Das könnte Ihnen auch gefallen

- S F S P: The Pecial Actor Taking LanDokument7 SeitenS F S P: The Pecial Actor Taking LanMG7FILMESNoch keine Bewertungen

- FINAL - PROJECT Report On HSBCDokument72 SeitenFINAL - PROJECT Report On HSBCgururaj77167% (3)

- Sbi and Hdfc"COMPARATIVE STUDY OF CUSTOMER'S SATISFACTION TOWARDS HDFC BANK AND STATE BANK OF INDIADokument68 SeitenSbi and Hdfc"COMPARATIVE STUDY OF CUSTOMER'S SATISFACTION TOWARDS HDFC BANK AND STATE BANK OF INDIArupesh singh84% (31)

- Regional Rural Banks of India: Evolution, Performance and ManagementVon EverandRegional Rural Banks of India: Evolution, Performance and ManagementNoch keine Bewertungen

- Islamic Banking And Finance for Beginners!Von EverandIslamic Banking And Finance for Beginners!Bewertung: 2 von 5 Sternen2/5 (1)

- Bank Product Analysis TemplateDokument14 SeitenBank Product Analysis TemplateGanesh TiwariNoch keine Bewertungen

- MGT201 Finalterm GoldenFileDokument230 SeitenMGT201 Finalterm GoldenFilemaryamNoch keine Bewertungen

- History of Banking in India GK Notes in PDF 2Dokument6 SeitenHistory of Banking in India GK Notes in PDF 2Yogesh LondheNoch keine Bewertungen

- History of Banking in India - GK Notes in PDFDokument5 SeitenHistory of Banking in India - GK Notes in PDFdasdibyendu095Noch keine Bewertungen

- History of Banking in India GK Notes in PDFDokument6 SeitenHistory of Banking in India GK Notes in PDFMohitNoch keine Bewertungen

- Module 1 Intro To BKG ExamDokument36 SeitenModule 1 Intro To BKG ExamVimal SoniNoch keine Bewertungen

- History of Banking - 573Dokument3 SeitenHistory of Banking - 573PRASHANT KUMAR GAUTAMNoch keine Bewertungen

- History of Indian BankingDokument23 SeitenHistory of Indian BankingLaxman KambleNoch keine Bewertungen

- 2020 A STUDY ON RECRUITMENT AND SELECTION PROCESS Research Report HRDokument63 Seiten2020 A STUDY ON RECRUITMENT AND SELECTION PROCESS Research Report HRanjali sikhaNoch keine Bewertungen

- 1.1 Overview of Banking IndustryDokument51 Seiten1.1 Overview of Banking IndustryRohit PathakNoch keine Bewertungen

- Nationalized BanksDokument12 SeitenNationalized BanksAakash JainNoch keine Bewertungen

- Indian Banking Industry by Ravi Ranjan SirDokument20 SeitenIndian Banking Industry by Ravi Ranjan SirRavi RanjanNoch keine Bewertungen

- Business Environment: Mba I-BDokument19 SeitenBusiness Environment: Mba I-BDivya PableNoch keine Bewertungen

- Explain The Rationale For The Nationalization of BanksDokument13 SeitenExplain The Rationale For The Nationalization of Bankssanjay parmarNoch keine Bewertungen

- TH THDokument34 SeitenTH THpmmppmNoch keine Bewertungen

- Indian Banking SystemDokument56 SeitenIndian Banking SystemManoj YadavNoch keine Bewertungen

- Project On ICICI BankDokument104 SeitenProject On ICICI BankVrinda KaushalNoch keine Bewertungen

- Comperative Study On Performance of Public & Private Sector BanksDokument96 SeitenComperative Study On Performance of Public & Private Sector BanksJaimit Shah Raja100% (2)

- Customer Satisfaction-ICICI BankDokument98 SeitenCustomer Satisfaction-ICICI BankSabinYadav88% (16)

- Ch.1 Indian Banking: IntroductionDokument54 SeitenCh.1 Indian Banking: Introductiont1g2Noch keine Bewertungen

- History of Banking System in IndiaDokument37 SeitenHistory of Banking System in IndiaSrijan DubeyNoch keine Bewertungen

- ICICI Project ReportDokument53 SeitenICICI Project ReportPawan MeenaNoch keine Bewertungen

- Unit 1Dokument57 SeitenUnit 1Anurag VarmaNoch keine Bewertungen

- Principles OF Banking - 1Dokument36 SeitenPrinciples OF Banking - 1Pulkit_Saini_789Noch keine Bewertungen

- Banking StudyDokument5 SeitenBanking Studymav7788Noch keine Bewertungen

- Ufi M 4Dokument42 SeitenUfi M 4sresthapatel28Noch keine Bewertungen

- Project Report ON Working Capital Management: Punjab National BankDokument65 SeitenProject Report ON Working Capital Management: Punjab National BankSurender Dhuran PrajapatNoch keine Bewertungen

- Growth in Indian Banking SectorDokument59 SeitenGrowth in Indian Banking SectorKishan KudiaNoch keine Bewertungen

- Time-Value of Money - IciciDokument27 SeitenTime-Value of Money - IciciJay PatelNoch keine Bewertungen

- Evolution of Indian BankingDokument5 SeitenEvolution of Indian BankingManu SainiNoch keine Bewertungen

- BanksDokument120 SeitenBankskoshycjNoch keine Bewertungen

- History of Banking in India: Managing New ChallengesDokument14 SeitenHistory of Banking in India: Managing New ChallengesPushpendra MittalNoch keine Bewertungen

- E-BANKING SERVICE HDFC ProjectDokument65 SeitenE-BANKING SERVICE HDFC ProjectSri KamalNoch keine Bewertungen

- History of Banking in India: 1) Pre-Nationalization EraDokument7 SeitenHistory of Banking in India: 1) Pre-Nationalization EraKoshyNoch keine Bewertungen

- Comparative Study of Education Loan Between Sbi and IciciDokument88 SeitenComparative Study of Education Loan Between Sbi and IciciAvtaar SinghNoch keine Bewertungen

- Chapter-1 History of Banking in IndiaDokument95 SeitenChapter-1 History of Banking in IndiaJaimit Shah RajaNoch keine Bewertungen

- Icici Bank ProjectDokument70 SeitenIcici Bank ProjectSonu Dhangar100% (2)

- Nationalization of Indian Commercial BanksDokument16 SeitenNationalization of Indian Commercial BanksAlbertNoch keine Bewertungen

- Mba ProjectDokument88 SeitenMba ProjectRupan VermaNoch keine Bewertungen

- History of Banking in IndiaDokument32 SeitenHistory of Banking in IndiaHedayatullah PashteenNoch keine Bewertungen

- Scenario of Foreign Banks in IndiaDokument62 SeitenScenario of Foreign Banks in IndiaYesha Khona100% (1)

- Banking SystemDokument3 SeitenBanking SystemharshtyagiNoch keine Bewertungen

- A Research Report On SbiDokument45 SeitenA Research Report On SbiSonu LovesforuNoch keine Bewertungen

- Noj HDeuw 3 Op Z2 y AWc 0 KWDokument4 SeitenNoj HDeuw 3 Op Z2 y AWc 0 KWimveryproNoch keine Bewertungen

- Project Report On Icici BankDokument44 SeitenProject Report On Icici BankRoyal Projects67% (3)

- Q. 4 There Are Three Different Phases in The History of Banking in India.Dokument4 SeitenQ. 4 There Are Three Different Phases in The History of Banking in India.MAHENDRA SHIVAJI DHENAKNoch keine Bewertungen

- Indian Banks RbiDokument8 SeitenIndian Banks RbiAashri SharmaNoch keine Bewertungen

- History of Banking in IndiaDokument2 SeitenHistory of Banking in Indiazealot5000Noch keine Bewertungen

- Part 2Dokument70 SeitenPart 2Ridhima MalhotraNoch keine Bewertungen

- Origin & Kinds of BanksDokument21 SeitenOrigin & Kinds of BanksPriyankamohanant SumaNoch keine Bewertungen

- Types of BankingDokument10 SeitenTypes of BankingJinu SajiNoch keine Bewertungen

- Banking India: Accepting Deposits for the Purpose of LendingVon EverandBanking India: Accepting Deposits for the Purpose of LendingNoch keine Bewertungen

- T R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)Von EverandT R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)Noch keine Bewertungen

- Major Bank Fraud Cases: A Critical ReviewVon EverandMajor Bank Fraud Cases: A Critical ReviewBewertung: 4.5 von 5 Sternen4.5/5 (6)

- The role of banks in the regional economic development of Uzbekistan: lessons from the German experienceVon EverandThe role of banks in the regional economic development of Uzbekistan: lessons from the German experienceNoch keine Bewertungen

- A Comparative Study On Specific Mutual Funds Schemes of SBI & ICICI Mutual FundDokument99 SeitenA Comparative Study On Specific Mutual Funds Schemes of SBI & ICICI Mutual FundGanesh TiwariNoch keine Bewertungen

- Experience and Satisfaction of Bancassurance Customers of SBI - Final AbhijeetDokument97 SeitenExperience and Satisfaction of Bancassurance Customers of SBI - Final AbhijeetGanesh TiwariNoch keine Bewertungen

- Synopsis On Growth of Venture CapitalDokument7 SeitenSynopsis On Growth of Venture CapitalGanesh TiwariNoch keine Bewertungen

- Experience and Satisfaction of Bancassurance Customers A Study On State Bank of IndiaDokument10 SeitenExperience and Satisfaction of Bancassurance Customers A Study On State Bank of IndiaGanesh TiwariNoch keine Bewertungen

- Final Project Part 2 (Overview of Study and Statement of Problem)Dokument15 SeitenFinal Project Part 2 (Overview of Study and Statement of Problem)Ganesh TiwariNoch keine Bewertungen

- T TestDokument5 SeitenT TestGanesh TiwariNoch keine Bewertungen

- T TestDokument5 SeitenT TestGanesh TiwariNoch keine Bewertungen

- 1Dokument27 Seiten1Ganesh TiwariNoch keine Bewertungen

- Failure of New Products of BankDokument10 SeitenFailure of New Products of BankGanesh TiwariNoch keine Bewertungen

- Project Synopsis A Study On Capital Market in Indian EconomyDokument6 SeitenProject Synopsis A Study On Capital Market in Indian EconomyGanesh TiwariNoch keine Bewertungen

- Project Report On STUDY OF RISK PERCEPTIDokument58 SeitenProject Report On STUDY OF RISK PERCEPTIGanesh TiwariNoch keine Bewertungen

- JMRA Vol 1 (1) 9-18Dokument10 SeitenJMRA Vol 1 (1) 9-18Ganesh TiwariNoch keine Bewertungen

- New Generation Banking in IndiaDokument9 SeitenNew Generation Banking in IndiaGanesh TiwariNoch keine Bewertungen

- GLC Legal Profession Accounts and Records Regulations Consolidated 2017Dokument20 SeitenGLC Legal Profession Accounts and Records Regulations Consolidated 2017tajhtechzNoch keine Bewertungen

- Unit - 3Dokument25 SeitenUnit - 3ShriHemaRajaNoch keine Bewertungen

- Dividend Policy: by Group 5: Aayush Kumar Lewis Francis Jasneet Sai Venkat Ritika BhallaDokument25 SeitenDividend Policy: by Group 5: Aayush Kumar Lewis Francis Jasneet Sai Venkat Ritika BhallaChristo SebastinNoch keine Bewertungen

- Global Family Office Report 2023.pdf - CoredownloadDokument102 SeitenGlobal Family Office Report 2023.pdf - Coredownloadpderby1Noch keine Bewertungen

- Cash Flow StatementDokument11 SeitenCash Flow StatementJonathanKelly Bitonga BargasoNoch keine Bewertungen

- Tax PaidDokument1 SeiteTax PaidRiya Mazumder Roll 286Noch keine Bewertungen

- Honor Mobile Flyer 3419Dokument2 SeitenHonor Mobile Flyer 3419bilal asifNoch keine Bewertungen

- 00004848-Ewa 7327693Dokument1 Seite00004848-Ewa 7327693radha jayaramanNoch keine Bewertungen

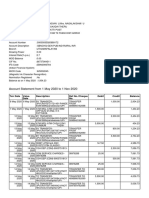

- Account Statement From 1 May 2020 To 1 Nov 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDokument9 SeitenAccount Statement From 1 May 2020 To 1 Nov 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceChellapandiNoch keine Bewertungen

- Vision of Microfinance in IndiaDokument28 SeitenVision of Microfinance in Indiashiva1720Noch keine Bewertungen

- 2018 Working Capital Management: Test Code: R38 WCAM Q-BankDokument6 Seiten2018 Working Capital Management: Test Code: R38 WCAM Q-BankMarwa Abd-ElmeguidNoch keine Bewertungen

- Personal Financial PlannerDokument18 SeitenPersonal Financial PlannerBeastPlaysNoch keine Bewertungen

- Fintech Insights Q2 2022 Quarterly: FT Partners ResearchDokument110 SeitenFintech Insights Q2 2022 Quarterly: FT Partners ResearchngothientaiNoch keine Bewertungen

- Engineering & Projects 21, Netaji Subhas Road Kolkata - 700 001Dokument77 SeitenEngineering & Projects 21, Netaji Subhas Road Kolkata - 700 001arjun 11Noch keine Bewertungen

- Investment Appraisal CasesDokument4 SeitenInvestment Appraisal CasesmatheussNoch keine Bewertungen

- Draft Version - Article On Cross Collateralization-C1Dokument6 SeitenDraft Version - Article On Cross Collateralization-C1Rohit Anand DasNoch keine Bewertungen

- Essentials of Treasury Management - Working Capital Class Final OutlineDokument32 SeitenEssentials of Treasury Management - Working Capital Class Final OutlinePablo VeraNoch keine Bewertungen

- E StatementDokument3 SeitenE StatementVarun Kumar BawaNoch keine Bewertungen

- The Performance of Diversified Emerging Market Equity FundsDokument16 SeitenThe Performance of Diversified Emerging Market Equity FundsMuhammad RoqibunNoch keine Bewertungen

- AssignmentDokument7 SeitenAssignmentMona VimlaNoch keine Bewertungen

- Public Mutual Private Retiremenent Scheme ProducthighlightDokument12 SeitenPublic Mutual Private Retiremenent Scheme ProducthighlightBenNoch keine Bewertungen

- Compensation Income - Fringe Benefit TaxDokument41 SeitenCompensation Income - Fringe Benefit Taxdelacruzrojohn600Noch keine Bewertungen

- Bank LoansDokument20 SeitenBank LoansMihir ShahNoch keine Bewertungen

- Correct?Dokument29 SeitenCorrect?Hong Anh NguyenNoch keine Bewertungen

- UntitledDokument8 SeitenUntitledRae SlaughterNoch keine Bewertungen

- C1 - Guaranty Trust Bank PLC Nigeria (A)Dokument15 SeitenC1 - Guaranty Trust Bank PLC Nigeria (A)Anisha RaiNoch keine Bewertungen

- Punjab & Sind Bank: Jump To Navigationjump To SearchDokument5 SeitenPunjab & Sind Bank: Jump To Navigationjump To SearchSakshi BakliwalNoch keine Bewertungen

- Chapter 1 Afar (Bus Com)Dokument24 SeitenChapter 1 Afar (Bus Com)jajajaredredNoch keine Bewertungen