Das könnte Ihnen auch gefallen

- RBI Dec Monetary PolicyDokument3 SeitenRBI Dec Monetary PolicyKalpesh AgrawalNoch keine Bewertungen

- RBI Mid QTR Policy Review 16122010Dokument3 SeitenRBI Mid QTR Policy Review 16122010tamirisaarNoch keine Bewertungen

- RBI's Monetary Policy Objectives and ToolsDokument6 SeitenRBI's Monetary Policy Objectives and ToolspundirsandeepNoch keine Bewertungen

- Monetary Policy-RBI-Second Quarter Review of Nov.10-VRK100-03112010Dokument5 SeitenMonetary Policy-RBI-Second Quarter Review of Nov.10-VRK100-03112010RamaKrishna Vadlamudi, CFANoch keine Bewertungen

- Market Insight Q3FY12 RBI Policy Review Jan12Dokument3 SeitenMarket Insight Q3FY12 RBI Policy Review Jan12poojarajeswariNoch keine Bewertungen

- Presentation ON An Overview of Monetary PolicyDokument22 SeitenPresentation ON An Overview of Monetary PolicybhoopendratNoch keine Bewertungen

- Rbi Credit PolicyDokument8 SeitenRbi Credit PolicyamishkanungoNoch keine Bewertungen

- KBSL - Credit Policy AnalysisDokument4 SeitenKBSL - Credit Policy AnalysisRahulNoch keine Bewertungen

- Key Highlights:: Inflationary Pressures Overrides Downside Risks To GrowthDokument6 SeitenKey Highlights:: Inflationary Pressures Overrides Downside Risks To Growthsamyak_jain_8Noch keine Bewertungen

- Management Discussion and Analysis 2015Dokument37 SeitenManagement Discussion and Analysis 2015Rohit SharmaNoch keine Bewertungen

- F F y Y: Ear Uls MmetrDokument5 SeitenF F y Y: Ear Uls MmetrBelinda WinkelmanNoch keine Bewertungen

- MONETARY & FISCAL POLICY INSIGHTSDokument29 SeitenMONETARY & FISCAL POLICY INSIGHTSKenny AdamsNoch keine Bewertungen

- Impact of Monetary Policy on Indian IndustryDokument13 SeitenImpact of Monetary Policy on Indian IndustryVikalp Saxena50% (2)

- RBI Credit Policy Analysis November 2010Dokument8 SeitenRBI Credit Policy Analysis November 2010gaurav880Noch keine Bewertungen

- RBI monetary policy effectiveness containing inflationDokument31 SeitenRBI monetary policy effectiveness containing inflationArpit PangasaNoch keine Bewertungen

- Macro Economic Impact Apr08Dokument16 SeitenMacro Economic Impact Apr08shekhar somaNoch keine Bewertungen

- (Kotak) ICICI Bank, January 31, 2013Dokument14 Seiten(Kotak) ICICI Bank, January 31, 2013Chaitanya JagarlapudiNoch keine Bewertungen

- RBI Monetary Policy ReviewDokument5 SeitenRBI Monetary Policy ReviewAngel BrokingNoch keine Bewertungen

- RBI Hikes Repo Rate For First Time in Four Years by Kapil KathpalDokument31 SeitenRBI Hikes Repo Rate For First Time in Four Years by Kapil Kathpal32divyanshuNoch keine Bewertungen

- FY 10 Monetary ReviewDokument4 SeitenFY 10 Monetary ReviewVivek SarinNoch keine Bewertungen

- RBI Rate Hike to Curb InflationDokument4 SeitenRBI Rate Hike to Curb InflationPranshu_Priyad_8742Noch keine Bewertungen

- C O M P A N Y P R O F I L E: Achal Gupta Managing Director & Chief Executive OfficerDokument61 SeitenC O M P A N Y P R O F I L E: Achal Gupta Managing Director & Chief Executive OfficervipinkathpalNoch keine Bewertungen

- RBI Credit Policy Trends 2001-2012Dokument4 SeitenRBI Credit Policy Trends 2001-2012Sandeep SheshamNoch keine Bewertungen

- 14.08.2023 - Morning Financial News UpdatesDokument5 Seiten14.08.2023 - Morning Financial News UpdatesPratik ChavanNoch keine Bewertungen

- RBI Policy Review Oct 2011 Highlights and RecommendationDokument7 SeitenRBI Policy Review Oct 2011 Highlights and RecommendationKirthan Ψ PurechaNoch keine Bewertungen

- Pest Analysis of Indian Banking Industry:: Files Without This Message by Purchasing Novapdf PrinterDokument12 SeitenPest Analysis of Indian Banking Industry:: Files Without This Message by Purchasing Novapdf PrinterBhasvanth SrivastavNoch keine Bewertungen

- RBI Rate Cut ExpectationsDokument4 SeitenRBI Rate Cut ExpectationsDeepak SharmaNoch keine Bewertungen

- Assignment of Buisness Enviroment MGT 511: TOPIC: Changes in Monetary Policy On Banking Sector or IndustryDokument9 SeitenAssignment of Buisness Enviroment MGT 511: TOPIC: Changes in Monetary Policy On Banking Sector or IndustryRohit VermaNoch keine Bewertungen

- Monthly Test - February 2020Dokument7 SeitenMonthly Test - February 2020Keigan ChatterjeeNoch keine Bewertungen

- Fearful Symmetry Nov 2011Dokument4 SeitenFearful Symmetry Nov 2011ChrisBeckerNoch keine Bewertungen

- RBI monetary policy leaves debt market with safe opportunitiesDokument1 SeiteRBI monetary policy leaves debt market with safe opportunitiesChandan PreetNoch keine Bewertungen

- RBI Raised Interest Rates How This Impacts You!Dokument5 SeitenRBI Raised Interest Rates How This Impacts You!Aishwarya ShettyNoch keine Bewertungen

- SBP - Analyst Briefing NoteDokument3 SeitenSBP - Analyst Briefing Notemuddasir1980Noch keine Bewertungen

- RBI Springs Surprise, Cuts Repo by 50 Bps by Dinesh Unnikrishnan & Anup RoyDokument5 SeitenRBI Springs Surprise, Cuts Repo by 50 Bps by Dinesh Unnikrishnan & Anup RoymahaktripuriNoch keine Bewertungen

- Mrunal - Economic Survey IndiaDokument156 SeitenMrunal - Economic Survey IndiaakashsinglaNoch keine Bewertungen

- Article 3.0Dokument9 SeitenArticle 3.0Vinish ChandraNoch keine Bewertungen

- RBI cuts repo rate by 50 bps to 7.5% amid recession cloudsDokument4 SeitenRBI cuts repo rate by 50 bps to 7.5% amid recession cloudsnikhil6710349Noch keine Bewertungen

- RBI Policy Review Projects 7.7-8% GDP Growth, 6% Inflation by March 2012Dokument13 SeitenRBI Policy Review Projects 7.7-8% GDP Growth, 6% Inflation by March 2012Siddharth VaidNoch keine Bewertungen

- Icici Prudential Mutual Fund Rbi Second Quarter Review of Monetary Policy 2010-11Dokument4 SeitenIcici Prudential Mutual Fund Rbi Second Quarter Review of Monetary Policy 2010-11Vinit KumarNoch keine Bewertungen

- RBI's Third Quarter Review-Shift in Monetary Policy 2009-10 Stance-VRK100-29012010Dokument7 SeitenRBI's Third Quarter Review-Shift in Monetary Policy 2009-10 Stance-VRK100-29012010RamaKrishna Vadlamudi, CFANoch keine Bewertungen

- Financials Result ReviewDokument21 SeitenFinancials Result ReviewAngel BrokingNoch keine Bewertungen

- Market Outlook 16th March 2012Dokument4 SeitenMarket Outlook 16th March 2012Angel BrokingNoch keine Bewertungen

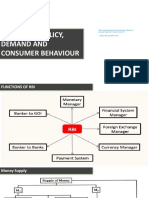

- Monetary Policy, Demand and Consumer Behaviour: Alculator/repo-Rate-Vs-Bank-Rate - HTML - Repo Rate and Bank RatreDokument23 SeitenMonetary Policy, Demand and Consumer Behaviour: Alculator/repo-Rate-Vs-Bank-Rate - HTML - Repo Rate and Bank RatreBhavya NarangNoch keine Bewertungen

- Slide - 1: 2009. Between March 2010 and October 2011 The Reserve Bank Raised Its Policy RepoDokument3 SeitenSlide - 1: 2009. Between March 2010 and October 2011 The Reserve Bank Raised Its Policy RepoGarrima ParakhNoch keine Bewertungen

- JUL 27 DBS Daily Breakfast SpreadDokument7 SeitenJUL 27 DBS Daily Breakfast SpreadMiir ViirNoch keine Bewertungen

- LG Zi 39285932Dokument28 SeitenLG Zi 39285932erlanggaherpNoch keine Bewertungen

- Monetary Policy, Inflation and Liquidity Crisis: Bangladesh Economic UpdateDokument17 SeitenMonetary Policy, Inflation and Liquidity Crisis: Bangladesh Economic UpdateMuhammad Hasan ParvajNoch keine Bewertungen

- Monetary Policy of PakistanDokument8 SeitenMonetary Policy of PakistanWajeeha HasnainNoch keine Bewertungen

- Market Outlook 5th October 2011Dokument4 SeitenMarket Outlook 5th October 2011Angel BrokingNoch keine Bewertungen

- Reserve Bank of India and Its Impact On The Indian Economy Post 1991 (Interest Rates, Exchange Rates and Inflation)Dokument7 SeitenReserve Bank of India and Its Impact On The Indian Economy Post 1991 (Interest Rates, Exchange Rates and Inflation)Mrunal DubeyNoch keine Bewertungen

- Tathya Ashish Isb HyderabadDokument4 SeitenTathya Ashish Isb HyderabadAshish KumarNoch keine Bewertungen

- Steps Taken By RBI To Control InflationDokument7 SeitenSteps Taken By RBI To Control Inflationliyakat_khanNoch keine Bewertungen

- Latest Policy RatesDokument3 SeitenLatest Policy RatesAbhishek BidhanNoch keine Bewertungen

- Indian Election EconomyDokument1 SeiteIndian Election Economypathanfor786Noch keine Bewertungen

- Assignment 3Dokument5 SeitenAssignment 3SuprityNoch keine Bewertungen

- Press Release: Communications DepartmentDokument3 SeitenPress Release: Communications DepartmentRandora LkNoch keine Bewertungen

- Business Ethics Concepts & Cases: Manuel G. VelasquezDokument19 SeitenBusiness Ethics Concepts & Cases: Manuel G. VelasquezRaffi MouradianNoch keine Bewertungen

- SIM7020 Series - HTTP (S) - Application Note - V1.04Dokument15 SeitenSIM7020 Series - HTTP (S) - Application Note - V1.04Vinicius BarozziNoch keine Bewertungen

- Short Answers Class 9thDokument14 SeitenShort Answers Class 9thRizwan AliNoch keine Bewertungen

- Lazo v. Judge TiongDokument9 SeitenLazo v. Judge TiongKing BadongNoch keine Bewertungen

- Department of Education Doña Asuncion Lee Integrated School: Division of Mabalacat CityDokument2 SeitenDepartment of Education Doña Asuncion Lee Integrated School: Division of Mabalacat CityRica Tano50% (2)

- Surface water drainage infiltration testingDokument8 SeitenSurface water drainage infiltration testingRay CooperNoch keine Bewertungen

- Current Developments in Testing Item Response Theory (IRT) : Prepared byDokument32 SeitenCurrent Developments in Testing Item Response Theory (IRT) : Prepared byMalar VengadesNoch keine Bewertungen

- Recent Developments in Ultrasonic NDT Modelling in CIVADokument7 SeitenRecent Developments in Ultrasonic NDT Modelling in CIVAcal2_uniNoch keine Bewertungen

- 6470b0e5f337ed00180c05a4 - ## - Atomic Structure - DPP-01 (Of Lec-03) - Arjuna NEET 2024Dokument3 Seiten6470b0e5f337ed00180c05a4 - ## - Atomic Structure - DPP-01 (Of Lec-03) - Arjuna NEET 2024Lalit SinghNoch keine Bewertungen

- Self Healing Challenge - March 2023 Workshop ThreeDokument16 SeitenSelf Healing Challenge - March 2023 Workshop ThreeDeena DSNoch keine Bewertungen

- BBRC4103 - Research MethodologyDokument14 SeitenBBRC4103 - Research MethodologySimon RajNoch keine Bewertungen

- Explanation of Four Ahadeeth From Imaam Al-Bukhaaree's Al-Adab-Ul-MufradDokument4 SeitenExplanation of Four Ahadeeth From Imaam Al-Bukhaaree's Al-Adab-Ul-MufradMountainofknowledgeNoch keine Bewertungen

- History of Veterinary MedicineDokument25 SeitenHistory of Veterinary MedicineAli AsadullahNoch keine Bewertungen

- The Diary of Anne Frank PacketDokument24 SeitenThe Diary of Anne Frank Packetcnakazaki1957Noch keine Bewertungen

- ComputerDokument26 SeitenComputer29.Kritika SinghNoch keine Bewertungen

- EDIBLE VACCINES: A COST-EFFECTIVE SOLUTIONDokument21 SeitenEDIBLE VACCINES: A COST-EFFECTIVE SOLUTIONPritish SareenNoch keine Bewertungen

- GSMA Moile Money Philippines Case Study V X21 21Dokument23 SeitenGSMA Moile Money Philippines Case Study V X21 21davidcloud99Noch keine Bewertungen

- D2DDokument2 SeitenD2Dgurjit20Noch keine Bewertungen

- Philip Larkin: The Art of Poetry 30Dokument32 SeitenPhilip Larkin: The Art of Poetry 30Telmo RodriguesNoch keine Bewertungen

- J-Garlic in CheeseDokument12 SeitenJ-Garlic in CheeseMary GinetaNoch keine Bewertungen

- C++ NotesDokument129 SeitenC++ NotesNikhil Kant Saxena100% (4)

- Introduction MCC Oxo ProcessDokument5 SeitenIntroduction MCC Oxo ProcessDeep PatelNoch keine Bewertungen

- Math-149 MatricesDokument26 SeitenMath-149 MatricesKurl Vincent GamboaNoch keine Bewertungen

- Financial Services : An OverviewDokument15 SeitenFinancial Services : An OverviewAnirudh JainNoch keine Bewertungen

- Marketing Budget: Expenses Q1 Q2 Q3 Q4 Totals Budget %Dokument20 SeitenMarketing Budget: Expenses Q1 Q2 Q3 Q4 Totals Budget %Miaow MiaowNoch keine Bewertungen

- Automotive E-Coat Paint Process Simulation Using FEADokument20 SeitenAutomotive E-Coat Paint Process Simulation Using FEAflowh_100% (1)

- Primary 2 (Grade 2) - GEP Practice: Contest Problems With Full SolutionsDokument24 SeitenPrimary 2 (Grade 2) - GEP Practice: Contest Problems With Full Solutionswenxinyu1002100% (1)

- SAP SD Course Content PDFDokument4 SeitenSAP SD Course Content PDFshuku03Noch keine Bewertungen

- 03 Seatwork 1 ProjectManagement SenisRachelDokument2 Seiten03 Seatwork 1 ProjectManagement SenisRachelRachel SenisNoch keine Bewertungen

- Snorkeling: A Brief History and Guide to This Underwater AdventureDokument3 SeitenSnorkeling: A Brief History and Guide to This Underwater AdventureBernadette PerezNoch keine Bewertungen