Das könnte Ihnen auch gefallen

- Final Examination: Suggested Answers - Syl2016 - June 2019 - Paper 17Dokument24 SeitenFinal Examination: Suggested Answers - Syl2016 - June 2019 - Paper 17Padmini SatapathyNoch keine Bewertungen

- Paper 33Dokument6 SeitenPaper 33AVS InfraNoch keine Bewertungen

- Delhi Public School Jodhpur: General InstructionsDokument4 SeitenDelhi Public School Jodhpur: General Instructionssamyak patwaNoch keine Bewertungen

- Revisionary Test Paper - Dec 2018: Final Group IV Paper 17: Corporate Financial Reporting (SYLLABUS - 2016)Dokument49 SeitenRevisionary Test Paper - Dec 2018: Final Group IV Paper 17: Corporate Financial Reporting (SYLLABUS - 2016)tukaram vdNoch keine Bewertungen

- Cma Question PaperDokument4 SeitenCma Question PaperHilary GaureaNoch keine Bewertungen

- Accounts Mock Test May 2019Dokument18 SeitenAccounts Mock Test May 2019poojitha reddyNoch keine Bewertungen

- CA Intermediate Advanced Accounting Mock Test 19 - 01 - 2024Dokument13 SeitenCA Intermediate Advanced Accounting Mock Test 19 - 01 - 2024rohit 6375Noch keine Bewertungen

- Suggested Answer - Syl12 - Jun2014 - Paper - 18 Final Examination: Suggested Answers To QuestionsDokument32 SeitenSuggested Answer - Syl12 - Jun2014 - Paper - 18 Final Examination: Suggested Answers To QuestionsMdAnjum1991Noch keine Bewertungen

- 4th Sem PRT 3Dokument25 Seiten4th Sem PRT 3Sunanda MathuriaNoch keine Bewertungen

- Cma Dec 22 Answers - DraftDokument24 SeitenCma Dec 22 Answers - DraftDispute FreezNoch keine Bewertungen

- Financial Accounting-Iii - HonoursDokument7 SeitenFinancial Accounting-Iii - HonoursAlankrita TripathiNoch keine Bewertungen

- 19696ipcc Acc Vol2 Chapter14Dokument41 Seiten19696ipcc Acc Vol2 Chapter14Shivam TripathiNoch keine Bewertungen

- Paper 17Dokument5 SeitenPaper 17VijayaNoch keine Bewertungen

- Suggested Answers 2017Dokument33 SeitenSuggested Answers 2017Ram UpendraNoch keine Bewertungen

- Sem-5 10 BCOM HONS DSE-5.2A CORPORATE-ACCOUNTING-0758Dokument5 SeitenSem-5 10 BCOM HONS DSE-5.2A CORPORATE-ACCOUNTING-0758hussain shahidNoch keine Bewertungen

- Paper - 5: Advanced Accounting: © The Institute of Chartered Accountants of IndiaDokument31 SeitenPaper - 5: Advanced Accounting: © The Institute of Chartered Accountants of IndiaVarun reddyNoch keine Bewertungen

- Financial Reporting & Financial Statement Analysis: Time - 3 Hours Group - ADokument6 SeitenFinancial Reporting & Financial Statement Analysis: Time - 3 Hours Group - Atanmoy sardarNoch keine Bewertungen

- Test Series: November, 2021 Mock Test Paper - 2 Intermediate (New) : Group - I Paper - 1: AccountingDokument8 SeitenTest Series: November, 2021 Mock Test Paper - 2 Intermediate (New) : Group - I Paper - 1: Accountingsunil1287Noch keine Bewertungen

- Compilation of Accounts-CompressedDokument304 SeitenCompilation of Accounts-Compressedsalaarbhai2322Noch keine Bewertungen

- Suggested Answer - Syl12 - June2017 - Paper - 12 Intermediate ExaminationDokument16 SeitenSuggested Answer - Syl12 - June2017 - Paper - 12 Intermediate ExaminationDevendra AryaNoch keine Bewertungen

- Cma Fina Group4 All MCQDokument205 SeitenCma Fina Group4 All MCQtusharjaipur7Noch keine Bewertungen

- Commerce (Regular) Accounting For Specialised Institutions (Group A: Accounting and Finance) Paper - 3.5 (A)Dokument4 SeitenCommerce (Regular) Accounting For Specialised Institutions (Group A: Accounting and Finance) Paper - 3.5 (A)Sanaullah M SultanpurNoch keine Bewertungen

- CP 123 PDFDokument4 SeitenCP 123 PDFJoshi DrcpNoch keine Bewertungen

- 6th Semester Paper 2022Dokument5 Seiten6th Semester Paper 2022Chandrarup BanerjeeNoch keine Bewertungen

- ANSWERDokument10 SeitenANSWERHilary GaureaNoch keine Bewertungen

- 12 Accounts 2020 21 Practice Paper 2Dokument8 Seiten12 Accounts 2020 21 Practice Paper 2Vijey RamalingamNoch keine Bewertungen

- Test Series: March 2022 Mock Test Paper 1 Intermediate: Group - Ii Paper - 5: Advanced AccountingDokument7 SeitenTest Series: March 2022 Mock Test Paper 1 Intermediate: Group - Ii Paper - 5: Advanced AccountingShrwan SinghNoch keine Bewertungen

- MTP1 May2022 - Paper 5 Advanced AccountingDokument24 SeitenMTP1 May2022 - Paper 5 Advanced AccountingYash YashwantNoch keine Bewertungen

- Paper 16 - Direct Tax Laws and International Taxation: MTP - Final - Syllabus 2016 - Jun 2020 - Set 1Dokument5 SeitenPaper 16 - Direct Tax Laws and International Taxation: MTP - Final - Syllabus 2016 - Jun 2020 - Set 1GODWIN VIJUNoch keine Bewertungen

- Paper12 Set1 SolutionDokument17 SeitenPaper12 Set1 SolutionMohamedThabrisNoch keine Bewertungen

- QP Insurance Company AccountsDokument6 SeitenQP Insurance Company AccountschetandeepakNoch keine Bewertungen

- Test 4Dokument8 SeitenTest 4govarthan1976Noch keine Bewertungen

- Test Series: October, 2020 Mock Test Paper Final (Old) Course: Group - Ii Paper - 7: Direct Tax LawsDokument11 SeitenTest Series: October, 2020 Mock Test Paper Final (Old) Course: Group - Ii Paper - 7: Direct Tax LawsAnshul JainNoch keine Bewertungen

- RTP Nov 14Dokument127 SeitenRTP Nov 14sathish_61288@yahooNoch keine Bewertungen

- Mock Questions ICAiDokument7 SeitenMock Questions ICAiPooja GalaNoch keine Bewertungen

- Model Test Paper-1Dokument24 SeitenModel Test Paper-1dawraparul27Noch keine Bewertungen

- CA Ipcc n19p1Dokument27 SeitenCA Ipcc n19p1rachitu2105Noch keine Bewertungen

- 61089bos49694 Ipc Nov2019 gp1Dokument93 Seiten61089bos49694 Ipc Nov2019 gp1iswerya n.sNoch keine Bewertungen

- Intermediate Group I Test PapersDokument57 SeitenIntermediate Group I Test Paperssantbaksmishra1261Noch keine Bewertungen

- Corporate Accounting - IIDokument5 SeitenCorporate Accounting - IIjeganrajrajNoch keine Bewertungen

- IFRS - 2019 - Solved QPDokument14 SeitenIFRS - 2019 - Solved QPSharan ReddyNoch keine Bewertungen

- IFRS - 2017 - Solved QPDokument15 SeitenIFRS - 2017 - Solved QPSharan ReddyNoch keine Bewertungen

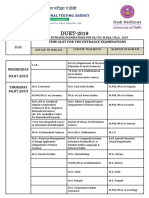

- Management Programme Term-End Examination June, 2019: Ms-004: Accounting and Finance For ManagersDokument4 SeitenManagement Programme Term-End Examination June, 2019: Ms-004: Accounting and Finance For ManagersreliableplacementNoch keine Bewertungen

- Paper 7-Direct Taxation: MTP - Intermediate - Syllabus 2012 - June2016 - Set 1Dokument7 SeitenPaper 7-Direct Taxation: MTP - Intermediate - Syllabus 2012 - June2016 - Set 1Ankit ShawNoch keine Bewertungen

- Pccquestionpapers (2008)Dokument20 SeitenPccquestionpapers (2008)Samenew77Noch keine Bewertungen

- TtryuiopDokument6 SeitenTtryuiopNAVEENNoch keine Bewertungen

- Question No.1 Is Compulsory. Candidates Are Required To Answer Any Four Questions From The Remaining Five QuestionsDokument7 SeitenQuestion No.1 Is Compulsory. Candidates Are Required To Answer Any Four Questions From The Remaining Five Questionsritz meshNoch keine Bewertungen

- Financial Reporting: Specimen Exam Applicable From September 2016Dokument25 SeitenFinancial Reporting: Specimen Exam Applicable From September 2016Jodlike bolteNoch keine Bewertungen

- 12 Accounts 2020 21 Practice Paper 3Dokument9 Seiten12 Accounts 2020 21 Practice Paper 3Vijey RamalingamNoch keine Bewertungen

- Paper - 5: Advanced Accounting: Particulars NosDokument32 SeitenPaper - 5: Advanced Accounting: Particulars NosAmolaNoch keine Bewertungen

- Ca Final New Direct Tax Laws and International Taxation May 2018 1525Dokument31 SeitenCa Final New Direct Tax Laws and International Taxation May 2018 1525pradeep kumarNoch keine Bewertungen

- Paper10 Set1Dokument8 SeitenPaper10 Set13 6 1 4 6 Ganesh Kumaran ANoch keine Bewertungen

- P5 Syl2012 Set2Dokument22 SeitenP5 Syl2012 Set2JOLLYNoch keine Bewertungen

- CFR Dec 2017Dokument22 SeitenCFR Dec 2017shubham bhardwajNoch keine Bewertungen

- CA Foundation AccountDokument7 SeitenCA Foundation Accountrishab kumarNoch keine Bewertungen

- Accountancy Sample Question PaperDokument8 SeitenAccountancy Sample Question PaperSoNam ZaNgmoNoch keine Bewertungen

- Financial Reporting May 22 Mock Test Ques PPRDokument7 SeitenFinancial Reporting May 22 Mock Test Ques PPRVrinda GuptaNoch keine Bewertungen

- A Comparative Analysis of Tax Administration in Asia and the Pacific—Sixth EditionVon EverandA Comparative Analysis of Tax Administration in Asia and the Pacific—Sixth EditionNoch keine Bewertungen

- A Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionVon EverandA Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionNoch keine Bewertungen

- Securitization in India: Managing Capital Constraints and Creating Liquidity to Fund Infrastructure AssetsVon EverandSecuritization in India: Managing Capital Constraints and Creating Liquidity to Fund Infrastructure AssetsNoch keine Bewertungen

- EA Asignment Cover PageDokument5 SeitenEA Asignment Cover PageBhupen SharmaNoch keine Bewertungen

- 06 - List of Tables FiguresDokument7 Seiten06 - List of Tables FiguresBhupen SharmaNoch keine Bewertungen

- FM Assignment Cover PagesDokument5 SeitenFM Assignment Cover PagesBhupen SharmaNoch keine Bewertungen

- Addressing To FAQ'S (Frequently Asked Questions) Regarding "Dissertation"Dokument2 SeitenAddressing To FAQ'S (Frequently Asked Questions) Regarding "Dissertation"Bhupen SharmaNoch keine Bewertungen

- Indas 113 PDFDokument8 SeitenIndas 113 PDFBhupen SharmaNoch keine Bewertungen

- Coop - Assignment Cover PagesDokument5 SeitenCoop - Assignment Cover PagesBhupen SharmaNoch keine Bewertungen

- Coop. GRP 3rd Sem EAFMDokument15 SeitenCoop. GRP 3rd Sem EAFMBhupen SharmaNoch keine Bewertungen

- The Institute of Cost Accountants of India: Cma Bhawan 12, Sudder Street, Kolkata - 700 016Dokument1 SeiteThe Institute of Cost Accountants of India: Cma Bhawan 12, Sudder Street, Kolkata - 700 016Bhupen SharmaNoch keine Bewertungen

- Paper 16 - Direct Tax Laws and International Taxation: MTP - Final - Syllabus 2016 - Dec 2019 - Set 2Dokument6 SeitenPaper 16 - Direct Tax Laws and International Taxation: MTP - Final - Syllabus 2016 - Dec 2019 - Set 2Bhupen SharmaNoch keine Bewertungen

- List of Notified Sections Applicable For June, 2020 Term ExaminationDokument36 SeitenList of Notified Sections Applicable For June, 2020 Term ExaminationBhupen SharmaNoch keine Bewertungen

- f12 Stats250 Bgunderson Statsfullyellowcard 0Dokument4 Seitenf12 Stats250 Bgunderson Statsfullyellowcard 0Bhupen SharmaNoch keine Bewertungen

- Corporate Governance: Kingdom of Saudi Arabia Capital Market AuthorityDokument16 SeitenCorporate Governance: Kingdom of Saudi Arabia Capital Market AuthorityBhupen SharmaNoch keine Bewertungen

- Factors Affecting Property Value PDFDokument2 SeitenFactors Affecting Property Value PDFJennifer100% (1)

- Loyalty Card Plus: Application FormDokument2 SeitenLoyalty Card Plus: Application FormKillah BeatsNoch keine Bewertungen

- Payment 4310725205Dokument1 SeitePayment 4310725205Radoslav TsvetkovNoch keine Bewertungen

- Video Production Quote TemplateDokument2 SeitenVideo Production Quote TemplateJosé Carlos Godinez VasquezNoch keine Bewertungen

- Ticks Hunter Bot GuideDokument7 SeitenTicks Hunter Bot GuideKingtayNoch keine Bewertungen

- Dodd Frank CertificationDokument1 SeiteDodd Frank CertificationTara IsmineNoch keine Bewertungen

- 2012a Buyback NoticeDokument4 Seiten2012a Buyback Noticekv chandrasekerNoch keine Bewertungen

- CH 08Dokument51 SeitenCH 08Daniel NababanNoch keine Bewertungen

- Solved Twelve Years Ago Marilyn Purchased Two Lots in An UndevelopedDokument1 SeiteSolved Twelve Years Ago Marilyn Purchased Two Lots in An UndevelopedAnbu jaromiaNoch keine Bewertungen

- Quizzer-CAPITAL BUDGETING - Non-Discounted (With Solutions)Dokument3 SeitenQuizzer-CAPITAL BUDGETING - Non-Discounted (With Solutions)Ferb Cruzada80% (5)

- 705 - PGBP AdjustmentsDokument10 Seiten705 - PGBP AdjustmentsKumar SwamyNoch keine Bewertungen

- Your Guide To Perfect CreditDokument168 SeitenYour Guide To Perfect Creditwhistjenn100% (5)

- Karla Company P-WPS OfficeDokument14 SeitenKarla Company P-WPS OfficeKris Van HalenNoch keine Bewertungen

- Commercial Property Advisors Due Diligence ChecklistsDokument8 SeitenCommercial Property Advisors Due Diligence ChecklistsAnonymous xcxC7m100% (1)

- Manufacturing Accounts FormatDokument7 SeitenManufacturing Accounts Formatlaguda babajide100% (10)

- Investment Decision RulesDokument14 SeitenInvestment Decision RulesprashantgoruleNoch keine Bewertungen

- Gap Thesis and The Survival of Informal Financial Sector in NigeriaDokument6 SeitenGap Thesis and The Survival of Informal Financial Sector in NigeriaMadiha MunirNoch keine Bewertungen

- Solved Rollo and Andrea Are Equal Owners of Gosney Company DuringDokument1 SeiteSolved Rollo and Andrea Are Equal Owners of Gosney Company DuringAnbu jaromiaNoch keine Bewertungen

- Audit of Property, Plant and Equipment: Auditing ProblemsDokument5 SeitenAudit of Property, Plant and Equipment: Auditing ProblemsLei PangilinanNoch keine Bewertungen

- Derivatives and Risk ManagementDokument5 SeitenDerivatives and Risk ManagementabhishekrameshnagNoch keine Bewertungen

- Brokerage Agreement-ExclusiveDokument3 SeitenBrokerage Agreement-ExclusiveMarvin B. SoteloNoch keine Bewertungen

- Ates Cagdas Ozan Behavioral Finance and Sports Betting Markets MSC 2004Dokument83 SeitenAtes Cagdas Ozan Behavioral Finance and Sports Betting Markets MSC 2004yexed63889Noch keine Bewertungen

- FX MrktsDokument46 SeitenFX MrktsSoe Group 1Noch keine Bewertungen

- Statement 1688358203630Dokument3 SeitenStatement 1688358203630Chinmay RajNoch keine Bewertungen

- Computation 2022-23Dokument2 SeitenComputation 2022-23DKINGNoch keine Bewertungen

- Tr3ndy Jon's Trading StrategiesDokument3 SeitenTr3ndy Jon's Trading Strategieshotdog10Noch keine Bewertungen

- List of Project Topics For Accountancy DDokument4 SeitenList of Project Topics For Accountancy DnebiyuNoch keine Bewertungen

- Appraisal ReportDokument193 SeitenAppraisal ReportDicky BhaktiNoch keine Bewertungen

- Pre Test No. 1.2 HobaDokument2 SeitenPre Test No. 1.2 HobaJean TatsadoNoch keine Bewertungen

- World Bank (IBRD & IDA)Dokument5 SeitenWorld Bank (IBRD & IDA)prankyaquariusNoch keine Bewertungen