Das könnte Ihnen auch gefallen

- MaglalangDokument4 SeitenMaglalangmonchievalera100% (1)

- National Exchange Co Vs DexterDokument2 SeitenNational Exchange Co Vs DexterQueenie SabladaNoch keine Bewertungen

- 24 Manalo vs. Sistoza PDFDokument14 Seiten24 Manalo vs. Sistoza PDFshlm bNoch keine Bewertungen

- Ocampo v. OcampoDokument4 SeitenOcampo v. OcampoJoseph Paolo SantosNoch keine Bewertungen

- Spouses Alejandro Mirasol and Lilia E. Mirasol, Petitioners, vs. The Court of Appeals, Philippine National Bank, and Philippine Exchange Co. Inc.Dokument1 SeiteSpouses Alejandro Mirasol and Lilia E. Mirasol, Petitioners, vs. The Court of Appeals, Philippine National Bank, and Philippine Exchange Co. Inc.HaelSerNoch keine Bewertungen

- Benjamin C. Santos and Estrella, Remitio & Associates For Petitioner. Rodolfo V. Gumban For Private RespondentDokument5 SeitenBenjamin C. Santos and Estrella, Remitio & Associates For Petitioner. Rodolfo V. Gumban For Private RespondentLouisa FerrarenNoch keine Bewertungen

- G.G. Sportswear Manufacturing Corp. vs. Banco de Oro Unibank, Inc.Dokument2 SeitenG.G. Sportswear Manufacturing Corp. vs. Banco de Oro Unibank, Inc.kdescallarNoch keine Bewertungen

- Defective Contracts Guide PDFDokument5 SeitenDefective Contracts Guide PDFJade Belen ZaragozaNoch keine Bewertungen

- Time, Inc. v. ReyesDokument10 SeitenTime, Inc. v. ReyesShairaCamilleGarciaNoch keine Bewertungen

- National Exchange Vs DexterDokument6 SeitenNational Exchange Vs DexterDexter CircaNoch keine Bewertungen

- Lopez Realty Inc V Sps Tanjangco (2014)Dokument3 SeitenLopez Realty Inc V Sps Tanjangco (2014)AnnKhoLugasanNoch keine Bewertungen

- Virgilio S. Delima v. Susan Mercaida GoisDokument3 SeitenVirgilio S. Delima v. Susan Mercaida GoisbearzhugNoch keine Bewertungen

- 31) Tupaz IV v. CA and BPIDokument2 Seiten31) Tupaz IV v. CA and BPIRain HofileñaNoch keine Bewertungen

- Co vs. CA GR# 100776 (10.28.1993)Dokument6 SeitenCo vs. CA GR# 100776 (10.28.1993)Ken AliudinNoch keine Bewertungen

- Ignacio v. Pampanga Bus Co., Inc.Dokument11 SeitenIgnacio v. Pampanga Bus Co., Inc.Laura MangantulaoNoch keine Bewertungen

- TOSHIBA vs. CIRDokument3 SeitenTOSHIBA vs. CIRDeus DulayNoch keine Bewertungen

- Mercantile Bar Exam Questions 2012Dokument31 SeitenMercantile Bar Exam Questions 2012vylletteNoch keine Bewertungen

- ROHM Apollo Semiconductor v. CirDokument3 SeitenROHM Apollo Semiconductor v. Cirdll123Noch keine Bewertungen

- Philippine Long Distance Telephone Company vs. Citi Appliance M.C. Corporation, 922 SCRA 518, October 09, 2019Dokument41 SeitenPhilippine Long Distance Telephone Company vs. Citi Appliance M.C. Corporation, 922 SCRA 518, October 09, 2019Jane BandojaNoch keine Bewertungen

- Legal FormsDokument5 SeitenLegal FormsDolph LubrinNoch keine Bewertungen

- Arroyo Vs AzurDokument8 SeitenArroyo Vs AzurJela SyNoch keine Bewertungen

- Gonzalo v. TarnateDokument5 SeitenGonzalo v. TarnateFrances Ann TevesNoch keine Bewertungen

- Admin Digests Feb 25 (1 6)Dokument27 SeitenAdmin Digests Feb 25 (1 6)Cherlene TanNoch keine Bewertungen

- Vivas Vs Monetary BoardDokument9 SeitenVivas Vs Monetary BoardSur ReyNoch keine Bewertungen

- BPI FAMILY SAVINGS BANK v. St. MichaelDokument2 SeitenBPI FAMILY SAVINGS BANK v. St. MichaelNicki Vine CapuchinoNoch keine Bewertungen

- Kapisan NG Mga Manggagawa Vs Manila Railroad CompanyDokument3 SeitenKapisan NG Mga Manggagawa Vs Manila Railroad CompanywerliefeNoch keine Bewertungen

- Duty Free Philippines vs. Mojica FactsDokument2 SeitenDuty Free Philippines vs. Mojica FactsLito Paolo Martin IINoch keine Bewertungen

- Co v. Philippine National BankDokument3 SeitenCo v. Philippine National BankyodachanNoch keine Bewertungen

- Fil-Estate Properties Inc and Fil-Estate Network Inc Vs Spouses Conrado and Maria Victoria RonquilloDokument6 SeitenFil-Estate Properties Inc and Fil-Estate Network Inc Vs Spouses Conrado and Maria Victoria Ronquillomondaytuesday17Noch keine Bewertungen

- Subpoena NDCDokument3 SeitenSubpoena NDCOCP Santiago CityNoch keine Bewertungen

- Lorenzo - Shipping - Corp. - v. - VillarinDokument15 SeitenLorenzo - Shipping - Corp. - v. - VillarinHazel FernandezNoch keine Bewertungen

- Cojuanco Vs SandiganbayanDokument20 SeitenCojuanco Vs SandiganbayansirynspixeNoch keine Bewertungen

- 65 DBP V COADokument4 Seiten65 DBP V COArgtan3Noch keine Bewertungen

- Palay Inc. Vs ClaveDokument5 SeitenPalay Inc. Vs ClaveJA BedrioNoch keine Bewertungen

- Diong Bi Chu V Ca PDFDokument3 SeitenDiong Bi Chu V Ca PDFTrishalyVienBaslotNoch keine Bewertungen

- 1-Samahan NG Mangagawa NG Hanjin Vs BLRDokument16 Seiten1-Samahan NG Mangagawa NG Hanjin Vs BLRJoan Dela CruzNoch keine Bewertungen

- Sy Santos, Del Rosario and Associates For Petitioners-Appellants. Tagalo, Gozar and Associates For Respondents-AppelleesDokument2 SeitenSy Santos, Del Rosario and Associates For Petitioners-Appellants. Tagalo, Gozar and Associates For Respondents-AppelleesfrancisNoch keine Bewertungen

- CIR Vs PALDokument3 SeitenCIR Vs PALGab EstiadaNoch keine Bewertungen

- PCIB V GomezDokument7 SeitenPCIB V GomezFrances Angelica Domini KoNoch keine Bewertungen

- Central Sawmill vs. Alto InsuranceDokument3 SeitenCentral Sawmill vs. Alto InsuranceDara Compuesto0% (1)

- IN RE MUNESES, BM No 2112, July 24, 2012Dokument1 SeiteIN RE MUNESES, BM No 2112, July 24, 2012Markus Tran MoraldeNoch keine Bewertungen

- 226 Rural Bank of Lipa v. CADokument4 Seiten226 Rural Bank of Lipa v. CAmiyumiNoch keine Bewertungen

- Industry Highlights: Agriculture Industry in Prince Edward IslandDokument6 SeitenIndustry Highlights: Agriculture Industry in Prince Edward Islandn3xtnetworkNoch keine Bewertungen

- Catipon Vs JapsonDokument19 SeitenCatipon Vs JapsonMark John Geronimo BautistaNoch keine Bewertungen

- Magcamit vs. PDEADokument8 SeitenMagcamit vs. PDEAXryn MortelNoch keine Bewertungen

- In Re: Benjamin Dacanay (FULL TEXT)Dokument2 SeitenIn Re: Benjamin Dacanay (FULL TEXT)Anonymous Mickey MouseNoch keine Bewertungen

- Freedom of ExpressionDokument31 SeitenFreedom of ExpressionRomnick Jesalva100% (1)

- ALPHA INSURANCE AND SURETY CO., Petitioner, vs. ARSENIA SONIA CASTOR, RespondentDokument9 SeitenALPHA INSURANCE AND SURETY CO., Petitioner, vs. ARSENIA SONIA CASTOR, RespondentClaudine Mae G. TeodoroNoch keine Bewertungen

- Republic Act No. 11976 (EOPT) - Infographics - SGVDokument3 SeitenRepublic Act No. 11976 (EOPT) - Infographics - SGVAlbert SantiagoNoch keine Bewertungen

- San Luis vs. CADokument4 SeitenSan Luis vs. CADowie M. MatienzoNoch keine Bewertungen

- 104 Municipality of Makati v. CADokument1 Seite104 Municipality of Makati v. CAAMIDA ISMAEL. SALISANoch keine Bewertungen

- TAX Remedies (Jurisdiction of Courts, Prescription, Remedies Against Assessment Notice)Dokument11 SeitenTAX Remedies (Jurisdiction of Courts, Prescription, Remedies Against Assessment Notice)KAREENA AMEENAH ACRAMAN BASMANNoch keine Bewertungen

- In Re: Undated Letter of Louis BiraogoDokument10 SeitenIn Re: Undated Letter of Louis BiraogoJoVic2020Noch keine Bewertungen

- Table of Contents and Front PageDokument2 SeitenTable of Contents and Front PageBarry Rayven CutaranNoch keine Bewertungen

- Balleta, Malvin A. - SPECPRO SYLLABUSDokument36 SeitenBalleta, Malvin A. - SPECPRO SYLLABUSMalvin Aragon BalletaNoch keine Bewertungen

- 1-10 Tax Sept 9Dokument11 Seiten1-10 Tax Sept 9Niña ArmadaNoch keine Bewertungen

- Summary of Significant CTA Decisions (February 2011)Dokument2 SeitenSummary of Significant CTA Decisions (February 2011)ShaneBeriñaImperialNoch keine Bewertungen

- Doctrine in Taxation Consolidated CasesDokument29 SeitenDoctrine in Taxation Consolidated CasesStela PantaleonNoch keine Bewertungen

- CIR Vs CTA DigestDokument2 SeitenCIR Vs CTA DigestAbilene Joy Dela Cruz83% (6)

- Case Digest TaxDokument13 SeitenCase Digest TaxNonelyn GalanoNoch keine Bewertungen

- 2023 06 ToR Mexico Options To Decarbonize Large Industry - EoIDokument6 Seiten2023 06 ToR Mexico Options To Decarbonize Large Industry - EoIDean CainilaNoch keine Bewertungen

- Freedom of Expression/ Right To Peaceably Assemble: 2020 Constitutional Law 2 (Lecture 3)Dokument66 SeitenFreedom of Expression/ Right To Peaceably Assemble: 2020 Constitutional Law 2 (Lecture 3)Dean CainilaNoch keine Bewertungen

- Working Efficiently - 1Dokument1 SeiteWorking Efficiently - 1Dean CainilaNoch keine Bewertungen

- Social Legislation - Case DigestsDokument27 SeitenSocial Legislation - Case Digestskrys_elleNoch keine Bewertungen

- UST Dean - S Circle DigestsDokument182 SeitenUST Dean - S Circle DigestsTed Castello100% (3)

- (Lecture 1) : 2020 Constitutional Law 2Dokument18 Seiten(Lecture 1) : 2020 Constitutional Law 2Dean CainilaNoch keine Bewertungen

- Arrests/ Searches AND Seizures: (Lecture 2)Dokument15 SeitenArrests/ Searches AND Seizures: (Lecture 2)Dean Cainila100% (1)

- Religion: By: Atty. Enrique V. Dela Cruz, JRDokument62 SeitenReligion: By: Atty. Enrique V. Dela Cruz, JRDean Cainila100% (1)

- StateImmunity C18 EspinoDokument3 SeitenStateImmunity C18 EspinoDean CainilaNoch keine Bewertungen

- NCCADokument2 SeitenNCCADean CainilaNoch keine Bewertungen

- Chapter 4-Philippine Mining ACT OF 1995: AGUILAR, Krystalynne F. 2018890203Dokument75 SeitenChapter 4-Philippine Mining ACT OF 1995: AGUILAR, Krystalynne F. 2018890203Krystalynne AguilarNoch keine Bewertungen

- StateImmunity C19 YangaDokument1 SeiteStateImmunity C19 YangaDean CainilaNoch keine Bewertungen

- StateImmunity C14 BisaresDokument5 SeitenStateImmunity C14 BisaresDean CainilaNoch keine Bewertungen

- StateImmunity C11 JambalosDokument3 SeitenStateImmunity C11 JambalosDean CainilaNoch keine Bewertungen

- StateImmunity C13 CalderonDokument2 SeitenStateImmunity C13 CalderonDean CainilaNoch keine Bewertungen

- StateImmunity C13 CalderonDokument2 SeitenStateImmunity C13 CalderonDean CainilaNoch keine Bewertungen

- StateImmunity C8 EspinoDokument2 SeitenStateImmunity C8 EspinoDean CainilaNoch keine Bewertungen

- StateImmunity - C15 - Yanga Cosculluela Vs CADokument2 SeitenStateImmunity - C15 - Yanga Cosculluela Vs CADean Cainila0% (1)

- StateImmunity C10 BasalioDokument3 SeitenStateImmunity C10 BasalioDean CainilaNoch keine Bewertungen

- StatePrinciples F12 CainilaDokument9 SeitenStatePrinciples F12 CainilaDean CainilaNoch keine Bewertungen

- StatePrinciples F12 (RECOMMENDED)Dokument5 SeitenStatePrinciples F12 (RECOMMENDED)Dean CainilaNoch keine Bewertungen

- H18 Aguinaldo V AquinoDokument5 SeitenH18 Aguinaldo V AquinoDean CainilaNoch keine Bewertungen

- DO 01202020egwegDokument4 SeitenDO 01202020egwegDean CainilaNoch keine Bewertungen

- DSWDDokument2 SeitenDSWDDean CainilaNoch keine Bewertungen

- Income-Tax Law: A Capsule For Quick Recap: Chapter 9: Advance Tax and Tax Deduction at SourceDokument5 SeitenIncome-Tax Law: A Capsule For Quick Recap: Chapter 9: Advance Tax and Tax Deduction at Sourcem310235Noch keine Bewertungen

- E-Filing of Taxes - A Research PaperDokument8 SeitenE-Filing of Taxes - A Research PaperRieke Savitri Agustin0% (1)

- MM2023 (Session 1)Dokument6 SeitenMM2023 (Session 1)richaNoch keine Bewertungen

- GA Taxes Delinquent-BusinessesDokument940 SeitenGA Taxes Delinquent-BusinessesMcMillan ConsultingNoch keine Bewertungen

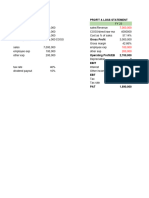

- Multi-Step Income Statement: Key Terms and Concepts To KnowDokument5 SeitenMulti-Step Income Statement: Key Terms and Concepts To KnowĐức NguyễnNoch keine Bewertungen

- Liabilities RS. Assets RS.: A. Balance Sheet of The Sarvodaya Sahakari Bank Ltd. For The Year Ended On 31 MARCH, 2006Dokument3 SeitenLiabilities RS. Assets RS.: A. Balance Sheet of The Sarvodaya Sahakari Bank Ltd. For The Year Ended On 31 MARCH, 2006bhaveshpipaliyaNoch keine Bewertungen

- Multiple Choice Questions 1 Which of The Following Increase S A Taxpayer SDokument2 SeitenMultiple Choice Questions 1 Which of The Following Increase S A Taxpayer STaimour HassanNoch keine Bewertungen

- BIR Ruling DA 509-06Dokument12 SeitenBIR Ruling DA 509-06Harry Bill Dela FuenteNoch keine Bewertungen

- Assessment of Various EntitiesDokument31 SeitenAssessment of Various Entitiesinsathi0% (1)

- Acctg Lab 7Dokument8 SeitenAcctg Lab 7AngieNoch keine Bewertungen

- OD125549891478426000Dokument1 SeiteOD125549891478426000अमित कुमारNoch keine Bewertungen

- Thesis Jan 20Dokument18 SeitenThesis Jan 20Kristy Dela CernaNoch keine Bewertungen

- Group Assigment CONCH PART1Dokument4 SeitenGroup Assigment CONCH PART1BashirNoch keine Bewertungen

- Ias 12Dokument32 SeitenIas 12Cat ValentineNoch keine Bewertungen

- LPC Saima SadiqDokument2 SeitenLPC Saima Sadiqlatestever28Noch keine Bewertungen

- Shut-Down or ContinueDokument8 SeitenShut-Down or ContinueSanjay Smart100% (1)

- Problem 3-1Dokument2 SeitenProblem 3-1Omar CirunayNoch keine Bewertungen

- 1274 PDFDokument1 Seite1274 PDFAbhilashKrishnanNoch keine Bewertungen

- GST Registration PDFDokument3 SeitenGST Registration PDFRanjit MankuNoch keine Bewertungen

- Commissioner of Internal Revenue vs. Goodyear Philippines, Inc. - GR No. 216130 - Aug. 3, 2016Dokument10 SeitenCommissioner of Internal Revenue vs. Goodyear Philippines, Inc. - GR No. 216130 - Aug. 3, 2016Kristel Anne LiwagNoch keine Bewertungen

- Liquidation Report Template - 001Dokument12 SeitenLiquidation Report Template - 001Des GallegoNoch keine Bewertungen

- SS Flat RateDokument1 SeiteSS Flat RaterohitNoch keine Bewertungen

- Profession Tax Challan - MaharashtraDokument1 SeiteProfession Tax Challan - MaharashtraPaymaster Services80% (5)

- Additional Consolidation Reporting Issues: Mcgraw-Hill/IrwinDokument40 SeitenAdditional Consolidation Reporting Issues: Mcgraw-Hill/IrwinRizki ApriyansyahNoch keine Bewertungen

- Level IV Code 1 Project OneDokument5 SeitenLevel IV Code 1 Project OneAye Tube100% (2)

- Probate Inheritance Tax Form (IHT400 Notes)Dokument88 SeitenProbate Inheritance Tax Form (IHT400 Notes)internichtNoch keine Bewertungen

- Fall 2023 - Tax ProjectDokument4 SeitenFall 2023 - Tax Projectacwriters123Noch keine Bewertungen

- Accomplishment Report: Submitted By: Certified and Approved byDokument2 SeitenAccomplishment Report: Submitted By: Certified and Approved byMarc MendozaNoch keine Bewertungen

- Italian Purchase VAT RegisterDokument9 SeitenItalian Purchase VAT RegisterArcotsinghNoch keine Bewertungen

- Task 1Dokument3 SeitenTask 1Simran GanganeNoch keine Bewertungen