Das könnte Ihnen auch gefallen

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryVon EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryBewertung: 3.5 von 5 Sternen3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Von EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Bewertung: 4.5 von 5 Sternen4.5/5 (119)

- Never Split the Difference: Negotiating As If Your Life Depended On ItVon EverandNever Split the Difference: Negotiating As If Your Life Depended On ItBewertung: 4.5 von 5 Sternen4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaVon EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaBewertung: 4.5 von 5 Sternen4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingVon EverandThe Little Book of Hygge: Danish Secrets to Happy LivingBewertung: 3.5 von 5 Sternen3.5/5 (399)

- Grit: The Power of Passion and PerseveranceVon EverandGrit: The Power of Passion and PerseveranceBewertung: 4 von 5 Sternen4/5 (587)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyVon EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyBewertung: 3.5 von 5 Sternen3.5/5 (2219)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeVon EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeBewertung: 4 von 5 Sternen4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnVon EverandTeam of Rivals: The Political Genius of Abraham LincolnBewertung: 4.5 von 5 Sternen4.5/5 (234)

- Shoe Dog: A Memoir by the Creator of NikeVon EverandShoe Dog: A Memoir by the Creator of NikeBewertung: 4.5 von 5 Sternen4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerVon EverandThe Emperor of All Maladies: A Biography of CancerBewertung: 4.5 von 5 Sternen4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreVon EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreBewertung: 4 von 5 Sternen4/5 (1090)

- Her Body and Other Parties: StoriesVon EverandHer Body and Other Parties: StoriesBewertung: 4 von 5 Sternen4/5 (821)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersVon EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersBewertung: 4.5 von 5 Sternen4.5/5 (344)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceVon EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceBewertung: 4 von 5 Sternen4/5 (890)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureVon EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureBewertung: 4.5 von 5 Sternen4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaVon EverandThe Unwinding: An Inner History of the New AmericaBewertung: 4 von 5 Sternen4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)Von EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Bewertung: 4 von 5 Sternen4/5 (98)

- On Fire: The (Burning) Case for a Green New DealVon EverandOn Fire: The (Burning) Case for a Green New DealBewertung: 4 von 5 Sternen4/5 (73)

- KieselDokument38 SeitenKieselNEWS CENTER Maine100% (1)

- Flightline Maintenance Manual: Flight Control SystemDokument101 SeitenFlightline Maintenance Manual: Flight Control SystemAVDB100% (2)

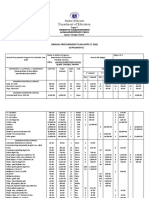

- ANNUAL PROCUREMENT PLAN - APP SupplementalDokument5 SeitenANNUAL PROCUREMENT PLAN - APP SupplementalCarlota Tejero100% (3)

- Erp Interview Questions and Answers PDFDokument2 SeitenErp Interview Questions and Answers PDFAprilNoch keine Bewertungen

- RC CA Curs 03 Digital Transmission ASK FSK PSKDokument54 SeitenRC CA Curs 03 Digital Transmission ASK FSK PSKRed FoxNoch keine Bewertungen

- ECON 601 - Module 7 PS - Solutions - FA 19 PDFDokument8 SeitenECON 601 - Module 7 PS - Solutions - FA 19 PDFTamzid IslamNoch keine Bewertungen

- Module 7Dokument2 SeitenModule 7Tamzid IslamNoch keine Bewertungen

- ECON 601 - Module 6 PS - Solutions - FA 19 PDFDokument16 SeitenECON 601 - Module 6 PS - Solutions - FA 19 PDFTamzid IslamNoch keine Bewertungen

- ECON 601 - Module 4 PS - Solutions - FA 19 PDFDokument11 SeitenECON 601 - Module 4 PS - Solutions - FA 19 PDFTamzid IslamNoch keine Bewertungen

- TamzidulTomIslam - MariahRippe.ErnaRismawaty - ECON 601 - Module 6 PSDokument24 SeitenTamzidulTomIslam - MariahRippe.ErnaRismawaty - ECON 601 - Module 6 PSTamzid IslamNoch keine Bewertungen

- ECON 601 - Module 2 PS - Solutions - FA 19 PDFDokument9 SeitenECON 601 - Module 2 PS - Solutions - FA 19 PDFTamzid IslamNoch keine Bewertungen

- ECON 601 - Module 3 PS - Solutions - FA 19 PDFDokument12 SeitenECON 601 - Module 3 PS - Solutions - FA 19 PDFTamzid IslamNoch keine Bewertungen

- TamzidulTomIslam - MariahRippe.ErnaRismawaty - ECON 601 - Module 6 PS PDFDokument20 SeitenTamzidulTomIslam - MariahRippe.ErnaRismawaty - ECON 601 - Module 6 PS PDFTamzid IslamNoch keine Bewertungen

- Log Models 2Dokument8 SeitenLog Models 2babutu123Noch keine Bewertungen

- TamzidulTom - Islam.MariahRippe - ErnaRismawaty.ECON 601 Module 5 PS - FA 19 PDFDokument11 SeitenTamzidulTom - Islam.MariahRippe - ErnaRismawaty.ECON 601 Module 5 PS - FA 19 PDFTamzid IslamNoch keine Bewertungen

- Syllabus CloudDokument3 SeitenSyllabus CloudphotosvideosmeowNoch keine Bewertungen

- Cyber-Physical Energy Systems Security Threat Modeling Risk Assessment Resources Metrics and Case StudiesDokument44 SeitenCyber-Physical Energy Systems Security Threat Modeling Risk Assessment Resources Metrics and Case StudiesAwishka ThuduwageNoch keine Bewertungen

- ZIA Fundamentals Student GuideDokument65 SeitenZIA Fundamentals Student GuideJSA JSANoch keine Bewertungen

- FIN Basic Tracker Step-by-Step Connection Guide: To Start Using This Document, Click HereDokument53 SeitenFIN Basic Tracker Step-by-Step Connection Guide: To Start Using This Document, Click Herewafa hedhliNoch keine Bewertungen

- Artificial Intelligence and The Reshaping of SEO: A Quantitative Analysis of AI-Driven Content Effects On Search AlgorithmsDokument7 SeitenArtificial Intelligence and The Reshaping of SEO: A Quantitative Analysis of AI-Driven Content Effects On Search AlgorithmsInternational Journal of Innovative Science and Research TechnologyNoch keine Bewertungen

- Width: 09c7fe2-1104514.css:1Dokument5 SeitenWidth: 09c7fe2-1104514.css:1Sean RoxasNoch keine Bewertungen

- VO ReseachPrinciplesII A4Dokument14 SeitenVO ReseachPrinciplesII A4Victor OkhoyaNoch keine Bewertungen

- Enterprise FW 05-Central ManagementDokument34 SeitenEnterprise FW 05-Central ManagementMarcos Vinicios Santos CorrêaNoch keine Bewertungen

- Garmin Pilot Users Guide For IosDokument188 SeitenGarmin Pilot Users Guide For IosKok KokNoch keine Bewertungen

- Access 9810 - UM (2018)Dokument218 SeitenAccess 9810 - UM (2018)Omar Alfredo Del Castillo QuispeNoch keine Bewertungen

- BlueZone Display & Printer HelpDokument688 SeitenBlueZone Display & Printer HelpLalo EscuderoNoch keine Bewertungen

- SM Mar2022Dokument60 SeitenSM Mar2022ehabNoch keine Bewertungen

- Fpga Implementation of Neural Networks: Main ContentsDokument21 SeitenFpga Implementation of Neural Networks: Main Contentsatef BenhaouesNoch keine Bewertungen

- Is Chapter 12Dokument6 SeitenIs Chapter 12Isabel ObordoNoch keine Bewertungen

- Zoom Setup InstructionsDokument5 SeitenZoom Setup InstructionsoNoch keine Bewertungen

- Student Roll Number and Name ListDokument4 SeitenStudent Roll Number and Name ListAryadeep ChakrabortyNoch keine Bewertungen

- Coot TutorialDokument21 SeitenCoot TutorialLINGCHEN TANNoch keine Bewertungen

- List of Materials With Out COE As USADokument77 SeitenList of Materials With Out COE As USAమనోహర్ రెడ్డిNoch keine Bewertungen

- Enterprise SEO PlatformsDokument58 SeitenEnterprise SEO PlatformsPolyNoch keine Bewertungen

- Sip Tls Between Ios Sip Gateway and Callmanager Configuration ExampleDokument14 SeitenSip Tls Between Ios Sip Gateway and Callmanager Configuration Examplejorigoni2013Noch keine Bewertungen

- Review Chapter 3Dokument8 SeitenReview Chapter 3Ahmed HassanNoch keine Bewertungen

- Chapter 3. The Fundamentals: Algorithms The Integers: Please Write Your NameDokument2 SeitenChapter 3. The Fundamentals: Algorithms The Integers: Please Write Your NameQuang NguyenNoch keine Bewertungen

- PI Server 2012 System Management GuideDokument222 SeitenPI Server 2012 System Management GuidePelife GoNoch keine Bewertungen

- Analyzed 2k Data Scientist and Data Engineer Jobs: Keywords and RequirementsDokument17 SeitenAnalyzed 2k Data Scientist and Data Engineer Jobs: Keywords and RequirementsMatheus MarinatoNoch keine Bewertungen

- Pm Debug InfoDokument86 SeitenPm Debug Infoteodorescumanu279Noch keine Bewertungen