Das könnte Ihnen auch gefallen

- Qtrly - Reportq1 FY 2008 2009Dokument2 SeitenQtrly - Reportq1 FY 2008 2009Bhavin SagarNoch keine Bewertungen

- Yap 31 1 19Dokument345 SeitenYap 31 1 19Bhavin SagarNoch keine Bewertungen

- Nebbia Mutual NDADokument3 SeitenNebbia Mutual NDABhavin SagarNoch keine Bewertungen

- Bse Sme Ipo IndexDokument4 SeitenBse Sme Ipo IndexBhavin SagarNoch keine Bewertungen

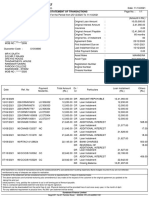

- Statement of Transactions: Sundaram Finance LimitedDokument1 SeiteStatement of Transactions: Sundaram Finance LimitedBhavin SagarNoch keine Bewertungen

- Revised Underwriting Agreement 31.03Dokument14 SeitenRevised Underwriting Agreement 31.03Bhavin SagarNoch keine Bewertungen

- Underwriters AgreementDokument15 SeitenUnderwriters AgreementBhavin SagarNoch keine Bewertungen

- Capital Reduction - Escorts LTD - GalacticoDokument10 SeitenCapital Reduction - Escorts LTD - GalacticoBhavin SagarNoch keine Bewertungen

- Amalgamation - Share India Securities - Turnaround Corporate AdvisorsDokument5 SeitenAmalgamation - Share India Securities - Turnaround Corporate AdvisorsBhavin SagarNoch keine Bewertungen

- August 2021 - Shipping Corporation of India LTD by Corporate ProfessionalsDokument10 SeitenAugust 2021 - Shipping Corporation of India LTD by Corporate ProfessionalsBhavin SagarNoch keine Bewertungen

- EKI Energy Services Limited: Payments MadeDokument2 SeitenEKI Energy Services Limited: Payments MadeBhavin SagarNoch keine Bewertungen

- Revised Market Making Agreement 31.03Dokument13 SeitenRevised Market Making Agreement 31.03Bhavin SagarNoch keine Bewertungen

- Amalgmation - August 2020 - Arihant Capital Shree Renuka Sugars LTDDokument10 SeitenAmalgmation - August 2020 - Arihant Capital Shree Renuka Sugars LTDBhavin SagarNoch keine Bewertungen

- Revised RV - Draft Valuation Report - Hakuna MatataDokument11 SeitenRevised RV - Draft Valuation Report - Hakuna MatataBhavin SagarNoch keine Bewertungen

- Demerger May 2021 - Tips Industries LTD by Inga Advisors MumbaiDokument4 SeitenDemerger May 2021 - Tips Industries LTD by Inga Advisors MumbaiBhavin SagarNoch keine Bewertungen

- MCA FinanicialsDokument50 SeitenMCA FinanicialsBhavin SagarNoch keine Bewertungen

- 01 Business Partnership Powerpoint TemplateDokument12 Seiten01 Business Partnership Powerpoint TemplateBhavin SagarNoch keine Bewertungen

- List of Valuation ReportsDokument18 SeitenList of Valuation ReportsBhavin SagarNoch keine Bewertungen

- 02 Corporate Orange Powerpoint Presentations 16x9 1Dokument13 Seiten02 Corporate Orange Powerpoint Presentations 16x9 1Bhavin SagarNoch keine Bewertungen

- EKI Energy Services Limited: Payments MadeDokument2 SeitenEKI Energy Services Limited: Payments MadeBhavin SagarNoch keine Bewertungen

- Corporate Deck - InternationalDokument16 SeitenCorporate Deck - InternationalBhavin SagarNoch keine Bewertungen

- 01 Business Partnership Powerpoint TemplateDokument12 Seiten01 Business Partnership Powerpoint TemplateBhavin SagarNoch keine Bewertungen

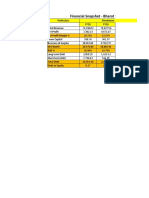

- Bharat Serums & Vaccines LTD - Financial SnapshotDokument2 SeitenBharat Serums & Vaccines LTD - Financial SnapshotBhavin SagarNoch keine Bewertungen

- Valuation Assignement - WIPDokument2 SeitenValuation Assignement - WIPBhavin SagarNoch keine Bewertungen

- Bulk DealsDokument63 SeitenBulk DealsBhavin SagarNoch keine Bewertungen

- Bhavin Valuation Cases For FY21Dokument17 SeitenBhavin Valuation Cases For FY21Bhavin SagarNoch keine Bewertungen

- Bhavin - Valuation Cases - May 2021Dokument3 SeitenBhavin - Valuation Cases - May 2021Bhavin SagarNoch keine Bewertungen

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5795)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (588)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (74)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (895)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (400)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2259)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (266)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (121)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- Driving Ambitions: The Business Case For Circular Economy in The Car IndustryDokument24 SeitenDriving Ambitions: The Business Case For Circular Economy in The Car IndustryComunicarSe-ArchivoNoch keine Bewertungen

- Palash RanchiDokument11 SeitenPalash RanchiBookya RajeshNoch keine Bewertungen

- MSDS BP Energol THB 46 PDFDokument4 SeitenMSDS BP Energol THB 46 PDFzaidan hadiNoch keine Bewertungen

- Angel ChennaiDokument34 SeitenAngel ChennaiData InfobankNoch keine Bewertungen

- Department of Construction Technology and Management: Specification and Quantity SurveyingDokument17 SeitenDepartment of Construction Technology and Management: Specification and Quantity Surveyingsamrawit aysheshimNoch keine Bewertungen

- Prathap Rajendran: Marketing ProfessionalDokument1 SeitePrathap Rajendran: Marketing ProfessionalNithyaNoch keine Bewertungen

- FabHotels 378L3 2223 01020 Invoice ZAKCAJDokument2 SeitenFabHotels 378L3 2223 01020 Invoice ZAKCAJRaviNoch keine Bewertungen

- Competencies FrameworkDokument17 SeitenCompetencies FrameworkVirah Sammy ChandraNoch keine Bewertungen

- CityLoops 2023 Handbook BiowasteDokument47 SeitenCityLoops 2023 Handbook BiowasteOCENR Legazpi CityR.M.AbacheNoch keine Bewertungen

- Waseeem Resume 222Dokument2 SeitenWaseeem Resume 222waseemraja1923Noch keine Bewertungen

- Sales and Distribution MGMT - Tapan K PandaDokument195 SeitenSales and Distribution MGMT - Tapan K PandaAvnit Chaudhary84% (19)

- Recruitment Tracker Someka Excel Template V9 Free Version 2Dokument5 SeitenRecruitment Tracker Someka Excel Template V9 Free Version 2haziziNoch keine Bewertungen

- SMM PanelDokument6 SeitenSMM PanelAneesh SharmaNoch keine Bewertungen

- Test 1 - 2021 - Mac 320Dokument17 SeitenTest 1 - 2021 - Mac 320pretty jesayaNoch keine Bewertungen

- GIM Assignment May 22Dokument16 SeitenGIM Assignment May 22shittu titilayo maryNoch keine Bewertungen

- Topic 1 Boundaries of The FirmDokument49 SeitenTopic 1 Boundaries of The FirmPeter MastersNoch keine Bewertungen

- SecA Group8 CaseMichiganManufacturingCorpDokument7 SeitenSecA Group8 CaseMichiganManufacturingCorpSuyash LoiwalNoch keine Bewertungen

- Seatwork - Day 20 - Leases AnswersDokument9 SeitenSeatwork - Day 20 - Leases AnswersRj ArenasNoch keine Bewertungen

- A Project On: Study On Challenges Encountered by The Start-Ups in IndiaDokument93 SeitenA Project On: Study On Challenges Encountered by The Start-Ups in IndiaAnas KaunchaleNoch keine Bewertungen

- Beautify - McKinsey & CompanyDokument6 SeitenBeautify - McKinsey & Companyieva_91Noch keine Bewertungen

- Journal of Business Strategy: Article InformationDokument6 SeitenJournal of Business Strategy: Article InformationWilliam YamadaNoch keine Bewertungen

- FM11 CH 12 Mini CaseDokument14 SeitenFM11 CH 12 Mini CaseRahul Rathi100% (1)

- GFR IiiDokument128 SeitenGFR Iiiavinash_vyas77813Noch keine Bewertungen

- CBE Lead Auditor Course ENDokument2 SeitenCBE Lead Auditor Course ENSaid AbdallahNoch keine Bewertungen

- Functions of InsuranceDokument8 SeitenFunctions of InsuranceBasappaSarkarNoch keine Bewertungen

- VelascoDokument3 SeitenVelascoRaymart SalamidaNoch keine Bewertungen

- Problem Sets Solutions 1 Accounting Statements and Cash FlowDokument5 SeitenProblem Sets Solutions 1 Accounting Statements and Cash FlowYaoyin Bonnie ChenNoch keine Bewertungen

- Industrial Management & Engineering EconomyDokument189 SeitenIndustrial Management & Engineering EconomyFejiru MuzemilNoch keine Bewertungen

- Answers R41920 Acctg Varsity Basic Acctg Level 1Dokument6 SeitenAnswers R41920 Acctg Varsity Basic Acctg Level 1John AceNoch keine Bewertungen

- Corporate Financial Accounting 16Th Edition Carl S Warren Full ChapterDokument51 SeitenCorporate Financial Accounting 16Th Edition Carl S Warren Full Chapterwm.baker518100% (10)