Das könnte Ihnen auch gefallen

- World Merit Factor Analysis for Hydrogen Fueled TransportationVon EverandWorld Merit Factor Analysis for Hydrogen Fueled TransportationNoch keine Bewertungen

- Green & Brown Field Development:: A Case For Associated Gas Utilisation in NigeriaDokument33 SeitenGreen & Brown Field Development:: A Case For Associated Gas Utilisation in NigeriayemiNoch keine Bewertungen

- Thomas Larsen, Senior Technical Manager, HOEG LNG Asia Pte Ltd.Dokument9 SeitenThomas Larsen, Senior Technical Manager, HOEG LNG Asia Pte Ltd.Shah Reza DwiputraNoch keine Bewertungen

- Mahdjouba BELAIFA Bolivia Presentation Final Resume Without SpeechDokument21 SeitenMahdjouba BELAIFA Bolivia Presentation Final Resume Without SpeechlucmontNoch keine Bewertungen

- Global Gas Market and Its ChallengesDokument15 SeitenGlobal Gas Market and Its ChallengesjosealvaroNoch keine Bewertungen

- Cement - PACRA Research - Mar'22 - 1648648517Dokument34 SeitenCement - PACRA Research - Mar'22 - 1648648517Ammad TahirNoch keine Bewertungen

- LPG Profile 1.4.2021: As OnDokument14 SeitenLPG Profile 1.4.2021: As OnSushobhan DasNoch keine Bewertungen

- The Global Small-Mid Scale LNG Story 2014Dokument1 SeiteThe Global Small-Mid Scale LNG Story 2014Fernando RoseroNoch keine Bewertungen

- LNG BasicsDokument19 SeitenLNG BasicsKalai Selvan100% (1)

- TestDokument67 SeitenTestPrabhakar SinhaNoch keine Bewertungen

- Course On LNG Business-Session4Dokument33 SeitenCourse On LNG Business-Session4Rahul Atodaria100% (1)

- CW - Webinar - TPR 3Q2020 - CopyrightedDokument20 SeitenCW - Webinar - TPR 3Q2020 - CopyrightedStockKingNoch keine Bewertungen

- World LNG 2017 IGU - Report PDFDokument100 SeitenWorld LNG 2017 IGU - Report PDFRABIU M RABIUNoch keine Bewertungen

- Feasibility Study Long Form 1.06.20 FINAL For WEBSITEDokument50 SeitenFeasibility Study Long Form 1.06.20 FINAL For WEBSITEselamet riantoNoch keine Bewertungen

- Trends in PV Markets: Gaëtan Masson, IEA PVPS Task 1 Operating Agent - Becquerel Institute Leonardo Energy - 04 Feb 2021Dokument43 SeitenTrends in PV Markets: Gaëtan Masson, IEA PVPS Task 1 Operating Agent - Becquerel Institute Leonardo Energy - 04 Feb 2021Ouzeren AbdelhakimNoch keine Bewertungen

- ST and Trends FINAL-08Dokument18 SeitenST and Trends FINAL-08anon-656678100% (1)

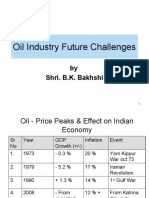

- Oil Industry Future Challenges: by Shri. B.K. BakhshiDokument21 SeitenOil Industry Future Challenges: by Shri. B.K. BakhshiGirish1412Noch keine Bewertungen

- Overview of Sonatrach Corporate ProfileDokument12 SeitenOverview of Sonatrach Corporate ProfilesijoNoch keine Bewertungen

- Low Carbon Growth: Indian Industry PerspectiveDokument29 SeitenLow Carbon Growth: Indian Industry PerspectiveakshayjohurNoch keine Bewertungen

- Производители базовых масел 2010Dokument27 SeitenПроизводители базовых масел 2010Konstantin FedotenkovNoch keine Bewertungen

- TCMB Cembureau - Brannvoll Presentation Final 1 Oct 3 2017Dokument41 SeitenTCMB Cembureau - Brannvoll Presentation Final 1 Oct 3 2017umutNoch keine Bewertungen

- LTATF TATASTEEL PresentationDokument8 SeitenLTATF TATASTEEL PresentationKiranNoch keine Bewertungen

- 21 AtlantiaDokument39 Seiten21 AtlantiapolopolpoNoch keine Bewertungen

- Condensed Consolidated Interim Results (Reviewed) : For The Six Months Ended 31 December 2020Dokument50 SeitenCondensed Consolidated Interim Results (Reviewed) : For The Six Months Ended 31 December 2020Serkan BirolNoch keine Bewertungen

- GCC - Plastic IndustryDokument44 SeitenGCC - Plastic IndustrySeshagiri KalyanasundaramNoch keine Bewertungen

- Ief Energy Outlook 2018-09-09Dokument18 SeitenIef Energy Outlook 2018-09-09sme2020Noch keine Bewertungen

- Presentation On LNG For Pip Seminar in Pso HouseDokument26 SeitenPresentation On LNG For Pip Seminar in Pso HouseRASHID AHMED SHAIKHNoch keine Bewertungen

- Top Contractors View v3Dokument65 SeitenTop Contractors View v3Sameh سامح MaherNoch keine Bewertungen

- Mayank Ashar PresentationDokument16 SeitenMayank Ashar PresentationtarangtusharNoch keine Bewertungen

- 2.2 Mark Evans Afa2014draftpaperDokument12 Seiten2.2 Mark Evans Afa2014draftpaperGurnam Singh0% (1)

- NickelMkt GoodDokument4 SeitenNickelMkt Goodtdazzv13784Noch keine Bewertungen

- Wilhelmsen Ships Agency LNG Outlook Report To 2030Dokument27 SeitenWilhelmsen Ships Agency LNG Outlook Report To 2030roberto_man5003Noch keine Bewertungen

- DatabaseDokument13 SeitenDatabaseRyangNoch keine Bewertungen

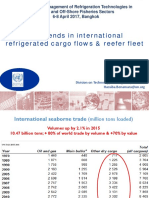

- Key Trends in International Refrigerated Cargo Flows & Reefer FleetDokument21 SeitenKey Trends in International Refrigerated Cargo Flows & Reefer FleetMiguel Rodríguez SoutoNoch keine Bewertungen

- LNG Journal JulAug08Dokument52 SeitenLNG Journal JulAug08HimSelfNoch keine Bewertungen

- LNG ShippingDokument46 SeitenLNG ShippingmekulaNoch keine Bewertungen

- The Nickel Market: I. Historical PricesDokument4 SeitenThe Nickel Market: I. Historical PricesTuan AnhNoch keine Bewertungen

- WKT Lindi Definitive Feasibility Study UpdatedDokument10 SeitenWKT Lindi Definitive Feasibility Study UpdatedRob FletcherNoch keine Bewertungen

- PNGRB Presentation 9th Bid Round New DelhiDokument24 SeitenPNGRB Presentation 9th Bid Round New DelhiG Vishwanath ReddyNoch keine Bewertungen

- Chapter 9 Policies in Industrialized CountriesDokument15 SeitenChapter 9 Policies in Industrialized CountriesMohamed Yacouba KalloNoch keine Bewertungen

- Reliance ModifiedDokument13 SeitenReliance ModifiedYASH BHATINoch keine Bewertungen

- Dry Bulk Shipping: Bi-Weekly ReportDokument2 SeitenDry Bulk Shipping: Bi-Weekly ReportResearch SaigalseatradeNoch keine Bewertungen

- Peng GB4e PPT ch05Dokument38 SeitenPeng GB4e PPT ch05GeddsueNoch keine Bewertungen

- Advances and Perspectives of Hybrid Rice in The Americas: Leandro PasqualliDokument31 SeitenAdvances and Perspectives of Hybrid Rice in The Americas: Leandro PasqualliPivaralNoch keine Bewertungen

- Dry Bulk Shipping: Bi-Weekly ReportDokument2 SeitenDry Bulk Shipping: Bi-Weekly ReportResearch SaigalseatradeNoch keine Bewertungen

- Dry Bulk Shipping: Bi-Weekly ReportDokument2 SeitenDry Bulk Shipping: Bi-Weekly ReportResearch SaigalseatradeNoch keine Bewertungen

- 2019 Barcelona - Wael Abdel MoatiDokument21 Seiten2019 Barcelona - Wael Abdel MoatiWaelNoch keine Bewertungen

- EV PRND Drivers FinalDokument47 SeitenEV PRND Drivers FinalResearchtimeNoch keine Bewertungen

- ICIS London 2018 Apu GosaliaDokument25 SeitenICIS London 2018 Apu GosaliaPrabhakar SinhaNoch keine Bewertungen

- Duke Investment Club: Caterpillar, Inc (CAT)Dokument12 SeitenDuke Investment Club: Caterpillar, Inc (CAT)Qiao WuNoch keine Bewertungen

- M1 P1 Energy Review World and India DR R R JoshiDokument36 SeitenM1 P1 Energy Review World and India DR R R JoshiAkshat RawatNoch keine Bewertungen

- QMAG Presentation 2008Dokument19 SeitenQMAG Presentation 2008tamtran_cnuNoch keine Bewertungen

- WMac BPlanDokument33 SeitenWMac BPlanpyush0786Noch keine Bewertungen

- Conocophillips (Cop) - 2007 Integrated Oil & Gas OutlookDokument4 SeitenConocophillips (Cop) - 2007 Integrated Oil & Gas OutlookSaul StermanNoch keine Bewertungen

- Methanol HandlingDokument46 SeitenMethanol HandlingManuel GuerreroNoch keine Bewertungen

- R S Sisodia PDFDokument42 SeitenR S Sisodia PDFDebatosh RoyNoch keine Bewertungen

- China Vs India: Human Capital: Washington J. Wuttke April 2006Dokument26 SeitenChina Vs India: Human Capital: Washington J. Wuttke April 2006PanvelNoch keine Bewertungen

- Cement and Steel in UAE - Dubai Chamber of CommerceDokument28 SeitenCement and Steel in UAE - Dubai Chamber of Commercesonia87Noch keine Bewertungen

- Group - 26: Presented byDokument23 SeitenGroup - 26: Presented byHetvi KhyaliNoch keine Bewertungen

- Supplimentary Paper 2 - Set BDokument15 SeitenSupplimentary Paper 2 - Set BcynaiduNoch keine Bewertungen

- Review of The Green Ammonia ProcessDokument5 SeitenReview of The Green Ammonia ProcessBrendan JonesNoch keine Bewertungen

- Tehnički Pregled Auta Na PlinDokument196 SeitenTehnički Pregled Auta Na PlinMario ŠestanjNoch keine Bewertungen

- UNI200 Brochure Medium Rev7aDokument6 SeitenUNI200 Brochure Medium Rev7aandy131078Noch keine Bewertungen

- Siemens in Western AustraliaDokument24 SeitenSiemens in Western AustraliasstrattonNoch keine Bewertungen

- The Oil and Gas Industry: NRGI ReaderDokument5 SeitenThe Oil and Gas Industry: NRGI ReaderFaisal ShafiqNoch keine Bewertungen

- Equation C-2b (HHV) Calculation SpreadsheetDokument6 SeitenEquation C-2b (HHV) Calculation SpreadsheetabcNoch keine Bewertungen

- Factors Affecting Coke Rate in A Blast Furnace - Ispatguru PDFDokument3 SeitenFactors Affecting Coke Rate in A Blast Furnace - Ispatguru PDFWallisson Mendes OsiasNoch keine Bewertungen

- Boiler Operation HassanDokument219 SeitenBoiler Operation HassanAhmad Tahir100% (3)

- Group C Presentation - Petrochemicals (UPDATED)Dokument52 SeitenGroup C Presentation - Petrochemicals (UPDATED)sunliasNoch keine Bewertungen

- Pakistan Petroleum LimitedDokument11 SeitenPakistan Petroleum Limitedmuazzamjani101100% (1)

- Examination Board of Boilers: Instructions To Candidates.Dokument9 SeitenExamination Board of Boilers: Instructions To Candidates.9766224189Noch keine Bewertungen

- Overview of Gas-Handling FacilitiesDokument6 SeitenOverview of Gas-Handling FacilitiesMatthew AdeyinkaNoch keine Bewertungen

- Diesel-To-Natural Gas Engine Conversions A Cost Effective AlternativeDokument14 SeitenDiesel-To-Natural Gas Engine Conversions A Cost Effective AlternativeFahmi KurniawanNoch keine Bewertungen

- Methanol Synthesis From Biogas A Thermodynamic AnalysisDokument12 SeitenMethanol Synthesis From Biogas A Thermodynamic AnalysisOmar Duvan RodriguezNoch keine Bewertungen

- 11 Readings 2Dokument5 Seiten11 Readings 2peejay gallatoNoch keine Bewertungen

- Power Plant-Gas Turbine BasedDokument15 SeitenPower Plant-Gas Turbine BasedmandhirNoch keine Bewertungen

- LNG Process Units 200904Dokument19 SeitenLNG Process Units 200904avijitb94% (18)

- Twin SealDokument29 SeitenTwin SealJefferson De Sousa Oliveira100% (1)

- ERP Part 1 (10%)Dokument37 SeitenERP Part 1 (10%)simi263100% (1)

- Refinery Bongaigaon PDFDokument15 SeitenRefinery Bongaigaon PDFBharat GogoiNoch keine Bewertungen

- Pipelines: Types and ApplicationsDokument3 SeitenPipelines: Types and ApplicationsStanley Scott ArroyoNoch keine Bewertungen

- Role of Production Engineering in Field DevelopmentDokument25 SeitenRole of Production Engineering in Field DevelopmentAbdalla Magdy Darwish100% (1)

- Evaluation of Chemical Kinetic Mechanisms For Methane Combustion: A Review From A CFD PerspectiveDokument31 SeitenEvaluation of Chemical Kinetic Mechanisms For Methane Combustion: A Review From A CFD PerspectiveEduardoNoch keine Bewertungen

- Barriers To Biogas Dissemination in IndiaDokument10 SeitenBarriers To Biogas Dissemination in IndiaJeyannathann KarunanithiNoch keine Bewertungen

- Secondary RecoveryDokument8 SeitenSecondary RecoverySaeikh Z. HassanNoch keine Bewertungen

- Lingga, Chapter 11 From Indonesia Post Pandemic Outlook Energy FINALDokument27 SeitenLingga, Chapter 11 From Indonesia Post Pandemic Outlook Energy FINALaurizaNoch keine Bewertungen

- Achyar Sutachyar, S.STDokument18 SeitenAchyar Sutachyar, S.STAndi Priyo JatmikoNoch keine Bewertungen

- Azerbaijan Energy Mix: Total Primary Energy Supply (TPES), 2015Dokument1 SeiteAzerbaijan Energy Mix: Total Primary Energy Supply (TPES), 2015adams abdallaNoch keine Bewertungen

- Malampaya Case StudyDokument15 SeitenMalampaya Case StudyMark Kenneth ValerioNoch keine Bewertungen