Das könnte Ihnen auch gefallen

- Ias 12 Income TaxesDokument52 SeitenIas 12 Income TaxesJames MutarauswaNoch keine Bewertungen

- Chapter-15 Tax CreditsDokument18 SeitenChapter-15 Tax CreditsakhtarNoch keine Bewertungen

- Sa 5 DT NovDokument9 SeitenSa 5 DT NovRishabh GargNoch keine Bewertungen

- PGBPDokument45 SeitenPGBPNidhi Lath100% (1)

- AFAR1 Franchise Accounting PDFDokument12 SeitenAFAR1 Franchise Accounting PDFMary Ann Hernandez DiomampoNoch keine Bewertungen

- 2023 Monthly Tax Special Topic June SlidesDokument44 Seiten2023 Monthly Tax Special Topic June Slidesgreenemma703Noch keine Bewertungen

- Final IBF (Numerical) Chapter 2, 5 & 15Dokument13 SeitenFinal IBF (Numerical) Chapter 2, 5 & 15Imtiaz SultanNoch keine Bewertungen

- Salient Features of Income Tax Act 2023Dokument79 SeitenSalient Features of Income Tax Act 2023Md. Abdullah Al ImranNoch keine Bewertungen

- C.1. G.R. No. 202792-2019-La - Sallian - Educational - Innovators - Foundation Vs CIRDokument11 SeitenC.1. G.R. No. 202792-2019-La - Sallian - Educational - Innovators - Foundation Vs CIR0506sheltonNoch keine Bewertungen

- FA - Pre Foundation Phase - Sample PaperDokument5 SeitenFA - Pre Foundation Phase - Sample PaperJaved MohammedNoch keine Bewertungen

- INCOME TAX Imp - SectionsDokument7 SeitenINCOME TAX Imp - SectionsDeepak Singh100% (1)

- Acc 110 Practice SetDokument42 SeitenAcc 110 Practice SetAndrea Marie P. GarinNoch keine Bewertungen

- CPAR Intro To Income Tax and Tax On Individuals Batch 91 HandoutDokument33 SeitenCPAR Intro To Income Tax and Tax On Individuals Batch 91 Handoutjohn paulNoch keine Bewertungen

- Answers, Solutions and Clarifications To Form 6Dokument5 SeitenAnswers, Solutions and Clarifications To Form 6Annie LindNoch keine Bewertungen

- WEEK 3-CPAR Intro To Income Tax and Income Tax On Individuals (Batch 92) - HandoutDokument33 SeitenWEEK 3-CPAR Intro To Income Tax and Income Tax On Individuals (Batch 92) - HandoutKristelleNoch keine Bewertungen

- TAX 03 Fundamentals of Income Taxation PDFDokument9 SeitenTAX 03 Fundamentals of Income Taxation PDFNita Costillas De MattaNoch keine Bewertungen

- 3109 - Taxation of Non-Individual TaxpayersDokument9 Seiten3109 - Taxation of Non-Individual TaxpayersMae Angiela TansecoNoch keine Bewertungen

- H04 - Final Income TaxationDokument6 SeitenH04 - Final Income Taxationnona galidoNoch keine Bewertungen

- Exam Practice Question Glori Fried Chicken Rima Puri v2 WZ AnswersDokument4 SeitenExam Practice Question Glori Fried Chicken Rima Puri v2 WZ AnswersJœ œNoch keine Bewertungen

- CGT - Fundamentals: Currency: 30 August 2017 (v006.5)Dokument59 SeitenCGT - Fundamentals: Currency: 30 August 2017 (v006.5)Jessica YuNoch keine Bewertungen

- Intangible Assets HomeworkDokument5 SeitenIntangible Assets HomeworkIsabelle Guillena100% (2)

- Bir Form 1603Dokument3 SeitenBir Form 1603Nava NavarreteNoch keine Bewertungen

- IFITC Chapter - 4 - 2019Dokument38 SeitenIFITC Chapter - 4 - 2019Kirill KucherenkoNoch keine Bewertungen

- Question Cpa-00102: Becker Professional Education Registered To: Dominique DantonioDokument111 SeitenQuestion Cpa-00102: Becker Professional Education Registered To: Dominique DantonioNhel Alvaro100% (1)

- Quarterly Remittance Return of Final Income Taxes Withheld: Background InformationDokument2 SeitenQuarterly Remittance Return of Final Income Taxes Withheld: Background InformationVincent John RigorNoch keine Bewertungen

- Kirby 1Q20 Earnings Presentation VFDokument14 SeitenKirby 1Q20 Earnings Presentation VFGerman O.Noch keine Bewertungen

- Pilmico Vs CIRDokument9 SeitenPilmico Vs CIRERNIL L BAWANoch keine Bewertungen

- Accounts Super Revision Marathon Notes Part 2Dokument157 SeitenAccounts Super Revision Marathon Notes Part 2gaxovi4187Noch keine Bewertungen

- O Reissue of 2019 Financial Statements o 1Q20 ResultsDokument17 SeitenO Reissue of 2019 Financial Statements o 1Q20 Resultsjenric19Noch keine Bewertungen

- All TaxesDokument9 SeitenAll TaxesJv FerminNoch keine Bewertungen

- Lesson 8: Deductions To Gross IncomeDokument28 SeitenLesson 8: Deductions To Gross IncomeeuniNoch keine Bewertungen

- Income TaxDokument31 SeitenIncome TaxUday KumarNoch keine Bewertungen

- Capital Gains and Losses: Ebook Summary - Chapter 12Dokument1 SeiteCapital Gains and Losses: Ebook Summary - Chapter 12arianxxxNoch keine Bewertungen

- DT RevisionDokument133 SeitenDT RevisionharshallahotNoch keine Bewertungen

- OwnerOccupiedExample - BLANKDokument3 SeitenOwnerOccupiedExample - BLANKmohahossam1992Noch keine Bewertungen

- TAX 2202E TBS01 02.solutionDokument2 SeitenTAX 2202E TBS01 02.solutionZhitong LuNoch keine Bewertungen

- Ifrs December 2020 Key WebDokument10 SeitenIfrs December 2020 Key Webjad NasserNoch keine Bewertungen

- Module 8 - Deductions From Gross IncomeDokument12 SeitenModule 8 - Deductions From Gross IncomeJimbo ManalastasNoch keine Bewertungen

- Republic Act No. 11976 (EOPT) - Infographics - SGVDokument3 SeitenRepublic Act No. 11976 (EOPT) - Infographics - SGVAlbert SantiagoNoch keine Bewertungen

- Module 35 Taxes: Partnerships:: 'S CC G C C Se e I 7 .E., o Co - Es Y. S CDokument2 SeitenModule 35 Taxes: Partnerships:: 'S CC G C C Se e I 7 .E., o Co - Es Y. S CEl Sayed AbdelgawwadNoch keine Bewertungen

- 8.special Tax Rates of Companies & MATDokument22 Seiten8.special Tax Rates of Companies & MATMuthu nayagamNoch keine Bewertungen

- Pakistan Income Tax LawDokument22 SeitenPakistan Income Tax Lawhssaroch75% (4)

- TAXATIONDokument3 SeitenTAXATIONcherry blossomNoch keine Bewertungen

- ACCTG 029 - Final Quiz 1Dokument1 SeiteACCTG 029 - Final Quiz 1mcespressoblendNoch keine Bewertungen

- ABC - Consolidated Financial Statement Date of AcquisitionDokument4 SeitenABC - Consolidated Financial Statement Date of AcquisitionJoshuji LaneNoch keine Bewertungen

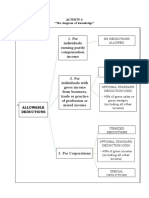

- For Individuals Earning Purely Compensation Income: Allowable DeductionsDokument4 SeitenFor Individuals Earning Purely Compensation Income: Allowable DeductionsJAN FEVRIER OLETENoch keine Bewertungen

- SCH 19Dokument10 SeitenSCH 19Vishal P RaoNoch keine Bewertungen

- BTAXREV Week 4 ACT185 Preferential Taxation 2Dokument16 SeitenBTAXREV Week 4 ACT185 Preferential Taxation 2gatotkaNoch keine Bewertungen

- ACC 309 FinalDokument42 SeitenACC 309 FinalSalman Khalid77% (22)

- CAPITALGAINS 3rdsep PDFDokument202 SeitenCAPITALGAINS 3rdsep PDFPhani Kumar SomarajupalliNoch keine Bewertungen

- Recent Developments in RE Laws Taxation by CA. Jayesh Kariya 1 PDFDokument55 SeitenRecent Developments in RE Laws Taxation by CA. Jayesh Kariya 1 PDFManu IttinaNoch keine Bewertungen

- Income Tax On Salaried EmployeesDokument22 SeitenIncome Tax On Salaried EmployeesAmin Haider Shah100% (1)

- Invalidating Tax Assessment January 2024 2Dokument68 SeitenInvalidating Tax Assessment January 2024 2arnulfojr hicoNoch keine Bewertungen

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineVon EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNoch keine Bewertungen

- What Every Real Estate Investor Needs to Know About Cash Flow... And 36 Other Key Financial Measures, Updated EditionVon EverandWhat Every Real Estate Investor Needs to Know About Cash Flow... And 36 Other Key Financial Measures, Updated EditionBewertung: 4.5 von 5 Sternen4.5/5 (15)

- PricewaterhouseCoopers' Guide to the New Tax RulesVon EverandPricewaterhouseCoopers' Guide to the New Tax RulesNoch keine Bewertungen

- CPA Review Notes 2019 - FAR (Financial Accounting and Reporting)Von EverandCPA Review Notes 2019 - FAR (Financial Accounting and Reporting)Bewertung: 3.5 von 5 Sternen3.5/5 (17)

- Week 8 - Other Rollover Provisions, Estate Planning and Death of TaxapyerDokument32 SeitenWeek 8 - Other Rollover Provisions, Estate Planning and Death of TaxapyerMike RaitsinNoch keine Bewertungen

- Week 4 - Sale of Shares Vs Assets - Post On CanvasDokument24 SeitenWeek 4 - Sale of Shares Vs Assets - Post On CanvasMike RaitsinNoch keine Bewertungen

- Week 7 - Anti Avoidance ProvisionsDokument27 SeitenWeek 7 - Anti Avoidance ProvisionsMike RaitsinNoch keine Bewertungen

- Week 3 - Corporate Disributions, PUC, Surplus, Deemed Dividends and Wind Up - Post On CanvasDokument33 SeitenWeek 3 - Corporate Disributions, PUC, Surplus, Deemed Dividends and Wind Up - Post On CanvasMike RaitsinNoch keine Bewertungen

- Week 1 and 2 Review - Shareholder Manager Renumeration and AOC - Post On CanvasDokument37 SeitenWeek 1 and 2 Review - Shareholder Manager Renumeration and AOC - Post On CanvasMike RaitsinNoch keine Bewertungen

- Rfso S A0011749958 1Dokument3 SeitenRfso S A0011749958 1Marian DimaNoch keine Bewertungen

- SPICESDokument10 SeitenSPICESjay bapodaraNoch keine Bewertungen

- Exception Report Document CodesDokument33 SeitenException Report Document CodesForeclosure Fraud100% (1)

- NSF International / Nonfood Compounds Registration ProgramDokument1 SeiteNSF International / Nonfood Compounds Registration ProgramMichaelNoch keine Bewertungen

- Dumo Vs RepublicDokument12 SeitenDumo Vs RepublicGladys BantilanNoch keine Bewertungen

- SPF 5189zdsDokument10 SeitenSPF 5189zdsAparna BhardwajNoch keine Bewertungen

- CA CHP555 Manual 2 2003 ch1-13Dokument236 SeitenCA CHP555 Manual 2 2003 ch1-13Lucas OjedaNoch keine Bewertungen

- 2011 CIVITAS Benefit JournalDokument40 Seiten2011 CIVITAS Benefit JournalCIVITASNoch keine Bewertungen

- Final ReviewDokument14 SeitenFinal ReviewBhavya JainNoch keine Bewertungen

- Bagabuyo v. Comelec, GR 176970Dokument2 SeitenBagabuyo v. Comelec, GR 176970Chester Santos SoniegaNoch keine Bewertungen

- (Complaint Affidavit For Filing of BP 22 Case) Complaint-AffidavitDokument2 Seiten(Complaint Affidavit For Filing of BP 22 Case) Complaint-AffidavitRonnie JimenezNoch keine Bewertungen

- Bookkeeping PresentationDokument20 SeitenBookkeeping Presentationrose gabonNoch keine Bewertungen

- 005 SPARK v. Quezon City G.R. No. 225442Dokument28 Seiten005 SPARK v. Quezon City G.R. No. 225442Kenneth EsquilloNoch keine Bewertungen

- Revenue Regulations No. 7-2012 (Sections 3 To 9 Only)Dokument43 SeitenRevenue Regulations No. 7-2012 (Sections 3 To 9 Only)Charmaine GraceNoch keine Bewertungen

- Pratical Venue Letter ICT 417 ParticalDokument2 SeitenPratical Venue Letter ICT 417 ParticalCh MusaNoch keine Bewertungen

- Bus Ticket Invoice 1465625515Dokument2 SeitenBus Ticket Invoice 1465625515Manthan MarvaniyaNoch keine Bewertungen

- Introduction To The Study of RizalDokument2 SeitenIntroduction To The Study of RizalCherry Mae Luchavez FloresNoch keine Bewertungen

- Narcotrafico: El Gran Desafío de Calderón (Book Review)Dokument5 SeitenNarcotrafico: El Gran Desafío de Calderón (Book Review)James CreechanNoch keine Bewertungen

- Nobels Ab1 SwitcherDokument1 SeiteNobels Ab1 SwitcherJosé FranciscoNoch keine Bewertungen

- Position Paper in Purposive CommunicationDokument2 SeitenPosition Paper in Purposive CommunicationKhynjoan AlfilerNoch keine Bewertungen

- CHALLANDokument1 SeiteCHALLANDaniyal ArifNoch keine Bewertungen

- Eric Adams' Approval Rating Falls To 29% As Voters Sour On NYC FutureDokument1 SeiteEric Adams' Approval Rating Falls To 29% As Voters Sour On NYC FutureRamonita GarciaNoch keine Bewertungen

- JAbraManual bt2020Dokument15 SeitenJAbraManual bt2020HuwNoch keine Bewertungen

- Position PAperDokument11 SeitenPosition PAperDan CuestaNoch keine Bewertungen

- CH05 Transaction List by Date 2026Dokument4 SeitenCH05 Transaction List by Date 2026kjoel.ngugiNoch keine Bewertungen

- K. A. Abbas v. Union of India - A Case StudyDokument4 SeitenK. A. Abbas v. Union of India - A Case StudyAditya pal100% (2)

- Management of TrustsDokument4 SeitenManagement of Trustsnikhil jkcNoch keine Bewertungen

- Promissory Notes Are Legal Tender BecauseDokument2 SeitenPromissory Notes Are Legal Tender BecauseDUTCH55140091% (23)

- Main ProjectDokument67 SeitenMain ProjectJesus RamyaNoch keine Bewertungen

- Consti (Taxation)Dokument2 SeitenConsti (Taxation)Mayra MerczNoch keine Bewertungen