Das könnte Ihnen auch gefallen

- Martin Luther King Action Team of Cape Cod Statement On George FloydDokument2 SeitenMartin Luther King Action Team of Cape Cod Statement On George FloydCape Cod TimesNoch keine Bewertungen

- Lawsuit by Nantucket Residents Against TurbinesDokument36 SeitenLawsuit by Nantucket Residents Against TurbinesCape Cod TimesNoch keine Bewertungen

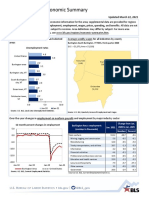

- Burlington Area Economy SummaryDokument2 SeitenBurlington Area Economy SummaryCape Cod TimesNoch keine Bewertungen

- Burlington Area Economy SummaryDokument2 SeitenBurlington Area Economy SummaryCape Cod TimesNoch keine Bewertungen

- Yarmouth Board of Health Letter On Pandemic EnforcementDokument1 SeiteYarmouth Board of Health Letter On Pandemic EnforcementCape Cod TimesNoch keine Bewertungen

- Phase II Comprehensive Site Assessment Work Barnstable County Fire & Rescue Training AcademyDokument30 SeitenPhase II Comprehensive Site Assessment Work Barnstable County Fire & Rescue Training AcademyCape Cod TimesNoch keine Bewertungen

- Ci-Opioid07 PDFDokument1 SeiteCi-Opioid07 PDFCape Cod TimesNoch keine Bewertungen

- ACLU Letter About Searches at Dennis BeachesDokument5 SeitenACLU Letter About Searches at Dennis BeachesCape Cod TimesNoch keine Bewertungen

- Guidance To Seasonal Community - EnglishDokument2 SeitenGuidance To Seasonal Community - EnglishCape Cod Times33% (3)

- Commonwealth vs. Michael BryantDokument20 SeitenCommonwealth vs. Michael BryantCape Cod TimesNoch keine Bewertungen

- Barnstable Officials Send Letter To Cumberland FarmsDokument3 SeitenBarnstable Officials Send Letter To Cumberland FarmsCape Cod TimesNoch keine Bewertungen

- Affidavit Motion For Summons by Thomas Latanowich's AttorneyDokument5 SeitenAffidavit Motion For Summons by Thomas Latanowich's AttorneyCape Cod TimesNoch keine Bewertungen

- Steamship Authority Letter To Gov. BakerDokument4 SeitenSteamship Authority Letter To Gov. BakerCape Cod TimesNoch keine Bewertungen

- Ci-Opioid07 PDFDokument1 SeiteCi-Opioid07 PDFCape Cod TimesNoch keine Bewertungen

- Nationwide College Cheating Scam ComplaintDokument204 SeitenNationwide College Cheating Scam ComplaintLaw&Crime100% (2)

- Ci-Opioid07 PDFDokument1 SeiteCi-Opioid07 PDFCape Cod TimesNoch keine Bewertungen

- Ci-Opioid07 PDFDokument1 SeiteCi-Opioid07 PDFCape Cod TimesNoch keine Bewertungen

- United States Sentencing Memorandum For Kimberly KittsDokument6 SeitenUnited States Sentencing Memorandum For Kimberly KittsCape Cod Times100% (1)

- Eastham Elementary School LetterDokument1 SeiteEastham Elementary School LetterCape Cod TimesNoch keine Bewertungen

- Deep Blue LLC Shark Deterrent PresentationDokument7 SeitenDeep Blue LLC Shark Deterrent PresentationCape Cod TimesNoch keine Bewertungen

- Indictment in College Admissions Bribery SchemeDokument23 SeitenIndictment in College Admissions Bribery SchemeCape Cod TimesNoch keine Bewertungen

- Court Documents in The Emory Snell CaseDokument30 SeitenCourt Documents in The Emory Snell CaseCape Cod Times100% (1)

- "Apellant Brief" in Adrian Loya CaseDokument48 Seiten"Apellant Brief" in Adrian Loya CaseCape Cod Times0% (1)

- Ruling On Summonsing RequestsDokument2 SeitenRuling On Summonsing RequestsCape Cod TimesNoch keine Bewertungen

- Pilgrim 2018 Annual Assessment LetterDokument5 SeitenPilgrim 2018 Annual Assessment LetterCape Cod TimesNoch keine Bewertungen

- Hyannis Woman Sentenced in Scheme That Targeted ElderlyDokument23 SeitenHyannis Woman Sentenced in Scheme That Targeted ElderlyCape Cod TimesNoch keine Bewertungen

- SJC Denies Appeal in Hyannis Counterfeiting CaseDokument3 SeitenSJC Denies Appeal in Hyannis Counterfeiting CaseCape Cod TimesNoch keine Bewertungen

- Ron Beaty Reprimand LetterDokument1 SeiteRon Beaty Reprimand LetterCape Cod TimesNoch keine Bewertungen

- Court Document Ordering Kitts Not To Sell Any PropertyDokument11 SeitenCourt Document Ordering Kitts Not To Sell Any PropertyCape Cod TimesNoch keine Bewertungen

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (73)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (120)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Listo Si Kap!Dokument32 SeitenListo Si Kap!Bluboy100% (3)

- Homicide Act 1957 Section 1 - Abolition of "Constructive Malice"Dokument5 SeitenHomicide Act 1957 Section 1 - Abolition of "Constructive Malice"Fowzia KaraniNoch keine Bewertungen

- Ethiopia Pulp & Paper SC: Notice NoticeDokument1 SeiteEthiopia Pulp & Paper SC: Notice NoticeWedi FitwiNoch keine Bewertungen

- OD428150379753135100Dokument1 SeiteOD428150379753135100Sourav SantraNoch keine Bewertungen

- Cadila PharmaDokument16 SeitenCadila PharmaIntoxicated WombatNoch keine Bewertungen

- Frias Vs Atty. LozadaDokument47 SeitenFrias Vs Atty. Lozadamedalin1575Noch keine Bewertungen

- Equilibrium Is A 2002 American: The Flag of Libria. The Four Ts On The Flag Represent The Tetragrammaton CouncilDokument5 SeitenEquilibrium Is A 2002 American: The Flag of Libria. The Four Ts On The Flag Represent The Tetragrammaton CouncilmuhammadismailNoch keine Bewertungen

- Grand Boulevard Hotel Vs Genuine Labor OrganizationDokument2 SeitenGrand Boulevard Hotel Vs Genuine Labor OrganizationCuddlyNoch keine Bewertungen

- Three VignettesDokument3 SeitenThree VignettesIsham IbrahimNoch keine Bewertungen

- StarbucksDokument19 SeitenStarbucksPraveen KumarNoch keine Bewertungen

- The Realistic NovelDokument25 SeitenThe Realistic NovelNinna NannaNoch keine Bewertungen

- 45-TQM in Indian Service Sector PDFDokument16 Seiten45-TQM in Indian Service Sector PDFsharan chakravarthyNoch keine Bewertungen

- E.I Dupont de Nemours & Co. vs. Francisco, Et - Al.Dokument3 SeitenE.I Dupont de Nemours & Co. vs. Francisco, Et - Al.Carmille Marge MercadoNoch keine Bewertungen

- Ta 9 2024 0138 FNL Cor01 - enDokument458 SeitenTa 9 2024 0138 FNL Cor01 - enLeslie GordilloNoch keine Bewertungen

- Cagayan Capitol Valley Vs NLRCDokument7 SeitenCagayan Capitol Valley Vs NLRCvanessa_3Noch keine Bewertungen

- Pre-Paid: Pickup Receipt - Delhivery Challan Awb - 2829212523430 / Delhivery Direct Standard Order ID - O1591795656063Dokument1 SeitePre-Paid: Pickup Receipt - Delhivery Challan Awb - 2829212523430 / Delhivery Direct Standard Order ID - O1591795656063Sravanthi ReddyNoch keine Bewertungen

- Reading Comprehension: Skills Weighted Mean InterpretationDokument10 SeitenReading Comprehension: Skills Weighted Mean InterpretationAleezah Gertrude RegadoNoch keine Bewertungen

- Romantic Criticism of Shakespearen DramaDokument202 SeitenRomantic Criticism of Shakespearen DramaRafael EscobarNoch keine Bewertungen

- What Is OB Chapter1Dokument25 SeitenWhat Is OB Chapter1sun_shenoy100% (1)

- JAR66Dokument100 SeitenJAR66Nae GabrielNoch keine Bewertungen

- 2023 10 3 19 47 48 231003 195751Dokument7 Seiten2023 10 3 19 47 48 231003 195751riyamoni54447Noch keine Bewertungen

- CSC Leave Form 6 BlankDokument3 SeitenCSC Leave Form 6 BlankARMANDO NABASANoch keine Bewertungen

- 2.1.. Democracy As An IdealDokument12 Seiten2.1.. Democracy As An IdealMichel Monkam MboueNoch keine Bewertungen

- Creative Writing PieceDokument3 SeitenCreative Writing Pieceapi-608098440Noch keine Bewertungen

- Listening Practice9 GGBFDokument10 SeitenListening Practice9 GGBFDtn NgaNoch keine Bewertungen

- DPS Quarterly Exam Grade 9Dokument3 SeitenDPS Quarterly Exam Grade 9Michael EstrellaNoch keine Bewertungen

- Evening Street Review Number 1, Summer 2009Dokument100 SeitenEvening Street Review Number 1, Summer 2009Barbara BergmannNoch keine Bewertungen

- Anaphy Finals ReviewerDokument193 SeitenAnaphy Finals Reviewerxuxi dulNoch keine Bewertungen

- Ronaldo FilmDokument2 SeitenRonaldo Filmapi-317647938Noch keine Bewertungen

- Lead The Competition: Latest Current AffairsDokument12 SeitenLead The Competition: Latest Current AffairsSagarias AlbusNoch keine Bewertungen