED vs. PCGG, 178 SCRA 236 (1989) PDFDokument8 SeitenA9 COCOFED vs. PCGG, 178 SCRA 236 (1989) PDFceilo coboNoch keine Bewertungen

- Fua Cam Lu V Yap FaucoDokument2 SeitenFua Cam Lu V Yap Faucoceilo coboNoch keine Bewertungen

- Buying & SellingDokument4 SeitenBuying & SellingYolanda DescallarNoch keine Bewertungen

- Report On ImportDokument21 SeitenReport On ImportER.Master Ajay RimalNoch keine Bewertungen

- Smart Platina Assure Brochure FinalDokument12 SeitenSmart Platina Assure Brochure Finalsksen007Noch keine Bewertungen

- An Empirical Analysis of Economic Policies, Institutions, and Investment Nexus in PakistanDokument20 SeitenAn Empirical Analysis of Economic Policies, Institutions, and Investment Nexus in PakistanNaveed SandhuNoch keine Bewertungen

- Expectation InvestingDokument35 SeitenExpectation InvestingThanh Tuấn100% (2)

- Can Hong Kong Port Remain Her Competitiveness?Dokument24 SeitenCan Hong Kong Port Remain Her Competitiveness?tkpst99238Noch keine Bewertungen

- Hotel BookingDokument2 SeitenHotel BookingdevbnwNoch keine Bewertungen

- Psm1 (New - Deg) - 0910 - v1.3 Nhs Bursary Application FormDokument26 SeitenPsm1 (New - Deg) - 0910 - v1.3 Nhs Bursary Application FormAZZIEAKHTAR100% (1)

- Eunice B. Rojas Merlinda P. Maata: School Principal III Municipal MayorDokument4 SeitenEunice B. Rojas Merlinda P. Maata: School Principal III Municipal MayorCherrie Lou Uba100% (1)

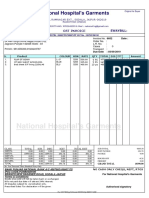

- National Hospital's GarmentsDokument1 SeiteNational Hospital's GarmentsShekhar GuptaNoch keine Bewertungen

- Tax Exemption SRO NO 5 Private Power Generation CompanyDokument1 SeiteTax Exemption SRO NO 5 Private Power Generation CompanyAshraful RaselNoch keine Bewertungen

- Public Finance List of Imp TopicsDokument18 SeitenPublic Finance List of Imp TopicsArslan AhmadNoch keine Bewertungen

- Caltex Philippines, Inc. V COA (1992)Dokument3 SeitenCaltex Philippines, Inc. V COA (1992)Anonymous wD8hMIPxJNoch keine Bewertungen

- TB January To December 2022Dokument102 SeitenTB January To December 2022Dhvani PanchalNoch keine Bewertungen

- Tax Replication From SAP CRM To SAP ECC - CRM - SCN WikiDokument10 SeitenTax Replication From SAP CRM To SAP ECC - CRM - SCN WikiloribeNoch keine Bewertungen

- Introduction To Production ManagementDokument158 SeitenIntroduction To Production ManagementAsmita ShilpiNoch keine Bewertungen

- 10 - Pas 20 - Government GrantsDokument4 Seiten10 - Pas 20 - Government GrantsAbbygail Michelle TalaveraNoch keine Bewertungen

- Local Government Code of 1991Dokument213 SeitenLocal Government Code of 1991adonaiaslaronaNoch keine Bewertungen

- 2017 31 The Peshawar Development Authority Act 2017Dokument21 Seiten2017 31 The Peshawar Development Authority Act 2017Naveed Aman SafiNoch keine Bewertungen

- Afisco Insurance Corporation Vs Court of AppealsDokument2 SeitenAfisco Insurance Corporation Vs Court of AppealsLorelieNoch keine Bewertungen

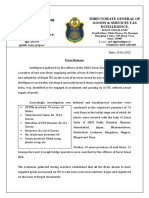

- Directorate General of Goods & Services Tax Intelligence,: Press ReleaseDokument2 SeitenDirectorate General of Goods & Services Tax Intelligence,: Press ReleaseAmit TiwariNoch keine Bewertungen

- A Statistical Account of Bengal Vol 14 GoogleBooksID c44BAAAAQAAJDokument415 SeitenA Statistical Account of Bengal Vol 14 GoogleBooksID c44BAAAAQAAJShah RulNoch keine Bewertungen

- 142-Heng Tong Textiles Co., Inc. v. CIR, August 26, 1968Dokument2 Seiten142-Heng Tong Textiles Co., Inc. v. CIR, August 26, 1968Jopan SJNoch keine Bewertungen

- Nicollet Mall Economic Impact StudyDokument9 SeitenNicollet Mall Economic Impact Studybpjohnson81Noch keine Bewertungen

- Proc No 226 2000 Petroleum Operations Income Tax AmendmentDokument1 SeiteProc No 226 2000 Petroleum Operations Income Tax AmendmentbiniNoch keine Bewertungen

- Earnings Statement: D Lane Agency Inc. 3348 Peachtree RD NE Suite 700 Atlanta, GA 30326Dokument1 SeiteEarnings Statement: D Lane Agency Inc. 3348 Peachtree RD NE Suite 700 Atlanta, GA 30326Muhammad AdeelNoch keine Bewertungen

- Mahatma Education Society's Pillai College of Arts, Commerce and Science (Autonomous) New Panvel ISO 9001:2015 CertifiedDokument17 SeitenMahatma Education Society's Pillai College of Arts, Commerce and Science (Autonomous) New Panvel ISO 9001:2015 CertifiedAbizer KachwalaNoch keine Bewertungen

- Political Law: Chanrobles Internet Bar Review: Chanrobles Professional Review, IncDokument37 SeitenPolitical Law: Chanrobles Internet Bar Review: Chanrobles Professional Review, IncDeeby PortacionNoch keine Bewertungen

- The Kali Age in The Early Medieval IndiaDokument4 SeitenThe Kali Age in The Early Medieval IndiaRamita Udayashankar100% (5)

- Lesson 6 - Construction Equipment, Maintenance and OperationDokument43 SeitenLesson 6 - Construction Equipment, Maintenance and OperationJubillee MagsinoNoch keine Bewertungen