Das könnte Ihnen auch gefallen

- Private Debt: Yield, Safety and the Emergence of Alternative LendingVon EverandPrivate Debt: Yield, Safety and the Emergence of Alternative LendingNoch keine Bewertungen

- Homeowner's Simple Guide to Property Tax Protest: Whats key: Exemptions & Deductions Blind. Disabled. Over 65. Property Rehabilitation. VeteransVon EverandHomeowner's Simple Guide to Property Tax Protest: Whats key: Exemptions & Deductions Blind. Disabled. Over 65. Property Rehabilitation. VeteransNoch keine Bewertungen

- Income From House Property: Solution To Assignment SolutionsDokument4 SeitenIncome From House Property: Solution To Assignment SolutionsAsar QabeelNoch keine Bewertungen

- House Property 1Dokument14 SeitenHouse Property 1Sarvar Pathan100% (3)

- Income From House Property (Practical)Dokument52 SeitenIncome From House Property (Practical)Bogadala Kirti RaoNoch keine Bewertungen

- 68 Practical Questions of House PropertyDokument14 Seiten68 Practical Questions of House PropertyshrikantNoch keine Bewertungen

- PDF - Learn More - House Property Peoblems and SolutionsDokument4 SeitenPDF - Learn More - House Property Peoblems and Solutionsbsc slpNoch keine Bewertungen

- Unit 5: Income From House PropertyDokument11 SeitenUnit 5: Income From House PropertySiddhant PowleNoch keine Bewertungen

- Income From Houseproperty A.Y. 2022-23Dokument4 SeitenIncome From Houseproperty A.Y. 2022-23Vivek LedwaniNoch keine Bewertungen

- Income From House PropertyDokument27 SeitenIncome From House PropertyJames Anderson0% (1)

- CH 11 Income On House PropertyDokument11 SeitenCH 11 Income On House PropertyJewelNoch keine Bewertungen

- 5.1 Questions On Income From House PropertyDokument3 Seiten5.1 Questions On Income From House PropertyAashi GuptaNoch keine Bewertungen

- Income From House PropertyDokument32 SeitenIncome From House PropertyhanumanthaiahgowdaNoch keine Bewertungen

- CAF-06 RISE Tax Complete Book by Sir Adnan RaufDokument417 SeitenCAF-06 RISE Tax Complete Book by Sir Adnan RaufSaim KhanNoch keine Bewertungen

- Income From House Property PracticalDokument52 SeitenIncome From House Property Practicalvivek raiNoch keine Bewertungen

- Prolems of House PropertyDokument2 SeitenProlems of House PropertypriyaNoch keine Bewertungen

- Income From House PropertyDokument26 SeitenIncome From House PropertySuyash Patwa100% (1)

- HP MCQDokument7 SeitenHP MCQ887 shivam guptaNoch keine Bewertungen

- 2 - House Property Problems 22-23Dokument5 Seiten2 - House Property Problems 22-2320-UCO-517 AJAY KELVIN ANoch keine Bewertungen

- House Property PDFDokument43 SeitenHouse Property PDFK Vijay Bhaskar ReddyNoch keine Bewertungen

- Income Tax Law and PracticeDokument3 SeitenIncome Tax Law and PracticeAbinash VeeraragavanNoch keine Bewertungen

- Income From House Property: Annual ValueDokument6 SeitenIncome From House Property: Annual ValueSaddam KhanNoch keine Bewertungen

- BCom Business Taxation Income Tax and Sales Tax Numerical 2018Dokument5 SeitenBCom Business Taxation Income Tax and Sales Tax Numerical 2018AHSAN LASHARINoch keine Bewertungen

- Income From House Property-1Dokument18 SeitenIncome From House Property-1Aaditya BhardwajNoch keine Bewertungen

- CA INTER CompilerDokument12 SeitenCA INTER CompilernehajnvniwarsiNoch keine Bewertungen

- House ProDokument7 SeitenHouse Prosb_jainNoch keine Bewertungen

- Unit 5: Income From House PropertyDokument11 SeitenUnit 5: Income From House PropertySeshanki ChaudhariNoch keine Bewertungen

- Lecture 11 - Determination of Annual Value PDF-converted NewDokument38 SeitenLecture 11 - Determination of Annual Value PDF-converted NewK.NALININoch keine Bewertungen

- INCOME FROM HOUSE PROPERTYcrDokument8 SeitenINCOME FROM HOUSE PROPERTYcrShin VhanNoch keine Bewertungen

- IT QuestionDokument3 SeitenIT QuestionSathish SmartNoch keine Bewertungen

- Chapter 6. Income From Property v2Dokument6 SeitenChapter 6. Income From Property v2LEARN FROM MENoch keine Bewertungen

- Income Under The Head "Income From House Property" and Its ComputationDokument20 SeitenIncome Under The Head "Income From House Property" and Its ComputationAanchal SinghalNoch keine Bewertungen

- House Propery QuestionsDokument6 SeitenHouse Propery QuestionsTauseef AzharNoch keine Bewertungen

- Unit 2 (Income From House Property)Dokument13 SeitenUnit 2 (Income From House Property)Vijay GiriNoch keine Bewertungen

- ATax - 04 - Property UpdatedDokument17 SeitenATax - 04 - Property UpdatedHaseeb Ahmed ShaikhNoch keine Bewertungen

- House PropertyDokument36 SeitenHouse PropertyRahul Tanver0% (1)

- House PropertyDokument2 SeitenHouse PropertyJimmy ShergillNoch keine Bewertungen

- House Property - IllustrationDokument10 SeitenHouse Property - IllustrationAnirban ThakurNoch keine Bewertungen

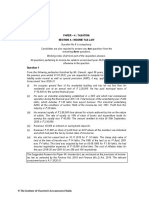

- Paper - 4: Taxation Section A: Income Tax Law: © The Institute of Chartered Accountants of IndiaDokument30 SeitenPaper - 4: Taxation Section A: Income Tax Law: © The Institute of Chartered Accountants of IndiaChhaya JajuNoch keine Bewertungen

- Lecture - 15: Computation of Income Under The Head House Property (Basic Terminology)Dokument41 SeitenLecture - 15: Computation of Income Under The Head House Property (Basic Terminology)Harjot SinghNoch keine Bewertungen

- Income Tax Law Practice Question PaperDokument0 SeitenIncome Tax Law Practice Question PaperbkamithNoch keine Bewertungen

- Income From House Property Income Chargeable To Tax Under The Head "House Property"Dokument10 SeitenIncome From House Property Income Chargeable To Tax Under The Head "House Property"Suriya DeviNoch keine Bewertungen

- Welcome To My Presentation: Susmit Singha ID:172011007 Department of Law Green University of BangladeshDokument5 SeitenWelcome To My Presentation: Susmit Singha ID:172011007 Department of Law Green University of BangladeshKUMAR SUSMITNoch keine Bewertungen

- House PropertyDokument14 SeitenHouse Property083 Ronak ShahNoch keine Bewertungen

- Income From House and BusinessDokument60 SeitenIncome From House and BusinessPuneet SinghNoch keine Bewertungen

- Income Tax and Auditing Code: B-104: AssignmentDokument2 SeitenIncome Tax and Auditing Code: B-104: AssignmentHritik singhNoch keine Bewertungen

- House PropertyDokument11 SeitenHouse PropertyMadhusudana p nNoch keine Bewertungen

- Income From House PropertyDokument47 SeitenIncome From House PropertyforamsssNoch keine Bewertungen

- Computation of Income From House PropertDokument23 SeitenComputation of Income From House PropertMríñålÀryäñNoch keine Bewertungen

- Basics & House Property - SolutionDokument6 SeitenBasics & House Property - Solutionvishwajeetpatil0542Noch keine Bewertungen

- CH 4 Income From House PropertyDokument89 SeitenCH 4 Income From House PropertyPratyashNoch keine Bewertungen

- Income From House PropertyDokument5 SeitenIncome From House Propertykiran malukaniNoch keine Bewertungen

- 75780bos61308 p4Dokument30 Seiten75780bos61308 p4Sathvika SathuNoch keine Bewertungen

- Legal and Taxation Aspect: House PropertyDokument2 SeitenLegal and Taxation Aspect: House PropertyPranav ShrivastavaNoch keine Bewertungen

- QB Ipu 2024Dokument2 SeitenQB Ipu 2024uditnarayan8721663Noch keine Bewertungen

- Less: Municipal Taxes Paid by Mr. Raj: © The Institute of Chartered Accountants of IndiaDokument11 SeitenLess: Municipal Taxes Paid by Mr. Raj: © The Institute of Chartered Accountants of IndiaKetan DedhaNoch keine Bewertungen

- Income Tax 20220119Dokument56 SeitenIncome Tax 20220119asadazhar002Noch keine Bewertungen

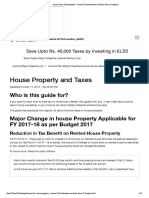

- Income From House Property - Income Tax Deductions On Home Loans & PropertyDokument13 SeitenIncome From House Property - Income Tax Deductions On Home Loans & Propertyrajesh_bNoch keine Bewertungen

- Income From House PropertyDokument31 SeitenIncome From House PropertyAarti SainiNoch keine Bewertungen

- Income From House Property PracticalDokument52 SeitenIncome From House Property PracticalShreekanta DattaNoch keine Bewertungen

- Offer and ObjectionDokument3 SeitenOffer and Objectionmarie deniegaNoch keine Bewertungen

- 165905-2011-Spouses Lago v. Abul Jr.20210424-12-15svzjrDokument8 Seiten165905-2011-Spouses Lago v. Abul Jr.20210424-12-15svzjrTure ThoreNoch keine Bewertungen

- 17 - Heirs of Arce v. DARDokument2 Seiten17 - Heirs of Arce v. DARPaul Joshua SubaNoch keine Bewertungen

- Rufino Luna, Et - Al V CA, Et - Al (G.R. No. 100374-75)Dokument3 SeitenRufino Luna, Et - Al V CA, Et - Al (G.R. No. 100374-75)Alainah ChuaNoch keine Bewertungen

- Official Language Policy OL - Docx-1Dokument10 SeitenOfficial Language Policy OL - Docx-1Vidhan Chandra ShahiNoch keine Bewertungen

- COMPANY Law - Business Law NotesDokument28 SeitenCOMPANY Law - Business Law NotesDiana FaridaNoch keine Bewertungen

- PDF Template Non Disclosure Agreement Nda TemplateDokument4 SeitenPDF Template Non Disclosure Agreement Nda TemplateFanny Romm Meneses100% (1)

- PR 1 by John Patrick Galbaroli-1-1Dokument6 SeitenPR 1 by John Patrick Galbaroli-1-1John Eevee Galbaroli PangilinanNoch keine Bewertungen

- Colorado Enhance Law Enforcement Integrity ActDokument25 SeitenColorado Enhance Law Enforcement Integrity ActMichael_Roberts2019100% (1)

- Joint Proposed Form of Order Granting in Part Plaintiffs' Motion For Preliminary Injunctive ReliefDokument6 SeitenJoint Proposed Form of Order Granting in Part Plaintiffs' Motion For Preliminary Injunctive ReliefKING 5 NewsNoch keine Bewertungen

- Hiring Any Attorney Waives Constitutional Protections, Makes Attorney - Wards of Court With Unsound MindDokument10 SeitenHiring Any Attorney Waives Constitutional Protections, Makes Attorney - Wards of Court With Unsound MindStephen Stewart100% (2)

- Ra 10756Dokument6 SeitenRa 10756Ar YanNoch keine Bewertungen

- Alvarez v. IAC - G.R. No. L-68053Dokument6 SeitenAlvarez v. IAC - G.R. No. L-68053Ann ChanNoch keine Bewertungen

- Yano CaseDokument4 SeitenYano CaseLeidi Chua BayudanNoch keine Bewertungen

- Republic Act No. 7883: An Act Granting Benefits and Incentives To Accredit Barangay Health Workers and For Other PurposesDokument2 SeitenRepublic Act No. 7883: An Act Granting Benefits and Incentives To Accredit Barangay Health Workers and For Other PurposesColleen De Guia Babalcon100% (1)

- Michigan Senate Bill 0044 (2023)Dokument2 SeitenMichigan Senate Bill 0044 (2023)WDIV/ClickOnDetroitNoch keine Bewertungen

- Pappuram CaseDokument2 SeitenPappuram CaseNupur KhandelwalNoch keine Bewertungen

- GR 173088 Aparejo Report On LTD FinalDokument8 SeitenGR 173088 Aparejo Report On LTD FinalmarlonNoch keine Bewertungen

- Neighborhood Watch ManualDokument37 SeitenNeighborhood Watch Manualdjdr1Noch keine Bewertungen

- Codthic June 12, 18Dokument48 SeitenCodthic June 12, 18sanNoch keine Bewertungen

- Republic Vs CA 107 SCRA 504Dokument2 SeitenRepublic Vs CA 107 SCRA 504Neon True BeldiaNoch keine Bewertungen

- GODARD V GRAY DigestDokument7 SeitenGODARD V GRAY DigeststoicclownNoch keine Bewertungen

- Roommate ContractDokument5 SeitenRoommate Contractapi-261355633Noch keine Bewertungen

- ADR Operations Manual - AC No 20-2002Dokument3 SeitenADR Operations Manual - AC No 20-2002Anonymous 03JIPKRkNoch keine Bewertungen

- People v. Ortega, Jr.Dokument1 SeitePeople v. Ortega, Jr.Kathleen del Rosario100% (2)

- Important Reminders: Step 1Dokument4 SeitenImportant Reminders: Step 1Kathleen ミNoch keine Bewertungen

- PublishedDokument14 SeitenPublishedScribd Government DocsNoch keine Bewertungen

- Carungcung v. NLRC, Sun Life Assurance Co. of Canada, G.R. No. 118086. December 15, 1997Dokument5 SeitenCarungcung v. NLRC, Sun Life Assurance Co. of Canada, G.R. No. 118086. December 15, 1997Tin LicoNoch keine Bewertungen

- Sps Jorge V MetrobankDokument2 SeitenSps Jorge V MetrobankJepoy FranciscoNoch keine Bewertungen

- Schedule E - Saudi Law IKDokument5 SeitenSchedule E - Saudi Law IKwangruiNoch keine Bewertungen