Das könnte Ihnen auch gefallen

- Corporate Financial Analysis with Microsoft ExcelVon EverandCorporate Financial Analysis with Microsoft ExcelBewertung: 5 von 5 Sternen5/5 (1)

- 8 LMS-Tutorial CFW PDFDokument6 Seiten8 LMS-Tutorial CFW PDFEnriko SagaNoch keine Bewertungen

- Caoital Case StudyDokument15 SeitenCaoital Case StudyTanvir Ahmed Rajib100% (1)

- IRR Vs MIRR Vs NPV (Finatics)Dokument4 SeitenIRR Vs MIRR Vs NPV (Finatics)miranirfanNoch keine Bewertungen

- Session 3: Project Unlevered Cost of Capital: N. K. Chidambaran Corporate FinanceDokument25 SeitenSession 3: Project Unlevered Cost of Capital: N. K. Chidambaran Corporate FinanceSaurabh GuptaNoch keine Bewertungen

- Projecting Financials & ValuationsDokument88 SeitenProjecting Financials & ValuationsPratik ModyNoch keine Bewertungen

- AC6101 Lecture 6 - Valuing Levered ProjectsDokument16 SeitenAC6101 Lecture 6 - Valuing Levered ProjectsKelsey GaoNoch keine Bewertungen

- CFADS Calculation & Application PDFDokument2 SeitenCFADS Calculation & Application PDFJORGE PUENTESNoch keine Bewertungen

- Project Finance: Valuing Unlevered ProjectsDokument41 SeitenProject Finance: Valuing Unlevered ProjectsKelsey GaoNoch keine Bewertungen

- IIM Kozhikode Project Finance Course OutlineDokument5 SeitenIIM Kozhikode Project Finance Course OutlinePressesIndiaNoch keine Bewertungen

- Capital Structure: Theory and PolicyDokument31 SeitenCapital Structure: Theory and PolicySuraj ShelarNoch keine Bewertungen

- Capital Budgeting AnswerDokument18 SeitenCapital Budgeting AnswerPiyush ChughNoch keine Bewertungen

- Financial Institutions ManagementDokument8 SeitenFinancial Institutions ManagementJesmon RajNoch keine Bewertungen

- Accrual Accounting ProcessDokument52 SeitenAccrual Accounting Processaamritaa100% (1)

- Capital Budgeting: Dr. Akshita Arora IBS-GurgaonDokument24 SeitenCapital Budgeting: Dr. Akshita Arora IBS-GurgaonhitanshuNoch keine Bewertungen

- Break EvenDokument36 SeitenBreak EvenNila ChotaiNoch keine Bewertungen

- III.B.6 Credit Risk Capital CalculationDokument28 SeitenIII.B.6 Credit Risk Capital CalculationvladimirpopovicNoch keine Bewertungen

- 1.0 Financial Modeling Intro v2Dokument28 Seiten1.0 Financial Modeling Intro v2Arif JamaliNoch keine Bewertungen

- Chap 016Dokument8 SeitenChap 016Bobby MarionNoch keine Bewertungen

- Discounted Cash Flow Valuation The Inputs: K.ViswanathanDokument47 SeitenDiscounted Cash Flow Valuation The Inputs: K.ViswanathanHardik VibhakarNoch keine Bewertungen

- M09 Gitman50803X 14 MF C09Dokument56 SeitenM09 Gitman50803X 14 MF C09dhfbbbbbbbbbbbbbbbbbhNoch keine Bewertungen

- CEC Case Study - Capital Structure and Financial Leverage OptionsDokument9 SeitenCEC Case Study - Capital Structure and Financial Leverage OptionsChirag Maheshwari100% (1)

- Advisors Report 2010Dokument35 SeitenAdvisors Report 2010bluesbankyNoch keine Bewertungen

- Model Management Guidance PDFDokument70 SeitenModel Management Guidance PDFChen CharlesNoch keine Bewertungen

- Csae Study of FMDokument4 SeitenCsae Study of FMAbdul Saqib17% (6)

- Capital Budgeting Techniques ExplainedDokument35 SeitenCapital Budgeting Techniques ExplainedGaurav gusaiNoch keine Bewertungen

- Fixed Income Instruments in IndiaDokument90 SeitenFixed Income Instruments in Indiaapi-19459467100% (11)

- HDFC Balanced Advantage Fund OverviewDokument11 SeitenHDFC Balanced Advantage Fund OverviewManasi AjithkumarNoch keine Bewertungen

- Chapter 04 Working Capital 1ce Lecture 050930Dokument71 SeitenChapter 04 Working Capital 1ce Lecture 050930rthillai72Noch keine Bewertungen

- D - Tutorial 7 (Solutions)Dokument10 SeitenD - Tutorial 7 (Solutions)AlfieNoch keine Bewertungen

- Capital Budgeting Techniques and StepsDokument13 SeitenCapital Budgeting Techniques and Stepsaon aliNoch keine Bewertungen

- Legal Disclaimer: Read and Accept Before Accessing The Tutorial WorkbookDokument15 SeitenLegal Disclaimer: Read and Accept Before Accessing The Tutorial WorkbooksubhashbuddanaNoch keine Bewertungen

- RSKMGT Module II Credit Risk CH 4 - Prediction of Exposure at DefaultDokument8 SeitenRSKMGT Module II Credit Risk CH 4 - Prediction of Exposure at DefaultAstha PandeyNoch keine Bewertungen

- Risk Management Solution Chapters Seven-EightDokument9 SeitenRisk Management Solution Chapters Seven-EightBombitaNoch keine Bewertungen

- Finec 2Dokument11 SeitenFinec 2nurulnatasha sinclairaquariusNoch keine Bewertungen

- Mutual Funds: Answer Role of Mutual Funds in The Financial Market: Mutual Funds Have Opened New Vistas ToDokument43 SeitenMutual Funds: Answer Role of Mutual Funds in The Financial Market: Mutual Funds Have Opened New Vistas ToNidhi Kaushik100% (1)

- MCQ On Cost ofDokument17 SeitenMCQ On Cost ofbarbie dollNoch keine Bewertungen

- Cost of CapitalDokument55 SeitenCost of CapitalSaritasaruNoch keine Bewertungen

- Financial Management MCQs on Capital Budgeting, Risk AnalysisDokument17 SeitenFinancial Management MCQs on Capital Budgeting, Risk Analysis19101977Noch keine Bewertungen

- Capital Budgeting in ExcelDokument9 SeitenCapital Budgeting in ExcelkaouechNoch keine Bewertungen

- Solutions BD3 SM24 GEDokument4 SeitenSolutions BD3 SM24 GEAgnes ChewNoch keine Bewertungen

- Lecture 7 Adjusted Present ValueDokument19 SeitenLecture 7 Adjusted Present ValuePraneet Singavarapu100% (1)

- Duration GAP analysis: Measuring interest rate riskDokument5 SeitenDuration GAP analysis: Measuring interest rate riskShubhash ShresthaNoch keine Bewertungen

- Tutorial 4 CHP 5 - SolutionDokument6 SeitenTutorial 4 CHP 5 - SolutionwilliamnyxNoch keine Bewertungen

- Capm and AptDokument10 SeitenCapm and AptRajkumar35Noch keine Bewertungen

- CH 8Dokument18 SeitenCH 8ahngehlah100% (3)

- Case Study 3Dokument2 SeitenCase Study 3Rao SNoch keine Bewertungen

- Rose Mwaniki CVDokument10 SeitenRose Mwaniki CVHamid RazaNoch keine Bewertungen

- Arbitrage Pricing TheoryDokument4 SeitenArbitrage Pricing TheoryShabbir NadafNoch keine Bewertungen

- School - of - Finance - - - 101 - Questions ответыDokument98 SeitenSchool - of - Finance - - - 101 - Questions ответыКирик ЕвченкоNoch keine Bewertungen

- Tutorial 2 Key Concepts Utility, Returns, DiversificationDokument1 SeiteTutorial 2 Key Concepts Utility, Returns, DiversificationDuoqi WangNoch keine Bewertungen

- Introduction to Infrastructure in IndiaDokument61 SeitenIntroduction to Infrastructure in Indiaanilnair88Noch keine Bewertungen

- Problemset5 AnswersDokument11 SeitenProblemset5 AnswersHowo4DieNoch keine Bewertungen

- Cost of CaptialDokument72 SeitenCost of CaptialkhyroonNoch keine Bewertungen

- Boeing CaseDokument7 SeitenBoeing CaseMengdi ZhangNoch keine Bewertungen

- Answers To Chapter 7 - Interest Rates and Bond ValuationDokument8 SeitenAnswers To Chapter 7 - Interest Rates and Bond ValuationbuwaleedNoch keine Bewertungen

- ThroughputDokument15 SeitenThroughputVaibhav KocharNoch keine Bewertungen

- Assignment 3Dokument7 SeitenAssignment 3Abdullah ghauriNoch keine Bewertungen

- CFADS Calculation ApplicationDokument2 SeitenCFADS Calculation Applicationtransitxyz100% (1)

- Energy Laws and RegulationsDokument10 SeitenEnergy Laws and RegulationsAbubakar IsmailNoch keine Bewertungen

- Pmo Strategy Implementation PDFDokument18 SeitenPmo Strategy Implementation PDFreogomezNoch keine Bewertungen

- Finance Function Partnering: For The Integration of Sustainability in BusinessDokument18 SeitenFinance Function Partnering: For The Integration of Sustainability in BusinessAbubakar IsmailNoch keine Bewertungen

- Competency Framework SMA-FINALDokument39 SeitenCompetency Framework SMA-FINALAbubakar IsmailNoch keine Bewertungen

- MBA Executive Learning Schedule Spring 2022Dokument1 SeiteMBA Executive Learning Schedule Spring 2022Abubakar IsmailNoch keine Bewertungen

- Finance Function Partnering: For The Integration of Sustainability in BusinessDokument18 SeitenFinance Function Partnering: For The Integration of Sustainability in BusinessAbubakar IsmailNoch keine Bewertungen

- Solar Systems and Blackouts Fact SheetDokument2 SeitenSolar Systems and Blackouts Fact SheetAbubakar IsmailNoch keine Bewertungen

- Executive Course To Master Electricity Markets 2020: 1 March 2021 - 14 June 2021Dokument3 SeitenExecutive Course To Master Electricity Markets 2020: 1 March 2021 - 14 June 2021Abubakar IsmailNoch keine Bewertungen

- Mba Executive Academic Calendar 2022Dokument1 SeiteMba Executive Academic Calendar 2022Abubakar IsmailNoch keine Bewertungen

- CFO As Value CreatorDokument27 SeitenCFO As Value CreatorAbubakar IsmailNoch keine Bewertungen

- Profitability Analytcis FrameworkDokument26 SeitenProfitability Analytcis Frameworkbefn35Noch keine Bewertungen

- Competency Framework SMA-FINALDokument39 SeitenCompetency Framework SMA-FINALAbubakar IsmailNoch keine Bewertungen

- 210 Vertex Whitepaper 2.0Dokument43 Seiten210 Vertex Whitepaper 2.0Abubakar IsmailNoch keine Bewertungen

- MA Competency Report FinalDokument32 SeitenMA Competency Report FinalAbubakar IsmailNoch keine Bewertungen

- 2021 Texas Power Outages: Facts and Initial Thoughts: February 22, 2021Dokument20 Seiten2021 Texas Power Outages: Facts and Initial Thoughts: February 22, 2021James JosephNoch keine Bewertungen

- FMR January 2021Dokument27 SeitenFMR January 2021Abubakar IsmailNoch keine Bewertungen

- Battery Room Ventilation RequirementsDokument5 SeitenBattery Room Ventilation RequirementsAbubakar IsmailNoch keine Bewertungen

- HVDC - U2013 The Chinese Experience by Ms. Quan BailuDokument132 SeitenHVDC - U2013 The Chinese Experience by Ms. Quan BailuAbubakar IsmailNoch keine Bewertungen

- Pak Rail TicketDokument1 SeitePak Rail TicketAbubakar IsmailNoch keine Bewertungen

- GS4 - Taxation of IT SectorDokument13 SeitenGS4 - Taxation of IT SectorAbubakar IsmailNoch keine Bewertungen

- Notified Vide SRO No. 575 Dated 22 May 2019Dokument3 SeitenNotified Vide SRO No. 575 Dated 22 May 2019Hussain RahibNoch keine Bewertungen

- Comments On Tax Laws (Second Amendment) Act, 2021Dokument15 SeitenComments On Tax Laws (Second Amendment) Act, 2021Abubakar IsmailNoch keine Bewertungen

- Equator Principles IIIDokument24 SeitenEquator Principles IIIdsusanto_indoNoch keine Bewertungen

- 2020 PVEL PV Module Reliability Scorecard PDFDokument38 Seiten2020 PVEL PV Module Reliability Scorecard PDFAbubakar IsmailNoch keine Bewertungen

- Circular Debt ReportDokument57 SeitenCircular Debt ReportAbubakar IsmailNoch keine Bewertungen

- TRF-362 K-Electric QTR Jul - 2016 To Mar 2019 31-12-2019Dokument38 SeitenTRF-362 K-Electric QTR Jul - 2016 To Mar 2019 31-12-2019Abubakar IsmailNoch keine Bewertungen

- 3 Hidden Causes of Industrial Energy WasteDokument2 Seiten3 Hidden Causes of Industrial Energy WasteAbubakar IsmailNoch keine Bewertungen

- Cea V VillanuevaDokument2 SeitenCea V Villanuevaangelo prietoNoch keine Bewertungen

- Taxfinalquiz 4Dokument67 SeitenTaxfinalquiz 4Aeron Rai RoqueNoch keine Bewertungen

- Concept of NPADokument40 SeitenConcept of NPAsonu_1986100% (2)

- The Liability of The Surety Is Co-Extensive With That of Principal Debtor. Refer With Case LawsDokument2 SeitenThe Liability of The Surety Is Co-Extensive With That of Principal Debtor. Refer With Case LawsAdan Hooda100% (2)

- Final Accounts: Trading, Profit & Loss, Balance Sheet ExplainedDokument20 SeitenFinal Accounts: Trading, Profit & Loss, Balance Sheet ExplainedSeri SummaNoch keine Bewertungen

- Debit Card Issued by A Bank Allowing The Holder To Transfer Money Electronically To Another Bank Account When Making A PurchaseDokument9 SeitenDebit Card Issued by A Bank Allowing The Holder To Transfer Money Electronically To Another Bank Account When Making A PurchaseShovan ChowdhuryNoch keine Bewertungen

- Features of MICR ChequeDokument10 SeitenFeatures of MICR ChequeAssignment HelperNoch keine Bewertungen

- Personal Property Security Act V. Chattel Mortgage Chattel Mortgage (NCC ACT 1508) PPSA (R.A. 11057)Dokument8 SeitenPersonal Property Security Act V. Chattel Mortgage Chattel Mortgage (NCC ACT 1508) PPSA (R.A. 11057)Jj JumalonNoch keine Bewertungen

- SBI Bond IssueDokument2 SeitenSBI Bond Issueanon_722571Noch keine Bewertungen

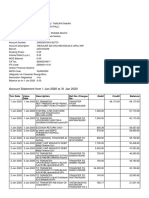

- Account Statement From 1 Jan 2020 To 31 Jan 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDokument4 SeitenAccount Statement From 1 Jan 2020 To 31 Jan 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceRama Mohan GhantasalaNoch keine Bewertungen

- Auto Finance 3.7Dokument16 SeitenAuto Finance 3.7Ali KhojaNoch keine Bewertungen

- Financial Rehabilitation Act SummaryDokument27 SeitenFinancial Rehabilitation Act SummaryNIKKA C MARCELONoch keine Bewertungen

- Cred - Statement SbiDokument6 SeitenCred - Statement SbiKENA PATELNoch keine Bewertungen

- Chapter 13: Commercial Bank Operations 3edDokument26 SeitenChapter 13: Commercial Bank Operations 3edMarwa HassanNoch keine Bewertungen

- Eastern Mindoro College Bongabong, Oriental Mindoro Telefax (043) 2835479 E-MailDokument2 SeitenEastern Mindoro College Bongabong, Oriental Mindoro Telefax (043) 2835479 E-MailPrecilla Zoleta SosaNoch keine Bewertungen

- Escrow Agreement TemplateDokument5 SeitenEscrow Agreement TemplatesamsarmaNoch keine Bewertungen

- R YHv E7 H 1 U Ew 1 MLR SDokument3 SeitenR YHv E7 H 1 U Ew 1 MLR SNaveen MaheshNoch keine Bewertungen

- Auto Loan ABS ManualDokument21 SeitenAuto Loan ABS ManualMike JonesNoch keine Bewertungen

- Check Credit Report & Get Only Official FICO ScoresDokument11 SeitenCheck Credit Report & Get Only Official FICO ScoresCarolNoch keine Bewertungen

- Bankruptcy Law in MexicoDokument151 SeitenBankruptcy Law in MexicoFrancisco Rodriguez NepoteNoch keine Bewertungen

- Latest Accepted For Value Formats Rev 8Dokument4 SeitenLatest Accepted For Value Formats Rev 8SovereignCC97% (223)

- Application of Payment, Cession, ConsignationDokument4 SeitenApplication of Payment, Cession, ConsignationRonald McRonaldNoch keine Bewertungen

- Freddie Mac Scandal Accounting IssuesDokument3 SeitenFreddie Mac Scandal Accounting IssuesKimmy Santos Victorino50% (2)

- LOMA 280 Test PDFDokument75 SeitenLOMA 280 Test PDFAbhijit80% (10)

- Discover Statement 20200225 4656 PDFDokument4 SeitenDiscover Statement 20200225 4656 PDFCarlos Estrada75% (4)

- Project Ratio AnalysisDokument106 SeitenProject Ratio AnalysisNital Patel33% (3)

- Debt Sculpting TutorialDokument2 SeitenDebt Sculpting TutorialYogesh More100% (1)

- ACC 211 Quiz-LIABILITIESDokument1 SeiteACC 211 Quiz-LIABILITIESAeyjay ManangaranNoch keine Bewertungen

- How To Take Money From ATM: Procedure TextDokument1 SeiteHow To Take Money From ATM: Procedure TextOctavinaNoch keine Bewertungen

- Project Finance Summary Debt Rating Criteria-S&P PDFDokument17 SeitenProject Finance Summary Debt Rating Criteria-S&P PDFReisha Ananda PutriNoch keine Bewertungen