Das könnte Ihnen auch gefallen

- Affordable Housing Unit Design OptimizationDokument1 SeiteAffordable Housing Unit Design OptimizationDhruval Jignesh PatelNoch keine Bewertungen

- 43' 13.11 floor plan layoutDokument1 Seite43' 13.11 floor plan layoutDhruval Jignesh PatelNoch keine Bewertungen

- Primavera ExerciseDokument36 SeitenPrimavera ExerciseSur Jis100% (8)

- Fround Floor OfficeDokument1 SeiteFround Floor OfficeDhruval Jignesh PatelNoch keine Bewertungen

- CPM TimeDokument9 SeitenCPM Timeshivani chauhanNoch keine Bewertungen

- Conference HallDokument1 SeiteConference HallDhruval Jignesh PatelNoch keine Bewertungen

- Construction ActivitiesDokument20 SeitenConstruction ActivitiesErika Kirby100% (19)

- Works Sub Works Materials and Machineries Details Time Duration Typology of Workers RequiredDokument1 SeiteWorks Sub Works Materials and Machineries Details Time Duration Typology of Workers RequiredDhruval Jignesh PatelNoch keine Bewertungen

- Book 1Dokument19 SeitenBook 1Dhruval Jignesh PatelNoch keine Bewertungen

- Planning Construction Project MappingDokument3 SeitenPlanning Construction Project MappingMarvin M. GamboaNoch keine Bewertungen

- Design BriefDokument5 SeitenDesign BriefDhruval Jignesh PatelNoch keine Bewertungen

- Planning Construction Project MappingDokument3 SeitenPlanning Construction Project MappingMarvin M. GamboaNoch keine Bewertungen

- Option 1 PDFDokument1 SeiteOption 1 PDFDhruval Jignesh PatelNoch keine Bewertungen

- First Floor ToiletDokument1 SeiteFirst Floor ToiletDhruval Jignesh PatelNoch keine Bewertungen

- Staff Lunch Hall Mezzanine Op1Dokument1 SeiteStaff Lunch Hall Mezzanine Op1Dhruval Jignesh PatelNoch keine Bewertungen

- Staff Lunch HalllDokument1 SeiteStaff Lunch HalllDhruval Jignesh PatelNoch keine Bewertungen

- Staff Lunch Hall Mezzanine Op2Dokument1 SeiteStaff Lunch Hall Mezzanine Op2Dhruval Jignesh PatelNoch keine Bewertungen

- SCHEDULE1Dokument1 SeiteSCHEDULE1Dhruval Jignesh PatelNoch keine Bewertungen

- Option 4 PDFDokument1 SeiteOption 4 PDFDhruval Jignesh PatelNoch keine Bewertungen

- Option 4Dokument1 SeiteOption 4Dhruval Jignesh PatelNoch keine Bewertungen

- Option 2 PDFDokument1 SeiteOption 2 PDFDhruval Jignesh PatelNoch keine Bewertungen

- Option 3Dokument1 SeiteOption 3Dhruval Jignesh PatelNoch keine Bewertungen

- Goibibo PDFDokument2 SeitenGoibibo PDFDhruval Jignesh PatelNoch keine Bewertungen

- Option 2Dokument1 SeiteOption 2Dhruval Jignesh PatelNoch keine Bewertungen

- Option 2Dokument1 SeiteOption 2Dhruval Jignesh PatelNoch keine Bewertungen

- 71 72 - First Floor Plan 1Dokument1 Seite71 72 - First Floor Plan 1Dhruval Jignesh PatelNoch keine Bewertungen

- Option 1Dokument1 SeiteOption 1Dhruval Jignesh PatelNoch keine Bewertungen

- Best Practice IndustrialDokument60 SeitenBest Practice Industrialplienovyras100% (3)

- Sketch Up 2018 Ref Card WinDokument1 SeiteSketch Up 2018 Ref Card WinEko MercuryNoch keine Bewertungen

- Design & Comparison of Various Types of Industrial BuildingsDokument17 SeitenDesign & Comparison of Various Types of Industrial BuildingsAnonymous UibQYvc6Noch keine Bewertungen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (265)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (119)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- FEBTC vs. Querimit ruling on CD paymentDokument1 SeiteFEBTC vs. Querimit ruling on CD paymentFayda Cariaga100% (3)

- The Bank of Punjab Internship ReportDokument76 SeitenThe Bank of Punjab Internship Reportbbaahmad89100% (4)

- Cardiff Cash Management V2.0Dokument108 SeitenCardiff Cash Management V2.0elsa7er2000Noch keine Bewertungen

- Promissory NoteDokument2 SeitenPromissory NoteMario Ryan Lauzon91% (23)

- Saving Account Analysis and ComparisonDokument76 SeitenSaving Account Analysis and ComparisonPrabhakar RahulNoch keine Bewertungen

- 2034 Glyn CT New Water BillDokument2 Seiten2034 Glyn CT New Water BillAce MereriaNoch keine Bewertungen

- Precision Drilling Announces Middle East New Build Award and Proposed Private OfferingDokument4 SeitenPrecision Drilling Announces Middle East New Build Award and Proposed Private OfferingzNoch keine Bewertungen

- Study of Non Performing Assets in Bank of Maharashtra.Dokument74 SeitenStudy of Non Performing Assets in Bank of Maharashtra.Arun Savukar60% (10)

- ExxxxxxDokument2 SeitenExxxxxxGuiness DeguzmanNoch keine Bewertungen

- The Evolution and Functions of Commercial BanksDokument26 SeitenThe Evolution and Functions of Commercial Banksabdu;l khalidNoch keine Bewertungen

- Indian Overseas Bank PO 2009 Solved Question PaperDokument8 SeitenIndian Overseas Bank PO 2009 Solved Question Paperkapeed_supNoch keine Bewertungen

- FINEX Board Resolutions SummaryDokument14 SeitenFINEX Board Resolutions SummaryciryajamNoch keine Bewertungen

- Deed of Assignment: This Deed of Assignment Is Made at Pune On This TH Day of The Month of July 2014Dokument9 SeitenDeed of Assignment: This Deed of Assignment Is Made at Pune On This TH Day of The Month of July 2014mukund100% (1)

- Course Outline FINA 482 Winter 21 DIARRA - GDokument8 SeitenCourse Outline FINA 482 Winter 21 DIARRA - GpopaNoch keine Bewertungen

- Audit of Cash and Cash EquivalentsDokument2 SeitenAudit of Cash and Cash EquivalentsWawex Davis100% (1)

- Global Insurance+ Review 2012 and Outlook 2013 14Dokument36 SeitenGlobal Insurance+ Review 2012 and Outlook 2013 14Harry CerqueiraNoch keine Bewertungen

- How to add Primary TradelinesDokument18 SeitenHow to add Primary Tradelinesmatt96% (82)

- Fee Based Activity in India BanksDokument12 SeitenFee Based Activity in India BanksMu'ammar RizqiNoch keine Bewertungen

- United States v. Lim BuancoDokument5 SeitenUnited States v. Lim BuancoJolas E. BrutasNoch keine Bewertungen

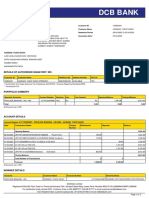

- DCB Bank: Statement of AccountDokument2 SeitenDCB Bank: Statement of AccounthasnainNoch keine Bewertungen

- Application, Tuition & Fees at Les Roches Hotel Management SchoolDokument2 SeitenApplication, Tuition & Fees at Les Roches Hotel Management SchoolShoaib ZaheerNoch keine Bewertungen

- False Alarm Bjorn LomborgDokument2 SeitenFalse Alarm Bjorn LomborgGraham DawsonNoch keine Bewertungen

- Questionnaire Final PDFDokument4 SeitenQuestionnaire Final PDFnidin johny100% (1)

- Annexure - 2 COS 38 Joint Hindu Family LetterDokument2 SeitenAnnexure - 2 COS 38 Joint Hindu Family LetterRahul Kumar50% (2)

- Financing Your: Massachusetts Institute of TechnologyDokument12 SeitenFinancing Your: Massachusetts Institute of TechnologyTruong CaiNoch keine Bewertungen

- Haldiram Foods International LTD 2005Dokument10 SeitenHaldiram Foods International LTD 2005Saurabh PatilNoch keine Bewertungen

- Customer Satisfaction Key to Banking SuccessDokument40 SeitenCustomer Satisfaction Key to Banking Successnavdeep2309Noch keine Bewertungen

- Sanction Letter CustDokument1 SeiteSanction Letter CustSanjay SolankiNoch keine Bewertungen

- RSM230 Midterm Study NotesDokument36 SeitenRSM230 Midterm Study Noteshugocheung7Noch keine Bewertungen