Das könnte Ihnen auch gefallen

- Flash - Memory - Inc From Website 0515Dokument8 SeitenFlash - Memory - Inc From Website 0515竹本口木子100% (1)

- Flash Memory AnalysisDokument25 SeitenFlash Memory AnalysisTheicon420Noch keine Bewertungen

- Flash Memory AnalysisDokument25 SeitenFlash Memory AnalysisaamirNoch keine Bewertungen

- Flash Memory Case SolutionDokument10 SeitenFlash Memory Case SolutionsahilkuNoch keine Bewertungen

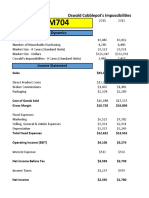

- Flash Memory ExcelDokument4 SeitenFlash Memory ExcelHarshita SethiyaNoch keine Bewertungen

- Harvard Case Study - Flash Inc - AllDokument40 SeitenHarvard Case Study - Flash Inc - All竹本口木子100% (1)

- Flash MemoryDokument9 SeitenFlash MemoryJeffery KaoNoch keine Bewertungen

- Flash Memory CaseDokument6 SeitenFlash Memory Casechitu199233% (3)

- Flash Memory IncDokument3 SeitenFlash Memory IncAhsan IqbalNoch keine Bewertungen

- Flash Memory, Inc.Dokument2 SeitenFlash Memory, Inc.Stella Zukhbaia0% (5)

- FlashMemory SolnDokument8 SeitenFlashMemory Solnchopra98harsh3311100% (4)

- Flash Memory Case Study SolutionDokument8 SeitenFlash Memory Case Study SolutionRohit Parnerkar57% (7)

- FlashMemory Beta NPVDokument7 SeitenFlashMemory Beta NPVShubham Bhatia50% (2)

- Flash Inc Financial StatementsDokument14 SeitenFlash Inc Financial Statementsdummy306075% (4)

- Flash Memory, IncDokument16 SeitenFlash Memory, Inckiller drama67% (3)

- Case - Flash Memory, Inc. - SolutionDokument11 SeitenCase - Flash Memory, Inc. - SolutionBryan Meza71% (38)

- New Heritage Doll CompanDokument9 SeitenNew Heritage Doll CompanArima ChatterjeeNoch keine Bewertungen

- Online AnswerDokument4 SeitenOnline AnswerYiru Pan100% (2)

- Assumptions: Comparable Companies:Market ValueDokument18 SeitenAssumptions: Comparable Companies:Market ValueTanya YadavNoch keine Bewertungen

- BurtonsDokument6 SeitenBurtonsKritika GoelNoch keine Bewertungen

- AirThread G015Dokument6 SeitenAirThread G015Kunal MaheshwariNoch keine Bewertungen

- Airthread Excel SolutionDokument18 SeitenAirthread Excel SolutionRiya ShahNoch keine Bewertungen

- AirThread Class 2020Dokument21 SeitenAirThread Class 2020Son NguyenNoch keine Bewertungen

- New Heritage DoolDokument9 SeitenNew Heritage DoolVidya Sagar KonaNoch keine Bewertungen

- Flash Memory IncDokument7 SeitenFlash Memory IncAbhinandan SinghNoch keine Bewertungen

- AirThread ConnectionDokument26 SeitenAirThread ConnectionAnandNoch keine Bewertungen

- HBS Mercury CaseDokument4 SeitenHBS Mercury CaseDavid Petru100% (1)

- Mercuryathleticfootwera Case AnalysisDokument8 SeitenMercuryathleticfootwera Case AnalysisNATOEENoch keine Bewertungen

- Valuation of Airthread April 2012Dokument26 SeitenValuation of Airthread April 2012Perumalla Pradeep KumarNoch keine Bewertungen

- Mercury Athletic (Student Templates) FinalDokument6 SeitenMercury Athletic (Student Templates) FinalGarland GayNoch keine Bewertungen

- Airthread SolutionDokument30 SeitenAirthread SolutionSrikanth VasantadaNoch keine Bewertungen

- (Shared) Day5 Harmonic Hearing Co. - 4271Dokument17 Seiten(Shared) Day5 Harmonic Hearing Co. - 4271DamTokyo0% (2)

- Tire City Spreadsheet SolutionDokument7 SeitenTire City Spreadsheet SolutionSyed Ali MurtuzaNoch keine Bewertungen

- MercuryDokument5 SeitenMercuryமுத்துக்குமார் செNoch keine Bewertungen

- Front Valuation Page: Un-Levered Firm ValueDokument61 SeitenFront Valuation Page: Un-Levered Firm Valueneelakanta srikar100% (1)

- Monmouth Group4Dokument18 SeitenMonmouth Group4Jake Rolly0% (1)

- Millions of Dollars Except Per-Share DataDokument14 SeitenMillions of Dollars Except Per-Share DataVishal VermaNoch keine Bewertungen

- Burton SensorsDokument2 SeitenBurton SensorsSankalp MishraNoch keine Bewertungen

- Heritage CaseDokument3 SeitenHeritage CaseGregory ChengNoch keine Bewertungen

- NHDC Solution EditedDokument5 SeitenNHDC Solution EditedShreesh ChandraNoch keine Bewertungen

- Blaine SolutionDokument4 SeitenBlaine Solutionchintan MehtaNoch keine Bewertungen

- Sampa VideoDokument24 SeitenSampa VideodoiNoch keine Bewertungen

- Section I. High-Growth Strategy of Marshall, Company Financing and Its Potential Stock Price ChangeDokument11 SeitenSection I. High-Growth Strategy of Marshall, Company Financing and Its Potential Stock Price ChangeclendeavourNoch keine Bewertungen

- New Heritage Doll Company Case SolutionDokument31 SeitenNew Heritage Doll Company Case SolutionSoundarya AbiramiNoch keine Bewertungen

- Blaine Kitchenware ExcelDokument1 SeiteBlaine Kitchenware ExcelRoderick Jackson JrNoch keine Bewertungen

- Monmouth Case SolutionDokument16 SeitenMonmouth Case SolutionAjaxNoch keine Bewertungen

- Caso TeuerDokument46 SeitenCaso Teuerjoaquin bullNoch keine Bewertungen

- Sampa Video: Project ValuationDokument18 SeitenSampa Video: Project Valuationkrissh_87Noch keine Bewertungen

- Exhibits of Blaine Kitchenware, Inc - CaseDokument6 SeitenExhibits of Blaine Kitchenware, Inc - CaseSadam Lashari100% (3)

- Flash MemoryDokument14 SeitenFlash MemoryPranav TatavarthiNoch keine Bewertungen

- Student Workbook Flash Amended Final PDFDokument21 SeitenStudent Workbook Flash Amended Final PDFGaryNoch keine Bewertungen

- Tire City ExhibitsDokument7 SeitenTire City ExhibitsAyushi GuptaNoch keine Bewertungen

- ACCOUNTING GroupProjectDokument17 SeitenACCOUNTING GroupProjectAshna KoshalNoch keine Bewertungen

- 36220602Dokument14 Seiten36220602Aijaz ShaikhNoch keine Bewertungen

- Copycooperative Financial Ratio Calculator 2011Dokument10 SeitenCopycooperative Financial Ratio Calculator 2011pradhan13Noch keine Bewertungen

- ANS #3 Ritik SehgalDokument10 SeitenANS #3 Ritik Sehgaljasbir singhNoch keine Bewertungen

- Under Armour Valuation and Forecasts Spreadsheet Completed On 7/1/2019Dokument14 SeitenUnder Armour Valuation and Forecasts Spreadsheet Completed On 7/1/2019Iqbal YusufNoch keine Bewertungen

- Lesson 3Dokument29 SeitenLesson 3Anh MinhNoch keine Bewertungen

- 1 - Week 6 Final Case Project Workbook - Abc Company - Spring 2019Dokument8 Seiten1 - Week 6 Final Case Project Workbook - Abc Company - Spring 2019Minh Van NguyenNoch keine Bewertungen

- Trabajo Final DireccionDokument17 SeitenTrabajo Final DireccionAnani RomeroNoch keine Bewertungen

- SuperannuationDokument12 SeitenSuperannuationNetaji DasariNoch keine Bewertungen

- Bank (Final)Dokument25 SeitenBank (Final)MishuNoch keine Bewertungen

- Letter of CreditDokument7 SeitenLetter of CreditAnam AshfaqNoch keine Bewertungen

- Halk Godisen 2016Dokument47 SeitenHalk Godisen 2016kasraNoch keine Bewertungen

- ACCOUNTING AllPapersDokument128 SeitenACCOUNTING AllPapersAbbas AliNoch keine Bewertungen

- CHA Participant Reference GuideDokument152 SeitenCHA Participant Reference GuideMegNoch keine Bewertungen

- IFRS 5 Non-Current Assets Held For SaleDokument25 SeitenIFRS 5 Non-Current Assets Held For SaleziyuNoch keine Bewertungen

- CV Stefano PasquarelliDokument1 SeiteCV Stefano PasquarelliDaniele RocchiNoch keine Bewertungen

- Main PDFDokument34 SeitenMain PDFLuminati ProNoch keine Bewertungen

- NBFCs Sip 2020Dokument52 SeitenNBFCs Sip 2020Prashant AgarkarNoch keine Bewertungen

- Green Bonds Getting The Harmony RightDokument82 SeitenGreen Bonds Getting The Harmony RightLía Lizzette Ferreira MárquezNoch keine Bewertungen

- An Economic Analysis of Dhaka - Chittagon PDFDokument24 SeitenAn Economic Analysis of Dhaka - Chittagon PDFshivu khatriNoch keine Bewertungen

- Role of Local Government in Promotion of TourismDokument17 SeitenRole of Local Government in Promotion of Tourismhayat_shaw100% (5)

- 2midterm ExaminationDokument3 Seiten2midterm ExaminationAlice KingsleighNoch keine Bewertungen

- Musharakah by Sheikh Muhammad Taqi UsmaniDokument9 SeitenMusharakah by Sheikh Muhammad Taqi UsmaniMUSALMAN BHAINoch keine Bewertungen

- Tutorial 9 Ak For Econ 1102Dokument7 SeitenTutorial 9 Ak For Econ 1102Jonathan JoesNoch keine Bewertungen

- Strategy AssignmentDokument17 SeitenStrategy AssignmentprasanthkurupNoch keine Bewertungen

- Blue Ocean Strategy in Construction IndustryDokument41 SeitenBlue Ocean Strategy in Construction Industrykrshn0775% (4)

- Introduction To Global Investment Banking - Merrill LynchDokument28 SeitenIntroduction To Global Investment Banking - Merrill LynchAlexander Junior Huayana Espinoza100% (2)

- GMOMelt UpDokument13 SeitenGMOMelt UpHeisenberg100% (2)

- Nestle Pakistan Limited Balance Sheet: 2020 2019 2018 Equity and Liabilities Share Capital and ReservesDokument39 SeitenNestle Pakistan Limited Balance Sheet: 2020 2019 2018 Equity and Liabilities Share Capital and ReservesFarah NazNoch keine Bewertungen

- Before Starting A Business Start Up ChecklistDokument65 SeitenBefore Starting A Business Start Up ChecklistJude21Noch keine Bewertungen

- Cmpma - 3 IMP PDFDokument5 SeitenCmpma - 3 IMP PDFtusharholey90Noch keine Bewertungen

- V2 Exam 2 PM PDFDokument30 SeitenV2 Exam 2 PM PDFMaharishi VaidyaNoch keine Bewertungen

- Course Outline: Prepared By: MD. EDRICH MOLLA JEWELDokument2 SeitenCourse Outline: Prepared By: MD. EDRICH MOLLA JEWELAlaminTanverNoch keine Bewertungen

- MTA JournalDokument9 SeitenMTA Journaltaylor144100% (10)

- Budget 2018-19: L'intégralité Des MesuresDokument145 SeitenBudget 2018-19: L'intégralité Des MesuresL'express Maurice100% (1)

- 2019 20 Budget EstimatesA PDFDokument252 Seiten2019 20 Budget EstimatesA PDFDmitri TuittNoch keine Bewertungen

- Gov UscourtsDokument414 SeitenGov UscourtsForeclosure Fraud100% (2)

- Project Report of Megha SharmaDokument117 SeitenProject Report of Megha SharmaSalman QureshiNoch keine Bewertungen