Das könnte Ihnen auch gefallen

- 2018 CIO Tech Poll: Economic OutlookDokument8 Seiten2018 CIO Tech Poll: Economic OutlookIDG_World100% (1)

- Gartner - Big Data Industry InsightsDokument41 SeitenGartner - Big Data Industry InsightsAndrey PritulyukNoch keine Bewertungen

- 21st Annual Global Ceo Survey Us SupplementDokument19 Seiten21st Annual Global Ceo Survey Us Supplementjayaramonline840Noch keine Bewertungen

- Roland Berger Myanmar Business Survey 1Dokument20 SeitenRoland Berger Myanmar Business Survey 1THAN HANNoch keine Bewertungen

- Seven Keys To Privacy White PaperDokument8 SeitenSeven Keys To Privacy White Paperzhiqunzeng1Noch keine Bewertungen

- NDTV and The Indian Broadcasting Industry: Research HighlightsDokument3 SeitenNDTV and The Indian Broadcasting Industry: Research Highlightssel23Noch keine Bewertungen

- CIO Tech Poll: Tech Priorities 2018Dokument7 SeitenCIO Tech Poll: Tech Priorities 2018IDG_WorldNoch keine Bewertungen

- 27th Ceo SurveyDokument29 Seiten27th Ceo SurveyRobert Frederic WoolleyNoch keine Bewertungen

- 2023 WIND Ventures VC Survey On Latin America For Startup GrowthDokument13 Seiten2023 WIND Ventures VC Survey On Latin America For Startup GrowthWIND VenturesNoch keine Bewertungen

- SME A2F Country2018 EUDokument2 SeitenSME A2F Country2018 EUUdroiu Radu BogdanNoch keine Bewertungen

- 2023 December Nick Atkeson How To Make Money in A World Where Fin Analyst Are WrongDokument60 Seiten2023 December Nick Atkeson How To Make Money in A World Where Fin Analyst Are WrongBob ReeceNoch keine Bewertungen

- Consumer Fintech Adoption Rates Globally From 2015 To 2019, by CategoryDokument1 SeiteConsumer Fintech Adoption Rates Globally From 2015 To 2019, by CategoryAbhishek ChhikaraNoch keine Bewertungen

- Caso Sanitas - ENGDokument3 SeitenCaso Sanitas - ENGGustavo Cruzado AsencioNoch keine Bewertungen

- Financial Services Talent Trends 2019Dokument12 SeitenFinancial Services Talent Trends 2019Marco MolanoNoch keine Bewertungen

- Corporation of Hamilton Research Results - July 6th 2010 RevisedDokument10 SeitenCorporation of Hamilton Research Results - July 6th 2010 RevisedbernewsNoch keine Bewertungen

- Real Estate in A Mixed Asset Portfolio: Djavadi, S - HSU, YP - Hoang, W - Luftschitz, B - Ullrich, SDokument25 SeitenReal Estate in A Mixed Asset Portfolio: Djavadi, S - HSU, YP - Hoang, W - Luftschitz, B - Ullrich, SwilliamhoangNoch keine Bewertungen

- 2020 SaaS Benchmarks Deck VFINALDokument53 Seiten2020 SaaS Benchmarks Deck VFINALAbcd123411Noch keine Bewertungen

- PWC H1 2020 Global Crypto M&A Fundraising Report Oct 2020 PDFDokument26 SeitenPWC H1 2020 Global Crypto M&A Fundraising Report Oct 2020 PDFForkLogNoch keine Bewertungen

- OOH Barometer: In&Out View and Full Channel Landscape For Snacks & DrinksDokument14 SeitenOOH Barometer: In&Out View and Full Channel Landscape For Snacks & DrinksQuynh TrangNoch keine Bewertungen

- IIM Kashipur Summer Placement Report 2017Dokument6 SeitenIIM Kashipur Summer Placement Report 2017Sarvesh GuptaNoch keine Bewertungen

- 2019.02.21 - OCEG Webinar - 2019 GRC Technology Survey Webinar-FINALDokument29 Seiten2019.02.21 - OCEG Webinar - 2019 GRC Technology Survey Webinar-FINALMuralidharNoch keine Bewertungen

- Key Findings: Pe Exits: 2018 Annual African Private Equity Data TrackerDokument1 SeiteKey Findings: Pe Exits: 2018 Annual African Private Equity Data TrackerethernalxNoch keine Bewertungen

- 2022 SaaS Performance Reporting BenchmarksDokument24 Seiten2022 SaaS Performance Reporting BenchmarksDương Thị Lệ QuyênNoch keine Bewertungen

- PWC Global Crypto M A and Fundraising Report April 2020Dokument28 SeitenPWC Global Crypto M A and Fundraising Report April 2020ForkLogNoch keine Bewertungen

- AvlogWealth Tech Research ReportDokument14 SeitenAvlogWealth Tech Research ReportVishnuTejaChundiNoch keine Bewertungen

- Salary Survey 2010Dokument36 SeitenSalary Survey 2010mauricechoyNoch keine Bewertungen

- The State of Crypto - Corporate Adoption - CoinbaseDokument14 SeitenThe State of Crypto - Corporate Adoption - CoinbaseKoloNoch keine Bewertungen

- Vietnam e Conomy Sea 2023 ReportDokument14 SeitenVietnam e Conomy Sea 2023 ReportMitsu BùiNoch keine Bewertungen

- Vietnam e Conomy Sea 2023 Report Share by WorldLine TechnologyDokument14 SeitenVietnam e Conomy Sea 2023 Report Share by WorldLine Technologyvan.vn0912Noch keine Bewertungen

- Ernst - Young (E - Y)Dokument33 SeitenErnst - Young (E - Y)Tanya Luna MoránNoch keine Bewertungen

- Tinkoff Lifestyle Banking StrategyDokument46 SeitenTinkoff Lifestyle Banking StrategyLinh Phuong Nguyen PhamNoch keine Bewertungen

- In Consulting Strategy Bfs Consumerbehavior 062016 NoexpDokument12 SeitenIn Consulting Strategy Bfs Consumerbehavior 062016 NoexpPhương TrầnNoch keine Bewertungen

- Final Placement Report: Indian Institute of Management KashipurDokument7 SeitenFinal Placement Report: Indian Institute of Management KashipurKrutinath MadaliNoch keine Bewertungen

- AMERCO Investor Presentation 2020Dokument25 SeitenAMERCO Investor Presentation 2020Daniel KwanNoch keine Bewertungen

- Thailand e Conomy Sea 2023 ReportDokument14 SeitenThailand e Conomy Sea 2023 ReportMitsu BùiNoch keine Bewertungen

- Global Happiness 2020: What Makes People Happy in The Age of COVID-19Dokument49 SeitenGlobal Happiness 2020: What Makes People Happy in The Age of COVID-19Ramon CruzNoch keine Bewertungen

- Global Insurance Market Index q1 2020Dokument16 SeitenGlobal Insurance Market Index q1 2020Karol Hdez MtnezNoch keine Bewertungen

- Rewards Overhaul and Socio-Economic DataDokument11 SeitenRewards Overhaul and Socio-Economic DataFarhan MNoch keine Bewertungen

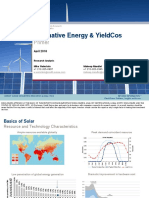

- CS Alternative Energy YieldCosDokument32 SeitenCS Alternative Energy YieldCosJonathan ChuahNoch keine Bewertungen

- A Practical Guide To Warranty & Indemnity Insurance: No. of Deals Placed FY15 - FY18Dokument8 SeitenA Practical Guide To Warranty & Indemnity Insurance: No. of Deals Placed FY15 - FY18Abel OliveiraNoch keine Bewertungen

- Foreign Investment Outlook 2023 - Navigating Headwinds Ahead - FinalDokument26 SeitenForeign Investment Outlook 2023 - Navigating Headwinds Ahead - FinalTruc LeNoch keine Bewertungen

- MMYT Investor Presentation - Q4 FinalDokument27 SeitenMMYT Investor Presentation - Q4 FinalvinitNoch keine Bewertungen

- Coffee Can PMS - Feb - 2021 PresentationDokument21 SeitenCoffee Can PMS - Feb - 2021 PresentationDeepak JoshiNoch keine Bewertungen

- The HotStats Hotel Confidence Monitor Q3 2010Dokument4 SeitenThe HotStats Hotel Confidence Monitor Q3 2010ehotelierNoch keine Bewertungen

- Hackett Key Issues Pro 1801Dokument10 SeitenHackett Key Issues Pro 1801Sandeep ChatterjeeNoch keine Bewertungen

- Salary Survey Report 2016Dokument10 SeitenSalary Survey Report 2016Pingviniko P PingvinikoNoch keine Bewertungen

- Individual Assignement Education D 4Dokument27 SeitenIndividual Assignement Education D 4VicNoch keine Bewertungen

- Clt3tab105cat562 20190128095558 PDFDokument43 SeitenClt3tab105cat562 20190128095558 PDFChinmay LearningNoch keine Bewertungen

- January 2008 - August 2009Dokument20 SeitenJanuary 2008 - August 2009Miki LitmanovitzNoch keine Bewertungen

- AMBITGOOD&CLEAN - Midcap PMS - Jan - 2022 - PresentationDokument24 SeitenAMBITGOOD&CLEAN - Midcap PMS - Jan - 2022 - Presentationbeza manojNoch keine Bewertungen

- InnoVen Capital Startup Outlook Report 2017Dokument16 SeitenInnoVen Capital Startup Outlook Report 2017NavinNoch keine Bewertungen

- IIM Shillong Final Placement Report 2021 22 - 12 04 2022 - UpdatedDokument7 SeitenIIM Shillong Final Placement Report 2021 22 - 12 04 2022 - UpdatedGaurav RawatNoch keine Bewertungen

- CCAFDokument8 SeitenCCAFsanket patilNoch keine Bewertungen

- Financial Wellbeing Index ReportDokument19 SeitenFinancial Wellbeing Index Reportcv10032Noch keine Bewertungen

- RKL Investor Presentation Jan 2020Dokument44 SeitenRKL Investor Presentation Jan 2020Jammigumpula PriyankaNoch keine Bewertungen

- WSO 2022 IB Working Conditions SurveyDokument42 SeitenWSO 2022 IB Working Conditions SurveyPhạm Hồng HuếNoch keine Bewertungen

- Thailand e Conomy Sea 2022 ReportDokument16 SeitenThailand e Conomy Sea 2022 ReportSiti Robiah HamdaniNoch keine Bewertungen

- Survey of The Food Processing Sector With Specific Reference To Bakery UnitsDokument13 SeitenSurvey of The Food Processing Sector With Specific Reference To Bakery UnitsAlpeshtomNoch keine Bewertungen

- Deutsche Bank Regional P&U Trading Update 2024.03.31Dokument15 SeitenDeutsche Bank Regional P&U Trading Update 2024.03.31kapil.mantriNoch keine Bewertungen

- Real World Project Management: Beyond Conventional Wisdom, Best Practices and Project MethodologiesVon EverandReal World Project Management: Beyond Conventional Wisdom, Best Practices and Project MethodologiesBewertung: 2 von 5 Sternen2/5 (1)

- Us Consumer Discretionary Equities PreferenceDokument52 SeitenUs Consumer Discretionary Equities PreferenceTung NgoNoch keine Bewertungen

- Chow Tai Fook Jewellery 120202Dokument24 SeitenChow Tai Fook Jewellery 120202Tung NgoNoch keine Bewertungen

- Csri Emerging Consumer Survey 2019Dokument68 SeitenCsri Emerging Consumer Survey 2019Valter SilveiraNoch keine Bewertungen

- CBBC Mother and Baby ReportDokument14 SeitenCBBC Mother and Baby ReportTung NgoNoch keine Bewertungen

- Whitepaper Responsible Consumption enDokument23 SeitenWhitepaper Responsible Consumption enTung NgoNoch keine Bewertungen

- Creating Value Beyond The DealDokument26 SeitenCreating Value Beyond The DealTung NgoNoch keine Bewertungen

- 2020-10-13-EDU.N-Thomson Reuters Stre-EDU.N - Event Transcript of New Oriental Education Technol... - 90015270Dokument14 Seiten2020-10-13-EDU.N-Thomson Reuters Stre-EDU.N - Event Transcript of New Oriental Education Technol... - 90015270Tung NgoNoch keine Bewertungen

- YTRA Sidoti InitiationDokument11 SeitenYTRA Sidoti InitiationTung NgoNoch keine Bewertungen

- Unilever NVDokument56 SeitenUnilever NVTung NgoNoch keine Bewertungen

- Riso Kyoiku Co., LTD.: Company Research and Analysis ReportDokument23 SeitenRiso Kyoiku Co., LTD.: Company Research and Analysis ReportTung NgoNoch keine Bewertungen

- 2019-04-25-9696.T-Jefferson Research-Jefferson Research Financial Sonar Report. A Detai... - 84988260Dokument11 Seiten2019-04-25-9696.T-Jefferson Research-Jefferson Research Financial Sonar Report. A Detai... - 84988260Tung NgoNoch keine Bewertungen

- POWER RANKING: The 10 Best Industries in 2020 For Entrepreneurs To Start Million-Dollar Businesses Despite The PandemicDokument6 SeitenPOWER RANKING: The 10 Best Industries in 2020 For Entrepreneurs To Start Million-Dollar Businesses Despite The PandemicTung NgoNoch keine Bewertungen

- UnileverDokument76 SeitenUnileverTung NgoNoch keine Bewertungen

- 2020-01-29-4714.T-FISCO Ltd.-Riso Kyoiku Co., Ltd. (4714) Healthy Expansion of Existing B... - 87343090Dokument27 Seiten2020-01-29-4714.T-FISCO Ltd.-Riso Kyoiku Co., Ltd. (4714) Healthy Expansion of Existing B... - 87343090Tung NgoNoch keine Bewertungen

- (Padini) Padini Holdings Berhad - 2013Dokument14 Seiten(Padini) Padini Holdings Berhad - 2013Tung NgoNoch keine Bewertungen

- 2021-07-07-Mirae Asset Securiti-2021 MID-YEAR OUTLOOK POST-PANDEMIC INVESTMENT STRATEGY-92953422Dokument58 Seiten2021-07-07-Mirae Asset Securiti-2021 MID-YEAR OUTLOOK POST-PANDEMIC INVESTMENT STRATEGY-92953422Tung NgoNoch keine Bewertungen

- 2020-08-13-REDU - OQ-Thomson Reuters Stre-REDU - OQ - Event Transcript of RISE Education Cayman LTD Conf... - 89488461Dokument8 Seiten2020-08-13-REDU - OQ-Thomson Reuters Stre-REDU - OQ - Event Transcript of RISE Education Cayman LTD Conf... - 89488461Tung NgoNoch keine Bewertungen

- DIOR VA Interactif-2 PDFDokument300 SeitenDIOR VA Interactif-2 PDFTung Ngo100% (1)

- DIOR VA Interactif-2 PDFDokument300 SeitenDIOR VA Interactif-2 PDFTung Ngo100% (1)

- LiFung FY19 AnnualResults PresentationDokument39 SeitenLiFung FY19 AnnualResults PresentationTung NgoNoch keine Bewertungen

- (Padini) Padini Holdings Berhad - 2013 - 1Dokument15 Seiten(Padini) Padini Holdings Berhad - 2013 - 1Tung NgoNoch keine Bewertungen

- (Padini) Padini Holdings Berhad - 2013Dokument14 Seiten(Padini) Padini Holdings Berhad - 2013Tung NgoNoch keine Bewertungen

- (Padini) Padini Holdings Berhad - 2013 - 1Dokument15 Seiten(Padini) Padini Holdings Berhad - 2013 - 1Tung NgoNoch keine Bewertungen

- 20.04.3408 Bab1Dokument13 Seiten20.04.3408 Bab1Tung NgoNoch keine Bewertungen

- BI PrimeDokument4 SeitenBI PrimeTung NgoNoch keine Bewertungen

- The Deal Process Exit Series 4Dokument14 SeitenThe Deal Process Exit Series 4Tung NgoNoch keine Bewertungen

- Insights Blue Skies PDFDokument18 SeitenInsights Blue Skies PDFTung NgoNoch keine Bewertungen

- SwiggyDokument5 SeitenSwiggyjhjk75% (4)

- Insights Blue Skies PDFDokument18 SeitenInsights Blue Skies PDFTung NgoNoch keine Bewertungen

- Past Simple Vs Past ContinuousDokument3 SeitenPast Simple Vs Past ContinuousNatalia SalinasNoch keine Bewertungen

- RSC Article Template-Mss - DaltonDokument15 SeitenRSC Article Template-Mss - DaltonIon BadeaNoch keine Bewertungen

- Aribah Ahmed CertificateDokument2 SeitenAribah Ahmed CertificateBahadur AliNoch keine Bewertungen

- The First Voyage Round The World by MageDokument405 SeitenThe First Voyage Round The World by MageGift Marieneth LopezNoch keine Bewertungen

- Description and Operating Instructions: Multicharger 750 12V/40A 24V/20A 36V/15ADokument34 SeitenDescription and Operating Instructions: Multicharger 750 12V/40A 24V/20A 36V/15APablo Barboza0% (1)

- Song LyricsDokument13 SeitenSong LyricsCyh RusNoch keine Bewertungen

- Gastroesophagea L of Reflux Disease (GERD)Dokument34 SeitenGastroesophagea L of Reflux Disease (GERD)Alyda Choirunnissa SudiratnaNoch keine Bewertungen

- Openvpn ReadmeDokument7 SeitenOpenvpn Readmefzfzfz2014Noch keine Bewertungen

- Bench-Scale Decomposition of Aluminum Chloride Hexahydrate To Produce Poly (Aluminum Chloride)Dokument5 SeitenBench-Scale Decomposition of Aluminum Chloride Hexahydrate To Produce Poly (Aluminum Chloride)varadjoshi41Noch keine Bewertungen

- Paul Spicker - The Welfare State A General TheoryDokument162 SeitenPaul Spicker - The Welfare State A General TheoryTista ArumNoch keine Bewertungen

- 1.161000 702010 New Perspectives 2ndedDokument43 Seiten1.161000 702010 New Perspectives 2ndedbimobimoprabowoNoch keine Bewertungen

- EP001 LifeCoachSchoolTranscriptDokument13 SeitenEP001 LifeCoachSchoolTranscriptVan GuedesNoch keine Bewertungen

- SOCIAL MEDIA DEBATE ScriptDokument3 SeitenSOCIAL MEDIA DEBATE Scriptchristine baraNoch keine Bewertungen

- SecurityFund PPT 1.1Dokument13 SeitenSecurityFund PPT 1.1Fmunoz MunozNoch keine Bewertungen

- Truss-Design 18mDokument6 SeitenTruss-Design 18mARSENoch keine Bewertungen

- Reflection in Sexually Transmitted DiseaseDokument1 SeiteReflection in Sexually Transmitted Diseasewenna janeNoch keine Bewertungen

- The Reason: B. FlowsDokument4 SeitenThe Reason: B. FlowsAryanti UrsullahNoch keine Bewertungen

- William Hallett - BiographyDokument2 SeitenWilliam Hallett - Biographyapi-215611511Noch keine Bewertungen

- Microfinance Ass 1Dokument15 SeitenMicrofinance Ass 1Willard MusengeyiNoch keine Bewertungen

- DN102-R0-GPJ-Design of Substructure & Foundation 28m+28m Span, 19.6m Width, 22m Height PDFDokument64 SeitenDN102-R0-GPJ-Design of Substructure & Foundation 28m+28m Span, 19.6m Width, 22m Height PDFravichandraNoch keine Bewertungen

- Benefits and Limitations of BEPDokument2 SeitenBenefits and Limitations of BEPAnishaAppuNoch keine Bewertungen

- Test Bank For The Psychology of Health and Health Care A Canadian Perspective 5th EditionDokument36 SeitenTest Bank For The Psychology of Health and Health Care A Canadian Perspective 5th Editionload.notablewp0oz100% (37)

- Sainik School Balachadi: Name-Class - Roll No - Subject - House - Assigned byDokument10 SeitenSainik School Balachadi: Name-Class - Roll No - Subject - House - Assigned byPagalNoch keine Bewertungen

- Hw10 SolutionsDokument4 SeitenHw10 Solutionsbernandaz123Noch keine Bewertungen

- Principles of Supply Chain Management A Balanced Approach 4th Edition Wisner Solutions ManualDokument36 SeitenPrinciples of Supply Chain Management A Balanced Approach 4th Edition Wisner Solutions Manualoutlying.pedantry.85yc100% (28)

- Dessler HRM12e PPT 01Dokument30 SeitenDessler HRM12e PPT 01harryjohnlyallNoch keine Bewertungen

- Barrett Beyond Psychometrics 2003 AugmentedDokument34 SeitenBarrett Beyond Psychometrics 2003 AugmentedRoy Umaña CarrilloNoch keine Bewertungen

- What You Need To Know About Your Drive TestDokument12 SeitenWhat You Need To Know About Your Drive TestMorley MuseNoch keine Bewertungen

- Outline Calculus3Dokument20 SeitenOutline Calculus3Joel CurtisNoch keine Bewertungen

- Accounting Students' Perceptions On Employment OpportunitiesDokument7 SeitenAccounting Students' Perceptions On Employment OpportunitiesAquila Kate ReyesNoch keine Bewertungen