Das könnte Ihnen auch gefallen

- Chapter 7 Loans ReceivableDokument12 SeitenChapter 7 Loans ReceivableJohn Fraleigh Dagohoy Carillo100% (1)

- Module 2d Loan ReceivableDokument24 SeitenModule 2d Loan ReceivableChen HaoNoch keine Bewertungen

- Loans Receivable Origination FeesDokument15 SeitenLoans Receivable Origination FeesTurksNoch keine Bewertungen

- NR EditedDokument46 SeitenNR Editedirish59% (22)

- Problem 6-8 Answer A Savage CompanyDokument6 SeitenProblem 6-8 Answer A Savage CompanyJurie BalandacaNoch keine Bewertungen

- IntAcc 6-3Dokument1 SeiteIntAcc 6-3Shirley Cortez-David100% (3)

- Remarkable Company - Audit On ReceivablesDokument2 SeitenRemarkable Company - Audit On ReceivablesShr BnNoch keine Bewertungen

- Chapter 5Dokument21 SeitenChapter 5XENA LOPEZ100% (1)

- Ia RF NDDokument75 SeitenIa RF NDKimberly Quin Cañas83% (12)

- C3Dokument16 SeitenC3Aaliyah Manuel100% (1)

- On June 1 AcctDokument5 SeitenOn June 1 AcctMelody Bautista100% (1)

- Adjust Accounts Receivable, Allowances and Notes ReceivableDokument6 SeitenAdjust Accounts Receivable, Allowances and Notes ReceivablekrizzmaaaayNoch keine Bewertungen

- Trade and Other Receivables 1. On December 31, 2013, The Accounts Receivable of Harem Company Had A Balance ofDokument11 SeitenTrade and Other Receivables 1. On December 31, 2013, The Accounts Receivable of Harem Company Had A Balance ofJude SantosNoch keine Bewertungen

- IA1 CH 4 & 5 AR and Estimation DA 2020Dokument86 SeitenIA1 CH 4 & 5 AR and Estimation DA 2020Jm Sevalla88% (8)

- Intermediate 1A: Problem CompilationDokument24 SeitenIntermediate 1A: Problem CompilationPatricia Nicole Barrios100% (3)

- Step 1 Bad Debts: Particulars Amount (P)Dokument2 SeitenStep 1 Bad Debts: Particulars Amount (P)XxxxxNoch keine Bewertungen

- Problem 3-3 Ajusted Book Balance Checks Drawn: Bank Statement Balance Per BankDokument3 SeitenProblem 3-3 Ajusted Book Balance Checks Drawn: Bank Statement Balance Per BankNika Bautista100% (2)

- Ia CH 6 & 7 NR LR 2020Dokument112 SeitenIa CH 6 & 7 NR LR 2020Jm Sevalla57% (14)

- Bleak Company Requirement A Debit Credit Requirement BDokument2 SeitenBleak Company Requirement A Debit Credit Requirement BAnonn100% (1)

- Vain Company Requirement: Prepare Journal Entries On The Books of Assignor Debit CreditDokument1 SeiteVain Company Requirement: Prepare Journal Entries On The Books of Assignor Debit CreditAnonnNoch keine Bewertungen

- Receivables Quiz (ARNR) AK PDFDokument5 SeitenReceivables Quiz (ARNR) AK PDFNeil Vincent Boco86% (7)

- Seatwork 2B ASSIGNDokument5 SeitenSeatwork 2B ASSIGNYzzabel Denise L. Tolentino100% (1)

- 500,000 Demand Deposit 4,000,000: Activity 2 - ProblemsDokument7 Seiten500,000 Demand Deposit 4,000,000: Activity 2 - ProblemsSaclao John Mark GalangNoch keine Bewertungen

- Chapter 5 Est. of Doubtful AcctDokument11 SeitenChapter 5 Est. of Doubtful AcctXENA LOPEZNoch keine Bewertungen

- Pittance Company Requirement: Prepare Journal Entries To Record The Transactions Debit CreditDokument23 SeitenPittance Company Requirement: Prepare Journal Entries To Record The Transactions Debit CreditAnonnNoch keine Bewertungen

- Affectionate CompanyDokument1 SeiteAffectionate CompanyAnonnNoch keine Bewertungen

- ACC 101 - NR Assignment SolutionDokument6 SeitenACC 101 - NR Assignment SolutionAdyangNoch keine Bewertungen

- Chameleon Company Requirement1 Debit CreditDokument3 SeitenChameleon Company Requirement1 Debit CreditAnonnNoch keine Bewertungen

- Chapter 8 & 9 AssignmentDokument8 SeitenChapter 8 & 9 AssignmentSamantha Charlize Vizconde67% (3)

- Cabael-Ae109-Proof of CashDokument4 SeitenCabael-Ae109-Proof of CashJanine MadriagaNoch keine Bewertungen

- Post-Test 2 Receivables Answer KeyDokument9 SeitenPost-Test 2 Receivables Answer KeyJOSCEL SYJONGTIANNoch keine Bewertungen

- " Represents Only Claims Arising From Sale ofDokument3 Seiten" Represents Only Claims Arising From Sale ofprecious2lojaNoch keine Bewertungen

- Computation:: Freeway Company Requirement1: Books of Motorway Company Debit CreditDokument2 SeitenComputation:: Freeway Company Requirement1: Books of Motorway Company Debit CreditAnonn100% (1)

- This Study Resource Was: Chapter 18: Accounts ReceivableDokument7 SeitenThis Study Resource Was: Chapter 18: Accounts ReceivableXENA LOPEZNoch keine Bewertungen

- Required Ending Allowance For Doubtful AccountsDokument4 SeitenRequired Ending Allowance For Doubtful AccountsAngelica SamonteNoch keine Bewertungen

- Chapter 11 Answers RepportDokument12 SeitenChapter 11 Answers RepportJudy56% (16)

- Intermediate Accounting 1 (Far 3) Accounting For Trade and Other ReceivablesDokument6 SeitenIntermediate Accounting 1 (Far 3) Accounting For Trade and Other ReceivablesJennilyn BercasioNoch keine Bewertungen

- Quarantine Company, A Manufacturer of Small Tools, Provided The Following Information For The Year Ended December 31, 2019Dokument9 SeitenQuarantine Company, A Manufacturer of Small Tools, Provided The Following Information For The Year Ended December 31, 2019Ann louNoch keine Bewertungen

- Chapter 2 Last PartDokument11 SeitenChapter 2 Last PartXENA LOPEZ100% (2)

- Journal Entries for Petty Cash Fund SystemsDokument2 SeitenJournal Entries for Petty Cash Fund SystemsMae JessaNoch keine Bewertungen

- Note Receivable Part 2Dokument7 SeitenNote Receivable Part 2Carlo VillanNoch keine Bewertungen

- SHARE BASED PAYMENTS PROBLEMS SOLVEDDokument80 SeitenSHARE BASED PAYMENTS PROBLEMS SOLVEDjay1ar1guyena100% (2)

- Accounts ReceivableDokument6 SeitenAccounts ReceivableNerish PlazaNoch keine Bewertungen

- Romela Company (Gross Method)Dokument2 SeitenRomela Company (Gross Method)AnonnNoch keine Bewertungen

- 6-4 Gullible Company Req 1Dokument2 Seiten6-4 Gullible Company Req 1mercyvienhoNoch keine Bewertungen

- Bak ReconDokument1 SeiteBak ReconFlorimar Lagda100% (1)

- Bigotry Company Proof of CashDokument4 SeitenBigotry Company Proof of CashGee Lysa Pascua VilbarNoch keine Bewertungen

- Proof of Cash ProblemDokument4 SeitenProof of Cash ProblemHtiduj Oretubag50% (4)

- 1 Cash and Cash Equivalents 3Dokument14 Seiten1 Cash and Cash Equivalents 3Abegail AdoraNoch keine Bewertungen

- Problem 5-4 5-5Dokument4 SeitenProblem 5-4 5-5Jicelle MendozaNoch keine Bewertungen

- Machete Company Requirement: Prepare Journal Entries Debit CreditDokument1 SeiteMachete Company Requirement: Prepare Journal Entries Debit CreditAnonnNoch keine Bewertungen

- Chapter 14 AnswersevenDokument4 SeitenChapter 14 AnswersevenJulianne Mejia100% (1)

- Notes ReceivableDokument2 SeitenNotes ReceivableGee Lysa Pascua VilbarNoch keine Bewertungen

- Accounting for Bad Debts MethodsDokument5 SeitenAccounting for Bad Debts Methodshoneyjoy salapantanNoch keine Bewertungen

- Actg 431 Quiz Week 7 Practical Accounting I (Part II) Inventories QuizDokument4 SeitenActg 431 Quiz Week 7 Practical Accounting I (Part II) Inventories QuizMarilou Arcillas PanisalesNoch keine Bewertungen

- S1.16 - Receivable Financing - StudentDokument8 SeitenS1.16 - Receivable Financing - StudentCyndy Villapando100% (1)

- Loans ReceivableDokument48 SeitenLoans ReceivableJoshua PaliwagNoch keine Bewertungen

- Loan Receivable Measurement and ImpairmentDokument10 SeitenLoan Receivable Measurement and Impairmentjustine cabanaNoch keine Bewertungen

- CHAPTER 9 Intermediate Acctng 1Dokument46 SeitenCHAPTER 9 Intermediate Acctng 1Tessang OnongenNoch keine Bewertungen

- Task No. 17 Loans ReceivableDokument33 SeitenTask No. 17 Loans ReceivableChamie CariñoNoch keine Bewertungen

- Edmodo 2Dokument5 SeitenEdmodo 2mattNoch keine Bewertungen

- 4 Speeches Part 2Dokument10 Seiten4 Speeches Part 2mattNoch keine Bewertungen

- 4 SpeechesDokument12 Seiten4 SpeechesmattNoch keine Bewertungen

- Assignment C7Dokument4 SeitenAssignment C7matt100% (1)

- Social Media SpeechDokument1 SeiteSocial Media SpeechmattNoch keine Bewertungen

- Job skills self-assessmentDokument2 SeitenJob skills self-assessmentmattNoch keine Bewertungen

- ICICI Bank Moratorium FAQsDokument8 SeitenICICI Bank Moratorium FAQsCNBCTV18 DigitalNoch keine Bewertungen

- ICICI Bank Notice 617005044500Dokument2 SeitenICICI Bank Notice 617005044500Elan ThamizhNoch keine Bewertungen

- Roman Coins Marked CountermarksDokument3 SeitenRoman Coins Marked CountermarksSvetlozar StoyanovNoch keine Bewertungen

- Accounting September Memo 2016Dokument18 SeitenAccounting September Memo 2016Jester LabanNoch keine Bewertungen

- Detailed Solutions To Problem 5Dokument3 SeitenDetailed Solutions To Problem 5Maria AngelicaNoch keine Bewertungen

- Chapter 3 ReceivablesDokument22 SeitenChapter 3 ReceivablesCale Robert RascoNoch keine Bewertungen

- Death of A Partner Test SPCC 23-24 Accounts - Docx (2)Dokument5 SeitenDeath of A Partner Test SPCC 23-24 Accounts - Docx (2)Shivansh JaiswalNoch keine Bewertungen

- Petroflo Trading Company: Cash Payment VoucherDokument10 SeitenPetroflo Trading Company: Cash Payment Vouchermuhammad ihtishamNoch keine Bewertungen

- Compound Interest Problems With Detailed SolutionsDokument11 SeitenCompound Interest Problems With Detailed SolutionsJerle Mae ParondoNoch keine Bewertungen

- Change Your Life PDF FreeDokument51 SeitenChange Your Life PDF FreeJochebed MukandaNoch keine Bewertungen

- Ias 16Dokument31 SeitenIas 16Reever RiverNoch keine Bewertungen

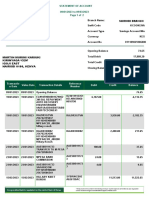

- Martin Murimi KariukiDokument2 SeitenMartin Murimi KariukiKameneja LeeNoch keine Bewertungen

- CIMB BANK Products and Services PresentationDokument20 SeitenCIMB BANK Products and Services PresentationAzwin YusoffNoch keine Bewertungen

- Receipt 1 PDFDokument3 SeitenReceipt 1 PDFsomenathbasakNoch keine Bewertungen

- Nism Series XV - Research Analyst Certification ExamDokument17 SeitenNism Series XV - Research Analyst Certification ExamRohit ShetNoch keine Bewertungen

- Measure and Manage Credit and Counterparty RiskDokument1 SeiteMeasure and Manage Credit and Counterparty RiskjupeeNoch keine Bewertungen

- V Imp Questions For Exams For Selected ChaptersDokument132 SeitenV Imp Questions For Exams For Selected ChaptersNkume Irene100% (1)

- Pas 21-The Effects of Changes in Foreign Exchange RatesDokument3 SeitenPas 21-The Effects of Changes in Foreign Exchange RatesAryan LeeNoch keine Bewertungen

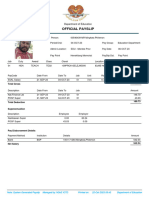

- Official Payslip: Department of EducationDokument1 SeiteOfficial Payslip: Department of Educationphillmingkwa2017Noch keine Bewertungen

- Business Finance-Q3-Week-1-2Dokument5 SeitenBusiness Finance-Q3-Week-1-2Axerob BmNoch keine Bewertungen

- SMChap 021Dokument56 SeitenSMChap 021testbank91% (11)

- Capital Market FundamentalsDokument27 SeitenCapital Market FundamentalsAbin VargheseNoch keine Bewertungen

- Kinshuk Sir - ReferenceDokument16 SeitenKinshuk Sir - ReferenceBhaskargrNoch keine Bewertungen

- Money Supply, Demand & CreationDokument13 SeitenMoney Supply, Demand & Creationpratyush mishraNoch keine Bewertungen

- SPFTB Loan and Savings Policies for Business, Personal AccountsDokument3 SeitenSPFTB Loan and Savings Policies for Business, Personal AccountsLeilalyn NicolasNoch keine Bewertungen

- FINALREPORTBANKNEW Converted 95201213Dokument58 SeitenFINALREPORTBANKNEW Converted 95201213dinjoNoch keine Bewertungen

- Partnership Formation Answer KeyDokument8 SeitenPartnership Formation Answer KeyNichole Joy XielSera TanNoch keine Bewertungen

- BangladeBangladesh Securities and Exchange Commissionsh Securities and Exchange CommissionDokument55 SeitenBangladeBangladesh Securities and Exchange Commissionsh Securities and Exchange CommissionMd. Farid AhmedNoch keine Bewertungen

- National IncomeDokument29 SeitenNational Incomeshahidul0Noch keine Bewertungen

- Ashwini G Report On Axis BankDokument49 SeitenAshwini G Report On Axis BankVishwas DeveeraNoch keine Bewertungen